Best Buy reported financial results: both first-quarter performance and second-quarter comparable sales guidance exceeded expectations.

A major U.S. consumer electronics retailer$Best Buy (BBY.US)$released its first-quarter fiscal 2026 earnings before the market opened on Thursday, significantly surpassing Wall Street expectations. Strong demand for core product categories—including laptops, smartphones, and gaming—as well as robust growth in high-margin advertising and third-party marketplace businesses, underscored the resilience of consumer electronics demand amid macroeconomic uncertainty. As of this report, the company’s stock price rose nearly 14% intraday to $73.36.

Q1 Performance Overview: Revenue and Profit Both Beat Expectations

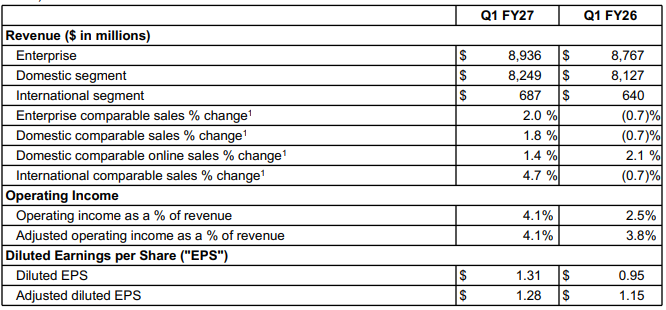

For the fiscal first quarter ended May 3,$Best Buy (BBY.US)$the company reported revenue of $8.94 billion, up 1.9% from $8.77 billion a year earlier, significantly exceeding the consensus market expectation of $8.82 billion. In terms of profitability, net income for the period reached $276 million, or $1.31 per share, a substantial increase from $202 million, or $0.95 per share, in the same period last year. Adjusted earnings per share came in at $1.28, also above the market forecast of $1.22.

Notably, Best Buy achieved a 2.0% year-over-year increase in comparable-store sales this quarter, far exceeding analysts’ expectations of approximately 1% growth. This marks the company’s return to growth after several consecutive quarters of weak sales, compared with a 0.7% decline in comparable sales during the same period last year. Strong performance in gaming, computing, mobile phones, and services drove the increase in comparable sales, largely offsetting the continued softness in home appliances, which had been dragging down overall results.

Notably, Best Buy achieved a 2.0% year-over-year increase in comparable-store sales this quarter, far exceeding analysts’ expectations of approximately 1% growth. This marks the company’s return to growth after several consecutive quarters of weak sales, compared with a 0.7% decline in comparable sales during the same period last year. Strong performance in gaming, computing, mobile phones, and services drove the increase in comparable sales, largely offsetting the continued softness in home appliances, which had been dragging down overall results.

$Best Buy (BBY.US)$In the earnings statement, CEO Corie Barry said, “Our comparable sales increased by 2% year-over-year, outperforming our prior outlook. Most of our major product categories posted positive growth, and our Best Buy Ads and Marketplace businesses also delivered strong results.”

By segment, domestic U.S. revenue rose 1.5% year-over-year to $8.25 billion, with domestic gross margin improving to 23.7% from 23.5% a year earlier. This improvement was primarily driven by robust growth in the Marketplace and advertising businesses, as well as a 1.8% increase in comparable-store sales. Internationally, revenue grew 7.3% to $687 million, reflecting continued recovery in overseas demand, with comparable-store sales rising 4.7%.

Outlook: Growth May Moderate, Full-Year Guidance Unchanged

Looking ahead, Best Buy’s management expressed cautious optimism about the second fiscal quarter. CFO Matt Bilunas noted that comparable sales remained strong in May, with a high-single-digit increase recorded month-to-date. However, he cautioned that growth in comparable-store sales for the second quarter is expected to moderate to approximately 1.0% due to the tough year-over-year comparison from the highly successful Nintendo Switch 2 launch in June of last year. This forecast still exceeds the market’s expectation of a 0.4% decline. Adjusted operating margin is expected to be around 3.9%, flat compared to the prior-year period.

For the full fiscal year, the company maintained its unchanged guidance for fiscal 2027: comparable sales are expected to range between a 1% decline and a 1% increase; adjusted earnings per share are projected to remain in the range of $6.30 to $6.60; and revenue is estimated to be between $41.2 billion and $42.1 billion.

Cost Pressures Under the Shadow of Tariffs

Notably, tariff-related impacts at the macroeconomic level are emerging as a shared challenge for$Best Buy (BBY.US)$and other major U.S. retailers. Walmart, Target, and Best Buy have all recently indicated that cost increases stemming from Trump-era tariffs are already being reflected in the prices of groceries, home goods, and electronics.

It is worth noting that the U.S. government has officially launched a tariff refund program. According to a Citi research report, Walmart is expected to receive approximately $10.2 billion in tariff refunds, while Target is projected to receive around $2.2 billion. As a significant importer in the consumer electronics sector, Best Buy is also poised to benefit. Analysts note that although these one-time refunds may not immediately be reflected in earnings guidance, they could provide a positive boost to companies’ balance sheets over the coming quarters.

Management Transition

Concurrently with this earnings release,$Best Buy (BBY.US)$the company’s leadership succession plan has drawn significant market attention. Corie Barry confirmed she will formally step down as CEO at the end of October this year, succeeded by Jason Bonfig, a senior executive within the company.

In her statement, Barry said, “Given the company’s current momentum, I believe now is the right time to transition leadership.” She will officially depart at the end of the third fiscal quarter and continue serving as a strategic advisor to the company for six months thereafter.

As Barry’s successor, Bonfig will bear the responsibility of accelerating the company’s shift toward higher-margin businesses. The long-tenured Best Buy executive has clearly articulated in his strategic vision a focus on enhancing the company’s retail, media, and technology platforms—expanding marketplace reach to improve business accessibility while comprehensively elevating the customer experience. Bonfig is widely regarded as the key driver behind Best Buy’s transformation into a “platform-based retailer,” and his appointment is broadly interpreted as a strategic signal of the company’s pivot from traditional retail toward deeper integration of ad tech and digital ecosystems.

High-Margin Businesses: Transitioning from Selling Products to Selling Advertising

Of particular significance is Best Buy’s ongoing and profound business model transformation. Advertising and marketplace platform services are gradually emerging as the company’s “second growth curve,” driving enhanced profitability.

Amid increasingly narrow profit margins in traditional retail, Best Buy is placing greater emphasis on high-margin businesses such as Geek Squad technical support services, paid membership programs, retail media advertising (Best Buy Ads), and its third-party seller marketplace platform (Marketplace).

According to prior company disclosures,$Best Buy (BBY.US)$the company’s marketplace platform officially launched in August 2025, onboarding over 500 vetted third-party sellers and expanding into more than 20 new product categories. Its brand portfolio now includes diverse product lines such as Martha Stewart cookware, Crock-Pot small appliances, Fanatics sports merchandise, and Yamaha guitars.

A deeper strategic consideration lies in its advertising business. Attracting more sellers through the third-party marketplace means Best Buy Ads gains greater ad inventory and brand partnership opportunities. The company has disclosed that its website receives over 200 million annual visits and processes more than one million transactions per week, offering substantial monetization potential for its retail media network. Bonfig previously stated explicitly that a key priority during his tenure would be to 'expand Best Buy’s reach and enhance customer experience,' with advertising serving as a central lever to achieve this objective.

“We are expanding into new profit streams, such as Best Buy Ads and the marketplace platform. We expect these businesses to deliver significant benefits over time,” Barry remarked during the earnings call.

It should be noted that expanding high-margin businesses is particularly critical for Best Buy, as the company faces operational cost pressures—global shortages of memory chips linked to the AI wave are driving up component prices, compelling the company to increase imports of computers and other electronics to hedge against rising costs. From a gross margin perspective, businesses such as advertising, marketplace commissions, membership fees, and Geek Squad services typically require minimal inventory investment and offer significantly higher margins than hardware sales like laptops and smartphones.

Regarding the ongoing optimization of its store network, Best Buy recently signaled an important shift—the company plans to net-add six U.S. stores in fiscal year 2027, marking its first net increase in domestic store count in over a decade.

This strategic shift carries significant implications. In contrast to the previous wave of large-scale store closures,$Best Buy (BBY.US)$the company plans to expand using a small-format store model, which has already yielded positive results in pilot markets—not only drawing foot traffic but also boosting local online orders. According to the company's annual report, this small-format model 'drove incremental revenue in smaller markets—through both in-store visits and local online orders.' This strategy reflects an industry-wide trend toward 'flexible, appropriately scaled stores' that serve dual functions as shopping destinations and fulfillment hubs. Entering fiscal year 2027, Best Buy further clarified that this would be the final 'year of significant investment' for both its marketplace platform and Best Buy Ads retail media network, after which both businesses will gradually transition toward sustainable growth and profitability, marking the company’s shift from a high-investment phase to one of profit realization.

Industry Competitive Landscape: Advertising Emerges as the New Battleground for Retail Giants

$Best Buy (BBY.US)$Best Buy’s strategic transformation is not an isolated case. Indeed, against the backdrop of major competitors such as Walmart and Target increasingly viewing advertising and third-party marketplace platforms as new engines for profit growth, Best Buy’s accelerated push into advertising aligns with the broader structural evolution underway across the industry.

Walmart’s advertising and membership revenues together contributed approximately 27% of its operating profit in the most recent fiscal year—a dramatic increase from 9% in 2021—as its online sales grew by 24% to $150.4 billion. Similarly, Target’s retail media network, Roundel, serves as a key pillar of its advertising business. Retail giants are transitioning from pure product retailers to operators of retail media networks, and Best Buy is clearly accelerating its pace in this arena.

Amid AI-driven upgrade cycles for computing devices, the continued expansion potential of its advertising business, and incremental revenue from its marketplace platform, Best Buy’s business model is undergoing profound transformation. However, uncertainties around tariff costs, risks of rising memory chip prices, and fluctuations in consumer confidence remain key concerns for investors. For this consumer electronics retail giant—with over 1,000 stores and a market capitalization exceeding $10 billion—the critical question over the coming quarters will be whether it can successfully navigate this pivotal leadership transition and deliver on its promises of growth in high-margin businesses.

Editor/melody