Pimco is bullish on Japan's 30-year government bonds, describing the yield curve as "too steep." Amid a global bond market turmoil, Pimco offered a vote of confidence, stating that Japan’s 30-year sovereign debt exhibits an "excessive risk premium," suggesting the global sell-off in long-end bonds may have gone too far.

Zhitong Finance APP has learned that Pacific Investment Management Co. (PIMCO), one of the world’s largest fixed-income investment managers, sees significant investment opportunities in Japan’s 30-year sovereign bonds, which are currently experiencing heavy selling pressure. The steepest long-end government bond yield curve globally has reached a window for correction. Meanwhile, global bond market traders’ concerns over inflation and government spending have pushed yields on these bonds to record highs.

PIMCO’s latest investment view on Japan’s 30-year bond market highlights that market pricing may be excessively reactive to expectations of interest rate hikes by major central banks such as the Federal Reserve and the Bank of Japan, and that risks related to inflation, fiscal expansion, monetary tightening, and term premiums are being significantly overstated.

The yield on the U.S. 30-year Treasury briefly approached 5.18%, nearing its highest level since 2007; Japan’s 30-year government bond yield surpassed 4%—a first since the maturity was introduced in 1999; and the UK’s 30-year yield rose close to 5.8%, hitting a peak not seen since 1998. Recently, the surge in global sovereign bond yields has intensified, severely pressuring valuations of global risk assets—including highly valued technology stocks and cryptocurrencies—and triggering pullbacks in bellwether tech indices such as the Philadelphia Semiconductor Index.

The yield on the U.S. 30-year Treasury briefly approached 5.18%, nearing its highest level since 2007; Japan’s 30-year government bond yield surpassed 4%—a first since the maturity was introduced in 1999; and the UK’s 30-year yield rose close to 5.8%, hitting a peak not seen since 1998. Recently, the surge in global sovereign bond yields has intensified, severely pressuring valuations of global risk assets—including highly valued technology stocks and cryptocurrencies—and triggering pullbacks in bellwether tech indices such as the Philadelphia Semiconductor Index.

According to PIMCO, this aggressive repricing of sovereign yield curves may reflect an overly hawkish market consensus that central banks worldwide are about to re-enter a sustained hiking cycle. Nevertheless, from a global bond market perspective, the recent sharp rise in long-end yields across the U.S., Japan, the UK, France, and other countries is indeed partly driven by energy shocks and inflation expectations. However, the persistent turbulence in long-dated government bonds appears more attributable to a joint reassessment of term premiums, fiscal sustainability, and bond supply-demand dynamics.

PIMCO turns bullish on Japan’s 30-year bonds, betting that the storm of rising ultra-long yields will eventually subside.

Marc Seidner, Chief Investment Officer of Non-Traditional Strategies at PIMCO, stated that Japan’s long-end yield curve has become “excessively steep” relative to other developed markets, thereby creating attractive investment value in longer-dated debt.

It is understood that the fixed-income-focused investment giant has firmly maintained a long position on Japan’s 30-year government bonds amid the recent surge in global sovereign yields—including the 10-year U.S. Treasury—and is simultaneously betting on further declines in the price of Japan’s 10-year bonds, anticipating a significant narrowing of the yield spread between the two tenors.

In an interview with media outlets in Singapore, Seidner remarked, “There is an additional risk premium embedded here that is attractive from both an absolute standpoint and relative to many other government bond markets.”

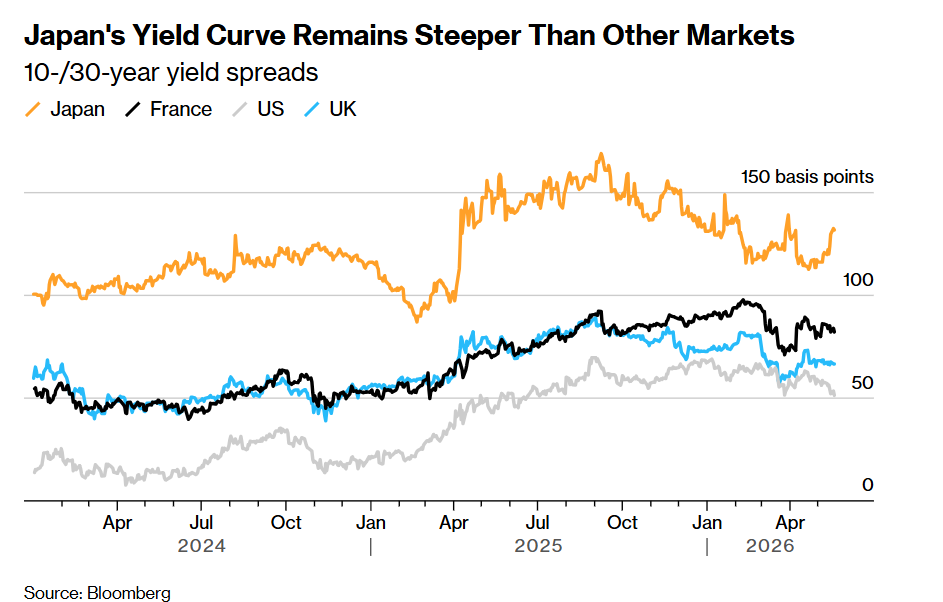

As illustrated in the chart above, Japan’s government bond yield curve remains steeper than those of other sovereign markets—the spread between 10-year and 30-year yields. Japan’s yield curve is the steepest among developed markets, reflecting investor concerns over persistently elevated domestic inflation—fueled by the country’s heavy reliance on Middle Eastern energy imports—and perceived delays in the Bank of Japan’s policy normalization, as well as growing unease about the nation’s long-term fiscal spending plans. This week, Japanese Prime Minister Sanae Takaichi called for supplementary budget measures to cushion the adverse impacts of rising energy and commodity prices, further exacerbating these concerns.

According to institutional data, the current yield spread between Japan’s 10-year and 30-year government bonds stands at approximately 130 basis points—significantly lower than the peak of 171 basis points recorded in September, yet still notably wider than the U.S. spread of just 52 basis points and the UK’s 67 basis points.

Seidner stated that the spread between Japan's 10-year and 30-year yields has already begun to narrow. 'It has normalized to some extent. It remains one of the steepest yield curves globally, which is why we continue to hold 30-year Japanese government bonds,' he said.

'With Japan’s economy and inflation growing faster than expected, this suggests the Japanese government bond market may face further pain,' said Mark Cranfield, a Markets Live strategist at Bloomberg Strategists.

Yields on Japan’s super-long-term government bonds fell on Wednesday—lower yields imply higher prices—following strong demand at the auction of 20-year JGBs. The yield on the 20-year bond declined by 5 basis points, while the 30-year yield dropped by 6.5 basis points.

The market has been discussing potential drivers that could further flatten Japan’s yield curve, with factors such as additional rate hikes by the Bank of Japan, easing fiscal concerns, and improved investor sentiment all seen as possible catalysts. Seidner remarked that it 'could be a bit of all of the above.'

Japan’s economy grew significantly faster than expected at the start of this year, bolstering the case for further rate hikes by the Bank of Japan. A member of the central bank’s policy board also called for raising interest rates as soon as possible, provided there are no signs of economic distress.

Japanese government bonds have underperformed their global peers overall, with a Bloomberg index tracking local-currency bond returns down 4.1% this year, compared with a 1.7% decline in the global benchmark index.

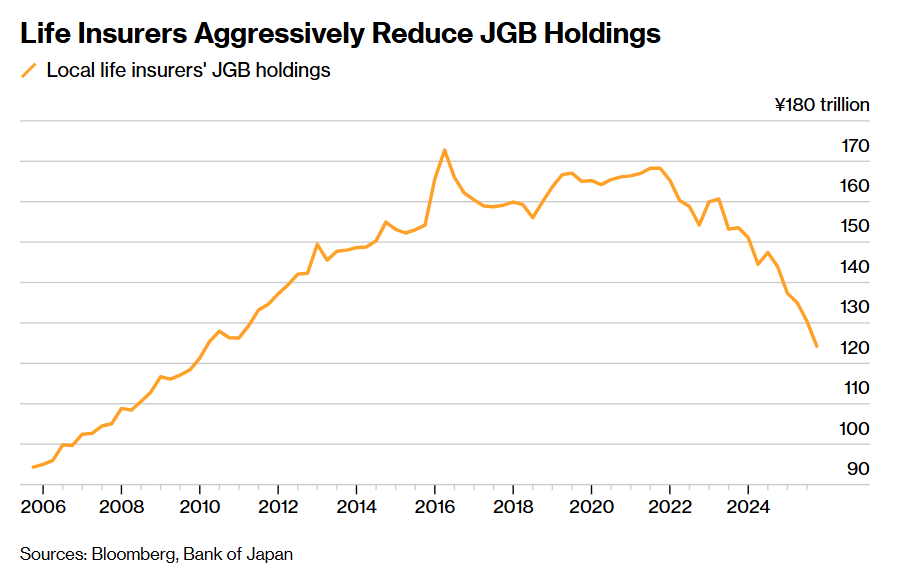

Foreign investors have started withdrawing from Japan’s super-long-term government bonds. Life insurers, historically among the largest buyers of Japanese bonds, have also been cutting back on purchases, adding pressure on longer-dated securities. As shown in the chart above, major Japanese life insurers—long-standing top holders of JGBs—have significantly reduced their holdings of Japanese government bonds.

'In our view, this truly creates an interesting investment opportunity and an attractive valuation entry point to go overweight on some 30-year Japanese government bonds,' Seidner said. 'We believe long-duration and super-long-duration bonds look quite compelling.'

With 38 years of experience in financial markets, Seidner helps PIMCO manage over USD 36 billion in assets, including the firm’s Dynamic Bond Fund. According to institutional data, this fixed-income fund has outperformed approximately 90% of its peers over the past year, delivering a return of 6.1%, compared with a gain of about 2.4% for the Bloomberg Global Aggregate Total Return Index over the same period.

From 5% U.S. Treasuries to 4% Japanese government bonds—the market may have priced in the rate-hike narrative too aggressively.

Market expectations that 'global central banks are about to re-enter a sustained hiking cycle' may be overly aggressive, but the reassessment that 'longer-dated government bonds require higher risk premia' may not be entirely excessive.

With the U.S. 30-year yield briefly approaching 5.18%, nearing its highest level since 2007, and Japan’s 30-year yield surpassing 4%—a first since the maturity was introduced in 1999—PIMCO’s positioning of being long Japanese 30-year JGBs and short 10-year JGBs does not fundamentally deny inflation risks. Rather, it reflects the view that the 10s/30s yield spread in Japan, at approximately 130 basis points, remains significantly wider than the comparable spreads in the U.S. (about 52 bps) and the U.K. (about 67 bps), implying that the ultra-long end has already priced in an 'excess risk premium' due to fiscal concerns, inflation fears, reduced demand from life insurers, and foreign investor outflows.

In other words, PIMCO is betting on a flattening trade in the Japanese government bond yield curve following an oversteepening, as well as on market expectations for inflation and the path of rate hikes being excessively hawkish.

Markets are currently embedding short-term energy-driven inflation risks, long-term fiscal concerns, and uncertainty around central bank reaction functions all at once into long-end yields. The Japanese government bond market is particularly illustrative: stronger-than-expected domestic inflation and economic growth, the possibility of further rate hikes by the Bank of Japan, additional government budget spending exacerbating fiscal worries, and reduced allocations to ultra-long JGBs by life insurers have collectively steepened the yield curve. However, when the 30-year yield offers excessive compensation relative to the 10-year, fixed-income investors like PIMCO conclude that pricing has become overly pessimistic and opt to hold ultra-long-dated Japanese government bonds.

Near-term market panic over inflation and a hawkish central bank trajectory may be exaggerated, but the shift in global long-end rates from the era of persistently low rates to one characterized by higher term premia is not entirely misplaced. If oil prices have peaked temporarily, U.S.-Iran tensions ease, and inflation expectations remain anchored, the Federal Reserve and the Bank of Japan are unlikely to hike rates mechanically and consecutively, allowing ultra-long bonds to recover. However, as long as elevated fiscal deficits, increased sovereign debt supply, central bank balance sheet runoff, and insufficient demand from long-term investors persist, long-end yields are unlikely to return to the low-volatility, low-rate regime of the past decade.

Moreover, for equity risk assets tied to the AI computing infrastructure supply chain, this implies that the window for a tech stock rebound hinges on whether long-end yields stabilize or decline—not merely on whether there will be 'one more rate hike.' For risk assets, a retreat in long-end yields would provide relief to technology and high-valuation growth stocks. Yet as long as global fiscal deficits, energy shocks, AI-related capital expenditure financing needs, and central bank quantitative tightening continue, long-end bond yields are unlikely to revert to the low-volatility, low-rate environment seen over the past ten years.

In stark contrast to economists’ views, bond markets at one point priced in a Fed rate hike within the year. Economists remain relatively dovish on the interest rate outlook overall, continuing to regard the inflation spike triggered by soaring energy prices—since the outbreak of conflict involving Iran two and a half months ago—as transitory and unlikely to spill over broadly into other consumer prices. In a survey conducted from May 14 to 19 involving 101 economists, nearly 85% (83 respondents) expect the policy rate to remain unchanged in the 3.50%–3.75% range through the third quarter. By comparison, just over half held this view last month, and nearly 70% in March expected at least one rate cut by then.

Regarding the year-end policy rate level, economists have yet to reach a clear consensus. However, nearly half (49 out of 101) now expect the Fed to make no rate changes this year—a proportion higher than the roughly one-third seen previously. Nearly one-third anticipate a single rate cut this year, mostly in December. Only four economists forecast a rate hike before December.

Editor/Deng