The newly appointed Federal Reserve Chair, Volcker, is viewed as a hawk on balance sheet reduction, fueling sustained market anxiety. However, Bank of America stated bluntly that Volcker has extremely limited room to maneuver—both in terms of scale and composition—with virtually zero direct market impact. The real breakthrough may lie in a mechanism reform largely overlooked by mainstream discourse: aligning the standing repo rate for banks with the interest rate on reserve balances.

Market concerns about newly appointed Federal Reserve Chair Kevin Warsh aggressively shrinking the balance sheet may significantly overstate what he can actually accomplish.

Warsh was formally confirmed by the Senate as Federal Reserve Chair. Given his long-standing criticism of the Fed's bloated balance sheet, markets widely fear he will swiftly push for large-scale quantitative tightening. However, in a research report released on May 18, Bank of America interest rate strategists Mark Cabana and Katie Craig stated bluntly that, whether measured by scale or composition, Warsh has extremely limited room to meaningfully adjust the balance sheet, and its direct market impact is expected to be nearly zero.

Bank of America’s core assessment is that the Federal Reserve completed the normalization of quantitative tightening in Q4 2025. Further balance sheet reduction would require shrinking one of three key liabilities: currency in circulation, the Treasury General Account (TGA), or reserves. Of these, only reserves are realistically within Warsh’s operational control—offering limited pathways and a slow pace.

Bank of America’s core assessment is that the Federal Reserve completed the normalization of quantitative tightening in Q4 2025. Further balance sheet reduction would require shrinking one of three key liabilities: currency in circulation, the Treasury General Account (TGA), or reserves. Of these, only reserves are realistically within Warsh’s operational control—offering limited pathways and a slow pace.

Regarding asset composition, the reinvestment arrangements for agency mortgage-backed securities (MBS) are already underway and fully priced into markets. Meanwhile, any compression effect on the weighted average maturity (WAM) of Treasuries is largely offset by market mechanisms, rendering its net impact close to zero. Neither factor tightens financial conditions nor signals an impending rate cut.

The report also outlines a scenario not yet widely considered by mainstream markets: setting the Standing Repo Facility (SRF) rate equal to the Interest on Reserve Balances (IORB) rate, combined with reduced disclosure requirements to mitigate stigma effects, could more effectively reduce banks’ demand for reserves—and thereby create genuinely actionable room for balance sheet runoff. Bank of America believes this approach could have a greater practical impact than conventional market expectations regarding Warsh’s balance sheet reduction path.

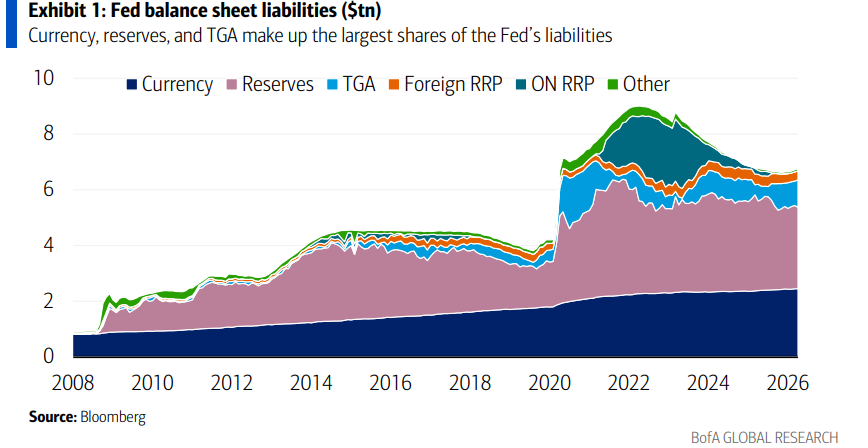

The Constraint of Scale: Three Liabilities, Only Reserves Are Adjustable

Following the completion of quantitative tightening normalization, the Federal Reserve’s balance sheet stands at approximately $6.78 trillion, driven by liabilities on the balance sheet. The three core liability components are: reserves (approximately $3.12 trillion, or 46%), currency in circulation (approximately $2.46 trillion, or 36%), and the Treasury General Account (TGA) (approximately $807 billion, or 12%).

Currency in circulation is regarded by the central bank as an 'exogenous' liability beyond the reach of monetary policy tools. Bank of America notes that, in theory, it could be reduced by eliminating high-denomination banknotes—but adds that 'this will not happen in the United States.'

On the TGA front, the U.S. Treasury has clearly indicated it has no intention to shrink the account, projecting that the TGA will rise to $900 billion by the end of Q2 2025 and further increase to $950 billion by the end of Q3 2025.

Bank of America acknowledges that marginal adjustments to the TGA via repo investments are possible but would have minimal impact; adjustments through the Treasury Tax and Loan (TT&L) channel are deemed 'highly unlikely.'

Reserves represent the most realistic option for Waller to shrink the balance sheet, but each pathway faces constraints.

"Bank-unfriendly" approaches—such as imposing reserve caps or implementing tiered interest rates—would compress bank liquidity and weaken market-making and lending incentives, thereby weighing on the economy. Bank of America believes Waller is unlikely to adopt such measures.

The 'bank-friendly' approach involves easing regulations and allowing banks to pre-pledge collateral at the discount window to expand their holdings of high-quality liquid assets (HQLA), thereby reducing reserve requirements.

Bank of America estimates this approach could ultimately reduce reserves by approximately $200 billion to $500 billion, though the process would be gradual and, since it would not tighten financial conditions, would not constitute grounds for rate cuts.

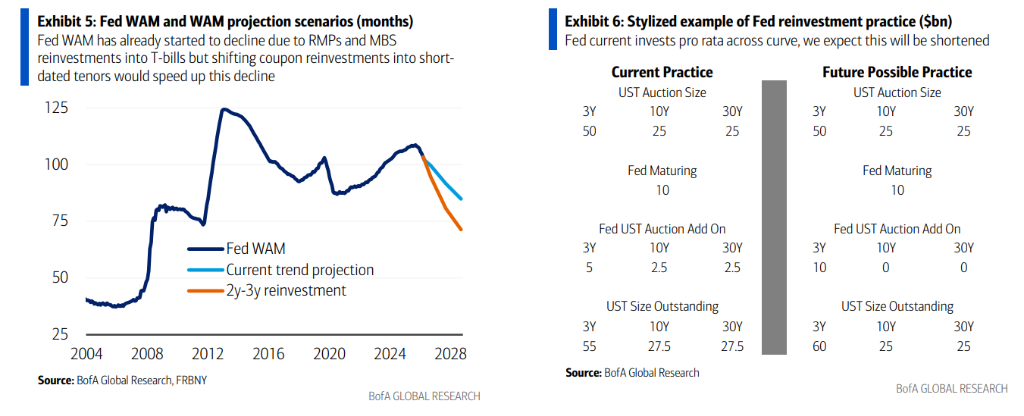

Portfolio Rebalancing: The impact of WAM compression is neutralized by offsetting mechanisms.

At the portfolio composition level, Waller’s room for maneuver is similarly constrained by institutional mechanisms.

The Federal Reserve currently holds approximately $1.98 trillion in agency mortgage-backed securities (MBS) and is gradually reducing this position at a pace of $10–20 billion per month by allowing maturing and prepaid MBS to roll off and reinvesting the proceeds into Treasury bills.

Bank of America considers outright MBS sales highly unlikely (unless directly repurchased by Fannie Mae or Freddie Mac—a scenario deemed low-probability). The current approach is already fully priced into markets and thus poses no new disruption.

Shortening the weighted average maturity (WAM) of the Treasury portfolio is another key focus area.

Waller could accelerate WAM compression by shifting reinvestment of maturing Treasury coupon payments—currently allocated proportionally across maturities—to concentrate instead in the short end (e.g., 2- to 3-year Treasuries). However, the Fed’s reinvestment process uses an auction 'add-on' mechanism, which directly increases the stock of short-term Treasuries rather than replacing longer-dated securities.

This raises a critical question: Will the Treasury Department offset the Fed’s shortening of the weighted average maturity (WAM) by adjusting its debt issuance structure? Bank of America answers in the negative. If this assessment holds true, the actual impact of the Fed’s WAM compression on the overall Treasury market and financial conditions would be zero, leaving Walsh with no logical basis to advocate for rate cuts on this ground.

Ample Reserves: Walsh Neither Has the Will nor the Ability to Change Course

In Bank of America’s view, the most critical question regarding Walsh is whether he would support an 'ample' or a 'scarce' reserve regime. Bank of America’s answer is: ample—and with very high certainty.

The advantages of an ample reserves regime lie in its operational simplicity, ensuring sufficient liquidity in the banking system, dampening money market volatility, and supporting relatively accommodative financial conditions—at the cost of only a modestly larger balance sheet. By contrast, while a scarce reserves regime could further shrink the balance sheet, it would entail substantial risks, including heightened money market volatility and liquidity pressures.

Bank of America offers two supporting arguments. First, Trump places far greater emphasis on accommodative financial conditions than on the size of the Federal Reserve’s balance sheet, and Walsh is expected to remain receptive to this policy preference.

Second, the Federal Reserve formally adopted the ample reserves regime in 2019, and the current leadership unanimously supports it, with some officials expressing particularly strong views—Bank of America cites Federal Reserve Governor Waller’s remarks in a February 2026 speech: 'You don’t want banks looking under their couch cushions every night for cash... That’s extremely inefficient—and extremely stupid.' Bank of America specifically highlighted the last word in its report.

Bank of America believes that Walsh is not only subjectively inclined toward the ample regime but will also be constrained objectively by the Fed’s internal consensus.

SRP=IOR Mechanism May Be the Real Game-Changer

In its report, Bank of America proposes a mechanism reform that goes beyond conventional frameworks, drawing from prior statements by Dallas Fed President Logan: setting the Standing Repo Facility rate (SRP) equal to the Interest on Reserve Balances rate (IORB).

The specific design entails allowing banks to pledge Treasury or agency securities to the Fed around the clock in exchange for cash at a rate equal to the interest paid on their reserve balances. The facility would operate similarly to the discount window but would be open continuously, without discrete operational time windows.

Because the interest rate is competitive and carries no premium, banks are more willing to use it, thereby reducing their demand for precautionary reserve buffers and creating operational room for the Federal Reserve to shrink its balance sheet. The Bank of England currently employs a similar mechanism.

To further enhance its effectiveness, Bank of America recommends accompanying this with reforms to disclosure practices, specifically including the elimination of the current weekly report that discloses reserve distributions by region. Market participants currently use this report to track institutions potentially facing liquidity stress; removing it would effectively reduce the 'stigma' associated with using the Standing Repo Facility (SRP), making banks more willing to draw on the facility when needed rather than hoarding excessive reserves.

The report also notes that the SRP for banks should be differentiated from that for dealers: the dealer SRP rate should be set approximately 5 to 10 basis points higher than the bank SRP rate to ensure banks remain incentivized to lend in the repo market while preserving pricing space for open-market transactions.

Bank of America concludes that aligning the bank SRP rate with the Interest on Reserves (IOR) rate, combined with reforms to reporting practices, could substantially lower banks’ reserve demand and thus provide a genuinely viable path for Waller to shrink the balance sheet. Although this proposal has not yet entered mainstream market discussions, Bank of America expects it will eventually attract significant attention—its impact potentially far exceeding current market estimates of Waller’s capacity to conduct balance sheet reduction.

Editor/Deng