Global asset management giant BlackRock has put forward a view that diverges from the current market consensus, arguing that under incoming Federal Reserve Chair Kevin Warsh, the Fed may have sufficient grounds to opt for interest rate cuts rather than hikes.

Zhitong Finance APP learned that global asset management giant BlackRock has put forward a view that diverges from current market consensus, suggesting that under new Federal Reserve Chair Kevin Warsh, the Fed may have sufficient grounds to cut rates rather than hike them. When asked about the likelihood of rate hikes under Warsh, Neeraj Sethi, Head of Global Fixed Income for Asia Pacific at BlackRock, stated: “If you force me to choose between a rate hike and a rate cut, I believe there are already enough factors supporting a rate cut.” He added, “Looking ahead, the labor market will face some pressure, which could mean the Fed either holds steady or opts to cut rates.”

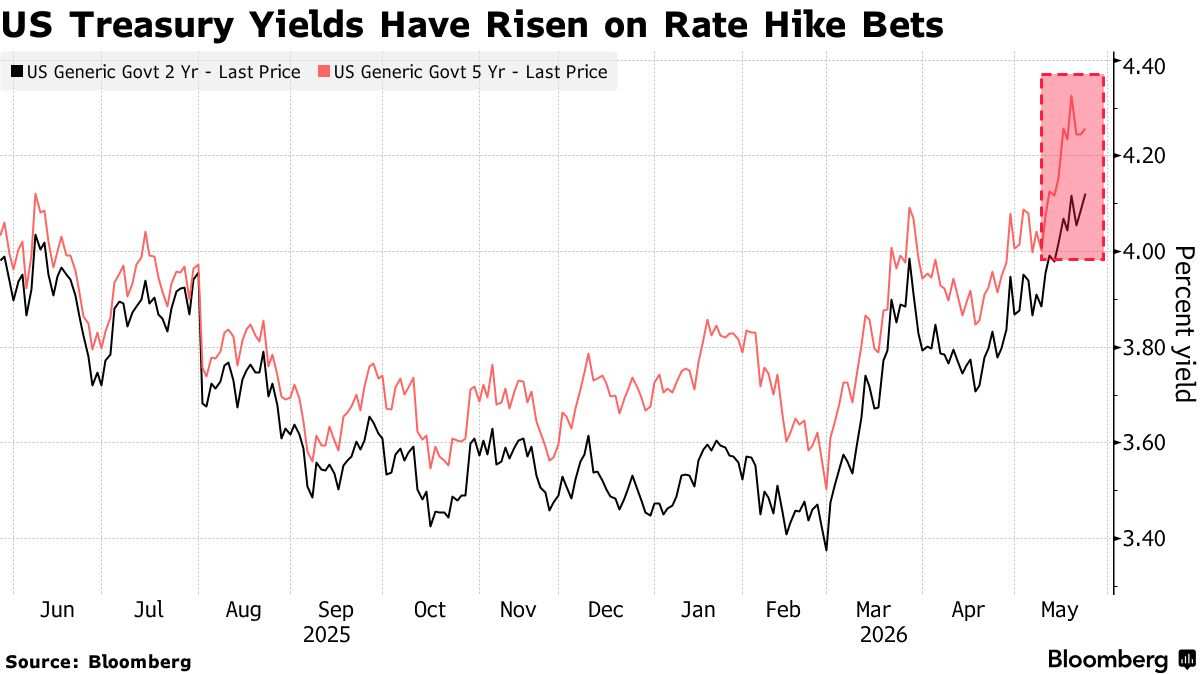

Sethi’s comments stand in stark contrast to the prevailing expectations among bond investors, who largely bet that Warsh would prioritize safeguarding the Fed’s credibility in fighting inflation over accommodating U.S. President Trump’s calls for lower interest rates. Meanwhile, rising expectations of inflation—fueled by Middle Eastern conflicts pushing up fuel and other raw material prices—have further strengthened investor bets that the Fed will raise rates to contain inflation. Current market pricing indicates near certainty that the Fed will hike rates by December. The yield on the U.S. two-year Treasury note, which is highly sensitive to monetary policy shifts, has climbed to 4.12% as of last Friday from a March low of 3.36%, reflecting this shift in market sentiment.

However, according to Sethi, while the U.S. economy benefits from certain tailwinds—such as the surge in AI investment—the labor market could face pressure in the future. He noted that the current strength of the U.S. economy is partly driven by massive corporate investments in AI, much of which ultimately aims to replace human labor with machines or software. He remarked, “In an environment where it’s uncertain whether the economy will strengthen or weaken over the next year, the safest course of action might be to do nothing at all.”

However, according to Sethi, while the U.S. economy benefits from certain tailwinds—such as the surge in AI investment—the labor market could face pressure in the future. He noted that the current strength of the U.S. economy is partly driven by massive corporate investments in AI, much of which ultimately aims to replace human labor with machines or software. He remarked, “In an environment where it’s uncertain whether the economy will strengthen or weaken over the next year, the safest course of action might be to do nothing at all.”

Sethi’s core argument—that the Fed may soon have room to cut rates—aligns with the view of Kevin Hassett, Director of the White House National Economic Council. However, Hassett bases his outlook for potential Fed rate cuts on declining energy prices. Over the past weekend, Hassett stated that if a deal between the U.S. and Iran to reopen the Strait of Hormuz—a critical global energy transit chokepoint—is finalized, oil prices would drop sharply. Lower energy costs, he argued, could significantly ease inflationary pressures and thereby create more room for the Fed under Warsh to cut rates.

Hassett also pointed out that beyond falling energy prices, other disinflationary trends could eventually make Fed rate cuts justified. He stated, “Many forces are exerting downward pressure on prices,” citing AI-driven productivity gains and a “massive and unprecedented boom in AI-related capital expenditures.”

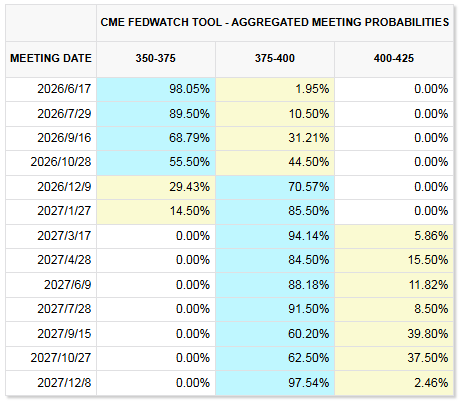

Market expectations for a Fed rate hike continue to intensify.

For now, however, the dominant market view remains that the Fed will tighten monetary policy. The CME Group’s 'FedWatch Tool' shows traders are betting that the Fed will most likely implement a 25-basis-point rate hike by December this year.

Data released earlier this month confirmed ongoing inflationary pressures in the U.S. economy. Driven by persistently rising gasoline prices due to the Middle East conflict and a sharp increase in grocery costs, U.S. inflation continued to accelerate, with the Consumer Price Index (CPI) rising 3.8% year-over-year in April—the fastest pace since 2023. Meanwhile, the Producer Price Index (PPI) surged 1.4% month-over-month in April, marking the largest single-month increase since March 2022 and far exceeding the market expectation of 0.5%. On an annual basis, PPI rose 6.0%—the highest since December 2022 and significantly above the market forecast of 4.8%.

At the same time, the hawkish faction within the Federal Reserve is growing. Last month’s FOMC meeting saw the highest level of dissent since 1992, with as many as three officials voting against a policy statement perceived as leaning toward easing. Meeting minutes revealed that, against the backdrop of Middle East tensions driving up energy prices and reigniting inflation concerns, the Fed is clearly shifting toward a more hawkish stance. Most officials believe that current high interest rates may need to be maintained longer than previously anticipated, and that further rate hikes could even be necessary if inflation remains persistently above the 2% target.

Several Fed officials have recently sent hawkish signals. Last week, Philadelphia Fed President Susan Bostic—who will be a voting member of the Federal Open Market Committee (FOMC) in 2026—stated she favors holding rates steady and believes rate cuts would only be appropriate if sustained progress is made in curbing inflation. She said, “Current monetary policy is mildly restrictive, and this restrictiveness is helping to contain inflationary pressures while the labor market remains stable.” She added, “Maintaining rates unchanged allows us to assess how the economy evolves and evaluate risks to both price stability and the labor market.” Bostic noted that the unemployment rate has remained “unusually stable,” indicating the labor market is “essentially in balance,” and emphasized that inflation was already too high even before the Middle East conflict pushed up energy prices. She concluded, “Assuming the labor market remains balanced, rate cuts would only become appropriate once we see sustained progress on inflation.”

Federal Reserve Governor Christopher Waller explicitly stated that the Fed needs to send a clear signal to markets that, in the future path of interest rates, the probabilities of 'rate hikes' and 'rate cuts' are currently perfectly balanced. Waller warned that if inflation does not return to a downward trajectory in the near term, he would not rule out the possibility of further rate hikes. He also expressed support for removing the current language in future policy statements that implies a 'dovish bias.' Waller emphasized that the inflation outlook remains the most critical factor determining the direction of monetary policy. He noted that should signs emerge indicating that longer-term inflation expectations are becoming 'unanchored,' he would not hesitate to support raising the target range for the federal funds rate.

Additionally, Kansas City Fed President Jeffrey Schmid stated that inflation poses the greatest risk to the U.S. economy. Minneapolis Federal Reserve Bank President Neel Kashkari remarked that the war in the Middle East has exacerbated already elevated inflation, and the Fed must bring inflation back to its 2% target. Boston Fed President Susan Collins also cautioned that if inflationary pressures persist without relief, the Fed may need to raise rates again. Chicago Fed President Austan Goolsbee pointed out that inflation is moving in the wrong direction—and this adverse trend extends beyond oil-related factors and tariff-related factors alone. These officials’ emphasis on inflation collectively signals that the Fed is keeping the door open to potential rate hikes.

Now officially at the helm of the Federal Reserve, Kevin Warsh will preside over his first FOMC meeting as chair in mid-June, which will serve as a crucial window for investors to assess his policy stance. Market participants note that Warsh assumes leadership at a time when the Fed faces one of its most complex policy environments in recent years: on one hand, Middle Eastern conflicts are pushing up oil prices and reigniting inflationary pressures; on the other, U.S. economic growth is slowing, while Trump continues to urge the Fed to cut rates promptly.

As market concerns about inflation intensify, if Warsh adopts an increasingly hawkish stance, it could further reshape market expectations—suggesting that the Fed may need to raise rates in the coming months or, at best, maintain the current rate level for an extended period. Economists at TS Lombard stated, 'Given rising inflation risks, holding rates steady in June would effectively amount to a dovish policy move.'

Analysts note that the expansion of the hawkish faction within the Federal Reserve, coupled with inflationary pressures stemming from the Middle East conflict, is reshaping market expectations regarding U.S. monetary policy. Although Warsh himself has previously expressed a desire to achieve rate cuts while maintaining control over inflation, the prevailing sentiment within the Fed has clearly shifted from 'when to cut rates' to 'whether another rate hike is necessary.'

Editor/Deng