Goldman Sachs believes that three structural shifts—sustained AI-driven demand, supply constraints, and long-term supply agreements (LTAs)—are driving the memory industry’s transformation toward AI infrastructure. The firm expects the supply-demand imbalance to persist through 2028. Previously, both Morgan Stanley and JPMorgan noted that memory giants are at a historic inflection point in their valuation paradigm, with earnings predictability comparable to Taiwan Semiconductor, and that their current forward price-to-earnings ratio of 7.3x offers significant potential for historic valuation repair.

The global memory chip industry is undergoing a historic paradigm shift: it is evolving from a traditional cyclical commodity characterized by 'boom-and-bust' volatility into a strategic AI infrastructure resource with high predictability. The most fundamental impact lies in the complete overhaul of valuation frameworks—transitioning decisively from price-to-book (P/B) to price-to-earnings (P/E).

On June 1, according to ZuiFeng Trading Desk, Goldman Sachs stated in its latest in-depth research report on the global semiconductor memory industry that the current upcycle differs fundamentally from past cycles. Sustained AI-driven demand, constrained supply growth, and structural shifts stemming from long-term agreements (LTAs) are collectively transforming the memory sector from a highly cyclical commodity segment into a predictable, AI infrastructure-oriented business.

The report identifies four disruptive shifts occurring in industry fundamentals and valuation logic:

The report identifies four disruptive shifts occurring in industry fundamentals and valuation logic:

First, the supply-demand gap has been significantly revised upward, with tightness in the DRAM, NAND, and HBM markets expected to intensify in 2027 beyond 2026 levels, and shortages projected to persist through 2028;

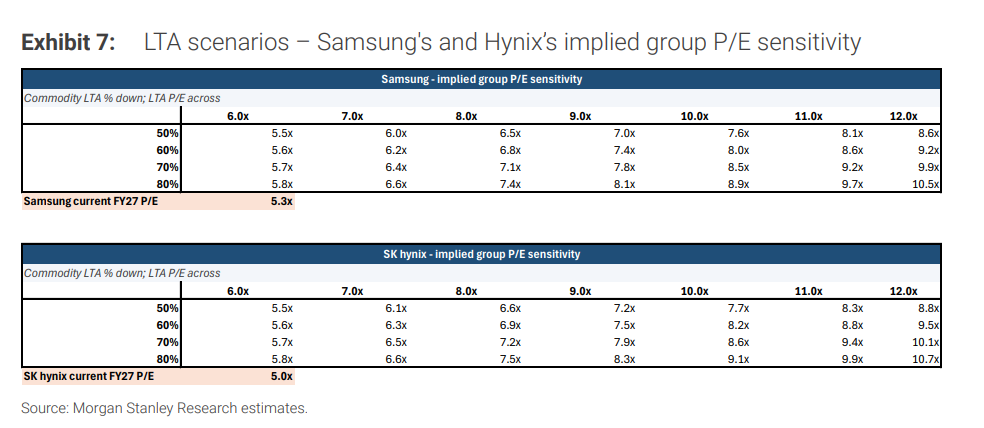

Second, a historic shift has occurred in the valuation framework, with the industry benchmark officially transitioning from price-to-book (P/B) to price-to-earnings (P/E), driving substantial upward revisions to target prices across the 'Big Three' ( $SK Hynix (000660.KR)$ implying approximately 53% upside potential, $Samsung Electronics (005930.KR)$ implying approximately 60%);

Third, the pricing logic for HBM is being repriced, with average HBM prices in 2027 expected to achieve a 44% 'catch-up' premium over standard DRAM, and its total addressable market (TAM) revised upward by 54% to USD 116 billion in 2027;

Finally, medium- to long-term operating profit forecasts for the Big Three have been comprehensively upgraded, with high profitability expected to persist throughout the forecast horizon.

In a similar vein, prior to Goldman Sachs, major Wall Street investment banks Morgan Stanley and JPMorgan reached the same conclusion in their latest research reports: memory giants such as Samsung and SK hynix stand at a historic inflection point in valuation paradigm shifts.

Morgan Stanley and JPMorgan argue that the widespread adoption of long-term agreements (LTAs) could prompt the market to reprice these companies from 'highly cyclical commodities' to 'technology infrastructure assets with stable cash flow characteristics.' Currently, memory giants trade at a forward P/E of approximately 7.3x, representing a 50%–80% valuation discount relative to Taiwan Semiconductor.

Three Structural Anomalies: Why Will This Cycle Remain Elevated for an Extended Period?

The current cycle has fully diverged from the historical trajectory of 2017–2018, which was driven solely by cloud data centers. Goldman Sachs believes that the fundamental underlying dynamics are being reshaped by three structural forces:

Demand Side: AI Servers Assume Absolute Dominance

The cyclical drag from consumer electronics has been completely marginalized. Data shows that in 2025, servers will account for approximately 50% of total industry DRAM demand and 40% of NAND demand; by 2028, these shares are projected to rise further to 61% and 43%, respectively. The global server memory market is expected to reach approximately $449 billion in 2025, representing a 7.4-fold increase compared to 2017.

As large language models (LLMs) evolve toward enterprise-grade agentic AI, token consumption is forecast to exceed current processing capacity by more than 24 times by 2030. Memory bandwidth and capacity have thus become critical bottlenecks constraining AI development.

Supply Side: HBM Capacity Exerts an Increasingly ‘Cannibalizing’ Effect

Traditional memory expansion is now facing hard physical constraints. HBM production requires 3–4 times the wafer capacity of standard DRAM. As HBM evolves toward HBM4 and HBM4E, the wafer intensity per unit continues to rise.

Between 2026 and 2030, approximately 30% of the combined monthly cleanroom capacity—ranging from 1.39 million to 1.54 million wafers—from the three major manufacturers will be effectively locked in for HBM production. This will cause the compound annual growth rate (CAGR) of traditional DRAM supply to contract sharply from 19% during 2017–2018 to just 15%.

Business Model: Long-Term Agreements (LTAs) Reinforce Earnings Visibility

Memory manufacturers and hyperscale cloud providers are systematically dampening cyclicality through LTAs. Clear financial evidence has already emerged: SanDisk’s Q3 FY26 earnings report disclosed $42 billion in deferred revenue obligations (RPO) and $400 million in advance payments under its new business model agreements, both subject to contractual penalties for breach.

Historical precedent from the silicon wafer industry demonstrates that widespread adoption of LTAs can confer exceptional profit stability upon oligopolistic sectors—a key foundation supporting higher valuation multiples for the memory segment.

Supply-Demand Gap Deep Dive: A More Severe Shortage Looms in 2027

Data show that the supply-demand gaps for the three major product categories will not only remain unresolved by 2027 but will further deteriorate compared to 2026:

DRAM: The supply-demand gaps are projected to plunge to -5.0%, -5.9%, and -3.9% in 2026, 2027, and 2028, respectively. Driven by robust server DRAM demand, average DRAM prices in 2026 are expected to surge by 326% year-over-year, with operating margins stabilizing near a historic peak of approximately 80%.

NAND: The supply-demand gaps are forecast at -4.4%, -4.6%, and -3.0% for 2026, 2027, and 2028, respectively. Enterprise SSD (eSSD) demand is set to skyrocket by 66% and 31% in 2026 and 2027, respectively, supporting NAND operating margins in the high 60% range.

HBM: The shortage is most acute, with gaps reaching -5.4%, -6.0%, and -4.3% in 2026, 2027, and 2028, respectively. Fueled by surging ASIC-side demand (projected to grow 172% in 2026), Goldman Sachs forecasts the HBM market size to reach $56 billion, $116 billion, and $168 billion in 2026, 2027, and 2028, respectively.

Shifting from PB to PE: Upside Revisions to Target Prices for the 'Big Three'

Given a fundamental shift in earnings visibility, Goldman Sachs has formally anchored its valuation of memory stocks to P/E multiples (using 9x as the baseline):

$SK Hynix (000660.KR)$ / $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$ (Buy): Target price surges to the KRW 3.3–3.5 million range. Stress tests indicate that even under an extreme adverse scenario of consecutive 30% annual price declines over two years, its profit margin would remain at a healthy 40%, thoroughly disproving the outdated notion that 'peak cycle equals losses.'

$Samsung Electronics (005930.KR)$ / $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$ (Buy): Target price raised to KRW 480,000. Operating profit for 2026 is projected to increase more than eightfold year-over-year, with ROE reaching a record high of 52%. Its HBM revenue is expected to soar to approximately USD 44 billion by 2027.

Notably, however, rising memory prices are beginning to hurt downstream segments: Samsung’s smartphone division’s operating margin is expected to collapse from 11% to a historic low of 2%.

$Kioxia Holdings (285A.JP)$ (Upgraded to Buy): Under the expectation of a prolonged NAND upcycle, the 12-month target price is set at JPY 93,000, based on a forward P/E of 7.8x FY3/28E earnings.

Wall Street Consensus Converges: How Morgan Stanley and JPMorgan View the Shift in Valuation Frameworks

This paradigm shift in valuation—from P/B to P/E—is not an isolated view of a single institution; Morgan Stanley and JPMorgan’s latest analyses strongly reinforce this perspective.

As previously reported by Wall Street Journal, Morgan Stanley explicitly stated that memory has become the absolute bottleneck in AI infrastructure. Long-term agreements (LTAs) are transforming what was traditionally a highly cyclical business into one with rigid supply guarantees and high-margin, long-duration cash flows.

If the market continues to value memory stocks as typical cyclical commodities, significant mispricing will result. Quantitative analysis shows that under a base-case scenario—assuming 100% LTA coverage for HBM and 70% coverage for conventional memory, valued at a 10x P/E—the implied blended P/E multiples for Samsung and SK Hynix should be 8.5–8.6x. If LTA coverage rises to 80%, the implied P/E would exceed 10.5x.

JPMorgan’s reasoning cuts directly to the core of commercial negotiation: buyers’ fear of supply disruption and sellers’ concern over demand shortfalls have jointly driven the adoption of legally binding long-term contracts.

The firm has likewise issued aggressive bullish calls: raising its target price for Samsung to KRW 480,000 (implying an 8x P/E) and for SK Hynix to KRW 3,000,000, while doubling Kioxia’s target price to JPY 80,000.

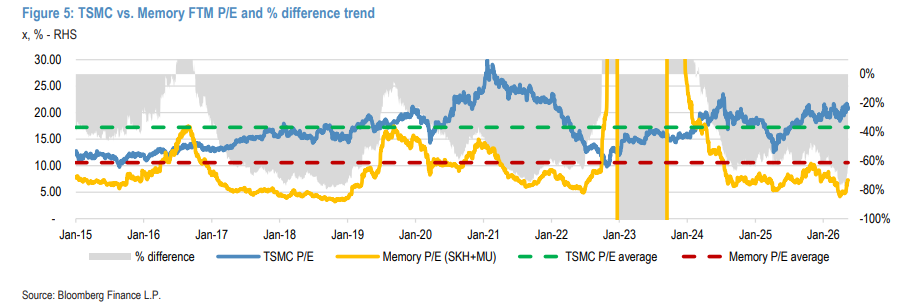

Notably, three top-tier Wall Street institutions have all pointed to Taiwan Semiconductor as the benchmark: after securing a long-term agreement with Apple in 2014, Taiwan Semiconductor successfully transitioned its valuation framework to P/E and has since consistently traded within a 10–30x P/E range.

Currently trading at a forward P/E of only around 7.3x, memory leaders face a historic opportunity to close the 50–80% valuation discount relative to Taiwan Semiconductor.

However, Wall Street maintains a final note of caution: contractual terms alone cannot fully insulate companies from cyclicality. At the tail end of the 2017 cycle, forward agreements became effectively worthless within just a few months following a collapse in demand.

This time, the only concrete evidence capable of underpinning the new valuation framework is the presence of actual cash prepayments on the balance sheet and legally binding deferred revenue obligations. Without genuine cash inflows as a safeguard, all grand narratives about navigating through cycles will remain nothing more than a mirage.

Looking to pick stocks or diagnose stock performance? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Looking to pick stocks or diagnose stock performance? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Editor/KOKO