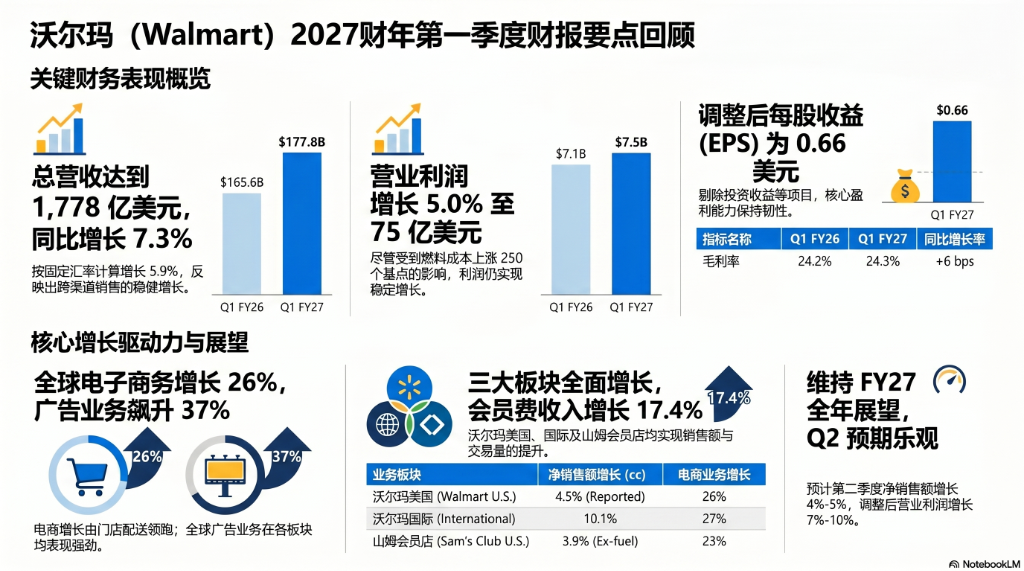

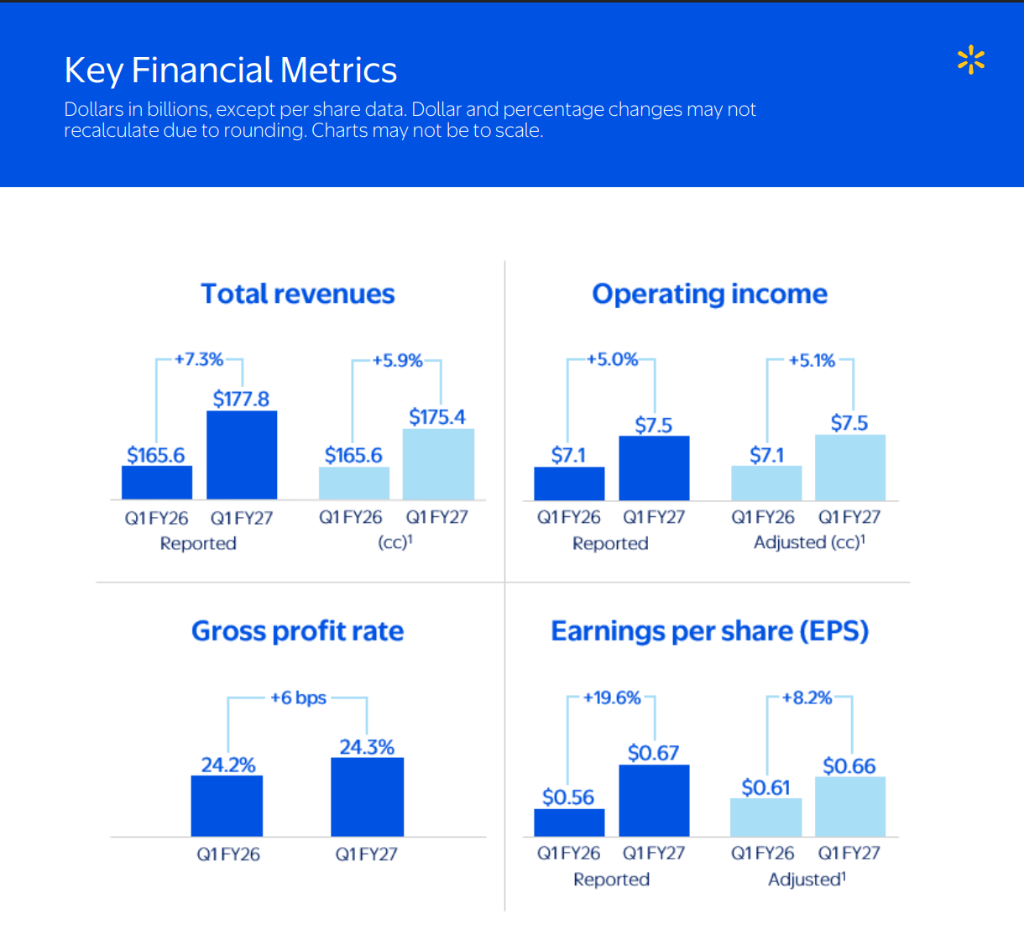

Walmart reported total revenue of $177.8 billion for Q1 FY27, an increase of 7.3% year-over-year, slightly exceeding expectations; adjusted earnings per share (EPS) were $0.66, in line with expectations.

Global e-commerce sales grew by 26%, and advertising revenue surged by 37%, as high-margin businesses continued to optimize the profit mix. However, higher fuel costs reduced operating profit growth by 250 basis points, and the company chose to absorb these costs internally without passing them on to consumers.

On May 21, $Walmart (WMT.US)$Walmart released its first-quarter FY27 earnings report, reporting total revenue of $177.8 billion, an increase of 7.3% year-over-year, exceeding the market estimate of $175.06 billion. Adjusted earnings per share came in at $0.66, in line with market expectations. However, the company provided second-quarter adjusted EPS guidance of $0.72 to $0.74, below the market estimate of $0.75, causing Walmart’s U.S.-listed shares to fall nearly 3% in pre-market trading. During regular trading hours, the stock dropped nearly 7%, closing at $121.81.

During the quarter, comparable sales in the U.S. (excluding fuel) rose by 4.1%, slightly exceeding expectations. Global e-commerce sales increased by 26% year-over-year, spanning Walmart U.S., international operations, and Sam’s Club. Global advertising revenue surged by 37%, while membership fee income grew globally by 17.4%. These two high-margin businesses are becoming key drivers in optimizing Walmart’s profit structure.

During the quarter, comparable sales in the U.S. (excluding fuel) rose by 4.1%, slightly exceeding expectations. Global e-commerce sales increased by 26% year-over-year, spanning Walmart U.S., international operations, and Sam’s Club. Global advertising revenue surged by 37%, while membership fee income grew globally by 17.4%. These two high-margin businesses are becoming key drivers in optimizing Walmart’s profit structure.

Operating profit rose 5.0% year-over-year to USD 7.493 billion, though this growth lagged behind revenue growth, primarily due to higher fuel costs. Increased fuel expenses in distribution and fulfillment negatively impacted operating margin by 250 basis points. CFO John David Rainey stated that the company 'absorbed almost all' of the fuel cost increases during the quarter and expects similar or even greater challenges in the current quarter.

Looking ahead to the second quarter,$Walmart (WMT.US)$The company expects net sales growth of 4% to 5% on a constant currency basis and adjusted operating profit growth of 7% to 10%. Full-year FY27 guidance remains unchanged: net sales growth of 3.5% to 4.5%, adjusted operating profit growth of 6% to 8%, and adjusted EPS of $2.75 to $2.85.

Walmart U.S.: Dual Engines of E-commerce and Advertising

As$Walmart (WMT.US)$the core business segment, Walmart U.S. generated net sales of $117.2 billion this quarter, up 4.5% year-over-year; comparable sales (excluding fuel) rose by 4.1%. A more notable structural shift lies in the fact that transaction count increased by 3.0%, while average ticket size rose only marginally by 1.1%—indicating that growth was driven not by inflation-driven price increases but by sustained improvement in traffic quality, reflecting genuine market share gains.

E-commerce was the undisputed growth engine, with sales rising 26% and contributing approximately 530 basis points to comparable sales—significantly higher than the 350 basis points contribution in the same period last year. Store-fulfilled delivery emerged as the core driver, while the third-party marketplace also maintained strong expansion momentum. E-commerce is not only boosting sales but also reshaping Walmart’s cost structure.

Advertising revenue also posted robust growth, increasing by 36% overall. Excluding VIZIO, revenue from the Walmart Connect platform surged by 44%, underscoring the continued monetization potential of its Retail Media Network as a high-margin business. Membership fee income recorded double-digit growth, with net new memberships in the first quarter reaching a record high for the period—demonstrating accelerating user adoption of Walmart+.

Profitability showed mixed results. Gross margin improved by 29 basis points, primarily driven by ongoing optimization of business and product mix—the rising share of high-margin businesses such as advertising, memberships, and third-party marketplace is enhancing the quality of Walmart’s revenue. However, operating expense ratio increased by 56 basis points year-over-year (i.e., operating deleverage), mainly due to higher depreciation expenses and rising employee healthcare costs.

Adjusted operating profit rose 5.7% to USD 6.023 billion, supported by improved e-commerce economics, membership growth, and contributions from other income streams. Inventory levels increased by 8.0%, primarily due to timing of receipts and heightened stocking needs driven by accelerated grocery sales. Management indicated that overall inventory quality remains healthy, with no risk of overstocking.

International Business: Favorable Foreign Exchange Tailwinds Accelerate Growth, with E-commerce and Advertising Flourishing Across the Board

$Walmart (WMT.US)$International segment net sales reached $35.1 billion this quarter, up 18.0% on a reported basis and 10.1% on a constant currency basis, with foreign exchange fluctuations contributing approximately $2.3 billion in positive impact. Operating profit on a constant currency basis increased by 10.2% to $1.425 billion.

Operationally, transaction counts and units sold increased across all major markets. Global e-commerce sales grew by 27%, with digital sales penetration rising in every market, and store-based fulfillment models continuing to advance. Advertising revenue surged by 32%, primarily driven by Flipkart’s sustained strong performance. Narrowing e-commerce losses and ongoing business portfolio optimization jointly contributed to improved operating profit.

Fuel Costs: A 250-Basis-Point 'Profit Assassin'

Fuel costs were the largest drag on Walmart’s profitability this quarter.

The company stated that rising fuel expenses at distribution centers and within its fulfillment network negatively impacted operating profit growth by 250 basis points, primarily due to geopolitical conflicts driving up diesel and gasoline prices. Walmart chose to absorb these costs internally. CFO Rainey noted that the company 'absorbed nearly all' of the fuel cost increases in the first quarter and did not pass them on to consumers through higher prices.

As a result of this decision, Walmart U.S. revenue grew by 4.5%, while operating profit increased by only 3.5%. Excluding fuel-related and other adjustments, adjusted operating profit growth stood at 5.7%. Rainey expects fuel cost pressures in the second quarter to be 'flat or potentially greater.'

Editor/melody