Bernstein's 97-page in-depth report: AI data center connectivity, not compute power, has become the new bottleneck; copper and optical interconnects will coexist long-term; CPO adoption is clear in direction but large-scale deployment unlikely before 2028; more certain earnings in 2026 are expected in PCB, ABF, and LPO/NPO segments.

Bernstein’s latest 97-page in-depth report states that copper and optical interconnects in AI data centers are not mutually substitutable but will coexist over the long term in both vertical and horizontal scaling scenarios. Although co-packaged optics (CPO) offers advantages in power consumption and cost, manufacturing and maintenance challenges hinder its widespread deployment, making large-scale adoption unlikely before 2028. Thus, linear-drive pluggable optics (LPO)/non-pluggable optics (NPO) may emerge as leaders during this transitional period. However, CPO is fundamentally reshaping the value chain, shifting profit centers away from traditional optical module suppliers toward chip designers, advanced packaging providers, and system integrators.

It is important to note that Bernstein (officially Sanford C. Bernstein) is a globally recognized investment research and asset management firm headquartered in the United States. Founded in 1967, it is now part of AllianceBernstein (AB), one of the world’s leading global asset managers. Bernstein is also among the largest and oldest independent sell-side research institutions. Below is a detailed breakdown of Bernstein’s report.

The Bernstein report focuses on three core aspects: (1) Why has connectivity replaced compute as the new bottleneck? (2) What is the timeline for CPO commercialization? (3) Why are PCB/ABF substrates a more realistic near-term earnings driver for 2026?

The Bernstein report focuses on three core aspects: (1) Why has connectivity replaced compute as the new bottleneck? (2) What is the timeline for CPO commercialization? (3) Why are PCB/ABF substrates a more realistic near-term earnings driver for 2026?

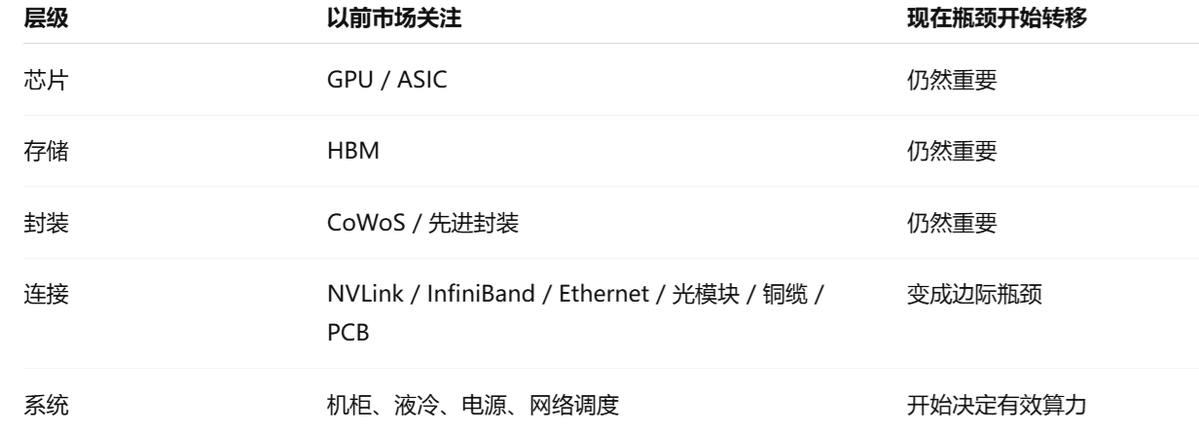

What the report truly emphasizes is not that 'CPO is about to explode,' but rather that bottlenecks in AI data centers are shifting further downstream—from GPUs, HBM, and CoWoS—toward the 'interconnect system.' The future investment theme is not CPO alone, but a coordinated upgrade across optical, electrical, copper, boards, packaging, and testing.

More plainly: in the past, the market viewed AI primarily through the lens of GPU compute power.

Now, the market is starting to focus on how GPUs are interconnected.

In the future, the key question will be whether compute utilization can be unlocked by the interconnect system.

This is precisely what the report’s title refers to as the 'War for AI Data Center Connectivity.'

I. Why Has 'Connectivity' Become the New Bottleneck for AI Data Centers?

An AI cluster is not simply a matter of stacking GPUs together. The real challenge lies in the fact that these GPUs must synchronize at high speed, exchange parameters, transmit activation values, perform AllReduce operations, and support both model parallelism and data parallelism. No matter how powerful the theoretical compute capacity is, actual utilization will drop if inter-GPU communication cannot keep up.

An AI cluster can be thought of as a massive factory:

Why has connectivity replaced compute capacity as the new bottleneck?

The root of this issue lies in how large models are trained. There are two primary parallelization methods used in large model training: tensor parallelism and expert parallelism. Both approaches share a key characteristic—they require frequent, large-scale data exchanges between GPUs.

The volume of data exchanged between GPUs during a single training run is astronomical. What does this mean? In the past, simply increasing the number of GPUs was sufficient. Now, the more GPUs you add, the greater the communication overhead between them becomes. Beyond a certain threshold, adding more GPUs no longer accelerates training—in fact, it exacerbates communication congestion. This is the connectivity bottleneck.

Bernstein provided a comparison: inside a standard NVIDIA GB30 rack, GPUs are interconnected using copper cables because the short distances make copper cost-effective and reliable. However, inter-rack connections must use fiber optics, as copper cables suffer unacceptable signal attenuation beyond two meters. Fiber optic links require optical transceivers at both ends to convert electrical signals into optical signals and back again.

Herein lies the problem: a 1.6T optical transceiver consumes approximately 30 watts of power, with the majority consumed by a digital signal processor (DSP) chip. With hundreds of such transceivers in a single rack, the power consumption attributable solely to communications becomes difficult to reduce.

Thus, the real challenge facing today’s AI data centers is not insufficient compute capacity or hitting power limits. NVIDIA itself states that its next-generation CPU-based switches can reduce power consumption by 70% compared to traditional optical transceivers. For a 51.2T switch, this translates into a 500-watt saving—power that can instead be allocated to additional GPUs.

$NVIDIA(NVDA.US)$NVIDIA is also reinforcing this narrative. In March 2025, NVIDIA launched Spectrum-X Photonics and Quantum-X silicon photonics switches, emphasizing that they are designed to connect millions of GPUs within AI factories while reducing energy consumption and operational costs. NVIDIA claims its photonics switches deliver 1.6 terabits per second per port, a 3.5x improvement in energy efficiency, a 63x enhancement in signal integrity, and a 10x increase in network resilience.

The underlying logic of this Bernstein report is that the next phase of AI capital expenditure will not simply involve purchasing more GPUs, but rather investing in greater 'interconnect capabilities that enable GPUs to work effectively.'

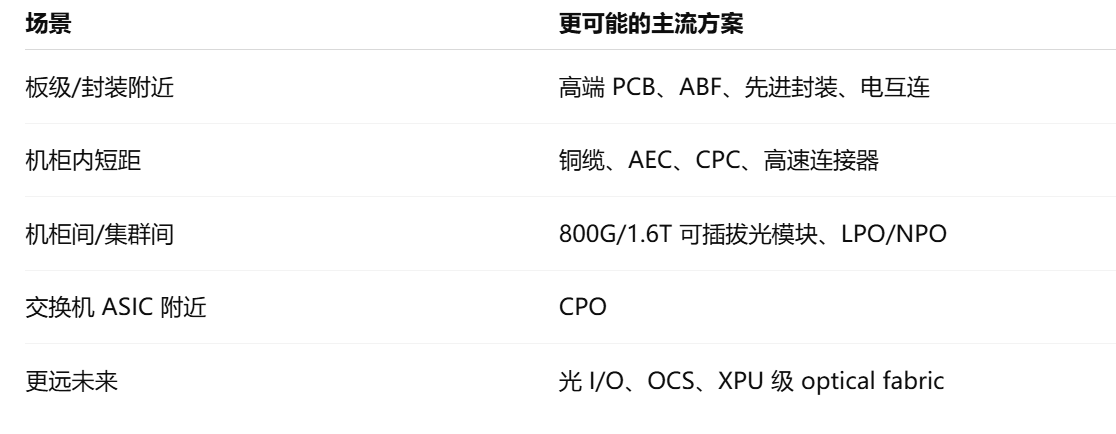

II. The report's core thesis: It is not a case of 'copper out, optical in,' but rather 'coexistence across multiple pathways.'

There is often a simplistic narrative in the market: 'optical in, copper out.'

However, the report offers a more nuanced view: copper and optical interconnects are not in a simple substitution relationship; instead, they will coexist over the long term under different conditions—such as transmission distance, bandwidth requirements, maintenance needs, and cost structures. Bernstein argues that copper and optical interconnects are not direct substitutes but will evolve separately in scale-up and scale-out scenarios. This assessment is critically important.

1. Scale-up: Copper remains strong for intra-rack/short-reach interconnects

Scale-up refers more closely to high-speed interconnects between GPU-to-GPU, GPU-to-switch, and within or near a rack. Key priorities in this context include:

Low latency, low cost, high reliability, serviceability, and short-distance transmission capability.

In this scenario, copper is far from obsolete.

Jensen Huang has also explicitly stated previously:$NVIDIA(NVDA.US)$NVIDIA will not immediately adopt co-packaged optics (CPO) for primary interconnects between flagship GPUs, as traditional copper connections are currently far more reliable than CPO-based optical links. NVIDIA plans to first deploy CPO in two new networking chips used in top-of-rack switches.

This statement is critically important. It clarifies that CPO represents a direction, but not an immediate, wholesale replacement of copper.

In other words, at least at this stage, NVIDIA’s logic is:

CPO can be adopted first on the switch side, while adoption on the GPU/XPU side should proceed more cautiously.

The reason is simple: GPUs are the most expensive and critical assets in the system. You cannot compromise reliability simply for the sake of optical interconnect energy savings. In an AI training cluster, frequent link disconnections result in losses far beyond hardware costs—training jobs are interrupted, GPU utilization drops, and scheduling complexity increases.

2. Scale-out: Optical interconnects hold a stronger advantage for inter-rack and inter-cluster connectivity

Scale-out refers to expanding GPU clusters across larger scales, typically involving east-west traffic over longer distances between racks or within a data center.

In this scenario, optical solutions demonstrate clearer advantages:

longer reach, higher bandwidth, lighter cabling, lower power consumption, and better cable density.

Therefore, the future will not involve 'a complete replacement of copper by optics,' but rather:

The greatest value of Bernstein’s report lies in the fact that it goes beyond the level of 'CPO concept stocks' and instead breaks down AI connectivity into multiple technological pathways.

III. CPO: Direction Matters, but 2026 Is Not the Year of Full-Scale Adoption

The part of this report most prone to misinterpretation by the market is CPO.

Many people see 'CPO' and immediately draw the conclusion:

Optical modules will be replaced; CPO will explode immediately; traditional optical module manufacturers are doomed.

This understanding is overly simplistic.

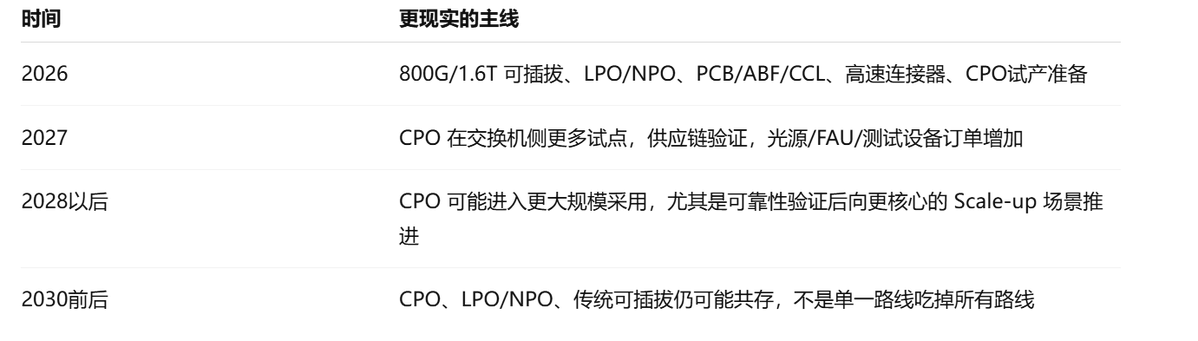

Bernstein expects limited-scale deployment of CPO in scale-out networks could begin in the second half of 2026, primarily to validate real-world performance and supply chain maturity. However, adoption in the more critical scale-up scenarios may be delayed until late 2028 or beyond, as the industry must first verify the long-term reliability of switch-side CPO before deploying it in higher-value, less fault-tolerant XPU systems.

This aligns with Jensen Huang’s earlier statements: CPO will initially be used for network switching chips rather than being rapidly deployed at scale in primary GPU interconnects.

Thus, the timeline should be understood as follows:

LightCounting’s view also supports a ‘gradual evolution’ rather than an ‘overnight switch.’ It forecasts that traditional retimed pluggables will remain dominant over the next five years, although LPO/CPO will account for a significant share of 800G and 1.6T ports between 2026 and 2028. EDN’s summary of industry perspectives also notes that Yole anticipates large-scale CPO deployment occurring between 2028 and 2030, while LightCounting believes optical modules will still constitute the majority of data center optical links within this decade, albeit with optical components continuously moving closer to ASICs.

Therefore, my assessment is:

CPO represents a medium- to long-term direction, but more certain revenue in 2026 may not necessarily come from the purest CPO-related stocks. Instead, it will likely emerge from components that must be upgraded ahead of the CPO inflection point—such as light sources, testing, packaging, PCBs, ABF, CCL, 1.6T optical modules, and LPO/NPO.

4. LPO/NPO: They are the 'transitional main theme' preceding the CPO boom.

A key aspect of this report is that it does not simplistically divide technological pathways into 'traditional optical modules vs. CPO.'

LPO and NPO also exist in between.

1. What is LPO?

LPO stands for Linear Pluggable Optics. Broadly speaking, it retains the pluggable form factor but removes or minimizes the DSP (digital signal processor), using linear drivers and host-side equalization to reduce power consumption.

Its advantages include lower power consumption, potentially lower cost, and retention of a degree of maintainability.

Its drawbacks include greater system tuning complexity, tighter link budget constraints, and higher requirements for host-side SerDes and overall system engineering.

The public abstract notes that by eliminating the DSP and offloading signal processing to linear components, LPO can significantly reduce power consumption compared to traditional pluggable modules while preserving modular maintenance convenience; Bernstein even suggests that LPO shipments could surpass those of CPO by 2030.

2. What is NPO?

NPO can be understood as Near-Packaged Optics, which places the optical engine closer to the ASIC but not fully integrated into the same package as in CPO.

Its value lies in striking a balance:

This suggests that over the next few years, the industry will likely not move directly to CPO, but rather follow this progression: traditional pluggable modules → LPO/NPO → CPO → optical I/O / optical fabric.

This is also why, in 2026, you cannot focus solely on CPO. The companies most likely to deliver tangible results may be those capable of supplying across multiple technological stages.

In summary, the CPO narrative will not materialize in 2026. CPO will only begin limited-volume shipments in the second half of 2026, exclusively for scale-out scenarios—widespread deployment across racks will not occur until 2028.

Why is adoption so slow? Bernstein cites three reasons:

First, cloud service providers are reluctant to abandon traditional optical modules. If an issue arises, operations teams can simply unplug and replace the module within minutes. In contrast, CPUs are soldered onto switches; if an optical engine fails, the entire switch must be returned to the factory for repair—a significant downtime and operational cost burden for these cloud providers.$Amazon(AMZN.US)$、Google-A (GOOGL.US)、Microsoft (MSFT.US)Moreover, optical modules have a non-negligible failure rate. Industry standards specify one failure per 100,000 hours of operation, which translates to approximately nine failures per year for every 10,000 modules—this accounts only for hard failures, excluding soft failures.

CPO integrates the optical engine directly into the chip package, requiring reliability improvements by several orders of magnitude before cloud providers will feel confident adopting it. Bernstein explicitly stated that in discussions with Zhongji Xuchuang, a Chinese optical module manufacturer, the company confirmed that none of its cloud service provider customers plan to deploy CPO at scale between 2026 and 2027—a critical point the market may not yet have fully absorbed.

The second reason is that transitional solutions have already emerged—CPO is not the only option. Two intermediate technologies exist: LPO and NPO. LPO removes the most power-hungry component in optical modules—the DSP chip—and replaces it with simpler circuitry. This reduces power consumption to one-third that of traditional optical modules while retaining pluggability. 800G LPO modules are already in mass production.

NPO places the optical engine on the PCB adjacent to the switch chip, but it remains removable. NVIDIA’s current product labeled as a CPU is, strictly speaking, one of these two transitional NPO solutions, which are expected to last for two to three years. Therefore, cloud service providers have every reason to say they will use LPUs for now and wait until CPO truly matures.

The third reason is that in scale-up scenarios—where connections between GPUs are referred to as 'scale-up'—copper cables are still very much alive. Their cost and reliability advantages currently have no viable alternatives.

Bernstein explicitly stated that from 2026 to 2028, copper cables will continue to dominate scale-up applications, benefiting Luxshare Precision. The company is directly competing with Amphenol in supplying copper cable connectors for NVIDIA’s GP300. Additionally, there is a transitional technology called CPC (Co-Packaged Copper), which further extends the lifecycle of copper cabling.

LightCounting, an industry consulting firm, forecasts that by 2029, copper cables will still account for nearly half of the 1.6T interconnect market.

V. The Greatest Impact of CPO: Not Simply Cost Reduction, but a Reallocation of the Profit Pool

The industrial significance of CPO lies not merely in energy efficiency or simply replacing optical modules.

What it truly changes is where profits are generated.

In the era of traditional pluggable optical modules, the value chain was roughly structured as follows: DSP / optical chips / TOSA/ROSA / module packaging / optical module manufacturers / switch vendors / cloud providers.

In the CPO era, it will evolve into: Switch ASIC / optical engines / external laser sources / FAU / advanced packaging / wafer fabrication / testing / system integration.

Bernstein conducted a cost breakdown of NVIDIA’s Quantum-X800 CPO switch: this switch is configured with four switch ASICs, each integrating 18 optical engines and connected to 18 external laser source modules. The estimated unit cost of a single Quantum-X800 CPO switch is approximately USD 570,000. The analysis also noted that under the CPO architecture, the DSP is eliminated, and the optical engines are co-packaged with the switch chip, shifting value creation toward chip design, advanced packaging, and wafer manufacturing.

This is why the report is bullish on these areas:

Relatively speaking, traditional optical module manufacturers face a challenge: if value shifts from module packaging to ASICs, packaging, optical engines, and system integration, their profit pools could be restructured.

However, this does not mean traditional optical module vendors will immediately become irrelevant. Between 2026 and 2028, there will still be substantial demand for 800G, 1.6T, and LPO/NPO solutions. CignalAI also notes that high-speed datacom modules—particularly 800GbE and emerging 1.6TbE designs—will remain the primary growth drivers in 2026.

Therefore, the correct interpretation is: CPO will reshape profit allocation across the optical module supply chain, but it will not eliminate pluggable optical modules outright by 2026.

VI. Why does the report emphasize PCBs, ABF, and CCL as more realistic opportunities for 2026?

This is, in my view, the most noteworthy point.

CPO has significant long-term potential, but its commercial realization timeline is relatively distant. In contrast, upgrades in PCBs, ABF, and CCL are much closer to near-term orders.

The reason is simple: even though CPO has not yet reached large-scale commercialization, AI servers and switches are already undergoing upgrades.

Rubin, Rubin Ultra, GB300, cloud providers’ ASICs, and next-generation switch ASICs are all driving higher requirements for board-level data rates, package footprint, power density, signal integrity, thermal management, and low-loss materials.

This is the most contrarian—and yet most overlooked—insight in the report. The real winners in 2026 will come from the established, cash-generative segment of PCBs, HDI, ABF, and substrates.

Why is this considered contrarian? Because this sector is too traditional. Printed circuit boards (PCBs) have been around for decades, and the global market is projected to reach $85 billion in 2025—hardly an exciting figure. Everyone is focused on co-packaged optics (CPO), optical modules, and NVIDIA, with no one willing to spend time researching PCBs. However, Bernstein’s data shows that this sector has quietly taken off in 2025.

Bernstein provided a set of figures: $Shenghong Technology(02476.HK)$ for HDI (high-density interconnect) PCB manufacturers, revenue grew 63% year-over-year in 2025. Wus Printed Circuit (Shanghai) Co., Ltd. reported a 45% revenue increase. These are actual, realized performance results—not projections or expectations, but fulfilled outcomes. Why is this sector rallying? There are three dimensions to consider:

First, AI servers have doubled the PCB content per unit. In the past, an NVIDIA H100 server—with 80 GPUs—had a total HDI plus PCB value of approximately $100–$150 per GPU. With the new GB200 VL72 rack system, this figure has jumped directly to $300 per GPU. What does this mean? For every GPU sold, PCB manufacturers now earn twice as much.

And that’s not all. The upcoming Vera Rubin platform will adopt a new structure called a midplane, replacing parts previously connected with copper cables with multilayer PCBs. This midplane uses a 44-layer board made with top-tier M8-grade copper-clad laminate. In the next-generation Rubin Ultra, it may even reach 78 layers using M9-grade materials. Doubling the layer count and upgrading materials doubles the value again.

Second, upstream materials are creating bottlenecks. A critical material used in ABF substrates is T-glass—a low coefficient of thermal expansion (CTE) glass fiber—designed to prevent substrate warping under high temperatures, which could otherwise cause solder joint failures in AI chips.

Currently, only one company globally can produce T-glass at the highest specification: Nittobo, with a CTE of 2.8%. Other manufacturers cannot achieve this level. Nittobo’s new capacity won’t come online until late 2026, and volume shipments won’t begin until 2027, meaning T-glass will remain in short supply throughout 2026.

What does T-glass shortage mean? It gives ABF substrate makers a legitimate reason to raise prices. Unimicron has already renegotiated pricing with its customers. Bernstein’s model forecasts that the average selling price (ASP) of ABF substrates will increase by 5% to 7% quarter-over-quarter in 2026, resulting in a cumulative annual increase of over 20%.

The third layer involves the hidden monopolist of ABF film. ABF film is one of the core materials used in ABF substrates. The inventor of this material is Ajinomoto, $Ajinomoto (2802.JP)$ the same Japanese food company known for producing monosodium glutamate (MSG). During MSG research and development in the 1990s, they accidentally discovered a special amino acid-derived thin film suitable as a thermal expansion layer in semiconductor substrates. Since then, 95% of the world’s ABF film has come from Ajinomoto.

According to Bernstein, Ajinomoto’s ABF business boasts a 60% gross margin, grew by 32% in fiscal year 2026, and is expected to accelerate to 45% growth in fiscal year 2027. No competitor has been able to challenge this business in 30 years.

Therefore, what is more certain for 2026 is not the 'overnight breakout of CPO,' but rather:

High-speed PCBs need upgrading; ABF substrates need upgrading; CCL must be upgraded to lower-loss materials; copper foil, glass fiber cloth, and low-Dk/low-Df materials require upgrades; testing and validation processes must also be enhanced.

Thus, a more realistic strategy for 2026 is to first focus on three areas of certainty: optical demand driven by the transition to 1.6T and LPO/NPO; PCB/ABF/CCL upgrades spurred by Rubin/ASIC adoption; and investments in testing, FAUs, light sources, and advanced packaging that are essential prior to CPO pilot production.

Because capital markets often make one key mistake:

They prefer to invest in the most distant concepts, yet the entities that actually generate early revenues are typically those building the infrastructure required before these long-term concepts can materialize.

CPO is like a future high-speed rail station.

But before the high-speed rail station becomes fully operational, the early profits are likely to go to those involved in road construction, track laying, power supply, signaling systems, and inspection equipment.

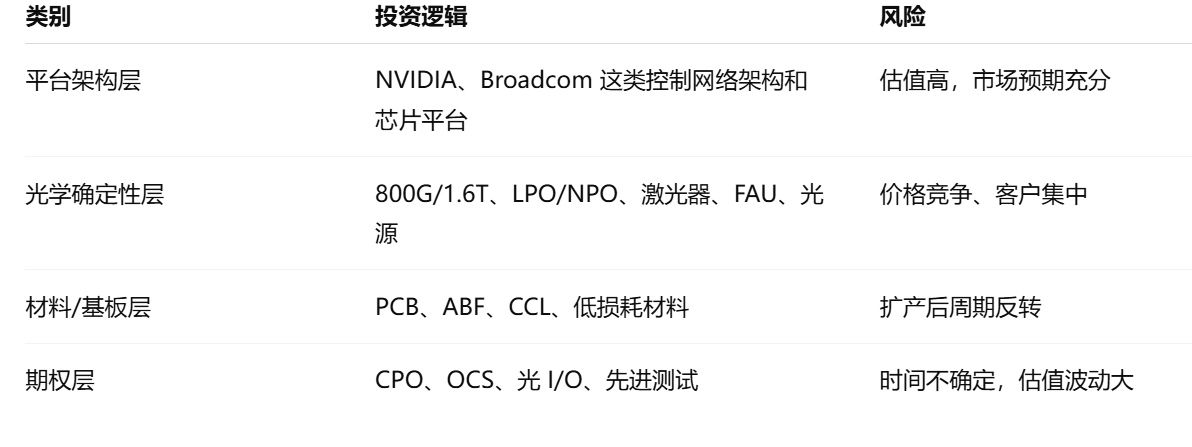

VII. Beneficiary Sequence in the Supply Chain Outlined in This Report

If the AI interconnect supply chain is divided into four layers:

1. Tier 1: The strongest platform-level winners

These companies do not merely sell a single component; they control the architecture.

NVIDIA's advantage lies not only in GPUs, but in the combination of GPU + NVLink + InfiniBand + Ethernet + Spectrum-X + Quantum-X + software ecosystem. NVIDIA's officially disclosed silicon photonics networking switches have already integratedTaiwan Semiconductor (TSM.US)、$Coherent (COHR.US)$、Corning (GLW.US) 、$Fabrinet(FN.US)$、$Lumentum(LITE.US)$、$Sanko Group (9069.JP)$, SPIL, Sumitomo Electric Industries (5802.JP), TFC Communication, and others into its ecosystem.

This indicates that$NVIDIA(NVDA.US)$it is engaged in one overarching initiative:

It is not just selling GPUs, but also bringing the network architecture of AI factories under its platform control.

(2)Taiwan Semiconductor (TSM.US)

It is the invisible hub of this entire narrative.

The Co-Packaged Optics (CPO) platform integrates electronic and photonic chips using hybrid bonding technology. All major clients—NVIDIA, Broadcom, and AI labs—are migrating to Taiwan Semiconductor. While this company does not generate substantial revenue directly from CPO itself, CPO significantly reinforces Taiwan Semiconductor’s dominance in advanced packaging and wafer foundry services.

Broadcom follows a different logic. Its approach resembles: Ethernet switch ASIC + custom ASIC + CPO + a cloud provider-customized chip ecosystem.

$Broadcom (AVGO.US)$In October 2025, it announced Tomahawk 6 Davisson, its third-generation CPO Ethernet switch, featuring 102.4 Tbps switching capacity, and stated that volume shipments have already begun. Broadcom claims that by integrating Taiwan Semiconductor’s COUPE optical engine and advanced multi-chip packaging, it has reduced optical interconnect power consumption by 70%, while supporting scale-up for 512 XPUs and over 100,000 XPUs in a two-tier network.

This highlights that Taiwan Semiconductor and Broadcom are critical players—alongside NVIDIA—in the AI networking and CPO value chain.

2. Tier Two: Optical and High-Speed Interconnects with Higher Certainty

This includes: 1.6T optical modules, LPO/NPO, silicon photonics, lasers, external light sources, FAUs, and optical connectors.

Representative directions include$Coherent (COHR.US)$、$Lumentum(LITE.US)$、$Fabrinet(FN.US)$、$Zhongji Xuchuang (300308.SZ)$、$Xinyisheng (300502.SZ)$、$Sanko Group (9069.JP)$、Corning (GLW.US) 、$Sumitomo (8053.JP)$and others. NVIDIA’s official ecosystem list includes multiple companies specializing in optics, packaging, and connectivity.

The focus at this layer is not on 'who resembles a CPO most,' but rather on which companies can simultaneously capture demand across 800G/1.6T, LPO/NPO, CPO pilot production, external light sources, and FAUs. Companies capable of spanning multiple phases have higher odds of success than those tied to a single concept.

3. Third layer: PCBs, ABF, CCL, and materials

This is considered the most likely area to be undervalued by 2026. Public summaries mention that the original report covered or referenced Chroma,$Luxshare Precision Industry (002475.SZ)$, Unimicron,$NVIDIA(NVDA.US)$、$Broadcom (AVGO.US)$、Taiwan Semiconductor (TSM.US)、$Ibiden Co., Ltd. (4062.JP)$and other companies.

Among these, Unimicron and$Ibiden Co., Ltd. (4062.JP)$—substrate/PCB supply chain companies like these warrant close attention, as rising AI server complexity means PCBs and packaging substrates are no longer merely passive components but have become performance constraints themselves.

4. Fourth layer: test equipment, yield, and reliability

The biggest challenge for CPO is not the PPT, but mass production. Mass production must address: optoelectronic coupling yield, stability of external laser sources, reliability in high-temperature environments, packaging stress, on-site maintenance, test duration, consistency, and post-failure repair models.

Therefore, test equipment and reliability validation providers could be excellent 'shovel sellers.' Such companies may not be the most glamorous, but if CPO enters pilot production, they are often the first to see orders.

8. Investment implications of this report: Do not buy the 'most conceptual,' but rather the 'hardest to bypass.'

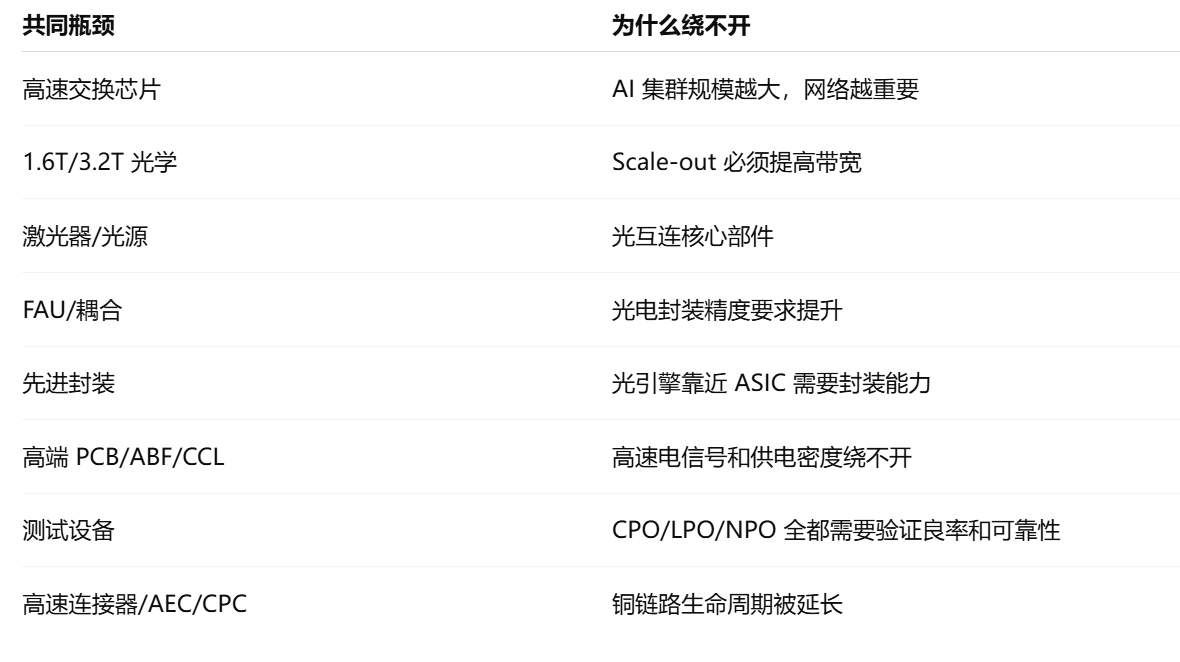

The key investment insight from this report is that AI connectivity is not a single-point technological revolution, but rather a shift in bottlenecks. Investors should focus on shared bottlenecks rather than betting on a single technical pathway.

What constitutes a shared bottleneck? It refers to components or capabilities that cannot be avoided regardless of whether the ultimate solution is CPO, LPO, NPO, or continued upgrades of traditional pluggable modules. Examples include:

In contrast, betting solely on a single pathway carries significant risk. For instance, if you invest only in 'pure CPO concepts,' the risks include delayed mass production timelines, unfulfilled orders, and an initial valuation correction.

Investing only in traditional optical modules carries the risk that CPO/NPO/LPO will restructure the value chain, with long-term profit pools shifting to platform vendors and chip/packaging suppliers.

Investing solely in PCBs/materials carries the risk of customers expanding capacity too quickly, concentrated supply releases, and gross margin reversals.

Thus, a better strategy is: buy certainty in 2026, order-driven upside in 2027, and architectural optionality from 2028 onward.

9. Personal assessment of the reasonableness of this report

Highly reasonable points

First, shifting the AI bottleneck from GPUs to interconnect systems is absolutely the right direction.$NVIDIA(NVDA.US)$、$Broadcom (AVGO.US)$Recent product launches are all validating this point.

Second, challenging the oversimplified narrative of 'copper out, optics in' is a critically important judgment. A Reuters report on Jensen Huang explicitly stated that copper still holds a reliability advantage in short-reach GPU/XPU interconnects in the near term.

Third, the view that co-packaged optics (CPO) is the right direction—but that scalability awaits reliability validation—is also reasonable. Industry assessments from LightCounting and Yole/EDN lean toward 'gradual migration rather than immediate, full-scale replacement.'

Fourth, emphasizing that upstream segments—such as PCBs, ABF substrates, copper-clad laminates (CCL), testing, and optical sources—are more likely to generate tangible revenue by 2026 is particularly valuable for investors. Capital markets often overvalue distant, speculative narratives while undervaluing near-term segments that are already securing real orders.

Points requiring caution

First, public summaries may oversimplify or sensationalize Bernstein’s views—for example, turning them into investment soundbites or clickbait headlines. The phrase 'The real AI battleground isn’t chips—it’s interconnects' is catchy, but strictly speaking, GPUs, HBM, and CoWoS remain core bottlenecks; it’s just that the marginal importance of interconnects has increased—not that chips have become unimportant.

Second, while the value migration toward CPO is correctly identified, its adoption speed may be overestimated by the market. CPO must resolve challenges related to manufacturing, packaging, field maintenance, failure replacement, and reliability—it is not a technology that scales immediately after a product launch.

Third, LPO/NPO solutions offer significant transitional value, but their system-level tuning complexity should not be underestimated. LPO is not simply a 'low-power pluggable' solution; it shifts substantial complexity to the host side and system-level debugging.

Fourth, although the PCB/ABF/CCL segment exhibits strong certainty, one must remain vigilant about capacity expansion cycles. Once materials and substrate industries observe high demand, they tend to expand capacity rapidly; if customer platform deployment subsequently slows, gross margins will suffer a backlash.

10. Over the next two to three years, track developments according to this timeline:

2026: Do not focus solely on CPO—monitor three areas of certainty

The key in 2026 will not be a major CPO breakout, but rather:

Whether 1.6T pluggable optical modules achieve volume production;

Whether LPO/NPO gain additional certifications from cloud providers or switch platforms;

Whether PCB/ABF/CCL continues to experience price increases or capacity expansions;

Whether CPO-related test equipment, FAUs, and external light sources begin receiving actual orders.

If these developments occur, it indicates that the report’s underlying thesis is entering its realization phase.

2027: Observe whether CPO pilots transition from 'prototypes' to 'customer deployments.'

Key indicators are:

Real-world customer deployments of NVIDIA Quantum-X / Spectrum-X Photonics;

Customer adoption expansion of Broadcom Davisson/Tomahawk CPO;

Adoption by CoreWeave, Lambda, Meta, Google, Microsoft, Amazon, and others;

Whether external light sources for CPO, FAUs, and test equipment have entered revenue recognition.

Beyond 2028: Monitor whether CPO enters the scale-up phase.

The most critical inflection points are:

Whether CPO moves from the switch side toward XPU/GPU proximity;

Whether optical I/O is integrated into high-end ASIC/GPU packaging;

Whether OCS/optical fabric begins to reshape data center network topologies.

If we reach this stage, CPO will no longer be merely about optical module replacement but will signify a shift in AI computing architecture.

XI. Investment Framework Based on This Report: Four Asset Classes, Four Rationales

If using this report to guide investments in U.S., Hong Kong, or A-share markets, I would categorize them into four groups.

The strategy I personally favor most is: allocate core positions to platform winners, allocate tactical positions to optical and PCB plays with high certainty, and use a small portion of an options position to bet on the long-term direction of CPO. It is not advisable to allocate all capital upfront to 'pure-play CPO concept stocks.'

XII. The Five Core Takeaways from This Report

First, the bottleneck in AI data centers is shifting from 'computing speed' to 'interconnect speed, reliability, and power efficiency.'

Second, optics will not immediately replace copper, nor will copper retain dominance across all scenarios indefinitely; different distances and system layers will adopt different solutions.

Third, CPO represents the long-term direction, but more realistic revenue opportunities by 2026 lie in 1.6T, LPO/NPO, light sources, testing, PCBs, ABF, and CCL.

Fourth, the true impact of CPO is not to make optical modules cheaper, but to shift the profit pool from traditional module packaging toward chips, packaging, optical engines, light sources, testing, and system platforms.

Fifth, when investing in AI connectivity, focus not on the hottest concepts but on the hardest-to-bypass bottlenecks.

This is a highly valuable report on 'AI Layer 2 infrastructure.' It reminds the market that following GPUs, the next component to be repriced will not be a single part, but the entire AI interconnect stack.

However, it should not be interpreted simplistically as 'CPO will surge immediately.' A more accurate reading is:

2026: Watch pluggable optics/LPO/NPO/PCB/ABF/testing;

2027: Watch pilot CPO orders;

Post-2028: Watch whether CPO and optical I/O truly enter the core architecture of AI computing.

Editor/melody