The global bond sell-off could trigger turmoil in Asia's weakest economies.

Zhitong Finance APP has learned that in May 2026, three of Asia’s most vulnerable emerging economies are being swept by a 'perfect storm.' On one front, the ongoing Iran conflict has led to a de facto blockade of the Strait of Hormuz for over eleven weeks, causing energy costs to surge and severely impacting the economic lifelines of net oil-importing countries such as Indonesia, India, and the Philippines. On another front, global bond markets are experiencing severe turbulence, with the yield on 30-year U.S. Treasuries surpassing the 5% mark for the first time since 2007. The strong dollar is drawing capital away from emerging markets, sharply reducing their asset appeal and triggering a flight of capital from these structurally weakest economies.

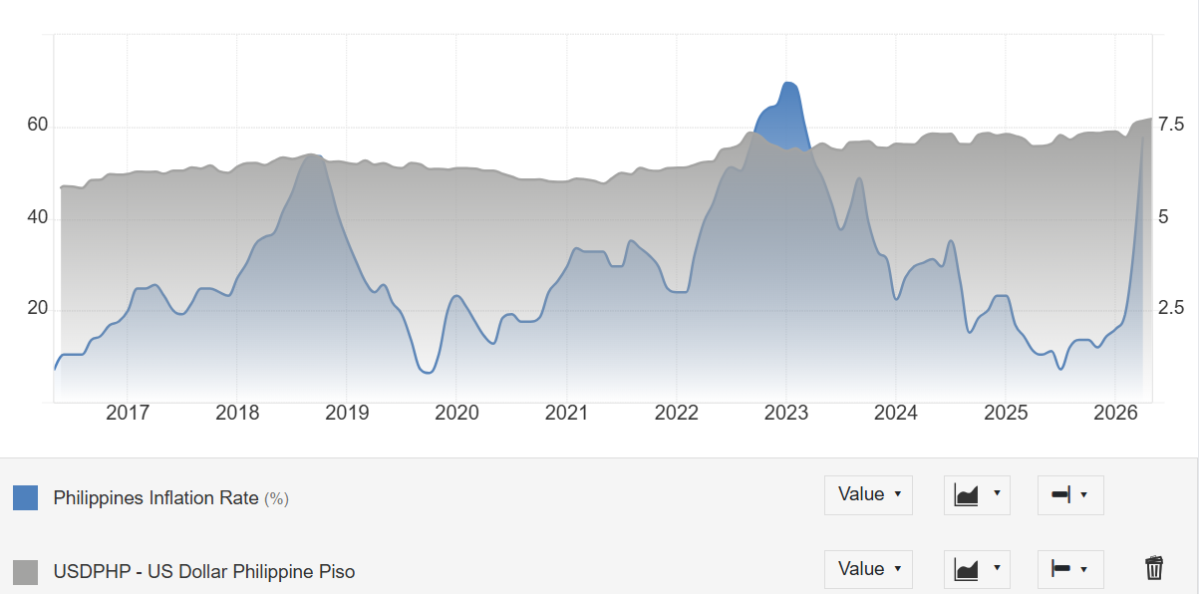

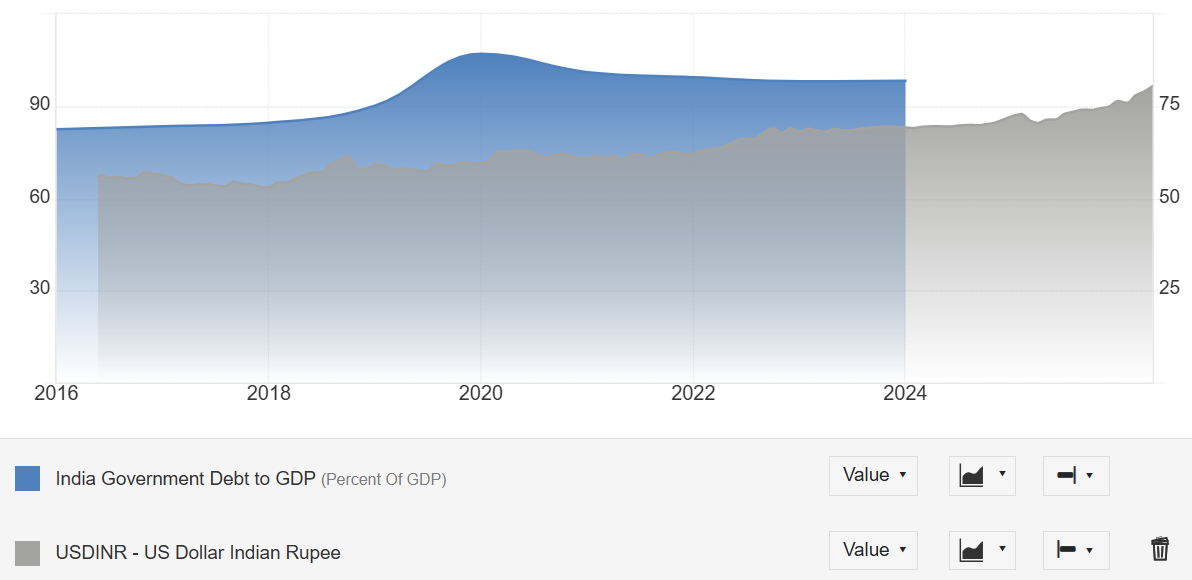

The destructive force of this storm is most evident in currency markets. Nearly all Asian currencies have depreciated, with the Indonesian rupiah, Indian rupee, and Philippine peso leading the declines. The rupiah extended its losses on Tuesday, hitting a record low of 17,730 against the U.S. dollar; the rupee hovered near its historic low of 96.3; and the peso hit consecutive record lows over two days last week. Rising energy prices have driven the Bloomberg Philippines Bond Index—denominated in U.S. dollars—to fall 13% year-to-date, the steepest decline among emerging Asian markets.

Jason Tuvey, Deputy Chief Emerging Markets Economist at Capital Economics, warned that interest rate hikes "can only offer a brief respite."$Nomura Holdings (NMR.US)$Rob Subramaniam, Chief Economist at Nomura Holdings, was more blunt—"The lessons from the taper tantrum and$ASIA FINANCIAL (00662.HK)$crisis are that risk premia can rise rapidly, seemingly ample reserves can dwindle quickly, and cost-of-living pressures could exacerbate political instability."

Jason Tuvey, Deputy Chief Emerging Markets Economist at Capital Economics, warned that interest rate hikes "can only offer a brief respite."$Nomura Holdings (NMR.US)$Rob Subramaniam, Chief Economist at Nomura Holdings, was more blunt—"The lessons from the taper tantrum and$ASIA FINANCIAL (00662.HK)$crisis are that risk premia can rise rapidly, seemingly ample reserves can dwindle quickly, and cost-of-living pressures could exacerbate political instability."

"Triple Storm" Hits Simultaneously

First Shock: Energy Lifeline Cut Off—Oil Shock Unprecedented in Scale

Since the joint U.S.-Israeli military operation against Iran on February 28, the Strait of Hormuz—the strategic chokepoint handling nearly 30% of global seaborne oil shipments—has been effectively closed for over eleven weeks. Global oil inventories are now declining at a record pace of approximately 4.8 million barrels per day. The International Energy Agency (IEA) estimates total lost oil exports exceed 13 million barrels per day, constituting the largest supply disruption in history. Morgan Stanley has warned that if the Strait of Hormuz remains closed, international oil prices could surge to $150 per barrel.

For India (which relies on imports for roughly 85% of its crude oil needs), Indonesia (a net oil importer), and the Philippines (with extremely low energy self-sufficiency), sustained Brent crude prices above $100 per barrel mean a sharp deterioration in import bills. According to Reuters, under persistently high oil prices, India’s monthly crude import bill alone could increase by $12–13 billion.

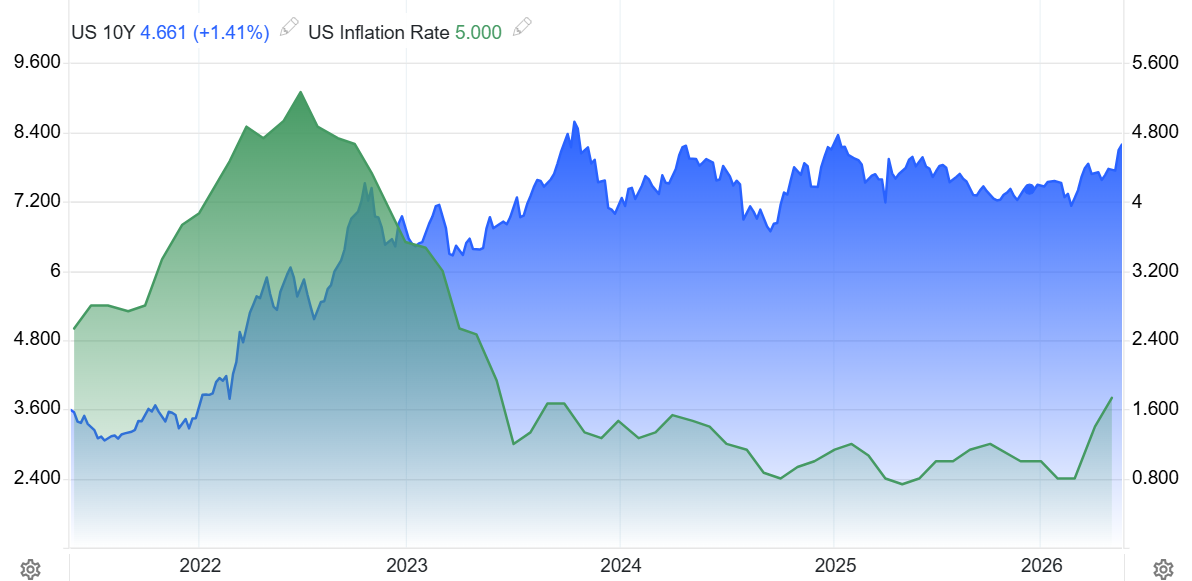

Second Shock: Global Bond Market Turmoil Accelerates Capital Flight

U.S. CPI rose sharply to 3.8% year-over-year in April, with core CPI holding at 2.8%, significantly exceeding inflation expectations and sparking market fears that the Federal Reserve may be forced to reverse its policy stance. Over the past week, the yield on 30-year U.S. Treasuries climbed to 5.16%—the highest since 2007—while the 10-year yield rose to 4.59%, and the policy-sensitive 2-year yield breached 3.95%.

The surge in U.S. Treasury yields has rapidly transmitted to emerging markets: a stronger dollar is eroding the attractiveness of emerging market assets, accelerating capital outflows from Asia, and sharply increasing debt-servicing costs for dollar-denominated liabilities. Central banks across these countries are being forced to deploy foreign exchange reserves or raise interest rates to defend their currencies—but rate hikes further suppress domestic growth, creating a stagflationary vicious cycle.

Third layer: Compounding political turmoil accelerates the erosion of confidence

Beyond oil price and currency pressures, each of the three countries faces unique domestic challenges. Philippine Vice President Sara Duterte is embroiled in an impeachment case, and leadership changes in the Senate have significantly narrowed the path to conviction, exacerbating investor concerns about policy continuity. In Indonesia, President Prabowo’s controversial remark—"villagers are unaffected by depreciation"—has raised market doubts about his policy direction. Meanwhile, Indian Prime Minister Modi has unusually urged citizens to "postpone gold purchases and reduce outbound travel," with the very intensity of such administrative intervention signaling heightened anxiety among policymakers.

$HSBC Holdings (HSBC.US)$Frederic Neumann, Chief Asia Economist at HSBC Holdings, stated unequivocally: "Growth will come under greater pressure across much of the region, leaving central banks in a difficult position as they grapple with surging price pressures. The situation could become even more severe. We are not out of the woods yet."

The plight of the three nations: One storm, different wounds

Indonesia: Central bank faces its "toughest policy meeting" today

On Wednesday, May 20, Bank Indonesia will conclude its two-day monetary policy meeting and announce its interest rate decision. A survey shows that 16 out of 29 economists (a narrow majority) expect the central bank to raise rates by 25 basis points to 5%, marking the first adjustment since October 2024. Tay Qi Hang, an economist at the Economist Intelligence Unit (EIU), stated bluntly that the key rationale for a rate hike lies in "the market's lack of confidence in the Indonesian government and central bank's measures to defend the rupiah."

However, pressure to hike rates coexists with real economic constraints. Indonesia’s Q1 2026 GDP grew by 5.61% year-on-year, a respectable performance; April inflation remained at 2.42%, still within the central bank’s 1.5%–3.5% target range—thanks largely to temporary government fuel subsidies that have dampened energy price pass-through. Yet these subsidies are fiscally unsustainable, and a widening current account deficit pushed the current account into deficit in Q4 last year, forcing heavy use of foreign exchange reserves for currency intervention. Jason Tuvey of Capital Economics noted that even if rates are raised, it would only grant the rupiah "a brief respite," and the fundamental solution lies in "authorities abandoning the populist and interventionist policies adopted since President Prabowo took office."

Moreover, Bank Indonesia has restarted an "Operation Twist"-style maneuver reminiscent of 2022—selling short-term bills while buying long-term government bonds—to support the rupiah without triggering a sharp rise in domestic yields. Finance Minister Bambang P.S. Brodjonegoro also confirmed the government has begun repurchasing government bonds to curb rising yields and capital outflows.

Investors’ core concern centers on Prabowo’s flagship free school meal program. The Indonesian government has allocated IDR 335 trillion (approximately SGD 25.1 billion) for the program this year—nearly 9% of the national budget, almost four times the IDR 71 trillion allocated last year. As a special report by Lianhe Zaobao noted in April: "There’s no such thing as a free lunch—not even nutritious meals for Indonesian children come without significant fiscal cost. With Middle Eastern conflicts driving up global energy prices, Indonesia needs fiscal space more than ever to manage inflation. Who ultimately pays for these free meals?" More critically, Indonesian law mandates that the fiscal deficit be kept within 3% of GDP, yet both energy subsidies and the free meal program are simultaneously straining this limited fiscal room.

Philippines: The specter of stagflation looms; Treasury forced to "reject bids"

The Philippines faces the most severe situation, nearly embodying all the elements of a 'perfect storm.' A confluence of energy shocks, political instability, currency collapse, and sharply contracting fiscal space is pushing the economy toward a stagflationary abyss.

On inflation, the year-on-year CPI surged to 7.2% in April—the highest in three years—far exceeding the central bank's target range of 2%–4%, driven primarily by soaring costs for fuel, transportation, and food. Gasoline and diesel prices have risen by 65.3% and 58.4%, respectively, compared to pre-war levels. On growth, GDP expanded by just 2.8% in the first quarter—the weakest performance in five years—and fell well short of the government’s minimum target of 5%. The International Monetary Fund (IMF) has sharply revised down its 2026 GDP growth forecast for the Philippines from 5.6% to 4.1%.

Currency markets have also taken a heavy hit. On May 16, the Philippine peso hit a new record low of 61.59 against the U.S. dollar for the second consecutive day; the Philippine Stock Exchange Index (PSEi) closed down 38.26 points at 5,976.77. Approximately one-third of government debt is owed to foreign creditors and denominated in U.S. dollars, meaning every incremental depreciation of the peso directly increases debt-servicing costs. ANZ forecasts that the Philippines’ current account deficit will reach 4% of GDP in 2026.

More troubling still, fiscal space is rapidly shrinking under the triple pressure of inflation, weak growth, and currency depreciation. On May 19, the Philippine Department of Finance rejected all bids for its PHP 30 billion (USD 487 million) seven-year Treasury bond auction after investors demanded an average yield of 7.915%—significantly higher than the previous day’s comparable yield of 7.60%, a seven-and-a-half-year high. This was the clearest signal of distrust from the bond market: investors are demanding higher risk premiums, and the government cannot afford such elevated borrowing costs. BMI Research, a unit of Moody’s, warned that the ongoing cost-of-living crisis is becoming 'the primary driver of rising social and political risks in the Philippines.'

Political uncertainty is further amplifying economic risks. The impeachment trial of Vice President Sara Duterte is advancing in the Senate, but a leadership change—where Alan Peter Cayetano, an ally of Duterte, assumed the role of Senate President—has significantly weakened the institutional foundation for conviction. MUFG Bank warned that escalating tensions between the Marcos and Duterte political clans could 'undermine investor confidence' and create an even more adverse environment for an economy already under stagflationary pressure. In its baseline scenario, MUFG expects the Bangko Sentral ng Pilipinas (BSP) to implement selective policy tightening if Middle East tensions subside by May; however, if Brent crude prices remain elevated in the third quarter, broader monetary tightening across the region is likely, with the Philippines and India at the forefront.

India: Modi Deploys a Dual Strategy of Gold Restrictions and 'Patriotism'

Unlike Indonesia and the Philippines, which have focused on monetary and fiscal policy responses, India has opted for a more administrative and trade-protective defensive approach—a measure in itself of the crisis’s severity.

Over the past month, the Indian government has rolled out a series of emergency measures: on May 13, it sharply raised import duties on gold and silver from 6% to 15%; days later, it reclassified silver bar imports from 'free' to 'restricted'; and it is now considering increasing tariffs on edible oil imports. Most notably, Prime Minister Modi launched an unusual 'patriotic mobilization,' publicly urging citizens to refrain from buying gold, reduce outbound travel, use public transport more frequently, and work remotely over the next year to conserve fuel. Brickwork Ratings estimates that if effectively adopted, Modi’s seven behavioral appeals—including working from home, avoiding international travel, pausing gold purchases, saving fuel, reducing edible oil consumption, promoting natural farming, and favoring domestic goods—could free up as much as USD 37.8 billion in foreign exchange buffers for India in the current fiscal year.

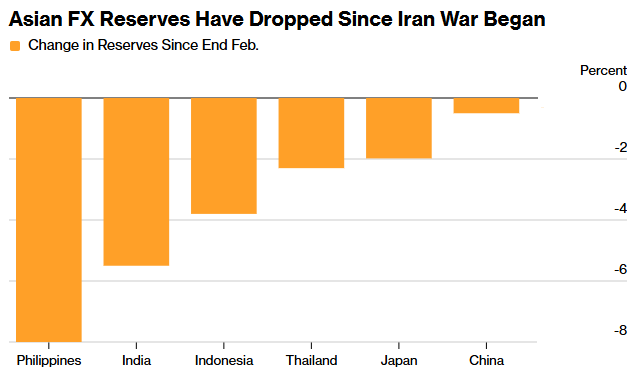

These measures come against an equally dire backdrop. As of May 18, the Indian rupee hit a historic low of 96.18 against the U.S. dollar, having depreciated by more than 5.5% since the outbreak of the Iran conflict, making it one of Asia’s worst-performing currencies. Foreign exchange reserves have declined by approximately USD 38 billion—from a pre-conflict peak of USD 728.49 billion on February 27—to USD 690.7 billion. The Reserve Bank of India’s net short position in U.S. dollars across onshore and offshore markets has approached USD 100 billion, marking a record level of intervention. ANZ forecasts India’s current account deficit will reach 1.9% of GDP in 2026.

However, analysts widely view these measures as short-term emergency tactics unlikely to fundamentally reverse the systemic pressures stemming from external conditions. Indian media point out that exchange rates are ultimately determined by foreign exchange supply and demand, and administrative interventions cannot sustainably override market pricing; if depreciation stems from chronic current account imbalances, the effectiveness of such interventions will be severely limited. Meanwhile, the 15% import duty on gold has created a substantial price gap between domestic and international markets, generating significant arbitrage opportunities that are already fueling a surge in illicit gold smuggling—a challenge likely to complicate India’s regulatory landscape going forward. Economists also caution that such trade-protective measures could spread to other Southeast Asian economies, particularly if food prices continue to rise sharply.

Echoes of History: Is the Ghost of 1997 Returning?

Widespread pressure on Asian currencies, surging energy prices forcing emergency measures, and central banks repeatedly drawing down foreign exchange reserves—these developments make it hard to avoid a historical parallel: is the 1997 Asian financial crisis repeating itself?

Analysts acknowledge that the similarities between the two episodes cannot be ignored. During the 1997 crisis, currencies in Thailand, Indonesia, and South Korea plummeted, and foreign exchange reserves evaporated within months, triggering severe economic recessions, soaring inflation, and political turmoil. In 2013, the U.S. Federal Reserve signaled tapering its stimulus program, sparking a 'taper tantrum' that triggered massive capital outflows from emerging markets, with India, Indonesia, and the Philippines among the hardest hit that year.

However, most economists argue that the institutional defenses built by Asian economies over the past three decades mean today’s vulnerabilities are fundamentally different from those in 1997. David Lubin, Senior Research Fellow at Chatham House, notes that the 1997 crisis was driven by a 'toxic combination of fixed exchange rates, high levels of short-term external debt, low foreign exchange reserves, and large current account deficits,' whereas 'today, Asian economies—precisely because of the lessons learned from the late-1990s crisis—are better protected.'

Brad Setser, Senior Research Fellow at the Council on Foreign Relations, draws a key distinction based on the nature of the shocks: the 1997 crisis was a financial account shock—bank funding dried up—whereas the current crisis is a current account shock—oil imports have been disrupted. 'One was a financial shock; the other is a real-economy shock. For the most affected Asian economies, the impact of the 1997–98 crisis was far greater.' Today’s Asian economies generally operate under more flexible exchange rate regimes, hold larger foreign exchange reserve buffers, have deeper local-currency bond markets, and exhibit significantly reduced reliance on short-term external debt—all of which contrast sharply with the vulnerability structure of 1997.

But this does not mean complacency is warranted. Sanjay Mathur, Chief Economist for Southeast Asia and India at ANZ, issued a particularly stark warning in last week’s report—"Given that foreign exchange reserves have already declined significantly and the headwinds from energy prices have yet to abate, foreign exchange interventions of this magnitude will become increasingly difficult to sustain."$Nomura Holdings (8604.JP)$Chief Economist Rob Subramaniam also warned that when global financial conditions tighten, risk premiums could surge sharply in a short period, and even seemingly adequate foreign exchange reserves could be rapidly depleted, while rising living costs could further amplify social and political risks.

Summary

Indonesia, the Philippines, and India—the three most vulnerable emerging markets in Asia—are simultaneously facing a 'perfect storm' of pressures stemming from energy, debt markets, currencies, and politics. Their respective firewalls vary in strength: India holds nearly $690 billion in foreign exchange reserves, sufficient to cover about nine months of imports, making its reserve position relatively secure; Bank Indonesia has responded with a combination of 'Operation Twist'-style measures and foreign exchange interventions and is likely to raise interest rates today; the Philippines faces the narrowest fiscal space and is squeezed between inflation and growth, exhibiting the most pronounced stagflation risks.

Yet their shared dilemma is this: as the war continues to push oil prices higher, as expectations of Federal Reserve tightening persistently transmit through bond markets, and as current account deficits simultaneously erode both reserves and exchange rates, unilateral defenses by any single country may be overwhelmed by the tide of reversing global capital flows. If oil prices remain above $100 per barrel and U.S. Treasury yields stay elevated near 5%, these three economies will face even tighter policy constraints, while social and political risks will accumulate faster under persistent cost-of-living pressures.

HSBC’s Neumann stated, 'We are not out of the woods yet.' Capital Economics’ Tuvey put it more bluntly—even interest rate hikes would offer only 'a brief respite.' In this storm, no country can remain insulated from the dual pressures of an energy crisis and global capital tightening. Asian emerging markets are undergoing their most severe comprehensive stress test in nearly three decades—since the crises of 1997 and 2013.

Editor/Vincent