According to a report by Guotai Junan and Haitong Securities, market expectations that Waller would drive monetary easing and push down U.S. Treasury yields have significantly overestimated the Federal Reserve's policy capacity. Domestically, the United States faces a triple structural constraint of persistent inflation, fiscal deficits, and an AI-driven asset bubble; externally, it is continually undermined by global supply chain realignment, spillovers from monetary easing by major trading partners, and the declining reserve currency status of the U.S. dollar. Regardless of the Fed’s actions, a steeper yield curve has become the most probable outcome.

Resurgent inflationary pressures have driven global bond yields to multi-year highs. The yield on the U.S. 30-year Treasury note reached 5.18%, its highest level since 2007, while the 10-year yield rose to 4.66%, marking a new high since January 2025.

Markets had anticipated that Kevin Warsh’s appointment as Federal Reserve Chair would usher in a dovish monetary policy shift, thereby lowering U.S. Treasury yields. However, a recent report by Cathay Securities and Haitong Securities argues that this expectation significantly overestimates the Fed’s policy maneuvering room.

The report contends that the U.S. currently faces three structural domestic constraints—inflation stickiness, expanding fiscal deficits, and an AI-driven capital bubble—leaving the Federal Reserve with far less policy space than markets assume. Simultaneously, three external pressures—the ongoing restructuring of global supply chains, spillover effects from monetary easing by key trading partners, and the continued erosion of the U.S. dollar’s status as the dominant global reserve currency—are further undermining the external conditions necessary for lower Treasury yields.

The report contends that the U.S. currently faces three structural domestic constraints—inflation stickiness, expanding fiscal deficits, and an AI-driven capital bubble—leaving the Federal Reserve with far less policy space than markets assume. Simultaneously, three external pressures—the ongoing restructuring of global supply chains, spillover effects from monetary easing by key trading partners, and the continued erosion of the U.S. dollar’s status as the dominant global reserve currency—are further undermining the external conditions necessary for lower Treasury yields.

Against this backdrop, regardless of who serves as Fed Chair, the scope for long-end rates to decline is extremely limited, making a steepening yield curve the most probable trajectory.

Domestic Constraints: The Triple Bind of Inflation, Fiscal Deficits, and the AI Bubble

Three structural domestic constraints in the United States have significantly narrowed the Federal Reserve’s policy space.

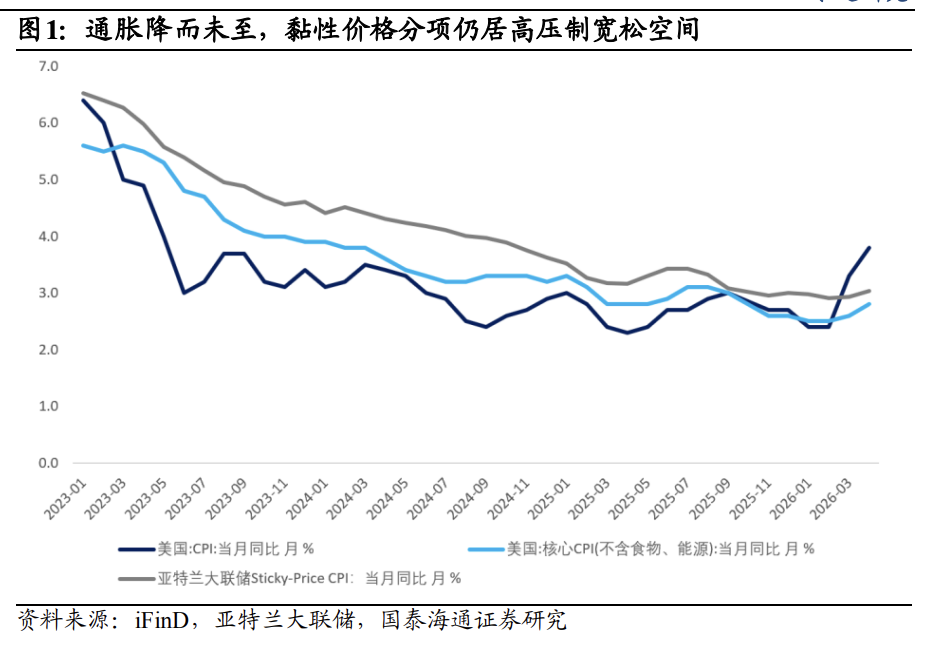

Inflation stickiness continues to intensify. In April 2026, U.S. headline CPI rose 3.8% year-over-year, while core CPI increased by 0.4% month-over-month—the largest single-month gain so far this year. The Atlanta Fed’s sticky-price CPI measure registered an annualized rate of 4.6%, with the core version jumping to 4.8%, indicating that inflationary pressures have deeply permeated slow-moving components such as rents and services. Market consensus forecasts suggest May’s CPI could surpass 4% year-over-year, making re-accelerating inflation the baseline scenario. Under these conditions, premature rate cuts would struggle to secure internal political support within the FOMC and would risk damaging the Fed’s credibility.

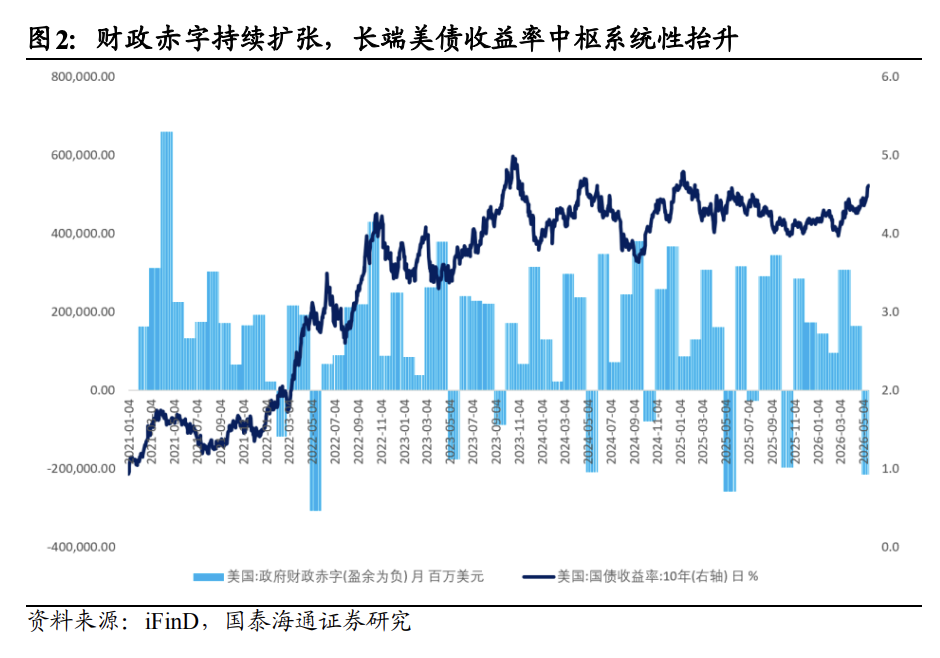

Expanding fiscal deficits are exacerbating upward pressure on long-end yields. The federal deficit for fiscal year 2025 has already reached $1.8 trillion, and large-scale tax reforms and spending plans over the next decade are projected to add more than $3 trillion to the deficit. The Treasury Department has significantly increased issuance of Treasury securities, with short-end T-bill supply potentially surging by over $1 trillion in the second half of the year. Subsequent issuance pressure from longer-duration coupon-bearing bonds will feed through to long-end yields. With persistently rising supply and no marginal increase in demand, long-end rates face structurally higher levels. Even if the Fed cuts rates, the 10-year Treasury yield may not necessarily follow downward, as monetary policy transmission has been substantially weakened by fiscal pressures.

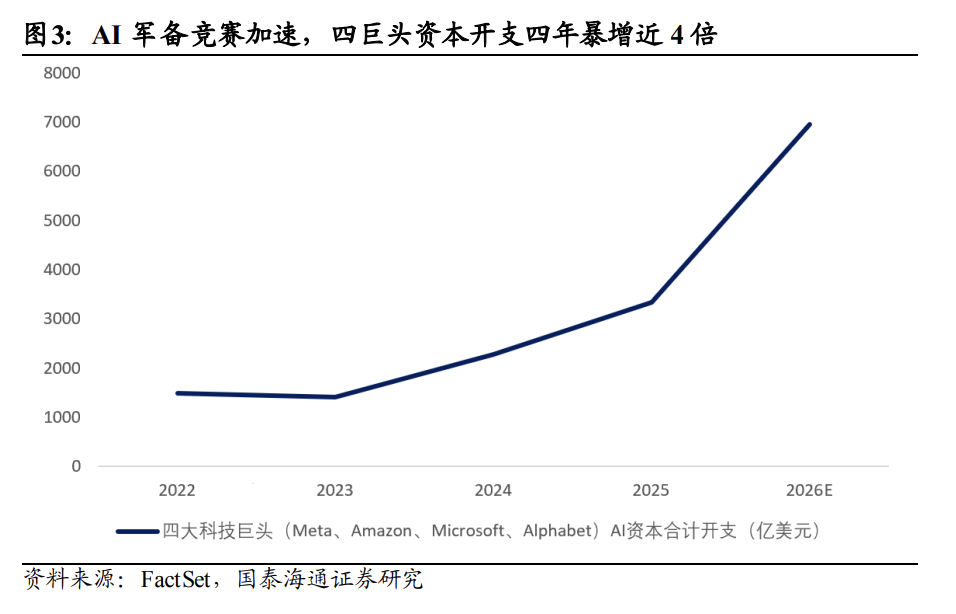

The AI bubble is fueling both inflation and market risk. In 2025, the combined AI-related capital expenditures of the four largest tech firms amounted to approximately $410 billion—about 1.3% of U.S. GDP—and are expected to rise to 1.6% in 2026. Narrative-driven, massive capital outlays in AI are pushing up prices for energy, land, and advanced manufacturing capacity. The S&P 500 is trading at roughly 23 times forward earnings, approaching valuation levels seen during the early-2000s internet bubble. This investment boom in the real economy continues to stoke inflationary pressures, and should the bubble burst, the Fed would face a dilemma between stabilizing markets and curbing inflation. Merely replacing the Fed Chair is unlikely to achieve a broad-based downward shift in the yield curve.

External Erosion: Diminishing U.S. Pricing Power Amid Global Supply Chain Restructuring

Global structural forces are also undermining the downside foundation for long-end U.S. Treasury yields along three dimensions.

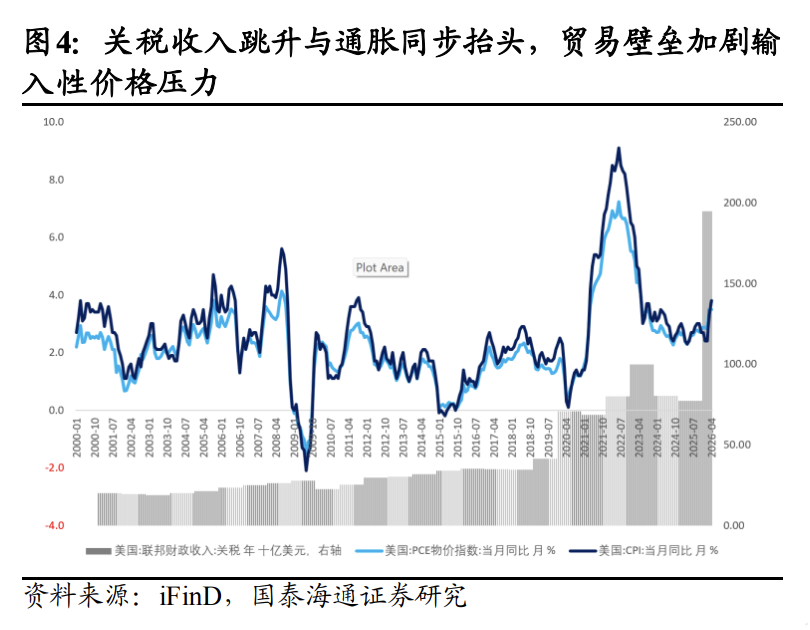

Tariffs are reshaping supply chains and elevating the inflation baseline. Excluding low-cost sources from global supply chains has forcibly raised the global cost base for production. According to data from the Federal Reserve Bank of St. Louis, between June and August 2025, tariffs contributed approximately 0.5 percentage points to annualized U.S. PCE inflation; over the 12 months ending in August 2025, tariffs accounted for 10.9% of total PCE inflation. The transmission mechanism that 'tariffs equal inflation' has now been robustly validated by empirical data.

Exchange rate volatility amplifies reflation risks. Major manufacturing economies have responded to trade tensions with monetary easing, leading their currencies to depreciate and export exchange rate volatility and commodity price pressures globally. Alternative supplier countries face longer capacity build-out cycles and higher costs, which in the short term further magnify global goods reflation risks. The International Monetary Fund notes that tariffs represent a supply shock for the United States but a demand shock for other economies, resulting in increasingly divergent inflation dynamics and significantly complicating global central bank policy coordination.

The U.S. dollar’s reserve currency status is eroding, weakening external demand for U.S. Treasuries. The dollar’s share in global official foreign exchange reserves has declined from around 71% at the start of the century to approximately 56% today—the lowest level in nearly two decades. Central banks worldwide are accelerating reserve diversification, steadily increasing strategic allocations to gold, the euro, and emerging market currencies. Marginal buying by foreign central banks is waning, leaving long-end U.S. Treasuries with increasingly thin demand support. Even the Federal Reserve’s own research acknowledges that if market confidence in U.S. debt-servicing capacity or monetary stewardship falters, demand for dollar-denominated assets could face deeper erosion.

TACO is unlikely to alter the broad interest rate trajectory; a steeper yield curve is the most probable path forward.

The term 'TACO' (Trump Always Chickens Out) describes a recurring pattern wherein markets plunge following Trump’s announcement of aggressive tariff measures, only for the White House to subsequently soften its stance and risk assets to rebound. After the 2025 postponement of tariffs on the European Union, the S&P 500 rose more than 2% in a single day, while the 30-year U.S. Treasury yield simultaneously approached 5% again. The bond market’s message is clear: tariff concessions cannot resolve fiscal deficits, sticky inflation, or supply-side pressures—these remain the core determinants of long-end pricing.

Regardless of the policy path pursued by the Federal Reserve under Waller, a steeper yield curve remains the most likely outcome.

Scenario one: continued rate cuts. Short-end rates decline alongside the federal funds rate, while long-end yields—constrained by fiscal issuance and inflation risk premiums—lag significantly, resulting in a bull-steepening curve. Since the Fed initiated its easing cycle in September 2024, the 10-year Treasury yield has risen rather than fallen, climbing from 3.65% to a peak of 4.79% in January 2025.

Scenario two: accelerated easing. If the Fed is pressured politically to quicken its pace of accommodation, markets may question its independence, prompting a repricing of inflation expectations and further upward pressure on the term premium of long-end yields. The current 10-year term premium has already reached its highest level since 2011.

Overall, placing a one-sided bet on a sharp decline in the 10-year Treasury yield offers very poor risk-reward under the current macro framework. In contrast, steepener trades such as 2s10s or 5s30s present a more compelling logic—they benefit both from expectations of short-end rate cuts and from long-end pressures driven by fiscal supply and inflation risk premiums, offering a clearly superior risk-return profile. Trump’s TACO behavior may create tactical opportunities for temporary long positions, but this constitutes tactical positioning rather than a strategic shift in direction.

Editor/melody