Source: Zhou Junzhi Macro Team, China Securities Co., Ltd.

Authors: Jiang Jiaxiu, Zhou Junzhi

The Zhou Junzhi Macro Team at China Securities Co., Ltd. stated that upside tail risks in oil prices have become the primary driver pushing U.S. Treasury yields higher. Both AI-driven and traditional sectors are simultaneously fueling inflation, leaving Waller facing 'reverse independence' and making it difficult to cut rates.

In the near term, U.S. Treasury yields above 4.5% are unlikely to decline. A meaningful pullback will require tangible negative feedback—such as economic stress or a rise in unemployment—and over the long term, yields are expected to oscillate within a high range of 4%–5%. Tech stocks will remain driven by secular industry trends over the long run.

Core Insights

The U.S.-Iran conflict has entered its third phase of 'fighting and talking.' Market narratives have shifted from TACO to NACHO, with the tail risk of higher oil prices being the most significant factor driving up U.S. Treasury yields.

The U.S.-Iran conflict has entered its third phase of 'fighting and talking.' Market narratives have shifted from TACO to NACHO, with the tail risk of higher oil prices being the most significant factor driving up U.S. Treasury yields.

AI and traditional sectors are jointly driving up inflation and economic activity. Under high inflation, Waller faces 'reverse independence,' making it even harder for him than for Powell to justify a rate cut. In the near term, U.S. Treasury yields are unlikely to fall without concrete progress on Strait of Hormuz transit.

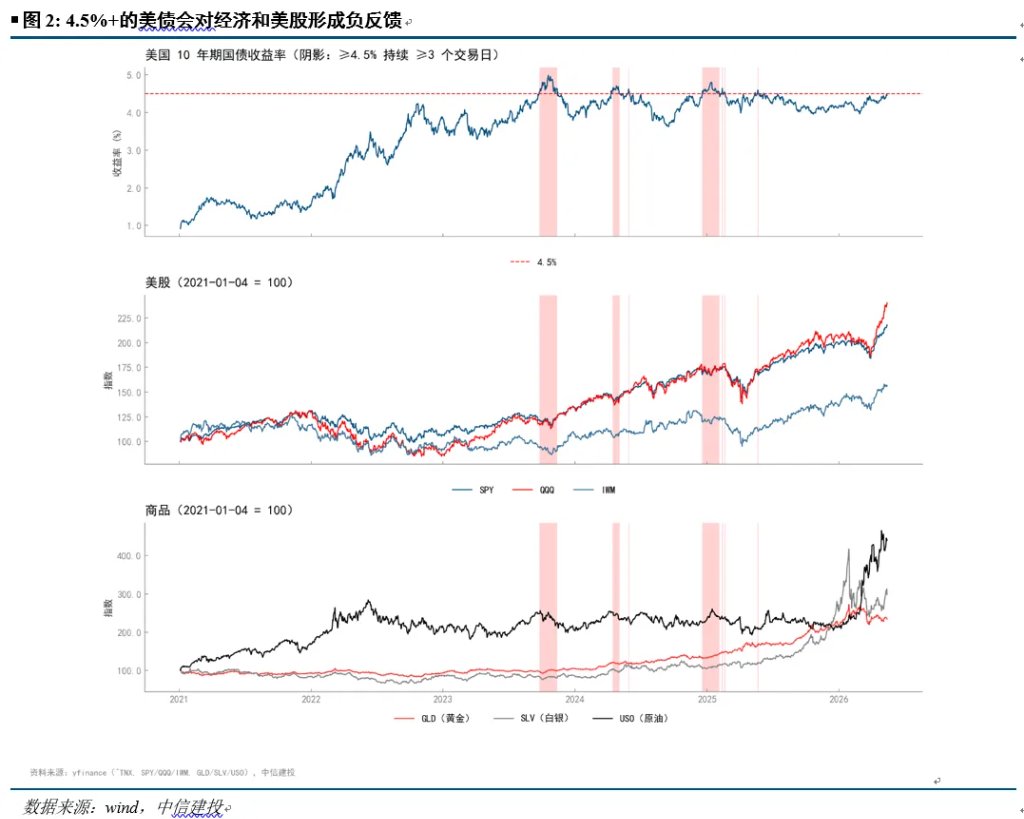

Over the medium term (6–12 months), U.S. Treasury yields above 4.5% will exert negative feedback on both the economy and U.S. equities—a pattern repeatedly validated in recent years. However, any yield decline hinges on observing actual negative feedback first, rather than pricing it in preemptively.

Over the long term (beyond 12 months), unresolved global debt pressures will continue to push term premiums higher, keeping yields entrenched in a high-range trading band.

High market concentration and elevated interest rates may temporarily curb the momentum of AI and semiconductor stocks, but over the long term, secular industry trends—not Treasury yields—will be the decisive factor for tech sector performance.

Main Text

I. What Is Driving the Rise in U.S. Treasury Yields?

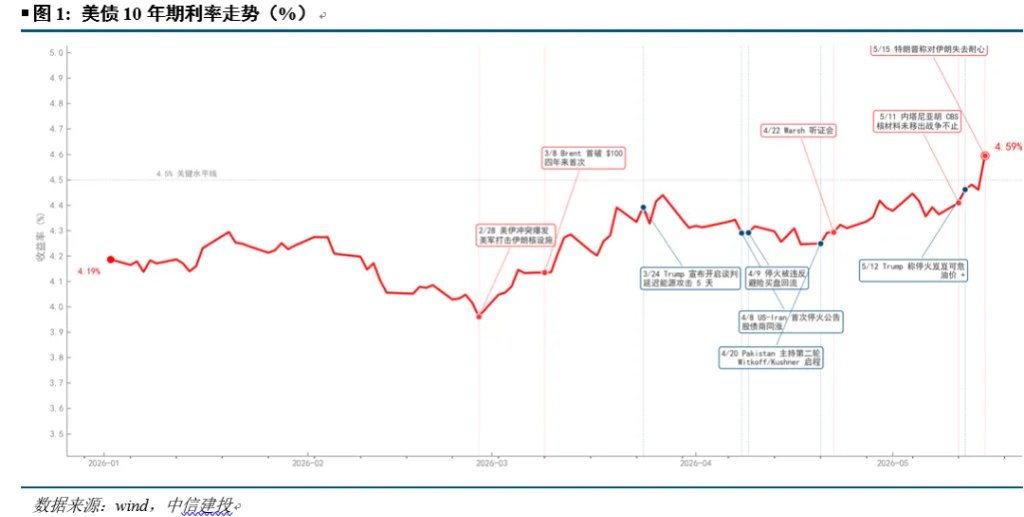

(I) U.S.-Iran Tensions Enter a New Phase: From TACO to NACHO

Market narratives surrounding U.S.-Iran tensions have evolved from the first phase (peak of full-scale military operations) and the second phase (Trump’s TACO and ceasefire negotiations) into the current third phase—a fragile equilibrium characterized by alternating escalations and talks. Core interests among the three key parties remain unresolved, yet all face practical constraints that prevent total escalation. Markets are no longer satisfied with unilateral negotiation signals from Trump; instead, they are focused on tangible progress toward ensuring open navigation through the Strait of Hormuz (see “Time to Focus on the Medium- to Long-Term Implications of U.S.-Iran Tensions” and “How Equities, Bonds, and FX Are Pricing U.S.-Iran Conflict”).

The defining feature of this third phase is not de-escalation but rather protracted tension. Market narratives have shifted from TACO to NACHO (Not A Chance Hormuz Opens). NACHO is essentially the inverse of TACO, reflecting markets’ ‘vote with their feet’ on Trump’s credibility in geopolitical policymaking.

This prolonged uncertainty implies that for bond markets, U.S. Treasury term premiums must continuously price in an 'Iran right-tail risk' rather than treating it as a one-off shock that can quickly dissipate.

(II) AI Is Simultaneously Boosting Inflation and Economic Growth in Both New and Old Economies

Capital expenditures by hyperscale cloud providers are projected to rise further in 2026, reaching $755 billion for the year—an 83% year-over-year increase—marking the largest 'new economy' capex cycle of the 21st century. The AI-driven infrastructure buildout represents the largest investment cycle since the dot-com bubble. In the early stages of transition between old and new economies, both sectors are jointly supporting inflation and economic data.

Meanwhile, capital spending on this scale is generating spillover effects into the old economy. For example, data center construction is boosting demand for power infrastructure and traditional construction. Surging electricity demand from AI is reviving long-stalled power infrastructure projects, including grid modernization, recommissioning of natural gas power plants, and small modular reactors (SMRs). Demand for traditional blue-collar roles is surging: median wages for robotics/technician positions have surpassed $80,000; hourly wages for data center construction workers are 32% higher than non-data center peers (annualized at $81,800); and some electricians working on Texas data centers now earn annual salaries of $240,000–$280,000.

Recent U.S. economic and inflation data have exceeded expectations, supporting higher Treasury yields. The ISM Manufacturing PMI rose to 52.7, with new orders accelerating to 54.1 and the prices component posting its fastest pace since April 2022. Industrial production increased by 0.7% month-over-month—the largest gain in 14 months—with information processing equipment up 1.7% and semiconductors up 1.0% collectively. CPI rose 3.8% year-over-year (the highest since May 2023), while PPI climbed 6% year-over-year (the highest since December 2022).

(III) Global Central Banks Pivot Toward Rate Hikes and Walsh Takes the Helm

As$Brent Last Day Financial Futures (JUL6) (BZmain.US)$With oil prices stabilizing above $110 per barrel, major central banks may find it difficult to ignore this crude oil shock amid persistently high inflation. In early May, the Bank of England Governor publicly stated, 'The strong price pressures stemming from Iran make a rate hike justified.' Markets have already priced in an ECB rate hike in June, while expectations for a Fed rate cut this year have once again evaporated.

The new Federal Reserve Chair, Wallsh, has taken office and adopted a hawkish stance during his Senate confirmation hearing in April. Wallsh stated, "Inflation remains the central concern for American households," "The Fed needs a new framework to address persistent inflation," and "The central bank's post-pandemic policy errors directly exacerbated price pressures." Markets are pricing in Wallsh's "reverse independence" under political pressure—when inflation faces constraints, Wallsh may find it even harder than Powell did in his later term to make rate-cut decisions.

However, from a medium- to long-term perspective, Wallsh’s remarks that "AI-driven productivity gains exert downward pressure on inflation" leave room for a dovish pivot by 2027.

(4) Global Debt Spillovers: Synchronized Pressure Across the UK, Japan, Europe, and the US

Following the pandemic, major economies—including the US, Japan, and Europe—pursued fiscal expansion and remain deeply entangled in fiscal consolidation challenges. Globally, fiscal policy is prone to easing but resistant to tightening, making long-end bond yields prone to rising but resistant to falling.

Geopolitical uncertainty has further compelled Europe and Japan to ramp up fiscal spending through "energy subsidies plus defense expansion." Japan’s Ministry of Finance has unveiled a new round of energy price subsidies, pushing Japanese government bond yields closer to levels signaling debt unsustainability. The UK has been forced to allocate additional fiscal space to assist households with energy costs, further exposing the shortfall in its autumn budget. The Labour Party’s heavy losses in local elections have intensified internal party pressure on the Prime Minister to resign; the pound has fallen for five consecutive trading days, and UK gilt yields have neared their 2008 highs.

II. Outlook for U.S. Treasury Yields

Last year’s reciprocal tariffs and this year’s U.S.-Iran conflict both triggered V-shaped market rebounds following Trump’s TACO statements. However, as the U.S.-Iran conflict enters a new phase, U.S. Treasury yields have hit new highs. We believe the fundamental difference between Trump’s geopolitical TACO this year and last year’s tariff-related TACO lies in the market’s widespread skepticism about Trump’s ability to reopen the Strait of Hormuz. Consequently, markets are pricing the Strait’s disruption not as a temporary geopolitical shock but as a persistent macro backdrop—and in this context, there is a genuine physical shortage in crude oil supply. The longer this situation persists, the less likely the impact will fade like tariffs did; instead, it may trigger tail risks of nonlinear oil price surges.

We believe current U.S. Treasury yields have already priced in$Brent Last Day Financial Futures (JUL6) (BZmain.US)$a base-case oil price of USD 85 per barrel and an inflation environment with CPI at 3.x%,$U.S. 10-Year Treasury Notes Yield (US10Y.BD)$and a yield centering around 4.5% is consistent with this fundamental outlook. However, the unresolved uncertainty surrounding the Strait of Hormuz means that, in the near term, 10-year yields are more likely to rise than fall.

Looking ahead, the two key divergences in expectations for U.S. Treasury yields are: (1) Will the narrative on AI’s economic impact shift toward job displacement and rising unemployment, or will both old and new economy sectors continue to jointly drive inflation higher? (2) Will the new Fed Chair, Kevin Warsh, lean hawkish or dovish?

Over a medium-term horizon (6–12 months), U.S. Treasury yields above 4.5% will exert negative feedback on both the economy and U.S. equities—a pattern repeatedly validated over the past several years. This negative feedback mechanism will be the primary endogenous driver behind a potential “peak-and-decline” trajectory for Treasury yields over the next 6–12 months.

If the 10-year U.S. Treasury yield breaches 4.8% and moves closer to 5%, the economy is likely to experience renewed pressure within the next 6–12 months, leading to higher unemployment and a subsequent temporary decline in Treasury yields—mirroring patterns seen in recent years. However, such a decline hinges on the actual manifestation of this negative feedback, not on market pricing that anticipates it prematurely. In other words, for the 10-year yield to fall back into the 4.0%–4.5% range, either substantive restoration of shipping through the Strait of Hormuz or a significant rise in the unemployment rate would need to occur.

Over the long term (beyond 12 months): global debt burdens remain intractable, term premiums continue to rise, and yields will oscillate persistently within a high range.

We believe the frequent emergence of government debt distress overseas signals a paradigm shift in the appropriate level of term premium relative to the low-rate era of 2010–2020. U.S. Treasury yields will likely remain entrenched in a high range of 4.0%–5.0% for an extended period, with limited prospects of falling sustainably below 4% (see “The Dilemma of Overseas Government Debt Resolution”).

III. High Interest Rates Do Not Undermine Long-Term Equity Gains Driven by Structural Industry Trends

High market concentration and elevated interest rates may temporarily curb the momentum of AI and semiconductor stocks, but over the long term, secular industry trends—not Treasury yields—will be the decisive factor for tech sector performance.

In the second half of the year, the focus of the AI investment theme will shift from “scale of capital expenditure” to “inflection point in marginal profitability.” Annual AI-related capex reached $700 billion in the first half, setting a new record for tech cycles. Market tolerance for the AI cycle is now transitioning from a “build capacity first, tell the story later” approach to one demanding “proof of ROI via cash flow.” The validation criterion is whether token economics can shift from breakeven or losses to delivering positive marginal contributions.

If token demand on the revenue side continues to grow substantially, while unit costs for large language models on the cost side keep declining and token pricing stabilizes, this would support an inflection point in marginal profitability for large-model providers, thereby enabling a virtuous cycle of future revenue growth and business model reinforcement. Specifically, improved marginal profitability enhances the sustainability of capex, which in turn boosts production capacity—further refining models and reducing costs. This expands the addressable scope of AI applications, driving synchronized growth in token consumption and AI-generated revenue, which reinforces profitability and cash flow.

We believe the monetization pathway of large models will determine the trajectory of AI-related equity performance in the second half of the year.

Moreover, while AI and semiconductors reached record highs in the first half of the year, we must also pay attention to two potential risks for AI development going forward.

Risk 1: The shift from 'self-funding' to 'external funding' means the market is beginning to scrutinize ROI rigorously.

Over the past three years, nearly all AI-related capital expenditures (capex) have been funded by the operating cash flows of leading cloud providers. The top four cloud vendors collectively generate over USD 300 billion in annual free cash flow—sufficient to cover their capex while still maintaining a positive residual balance—thus allowing the market to tolerate lower near-term returns on investment (ROI). However, a pivotal shift is expected in the first half of 2026, as model companies such as OpenAI, Anthropic, and xAI actively seek external financing.

External funding implies valuation by external investors. Consequently, in the second half of the year, the market will begin rigorously evaluating unit economics per token, the timing of inflection points in marginal profit margins, and the ratio of AI revenue to cumulative capital expenditure. The market’s previous tolerance for the 'build capacity first, tell the story later' approach will be replaced by a hard constraint requiring demonstrable ROI through cash flow generation. Additionally, in credit markets, attention will turn to the overall scale of AI-related bond issuance and changes in credit spreads.

Risk 2: Insufficient user stickiness in AI applications and uncertainty around the existence of a late-mover advantage—the DeepSeek pathway is once again driving pricing curves downward.

The late-mover advantage is exemplified by DeepSeek R1 achieving performance levels comparable to GPT-4 and Claude at one-tenth the inference cost. Concurrently, domestic models such as Alibaba’s Tongyi, Baidu’s ERNIE Bot, and Moonshot’s Kimi have reduced their API pricing, thereby challenging the structural assumption that prices for frontier-model APIs would remain stable or decline only gradually.

Risk Warning

If US-Iran tensions ease more than expected—if a durable ceasefire agreement is reached and normal transit through the Strait of Hormuz resumes—Brent crude prices could fall below USD 80 per barrel, potentially unraveling the NACHO narrative rapidly and pushing the 10-year US Treasury yield back down to the 4.0%–4.2% range in the near term.

Should the US labor market deteriorate materially—for instance, if the unemployment rate exceeds 4.7% or nonfarm payroll growth remains below 50,000 for three consecutive months—the Federal Reserve may be forced to pivot dovish earlier than anticipated, a scenario under which US equity earnings would face simultaneous downward pressure.

A significant downward revision in AI-related capital expenditures, with hyperscalers cutting their projected 2027 capex growth rates by more than 10% in their Q3/Q4 earnings reports.

If the Bank of Japan accelerates its pace of interest rate hikes, synchronized increases in global bond yields could trigger a liquidity shock.

Geopolitical conflict spills over and escalates, with the Iran conflict spreading to Saudi Arabia, the United Arab Emirates, and other areas, triggering a full-scale regional war.

Editor/melody