$Li Auto (LI.US)$On Thursday, the company released a mixed first-quarter 2026 earnings report: revenue slightly exceeded expectations but declined 11% year-over-year, profitability swung from profit to loss, and second-quarter guidance fell short of market expectations.

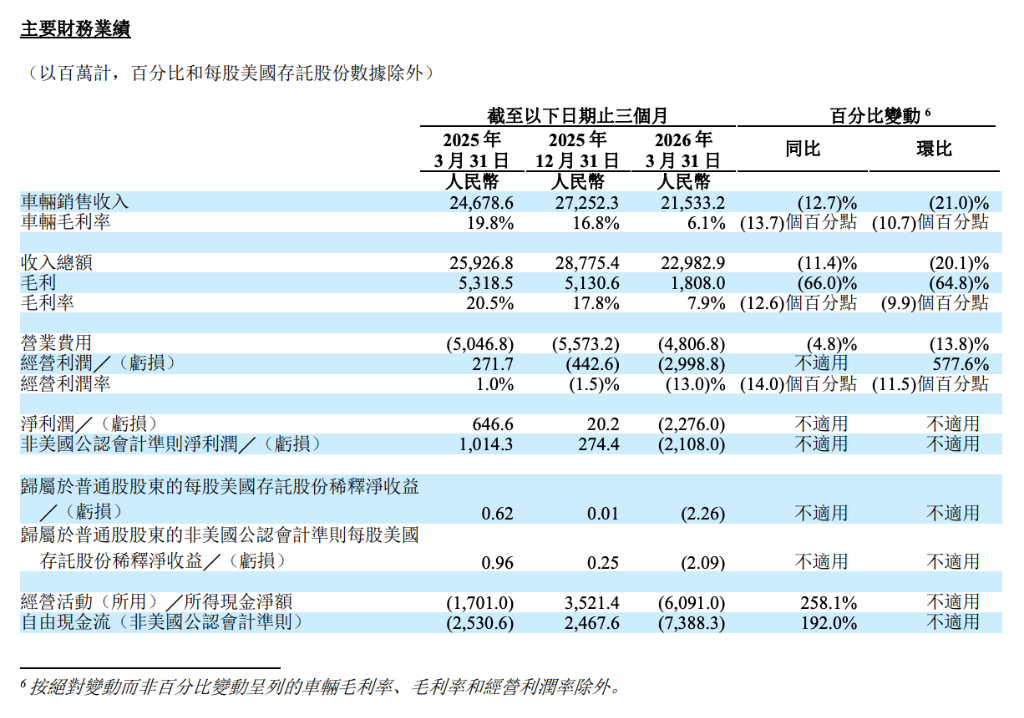

Specifically, total revenue for the first quarter amounted to RMB 22.98 billion, down 11% year-over-year but above the market expectation of RMB 22.09 billion. The company reported a net loss of RMB 2.3 billion, compared to a net profit of RMB 647 million in the same period last year and a net profit of RMB 200 million in the fourth quarter of last year.

In terms of profitability, the gross margin for the first quarter was 7.9%, lower than 20.5% in the same period last year but above the market expectation of 6.94%. Vehicle sales revenue totaled RMB 21.53 billion, down 13% year-over-year. Operating loss stood at RMB 3.0 billion, resulting in an operating margin of negative 13.0%, compared to a positive 1.0% in the same period last year.

For the second quarter outlook, the company expects revenue to range between RMB 24.1 billion and RMB 25.4 billion, below Bloomberg’s consensus estimate of RMB 29.28 billion. It also forecasts deliveries of 95,000 to 100,000 units, below the market expectation of 107,527 units.

For the second quarter outlook, the company expects revenue to range between RMB 24.1 billion and RMB 25.4 billion, below Bloomberg’s consensus estimate of RMB 29.28 billion. It also forecasts deliveries of 95,000 to 100,000 units, below the market expectation of 107,527 units.

Company management attributed these changes to adjustments in product mix—the delivery initiatives related to the Li Auto i6, fluctuations in raw material prices, and the overlapping impact of model transition cycles. On the product front, the all-new Li Auto L9 began deliveries in mid-May. The company’s self-developed chips, the Mach M100 and the Mach VLA large model, have been integrated into vehicles. As of the end of the first quarter, the company held RMB 94.3 billion in cash reserves and is executing a USD 1 billion share repurchase program. As of the time of writing,$Li Auto (LI.US)$the stock was down nearly 4% in pre-market trading, at USD 15.19 per share.

Declining Revenue: What Is the Cost of 'Price-for-Volume' During Model Transitions?

In the first quarter of 2026,$Li Auto (LI.US)$vehicle sales revenue amounted to RMB 21.5 billion, down 12.7% year-over-year and 21.0% quarter-over-quarter. The company stated that the year-over-year decline was primarily driven by a lower average selling price due to changes in product mix, while the quarter-over-quarter decline was further impacted by seasonal delivery reductions during the Chinese New Year holiday.

Other sales and service revenue reached RMB 1.4 billion, up 16.1% year-over-year, aligning with the cumulative growth in vehicle sales. After-sales services and parts-related ancillary revenue remained robust, representing one of the few bright spots in the quarter.

On the cost side, total cost of sales for the quarter amounted to RMB 21.2 billion, up modestly by 2.7% year-over-year, while revenue declined by double digits. The 'revenue contraction versus cost rigidity' scissors effect directly compressed gross profit margins.

Gross margin plummeted to 7.9%, resulting in a net loss of RMB 2.3 billion.

Profitability emerged as the primary focus of this quarter’s earnings report.$Li Auto (LI.US)$Gross margin for the first quarter stood at just 7.9%, a sharp decline of 12.6 percentage points from 20.5% in the same period last year and also below the 17.8% recorded in Q4 of last year. Specifically, vehicle gross margin dropped sharply from 19.8% a year ago to 6.1%.

Impacted by the compression in gross margin, the company reported an operating loss of RMB 3.0 billion for the first quarter, compared to an operating profit of RMB 270 million in the same period last year. Net loss reached RMB 2.28 billion, versus a net profit of RMB 650 million a year earlier. On a non-GAAP basis, net loss was RMB 2.11 billion, compared to a profit of RMB 1.01 billion in the prior-year period.

Li Tie, Chief Financial Officer of the company, explained in the earnings release that the first-quarter gross margin reflected 'the user-centric delivery initiatives related to the Li Auto i6, fluctuations in raw material prices, and the impact of model transition timing.'

Products and Strategy: The All-New L9 Launches Flagship Counteroffensive

$Li Auto (LI.US)$The company is intensifying its product efforts. The all-new Li Auto L9 officially launched in mid-May, offered in Ultra and Livis trims priced at RMB 459,800 and RMB 509,800, respectively, targeting the premium flagship SUV segment.

Key technological highlights of the new vehicle include the integrated deployment of the self-developed Mach M100 chip and the Mach VLA large model. The Livis variant is equipped with two Mach M100 chips and four LiDAR units, while the Ultra version features steer-by-wire technology and a third-generation dual-chamber, dual-valve Magic Carpet air suspension system. Li Xiang, CEO of the company, described it as a 'technological breakthrough leading the industry.'

Additionally, the company plans to launch the all-new Li Auto L8 by the end of June, further expanding its product portfolio. As of the end of Q1, the nationwide charging network comprised 4,057 Li Auto Super Charging Stations with 22,439 charging piles installed.

According to its second-quarter guidance, the company expects deliveries of 95,000 to 100,000 vehicles, representing a year-over-year decline of approximately 10% to 15%; revenue is projected at RMB 24.1 billion to RMB 25.4 billion, down roughly 16% to 20% year-over-year. Near-term pressures remain unresolved, and the performance of the new L9 and L8 models in the second half of the year will be critical variables in upgrading the product portfolio and restoring profitability.

Editor/melody