SpaceX may be the coolest company in history, but its high valuation makes its IPO highly risky. With a current price-to-sales ratio of approximately 107x and extreme market consensus bullishness—a classic sign of a market top—the parallels are concerning. From Tesla’s pre-crash precedent to Elon Musk’s habitual delays in meeting promises, questionable profitability, slowing Starlink growth, and potentialM&Aliabilities and rocket explosion risks, there has never been an equivalence between a great company and a great stock.

SpaceX may be one of the coolest companies in human history, but that does not necessarily mean it will be a good investment.

As expectations for a SpaceX IPO continue to build, market enthusiasm for valuing this rocket company has approached euphoria.

The current valuation stands at approximately 107 times price-to-sales, far exceeding the historical average for the most expensive IPOs ever—and some forecasters even consider a multi-trillion-dollar market capitalization as the base case scenario.

The current valuation stands at approximately 107 times price-to-sales, far exceeding the historical average for the most expensive IPOs ever—and some forecasters even consider a multi-trillion-dollar market capitalization as the base case scenario.

Such pervasive and unanimous bullish sentiment has historically often preceded market tops on Wall Street.

For investors, the real risk is not whether SpaceX will succeed—few actually question that. The core risk lies in the fact that the IPO pricing has already fully priced in all optimistic expectations, leaving buyers with an extremely limited margin of safety.

From Cisco to Amazon to Tesla, world-changing companies have all experienced brutal drawdowns following the bursting of their valuation bubbles. History has repeatedly shown that great companies do not always equate to great stocks.

Below are 12 reasons to be skeptical about the SpaceX IPO.

Reason 1: The most crowded consensus trade in the market

Even before SpaceX has officially filed its prospectus, its bullish narrative has already been widely accepted by the market—a warning signal in itself.

Venture capitalists are bullish on it, growth fund managers are bullish on it, and retail investors dream of owning shares in it.

Even Musk's critics have publicly acknowledged that they expect the stock price to be higher.

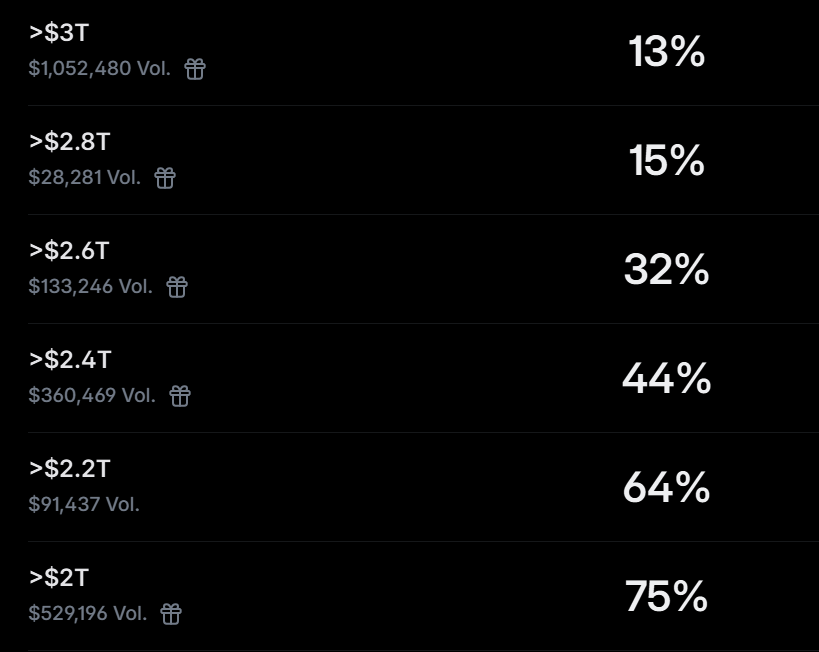

On Polymarket, discussions regarding SpaceX's market capitalization on its first day of trading have treated outcomes in the trillions of dollars as a baseline rather than an optimistic forecast.

(Polymarket’s analysis of SpaceX’s closing market capitalization on its first trading day)

The debate is no longer whether SpaceX will succeed, but whether it will become the most valuable company on Earth. History shows us that market tops quietly form precisely in such narrative-driven environments.

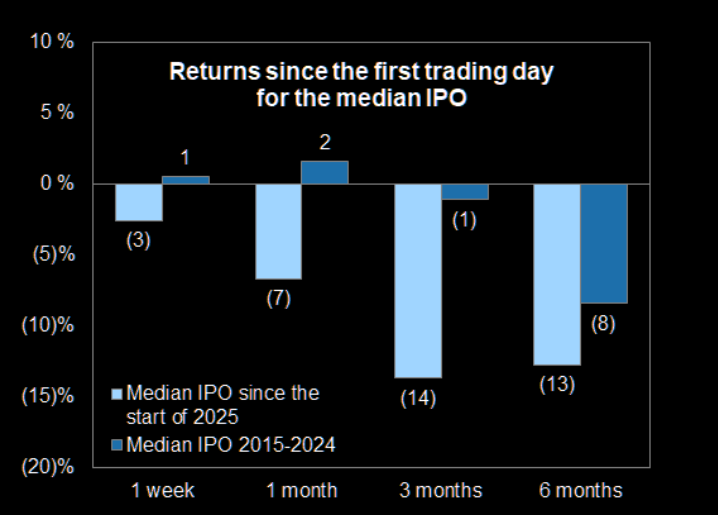

Reason Two: The IPO Surge Trap

According to Goldman Sachs data, recent IPO history is replete with cases of frenzied enthusiasm on listing day followed by prolonged underperformance.

Investors systematically pay a premium when narrative-driven sentiment reaches its saturation point, ultimately overpaying for the excitement.

This pattern is no coincidence. When a stock becomes the world’s most anticipated investment even before its listing, the first-day premium often exhausts months or even years of future return potential.

Reason Three: Lessons from Tesla

The best case study for understanding Musk’s investment logic is Tesla’s history.

Tesla’s share price declined by approximately 75% cumulatively between 2021 and 2023, following several drawdowns exceeding 50%.

Elon Musk’s management style ensures that the share price trajectories of his companies have never followed a smooth, upward path.

SpaceX investors should not assume that future drawdowns will be milder than those experienced by Tesla; they could even be more severe. Musk’s halo effect offers no protection to share prices—a fact already demonstrated by history.

Reason Four: The Musk Risk Premium

In fact, investing in Musk’s companies has indeed generated substantial returns in the past. However, buying into Musk’s ventures entails both rewards and risks.

Musk habitually challenges regulators, posts controversial messages at 3 a.m., stirs debate, and acts according to his own will. Shareholders are merely passengers riding along for the journey.

Tesla’s recent brand backlash in California serves as a reminder to the market that when a founder becomes highly politicized, brand loyalty can erode faster than anticipated.

Reason Five: Unresolved Profitability Concerns

Musk excels at generating substantial paper wealth for shareholders, yet the track record of his companies in delivering genuine profitability remains unimpressive.

SpaceX investors are buying into the future, but the core question is: what happens when public markets start demanding 'the present'?

This narrative is not unfamiliar. Tesla was also long priced based on 'future potential' rather than actual profitability.

This logic works well in periods of abundant liquidity, but quickly breaks down when markets shift focus to profitability, cash flow, and margins. The market’s patience for growth stories has always been cyclical.

Reason Six: A History of Promises and Delays

Elon Musk’s greatest strength lies in his ability to articulate grand, pulse-quickening visions—but this is also one of his greatest weaknesses.

Fully autonomous driving, robotaxis, humanoid robots, Mars timelines, production targets, launch schedules—many of these commitments have arrived late, some remain unfulfilled to this day, and others have proven far more complex than originally described.

Investors often focus on the ultimate destination, but the market sometimes cares more about delays along the way.

SpaceX may be different, but investors should at least acknowledge this historical pattern.

Reason Seven: The Tesla Merger Black Hole

The market widely expects that Elon Musk will eventually merge Tesla into SpaceX without causing losses to Tesla shareholders.

This means that SpaceX may in the future have to absorb a valuation 'black hole' on the order of approximately $400 billion.

This potential burden has been almost entirely overlooked in current discussions about SpaceX’s valuation.

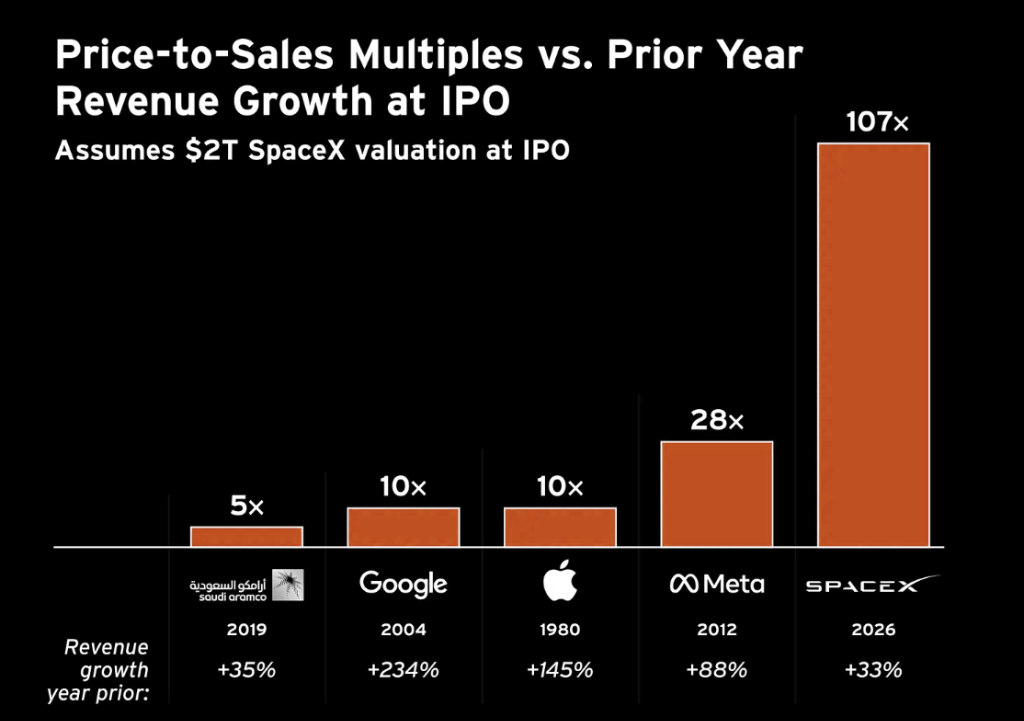

Reason #8: Valuation So High It’s Out of This World

SpaceX is expected to price its offering at a price-to-sales (P/S) ratio of 107x, which would make it one of the most richly valued public stocks in history.

By comparison, Palantir—the most expensive stock in the S&P 500 today—trades at a P/S ratio of 64x.

Compared with other landmark IPOs in history, SpaceX’s valuation appears even more excessive:

Meta went public with a P/S ratio of 28x, at a time when its revenue growth rate was as high as 88%;

Google’s P/S ratio at its IPO was just 10x, with a revenue growth rate soaring at 234%.

In other words, SpaceX’s revenue growth is several times slower than that of these two companies at the time of their IPOs, yet it is demanding a valuation multiple several to ten times higher.

Reason #9: The Ghost of 1999 FOMO Returns

This IPO round has raised a substantial amount of capital, and the funding sources are not exclusively sophisticated tech investors.

A significant portion comes from institutional capital whose primary motivation is not to assess intrinsic value, but to avoid being asked at their next board meeting, 'Why did you miss it?'

A similar dynamic was also at play during the internet bubble between 1999 and 2000. The outcome of that episode is well known.

Reason Ten: Timing the Contrarian Bet Against Musk

Peter Thiel’s famous adage—'Never bet against Musk failing'—has become something of a golden rule on Wall Street.

But people often forget that Thiel made his real fortune by betting on Musk when almost no one else believed in him.

Founders Fund entered the scene in 2008, when SpaceX had suffered consecutive rocket launch failures and was on the brink of bankruptcy—that was the decision that truly required courage.

Entering after SpaceX became the most anticipated IPO in history requires something entirely different.

The best time to invest in SpaceX may have been in 2008; the worst time might very well be the day of its IPO.

Reason Eleven: Doubts Surrounding Starlink’s Growth

Renowned short-seller Jim Chanos once asked: "Was Starlink’s March ARR (Annual Recurring Revenue) really lower than its December level?"

According to data in SpaceX’s prospectus, the company is profitable on a reported basis after adjusting for loss-related items.

However, signs that Starlink’s revenue has plateaued or even declined month-over-month represent a warning signal that cannot be ignored.

For a company primarily viewed as a growth story, the risk of slowing growth could be magnified in the public markets.

Reason Twelve: Rockets Explode

Finally, and most plainly: rockets explode, launches fail, schedules slip, and budgets overrun. The history of aerospace has never followed a smooth, upward exponential curve.

According to The Information, given SpaceX’s ambitious goals, it is almost certain that the company’s spacecraft will suffer another major failure at some point after going public.

SpaceX may ultimately reach Mars, reshape global communications, or become the most important company of this century.

Yet none of these outcomes guarantees that the stock will represent a sound investment at its IPO price. After all, gravity wins 100% of the time—even in space.