UBS Group believes the core thesis lies in the divergence between market pricing and fundamentals, which is precisely the source of excess returns.

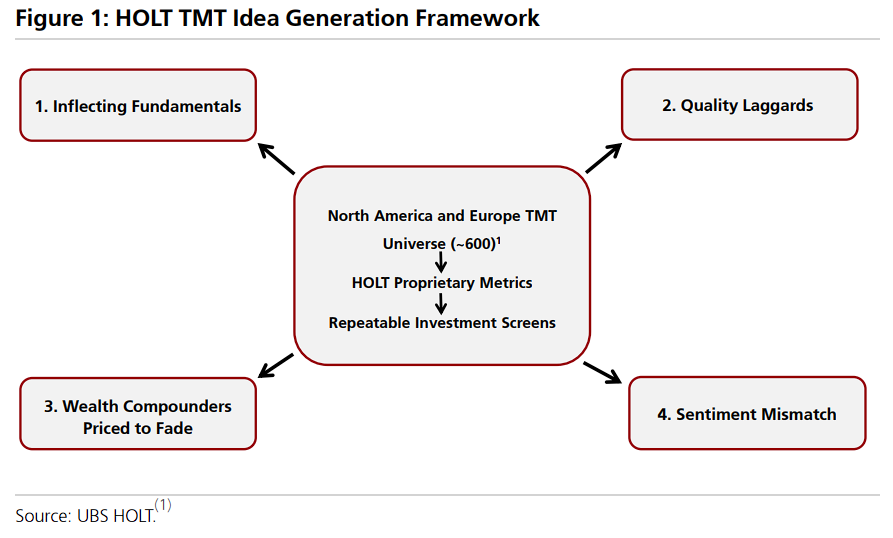

The bank has identified four key investment opportunities from a universe of 600 technology and communications companies: 1. Fundamental inflection points (exemplified by Broadcom, with an expected cash flow return on investment [CFROI] exceeding 80% by 2027); 2. High-quality laggards (exemplified by Accenture, trading at a valuation discount that is the widest in history); 3. Wealth compounding machines mispriced as being in secular decline (exemplified by Microsoft); and 4. Sentiment-misaligned stocks (exemplified by Amphenol).

As the Nasdaq index hits a new all-time high, elevated market valuations have left investors grappling with the classic dilemma of 'fear of missing out amid concerns over buying at peak levels.' However, this does not mean opportunities have vanished—the key lies in identifying assets mispriced by the market.

On May 27, according to ZHU Feng Trading Desk, UBS Group’s HOLT team released a new objective quantitative screening framework that systematically identifies four categories of investment opportunities from approximately 600 technology and communication services (TMT) companies in North America and Europe: Inflecting Fundamentals, Quality Laggards, Wealth Compounders Priced to Fade, and Sentiment Mismatch.

On May 27, according to ZHU Feng Trading Desk, UBS Group’s HOLT team released a new objective quantitative screening framework that systematically identifies four categories of investment opportunities from approximately 600 technology and communication services (TMT) companies in North America and Europe: Inflecting Fundamentals, Quality Laggards, Wealth Compounders Priced to Fade, and Sentiment Mismatch.

This framework strips away market noise and directly targets the core drivers of cash flow return on investment (CFROI) and asset growth. The four screening criteria are distinct and cater to investors with different risk preferences. Representative stocks include$Broadcom (AVGO.US)$、$Accenture (ACN.US)$、$Microsoft (MSFT.US)$and$Amphenol (APH.US)$, all of which have received a "Buy" rating from UBS Group.

UBS Group’s core thesis is that significant divergence exists between market pricing and fundamental realities—a discrepancy that serves as the source of excess returns.

Inflecting Fundamentals: Seeking ‘Top Performers’ with Dual Upside from Momentum and Returns

At elevated market levels, identifying companies whose fundamentals are accelerating represents a core strategy aligned with prevailing trends.

This framework identifies companies exhibiting faster CFROI (Cash Flow Return on Investment) improvement than peers and strong momentum, while excluding those trading at valuations significantly above historical or peer-group averages. It caters to investors seeking accelerated capital returns and robust business momentum.

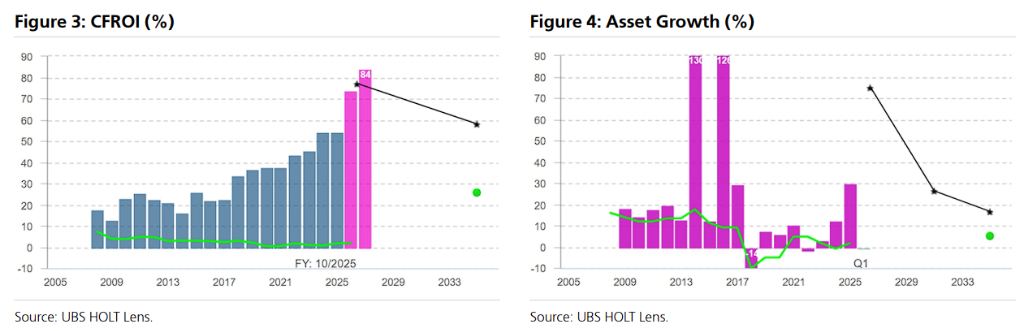

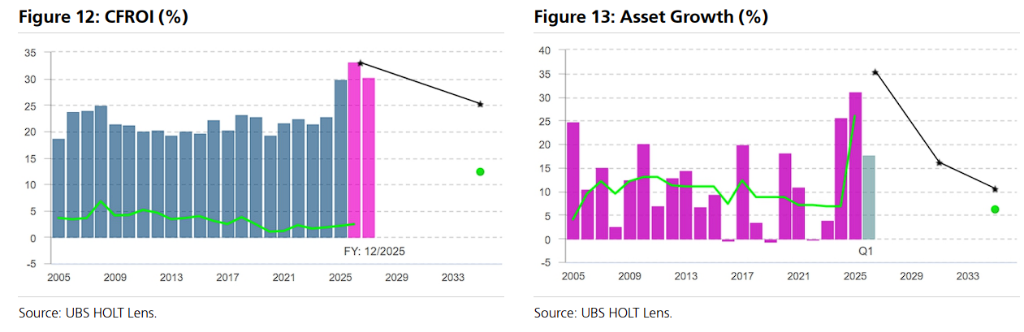

UBS Group’s 'Inflecting Fundamentals' model precisely targets assets with surging returns, using Broadcom as a case study. The firm notes that Broadcom’s leadership in ASIC chips is translating into strong earnings performance as inference—a critical component of AI workloads—grows increasingly important.

Data shows that,$Broadcom (AVGO.US)$Its CFROI is projected to exceed 80% by 2027, ranking 3rd within the entire technology sector and 5th globally among all companies.

Yet market pricing reflects a significant misjudgment: despite fundamentals having turned upward and reached new highs, the market continues to price Broadcom as if its CFROI will revert to pre-AI-era levels and its asset growth will remain in the mid-single digits.

Broadcom combines high quality, low embedded expectations, and exceptionally strong momentum—its CFROI upgrade magnitude ranks at the 100th percentile among U.S. technology stocks—making it a 'best-in-class' stock under this investment style.

High-Quality Value Stocks: Historically Rare Valuation Discounts from Market Overreaction

While market capital flows have poured into popular thematic concepts, some high-quality companies with proven long-term profitability have been indiscriminately sold off.

This framework focuses on companies that are high quality (with a CFROI forecast of at least 8%), have declined more than 5% year-to-date, and are trading below their historical valuation levels. The software and IT consulting sectors—due to market concerns over AI’s long-term impact—have become key areas of focus for this strategy.

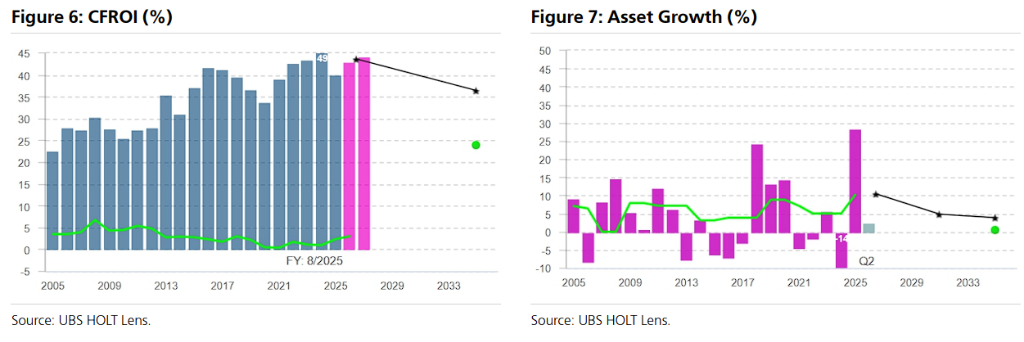

UBS Group’s screening criteria provide contrarian investors with an exceptional list of potential undervalued opportunities, with particular emphasis on$Accenture (ACN.US)$, noting that Accenture has consistently generated CFROI above 20% over the past two decades—a feat achieved by only 30 companies worldwide.

Recent consensus estimates indicate its CFROI will further rise to nearly 45%. However, investor concerns about disintermediation and margin pressure from emerging AI models have weighed heavily on sentiment, causing the stock to decline approximately 35% year-to-date.

From a valuation perspective, extreme pessimism has created a rare buying opportunity: measured by Economic P/E, Accenture currently trades at a discount to the market that is the widest on record; in absolute terms, the stock is now as cheap as it was during the depths of the 2009 financial crisis.

Wealth Compounding Machines Mispriced for Decline: Long-Term Value Amid Expectation Gaps

These companies are genuine 'cash-generating machines,' yet markets often misprice them for decline due to short-term increases in capital expenditures or excessive pessimism about the future—creating significant expectation gaps for long-term investors.

This framework identifies companies that have demonstrated high CFROI and high asset growth over many years, enabling them to compound economic profit at above-average rates, yet are mistakenly priced by the market as if their CFROI will decline over the long term.

UBS Group stated that Microsoft has demonstrated consistently exceptional operational performance over the past decade, with its CFROI increasing from approximately 15% in 2015 to over 25% last year.

Although CFROI is expected to moderate in the near term due to increased investments in AI infrastructure, its economic profit (EP) is still projected to rise by more than USD 25 billion by 2027.

Strong economic profit generation has been a hallmark of Microsoft’s value creation history, with only two years in the past two decades witnessing a material decline in economic profit. Despite this outstanding track record, the market remains skeptical about its current forecasted economic returns, pricing in a long-term CFROI erosion of nearly 900 basis points (900 bps).

This significant disconnect between fundamentals and market pricing underpins the core rationale for classifying Microsoft as a 'wealth compounding machine priced for decline.'

Sentiment Mismatch: Capturing the Divergence Between Fundamental Upgrades and Declining Share Prices

When analysts continuously revise a company’s earnings expectations upward while its share price continues to fall, it often indicates that market pricing has not fully reflected recent business momentum.

This framework identifies companies that have underperformed their regional benchmark by at least 10% over the past quarter while simultaneously experiencing upward revisions in CFROI expectations (analyst estimates). Such a mismatch between improving fundamentals and negative market sentiment serves as an excellent signal for identifying mispricing.

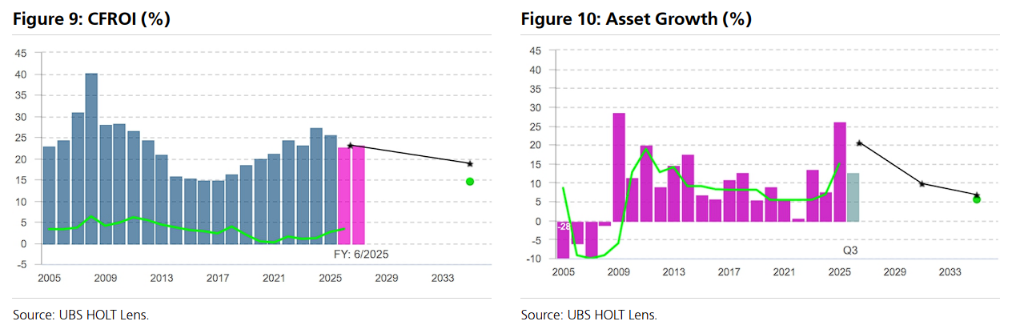

UBS Group stated that robust demand for high-speed interconnect systems from hyperscale cloud providers is driving this trend.$Amphenol (APH.US)$Its share price rose by approximately 100% in 2025. Despite continued strong consensus among analysts in raising their expectations, the stock has declined year-to-date, reflecting a shift in investor sentiment.

Market focus has now shifted to the risk side: concerns are mounting that Amphenol’s copper-based interconnect product portfolio could be overtaken by accelerating demand for optical solutions, as the company’s capabilities in optics are still perceived to be in a relatively early stage.

As the share price declines, its valuation has become increasingly attractive. The market is currently pricing in a CFROI level at its lowest point in over three decades, and Amphenol’s Market Implied Yield has reached a historical high, ranking it among the most attractive names in the technology hardware and equipment sector.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/melody