XPeng Motors reported revenue of RMB 13.03 billion and delivered 62,682 vehicles in the first quarter of 2026, both figures declining year-over-year, while its net loss widened to RMB 1.78 billion. Despite pressures from the traditional seasonal downturn and a product transition cycle, gross margin improved year-over-year to 20.6%, service revenue grew by 41.2%, and R&D expenses reached RMB 2.91 billion. The company’s second-quarter delivery guidance of 100,000 to 106,000 vehicles significantly exceeds market expectations.

Impacted by the traditional seasonal downturn and the product transition cycle,$XPeng (XPEV.US)$first-quarter revenue and deliveries both declined year-over-year, and the net loss widened; however, the second-quarter outlook is significantly better than market expectations.

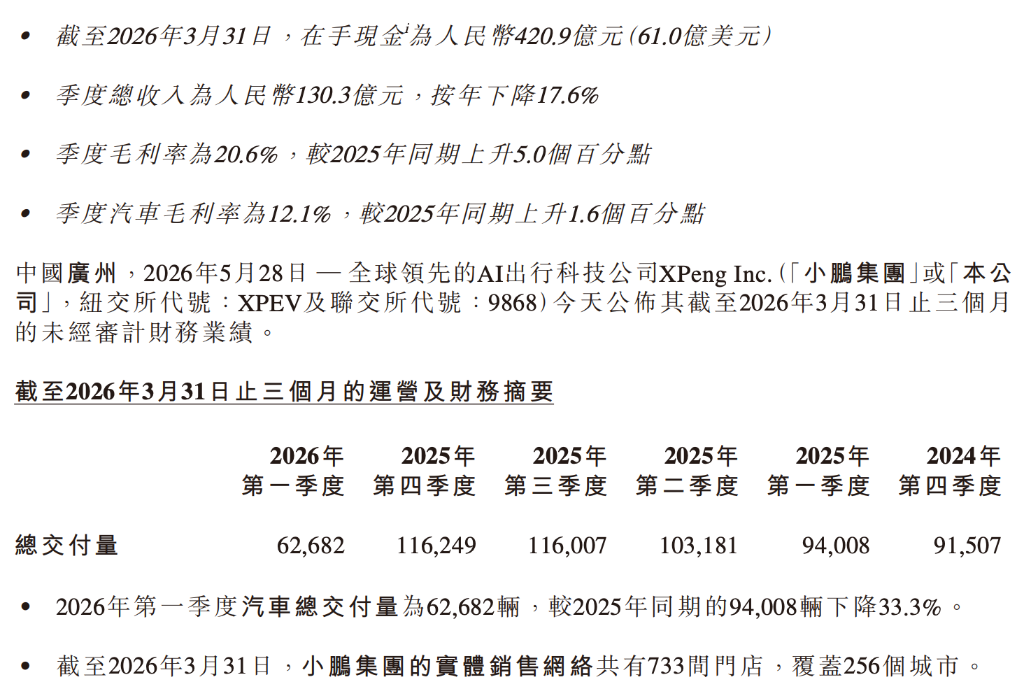

On May 28, XPeng Motors released its financial results for the first quarter of 2026. The data showed that total vehicle deliveries during the period amounted to 62,682 units, a year-over-year decrease of 33.3%. Total revenue was RMB 13.03 billion, down 17.6% year-over-year, slightly below the market estimate of RMB 13.16 billion. Operating loss stood at RMB 1.87 billion, and net loss widened to RMB 1.78 billion, significantly higher than RMB 660 million in the same period last year.

Despite the declines in both deliveries and revenue, key profitability metrics continued to improve. The company reported a gross margin of 20.6% for the first quarter, above the market expectation of 20% and an increase of 5 percentage points compared to the same period in 2025. Vehicle gross margin reached 12.1%, up 1.6 percentage points year-over-year.

Despite the declines in both deliveries and revenue, key profitability metrics continued to improve. The company reported a gross margin of 20.6% for the first quarter, above the market expectation of 20% and an increase of 5 percentage points compared to the same period in 2025. Vehicle gross margin reached 12.1%, up 1.6 percentage points year-over-year.

The improvement in gross margin was primarily driven by sustained cost control measures, optimization of the vehicle model mix, and structural enhancements from in-house technology development and international revenue. This validates management’s earlier assertion that the company could maintain a robust gross margin even during the industry’s off-season. Meanwhile, R&D expenses reached RMB 2.91 billion, exceeding the market estimate of RMB 2.53 billion, reflecting the company’s ongoing commitment to product and technological innovation.

Looking ahead to the second quarter,$XPeng (XPEV.US)$deliveries are expected to range between 100,000 and 106,000 units, representing a sequential increase of approximately 60% to 69% and exceeding Bloomberg consensus expectations of 96,923 units. Total revenue is projected at RMB 19.6 billion to RMB 20.8 billion, reflecting year-over-year growth of roughly 7% to 14%. The XPeng GX, a new tech flagship SUV launched on May 20, along with three additional new models slated for release this year, will form a robust product offensive. CEO He Xiaopeng stated, “We are about to enter a period of strong sales growth.”

As of the end of the first quarter, the company held cash and cash equivalents of RMB 42.09 billion (approximately USD 6.1 billion), down from RMB 47.66 billion at the end of 2025 but still at a relatively high level, providing ample strategic flexibility to support new product launches and R&D investments.

As of the time of writing,$XPeng (XPEV.US)$XPeng’s shares rose more than 3% in U.S. pre-market trading, reaching USD 17.04.

Deliveries: Dual pressures from seasonal slowdown and product transition—signs of recovery emerged in April

In the first quarter of 2026,$XPeng (XPEV.US)$Total deliveries amounted to only 62,682 units, down 33.3% year-over-year and nearly halved compared to the 116,249 units delivered in Q4 2025. This performance was not unexpected by the market—the first quarter is traditionally a slow season for auto sales, and the company is currently in a product cycle transition window, where the handover between old and new models has delayed the release of pent-up orders.

On a monthly basis, deliveries rebounded to 31,011 units in April. Cumulative deliveries for the year reached 93,693 units as of the end of April, indicating a gradual recovery in demand driven by new model launches. The tech flagship SUV, the XPeng GX, officially launched on May 20, with three additional new models scheduled for delivery later this year, completing the company’s product portfolio. If XPeng meets its second-quarter delivery guidance, it would represent a doubling of quarterly deliveries—a critical milestone toward achieving its full-year sales target.

Revenue Mix: Vehicle Sales Under Pressure, Services Emerge as a Standout Growth Driver

$XPeng (XPEV.US)$Automotive sales revenue amounted to RMB 11.0 billion in the first quarter, down 23.5% year-over-year. This decline was less severe than the drop in vehicle deliveries, indicating that average selling prices per vehicle remained relatively resilient. In contrast, services and other revenue performed strongly, reaching RMB 2.03 billion—a substantial 41.2% year-over-year increase—raising its share of total revenue from 9.1% in Q1 2025 to approximately 15.6%.

The growth in services revenue primarily stemmed from two sources: first, increased revenue from technology development services, reflecting XPeng Motors’ ongoing commercialization of AI and intelligent driving technologies for external partners; and second, higher sales of parts and accessories, closely tied to the expanding vehicle installed base.

It should be noted that services revenue in the prior quarter (Q4 2025) reached RMB 3.18 billion, largely driven by the one-time recognition of revenue associated with the achievement of a significant milestone. Revenue this quarter has since normalized. With a gross margin of 66.5%—more than five times that of the automotive hardware business—the rising contribution of services revenue has significantly boosted overall gross margin.

Gross Margin: Structural Improvement Evident, Though Cost Pressures Warrant Attention

$XPeng (XPEV.US)$The overall gross margin reached 20.6%, marking one of the standout highlights of the quarter’s financial results. This represents a 5-percentage-point improvement year-over-year and approaches the high of 21.3% recorded in Q4 2025, underscoring the continued strengthening of the company’s profitability.

Breaking this down, automotive gross margin stood at 12.1%, an improvement of 1.6 percentage points year-over-year, driven primarily by three factors: sustained supply chain cost optimization, component cost reductions enabled by in-house developed electronic/electrical architectures and powertrain systems, and product mix enhancement due to a higher proportion of premium-trim models.

However, compared to Q4 2025, automotive gross margin declined by 0.9 percentage points sequentially, mainly due to rising costs of memory chips and battery-related components, which pushed up per-vehicle costs on a quarter-over-quarter basis. This trend warrants close monitoring—if chip and battery cost pressures persist into Q2, the negative impact on gross margin could intensify.

Expenses: R&D Investment Surges, While SG&A Costs Show Initial Signs of Optimization

Research and development (R&D) expenses were the fastest-growing cost category this quarter, totaling RMB 2.91 billion in Q1—an increase of 46.8% year-over-year. This growth was primarily attributable to two areas: development costs for new vehicle models (including the GX and other models planned for launch this year), and continued high-intensity investment in AI-related technologies such as intelligent driving, Robotaxi, and humanoid robotics.

Management has clearly identified 'mass production of Robotaxi and humanoid robots' as a key strategic objective for 2026. The expansion of R&D investment is strategically necessary, but it also significantly contributed to the widened loss in the first quarter.

In contrast, selling, general, and administrative (SG&A) expenses demonstrated effective cost control. SG&A expenses amounted to RMB 1.88 billion in the first quarter, down 3.2% year-over-year, primarily due to reduced commissions paid to franchisees. From a cost-efficiency perspective, the year-over-year decline in SG&A expenses—despite a sharp drop in deliveries—suggests some improvement in channel operational efficiency.

AI-powered earnings insights in three steps to establish an options strategy! Open Futubull > Stock Page > Click [Company] >Earnings Update

Editor/melody