Market optimism fueled by U.S.-Iran negotiations and Trump’s conditions for reopening the Strait of Hormuz drove Brent crude oil prices down more than 16% in May. Royal Bank of Canada warned that markets are engaging in 'fragmented-memory' trading, overlooking persistent stalemates and military conflicts.

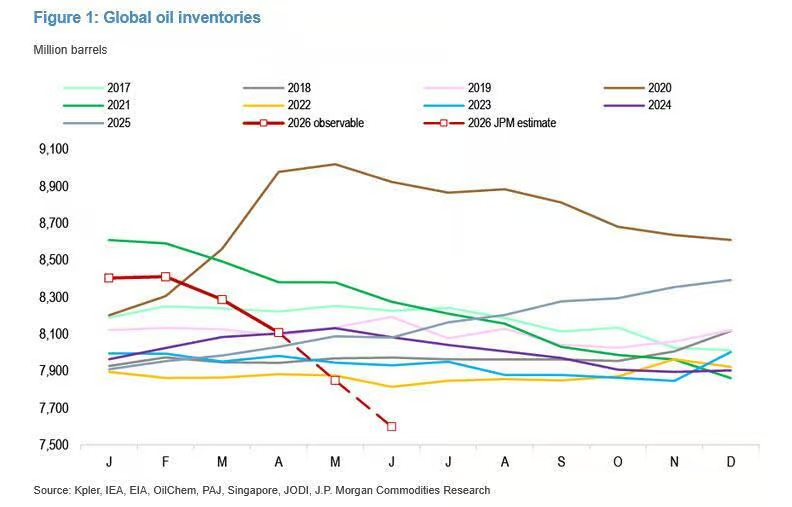

RBC noted that global inventories are being drawn down at a record pace and are projected to fall to historically dangerous lows by October, subjecting the crude oil market to a severe supply-demand stress test between June and August.

Brent crude posted its steepest monthly decline in six years in May, as markets bet that U.S.-Iran negotiations would lead to the reopening of the Strait of Hormuz, driving oil prices steadily lower. However, Helima Croft, Head of Commodities Research at Royal Bank of Canada (RBC), warned in a recent report that current price movements have significantly diverged from supply realities, with global inventories being drawn down at a record pace. If no substantive breakthrough is achieved, the crude market will face a severe stress test between June and August this year.

According to Xinhua News Agency, Trump posted on social media on Friday, local time the 29th, stating he would soon convene a meeting in the White House Situation Room to make a final decision regarding military action against Iran. The announcement once again dampened market sentiment.$Crude Oil Futures (JUL6) (CLmain.US)$WTI crude fell 1.73% on the day, closing at $87.36 per barrel; Brent crude declined 1.77%, settling at $92.05. For the entire month of May, Brent crude plunged more than 19%, marking its worst monthly performance since March 2020 when the global economy was hit by the COVID-19 pandemic; WTI dropped nearly 17% in May, its weakest monthly performance since April 2025.

According to Xinhua News Agency, Trump posted on social media on Friday, local time the 29th, stating he would soon convene a meeting in the White House Situation Room to make a final decision regarding military action against Iran. The announcement once again dampened market sentiment.$Crude Oil Futures (JUL6) (CLmain.US)$WTI crude fell 1.73% on the day, closing at $87.36 per barrel; Brent crude declined 1.77%, settling at $92.05. For the entire month of May, Brent crude plunged more than 19%, marking its worst monthly performance since March 2020 when the global economy was hit by the COVID-19 pandemic; WTI dropped nearly 17% in May, its weakest monthly performance since April 2025.

However, Trump simultaneously laid out a series of conditions that Tehran has historically rejected: Iran must pledge never to acquire nuclear weapons, immediately and unconditionally reopen the Strait of Hormuz to two-way traffic without imposing tolls, clear all remaining mines from the strait, and allow U.S. personnel to excavate and destroy enriched uranium buried under rubble following airstrikes. According to CNBC, citing U.S. officials, negotiators have agreed on a framework for a 60-day memorandum of understanding (MOU) covering an extended ceasefire and arrangements for talks on Iran’s nuclear program, though it still requires Trump’s final signature.

In her report, Croft wrote that she does not rule out the eventual formation of some form of MOU, but noted that 'with regard to a substantive agreement, current headlines and their impact on oil prices have clearly run well ahead of reality.' She reminded investors that reports suggesting 'a deal is imminent' have surfaced multiple times before—more than three weeks have passed since the first such reports emerged, during which Iran has lost the equivalent of nearly 300 million barrels of production capacity. In her view, the market has repeatedly been persuaded by headlines implying the crisis is ending, abandoning pricing for worst-case scenarios, while selectively forgetting the ongoing diplomatic deadlock and escalating military confrontations—this selective amnesia is precisely why the true crisis has remained masked until now.

Markets are engaging in 'Memento'-style trading, where narratives of a deal override reality

In her report, Croft described the current market trading logic as exhibiting a 'Memento'-like mindset—whenever news emerges suggesting 'a deal is imminent,' the market treats it as a decisive breakthrough, yet selectively forgets the persistent diplomatic impasse, fundamental disagreements over the nuclear issue, and recurring escalations in military friction.

This pattern repeated itself again this week. Just hours after the latest round of oil price declines, driven by reporting from Axios, new reports emerged that Iran had fired missiles at several vessels that had transited the strait without coordinating with the IRGC. On Thursday, U.S. forces intercepted four Iranian drones in the Strait of Hormuz and struck Iranian military positions near Bandar Abbas; the IRGC responded by launching a ballistic missile at a U.S. base in Kuwait, which was successfully intercepted by Kuwaiti forces. On Monday, U.S. forces also struck two vessels laying mines in the strait and an air defense site near Bandar Abbas.

Croft believes February 27, 2026, may ultimately prove to be the peak volume of tanker traffic through the Strait of Hormuz in the foreseeable future. Any ceasefire outcome that leaves de facto control of the strait in Iranian hands would result in transit volumes significantly below historical norms.

Inventory drawdown accelerates; October levels could hit historic danger zone

While deal-driven narratives dominate price action, RBC data reveals a rapidly deteriorating underlying fundamental reality.

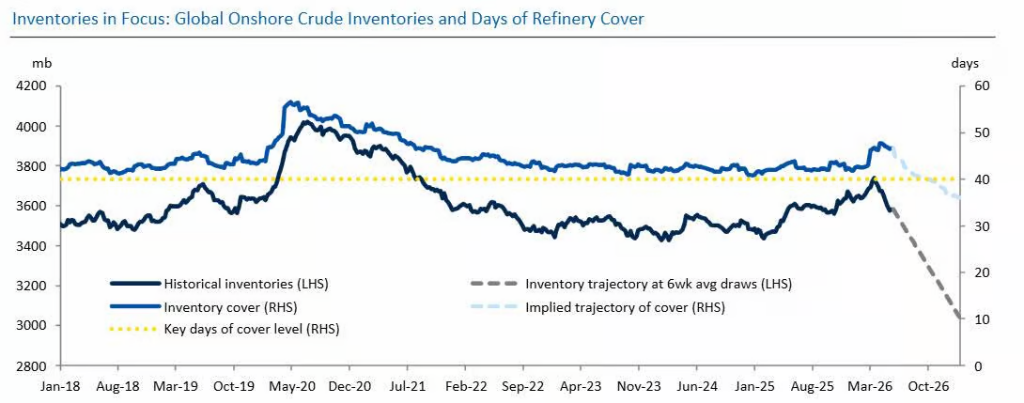

The crisis has entered its third month, and the ongoing drawdown of global inventories due to Middle Eastern supply disruptions is becoming increasingly evident. Croft estimates that if inventories continue to be depleted at the current six-week average rate, days of cover—measured as onshore crude oil inventories relative to refinery throughput—could fall into the 30- to 40-day range by October. This would represent the lowest level since RBC began compiling its dataset in 2016. Breaching this threshold could jeopardize normal industry operations due to logistical bottlenecks and insufficient feedstock availability.

Notably, the initial shock of the crisis was relatively manageable owing to ample starting inventory levels and coordinated releases of Strategic Petroleum Reserves (SPR) by various countries, which partially cushioned the immediate impact of what is now the largest supply disruption in history. However, Croft notes that these 'energy shock absorbers' are being rapidly depleted. RBC also forecasts that the pace of inventory drawdown will accelerate further in the coming weeks, potentially bringing forward the crisis inflection point earlier than expected. Moreover, limited visibility into market data from other countries suggests that the current reported inventory declines may be systematically underestimated, implying that the actual situation could be tighter than indicated by available data.

Based on this assessment, Croft concludes: absent any material breakthrough, RBC is confident that the period from June to August will constitute a severe stress test for the crude oil market—'a market that, until now, has been avoiding pricing in worst-case scenarios through self-persuasion.' She writes:

"Time is running out, and the window for reopening the Strait of Hormuz and averting a hard landing is rapidly narrowing."

Implementation Challenges: Logistics, Insurance, and Sanctions as Triple Barriers

Even if the U.S. and Iran ultimately sign a memorandum extending the ceasefire, RBC believes the Strait of Hormuz will struggle to achieve a meaningful and swift recovery.

Operationally, even if more vessels are permitted to transit, initial traffic will likely be unidirectional, adding logistical complexity to clearing the waterway. Given the persistent threats posed by missiles, drones, and naval mines, Croft finds it difficult to foresee how many Western shipping companies would be willing to risk returning to this route based solely on a 60-day memorandum of understanding (MOU). Exorbitant insurance premiums, coupled with legal obstacles under U.S. sanctions related to payments or coordination with entities affiliated with the Islamic Revolutionary Guard Corps (IRGC), further constrain shipowners’ practical options. Industry experts have already noted that an Iran-led reopening plan would most likely entail only limited transits, and full restoration of the strait may require the clear defeat of Iranian military forces and the establishment of unrestricted passage as prerequisites.

Meanwhile, the accelerated development of alternative overland transport routes through the United Arab Emirates and Saudi Arabia’s continued high-utilization operation of the East-West Pipeline have become pragmatic adaptations by Gulf states to this new reality.

Croft also raises a strategically significant question: Are there factions within Iran inclined to sustain the current status quo of 'neither war nor peace, with minimal oil flows'? Such actors might calculate that as summer approaches and the economic costs of inventory depletion become harder to mask through public messaging, Iran’s bargaining leverage will naturally strengthen. Although the dual blockade has clearly eroded Iranian government finances and hydrocarbon operational efficiency, reports indicate that Iran continues to sell previously sanctioned crude under exemption clauses and collects revenue from transit fees via the Strait of Hormuz.

More notably, despite hyperinflation now significantly worse than in January, the Iranian government has reportedly not faced a new wave of large-scale protests to date. It is also said that the IRGC has used the ceasefire period to rebuild some of its military capabilities—suggesting that Tehran’s hardliners may believe time is on their side.

Editor/melody