The Federal Reserve faces renewed challenges in its fight against inflation. April's PCE, driven by higher energy prices and semiconductor premiums, is expected to reach a three-year high of 3.8%. Price pressures are spreading across multiple sectors, potentially forcing the Fed to adopt a more hawkish stance and even reignite discussions on rate hikes.

At 20:30 Beijing time on Thursday, the Bureau of Economic Analysis (BEA) under the U.S. Department of Commerce will release the April Personal Consumption Expenditures (PCE) price index report. This inflation report—considered the Federal Reserve’s most closely watched gauge—is highly likely to show that inflationary pressures are not only persisting but also spreading into broader sectors.

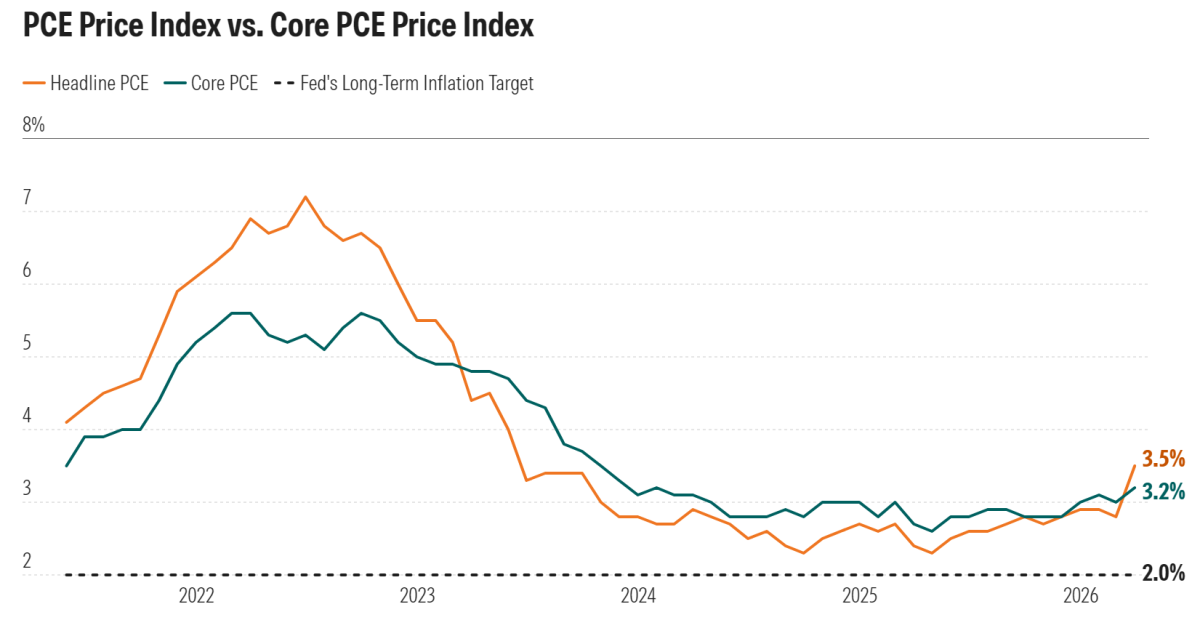

PCE and Core PCE Data

The market widely expects the year-over-year increase in the April PCE price index to rise to 3.8%, up from the previous reading of 3.5%, marking the highest level since June 2023. Even excluding the more volatile food and energy components, the core PCE annual rate is projected to edge up slightly to 3.3%.

The market widely expects the year-over-year increase in the April PCE price index to rise to 3.8%, up from the previous reading of 3.5%, marking the highest level since June 2023. Even excluding the more volatile food and energy components, the core PCE annual rate is projected to edge up slightly to 3.3%.

The month-over-month change in the April PCE price index is expected to come in at 0.5%, slowing from the prior month’s 0.7%; the core PCE monthly rate, excluding food and energy, is forecast to hold steady at 0.3%.

Last month’s report showed that energy prices were the ‘vanguard’ of this rebound—gasoline and other energy products surged nearly 21% month-over-month in March, with lingering effects still being felt. However, economists are even more concerned about inflation’s ‘contagiousness.’ Recent indicators suggest inflation is now spreading from energy into services and durable goods:

Food and logistics: Upstream fertilizer and logistics costs have been passed through the supply chain, leading to a marked acceleration in food price increases in April;

Travel costs: Pressure from jet fuel prices has compelled airlines to raise ticket prices, pushing airfare inflation higher for two consecutive months;

AI premium: A notable new factor is the surge in AI-related demand. Soaring demand for computing power has triggered a global shortage of memory chips, which in turn has driven up end-user prices for PCs and related hardware, adding further stickiness to inflation.

Preston Caldwell, Senior Economist at Morningstar, stated: ‘We thought we were nearing the “last mile” of inflation, but now it seems we’re heading in the opposite direction, with data even at risk of accelerating further.’

The resurgence in inflation data is fundamentally reshaping Wall Street’s policy expectations. Since May, a series of stronger-than-expected inflation readings has triggered significant volatility in the U.S. Treasury market, pushing the yield on the 30-year Treasury bond as high as 5.2%—its highest level since 2007.

Currently, CME Group's 'FedWatch' tool shows that although the market considers it highly likely the Fed will maintain its target rate range at 3.50%–3.75% in June, the proportion of bets on a rate hike by year-end is rising significantly.

Compared with the market’s pessimistic expectations, Goldman Sachs’ forecast appears somewhat more 'moderate.' Goldman Sachs expects April PCE prices to rise 0.44% month-over-month and 3.78% year-over-year—both slightly below the market consensus. David Mericle, Goldman Sachs’ chief U.S. economist, noted that this forecast model fully accounts for elevated oil prices, lingering effects of geopolitical conflicts, and inflationary pressures from AI-related demand—though he believes the inflationary impact of AI may be overstated or mismeasured.

Looking ahead, Goldman Sachs believes disinflation will take time, projecting core PCE inflation to remain around 3% in 2026 and overall inflation this year to stay below 4%.

Under new Fed Chair Kevin Warsh, the Federal Open Market Committee will face a difficult choice: whether to treat recent price increases as a 'one-off shock' and continue monitoring, or to adopt a decisive hawkish stance by raising rates again to prevent inflation expectations from becoming self-fulfilling.

Previously, markets had hoped the Federal Reserve would begin cutting rates this year. However, according to the latest Reuters survey, approximately 85% of economists now believe rates will remain unchanged until at least the third quarter, and a significant share of analysts have pushed back their rate-cut expectations to 2027.

Bank of America analysts argue that the Fed is currently in a 'wait-and-see' observation phase, but the policy balance has clearly tilted toward a hawkish bias. If Thursday’s data confirm that inflation has become entrenched across multiple sectors, discussions about 'rate hikes' will formally shift from market speculation to an actual policy option.

Against the backdrop of persistent supply-side shocks and geopolitical instability, high inflation may no longer be a 'transitory' pain but rather a new economic normal to be reckoned with over the coming years. For investors, April’s PCE report is not merely another data point—it is a watershed moment that could determine whether the Fed definitively ends the debate over rate cuts and instead embarks on a more challenging battle against inflation.

Stay ahead on major financial events and discover investment opportunities early! Open Futubull > Market > US Stocks >Financial Calendar/selected macroeconomic data, seize the investment opportunity!

Stay ahead on major financial events and discover investment opportunities early! Open Futubull > Market > US Stocks >Financial Calendar/selected macroeconomic data, seize the investment opportunity!

Editor/Jayden