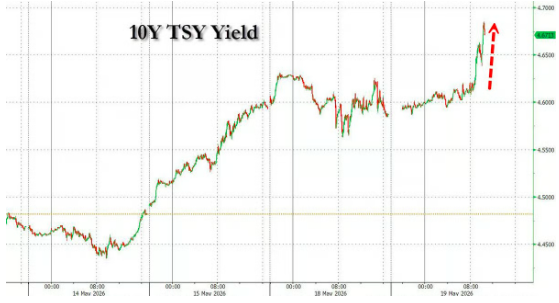

① Concerns that central banks will be forced to raise interest rates intensified, pushing the yield on 30-year U.S. Treasuries to its highest level in 19 years on Tuesday; ② A wave of large-scale selling in the U.S. Treasury futures market during early New York trading hours on Tuesday exacerbated panic in the world’s largest government bond market, valued at $31 trillion.

Shanghai-headquartered Caixin Media, May 20 (Editor: Xiaoxiang) — As investor concerns mounted that accelerating inflation will compel central bank officials to hike interest rates, the yield on the longest-dated U.S. Treasury security—the 30-year bond—rose further on Tuesday to its highest level in 19 years.

Market data shows that $U.S. 30-Year Treasury Bonds Yield (US30Y.BD)$ On Tuesday, yields rose intraday by as much as 7 basis points, briefly surpassing the 5.20% mark—a level last seen in 2007, just before the onset of the global financial crisis. Bond markets in Europe and Japan also declined that day, and this wave of bond sell-offs once again unfortunately spilled over into U.S. equity markets.

Global government bond yields have surged sharply in recent weeks, driven by soaring energy prices triggered by the Iran conflict, which has amplified inflation concerns and led traders to bet that the Federal Reserve could begin raising rates as early as this year. Widening government fiscal deficits have also prompted investors to demand higher compensation for holding longer-duration debt.

Global government bond yields have surged sharply in recent weeks, driven by soaring energy prices triggered by the Iran conflict, which has amplified inflation concerns and led traders to bet that the Federal Reserve could begin raising rates as early as this year. Widening government fiscal deficits have also prompted investors to demand higher compensation for holding longer-duration debt.

Liz Templeton, Senior Product Manager at Morningstar, stated, “The bond market is pricing in a ‘higher for longer’ interest rate policy, most visibly along the long end of the curve where duration sensitivity is greatest. This reflects persistent uncertainty surrounding Federal Reserve policy, energy-driven cost pressures, and heavier issuance of Treasury securities.”

Persistently rising yields threaten the pace of growth in the U.S. economy, which has shown resilience thus far, and are increasing borrowing costs for American homebuyers and businesses. Markets have even begun speculating whether senior U.S. government officials might deploy what investment bank Jefferies refers to as ‘unconventional intervention tools’ to forcibly curb runaway long-end Treasury yields—especially after authorities had already awkwardly tilted the government’s debt issuance structure toward shorter-term bills.

Intense ‘capitulation-style’ selling within one hour

What worries bondholders is that Tuesday’s bond selloff was not simply driven by a surge in oil prices—crude actually traded lower on the day—and was not attributable to any single catalyst. This suggests widespread nervousness in the market as investors reassess the clearing price of debt.

Market data indicated that a sudden wave of large-scale selling in the U.S. Treasury futures market on Tuesday heightened panic in the world’s largest government bond market, valued at $31 trillion, as fears of resurgent inflation prompted investors to price in higher interest rates. A spike in the 10-year Treasury yield, triggered by short positions in futures contracts, created ripple effects across the entire yield curve.

According to industry-aggregated data, these futures trades occurred during the most volatile hour of early New York trading on Tuesday, with a notional value equivalent to $15 billion worth of 10-year benchmark Treasury notes.

The first block trade on Tuesday entered the market at 9:38 a.m. New York time (Tuesday evening Beijing time), followed by a steady stream of sell orders until approximately 10:40 a.m. Within this roughly one-hour window, traders sold 136,500 contracts of 10-year Treasury futures and 83,000 contracts of 5-year Treasury futures via block trades. Trading volume in the 10-year Treasury futures was approximately 80% above its 20-day average.

These trades contributed a total risk weighting of approximately USD 12 million per basis point across 10 block orders. The transactions were executed anonymously, making it difficult to identify the firms involved or the ultimate beneficiaries of these positions.

Analysts noted that while Tuesday’s activity may have stemmed from traders unwinding long positions, market positioning over recent trading days has increasingly tilted bearish. Last week, open interest data reflected the accumulation of new short positions, as traders added risk exposure in 10-year Treasury futures amid rising yields.

Alan Taylor, founding partner at Archr LLP, described it as “a day of capitulation in the U.S. Treasury market,” adding that the selloff was accelerated by “multiple large sellers.”

Citi strategist David Bieber stated that over the past five days, traders “have aggressively added new short risk on the way down in price.” He added that short positions are now “highly extended” both tactically and structurally.

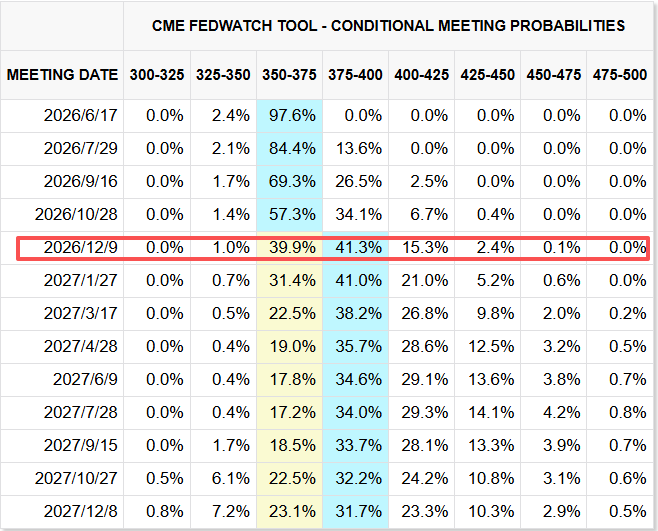

Expectations for interest rate hikes continue to intensify.

The shift in market sentiment is expected to soon test incoming Federal Reserve Chair Kevin Warsh. Traders now widely anticipate that the Fed’s next move will be a rate hike, potentially as early as year-end. In contrast, prior to the outbreak of the Iran conflict in late February, they had expected as many as three rate cuts by the Fed in 2026.

“Market expectations have clearly shifted toward rate hikes,” said Benjamin Schroeder, senior rates strategist at ING Groep, citing investor concerns that “energy price pressures could evolve into more than just a transitory inflationary phenomenon.”

Historically, a 5% yield on the 30-year U.S. Treasury bond has been viewed as a ‘red line’—a level at which some investors would step in to buy on dips. However, recent Treasury market selling is clearly overturning this assumption, potentially signaling the dawn of a new era for the USD 31 trillion U.S. Treasury market, which is widely regarded as the world’s premier safe-haven asset and the benchmark for global borrowing costs.

Strategists at Barclays and Citigroup have warned clients that long-end U.S. Treasury yields could breach 5.5%—a level last seen in 2004. Meanwhile, the head of BlackRock’s research division has advised investors to reduce allocations to developed-market government bonds, including U.S. Treasuries.

Ajay Rajadhyaksha, Chairman of Barclays Global Research, stated, 'With debt growing faster than the economy, worsening inflation dynamics, and a lack of political will for fiscal reform, there is little reason to chase long-term bonds.'

A similar dynamic to that of U.S. Treasuries is currently unfolding globally—$UK30-YearGovernmentBondYield (GB30Y.BD)$has approached 6%, while Germany's long-term borrowing rates are at their highest levels since 2011.

‘Yields reflect not only inflation volatility but increasingly signal a return of fiscal risk,’ said Laura Cooper, Global Investment Strategist and Head of Macro Credit at Nuveen. ‘At current yield levels, the bond market’s capacity to absorb this fiscal spending is limited and will not come without demanding additional compensation.’

It is worth noting that rising benchmark U.S. Treasury yields could also pose a challenge to the U.S. stock market, which has performed strongly this year, as higher borrowing costs exert pressure on both businesses and consumers. So far this year,$S&P 500 Index (.SPX.US)$has surged more than 7%, weathering the selling pressure seen across most bond markets.

However, on Tuesday, the index comprising small and mid-sized companies—which typically carry higher debt loads and have lower profitability than large enterprises—$Russell 2000 Index (.RUT.US)$, fell approximately 1% by the end of the trading day, extending its three-day cumulative loss to 4%. The S&P 500 and$NASDAQ 100 Index (.NDX.US)$also weakened in tandem with U.S. Treasury prices.

‘Whether U.S. equities can withstand the current bearish trend in the Treasury market is the true litmus test for assessing the impact of this bond sell-off,’ said Ian Lyngen, Head of U.S. Rates Strategy at BMO Capital Markets. ‘We expect that if the 30-year Treasury yield rises to 5.25% in the coming weeks, equity valuations will experience a more sustained correction.’

Editor/Rocky