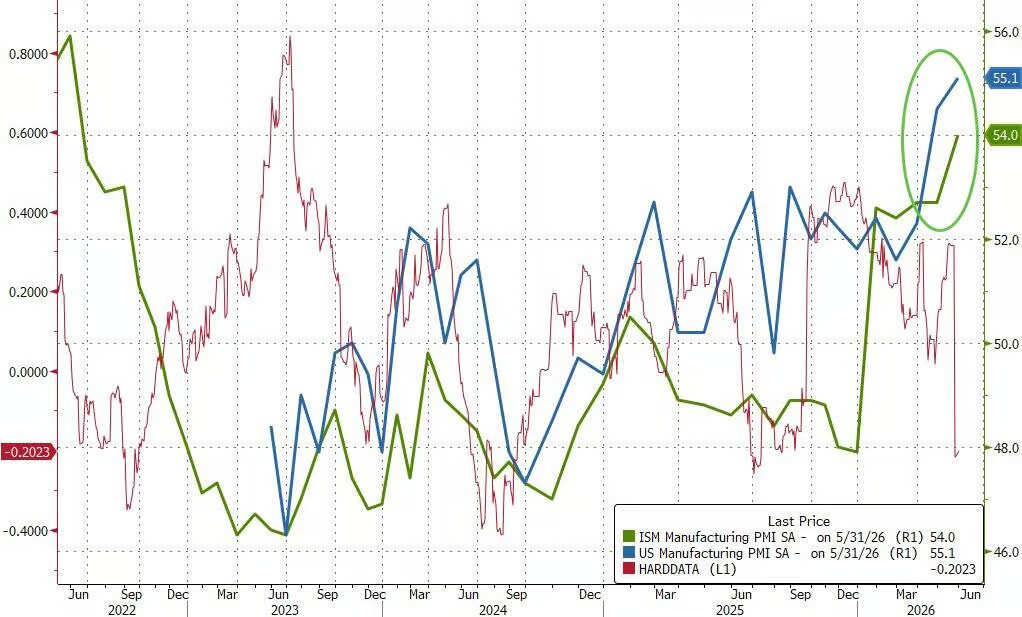

The U.S. ISM Manufacturing Index rose to 54 in May (expected: 53; previous: 52.7), reaching a four-year high and marking the fifth consecutive month of expansion, driven by surging orders fueled by AI infrastructure investment and inventory restocking. However, the conflict in Iran pushed up oil prices and raw material costs; the ISM Manufacturing Prices Paid Index stood at 82.1, slightly down but still near its highest level since 2022.

U.S. manufacturing has regained momentum amid a surge in artificial intelligence (AI) investment and stabilizing trade policies, with activity in May expanding at the fastest pace in four years. However, soaring supply chain costs triggered by the conflict in Iran are emerging as a significant risk.

Data released Monday by the Institute for Supply Management (ISM) showed that the U.S. Manufacturing PMI rose by 1.3 percentage points to 54 in May, remaining in expansion territory (above 50) for the fifth consecutive month.

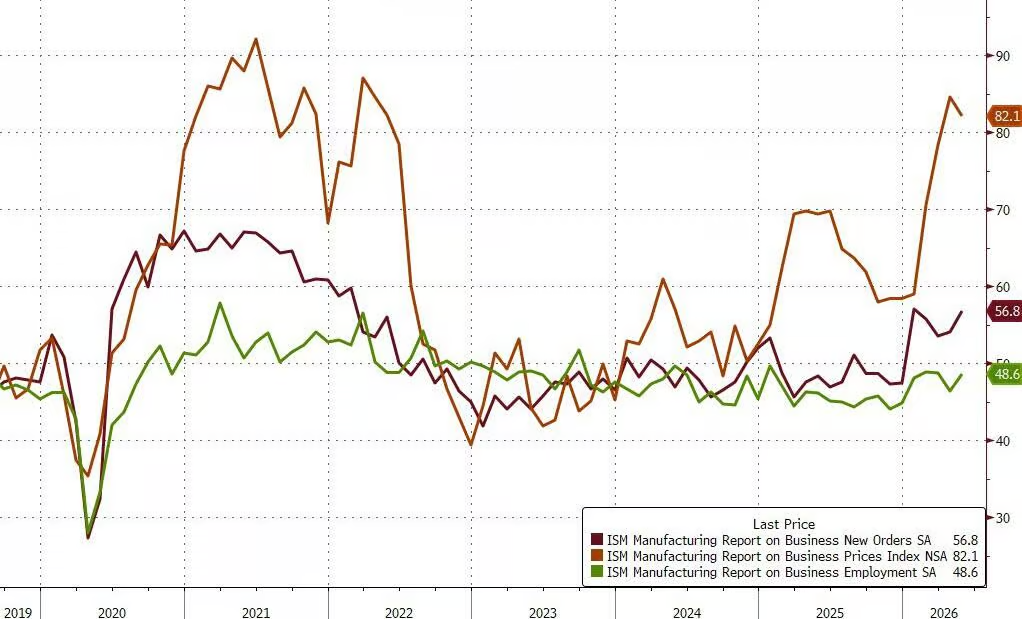

New orders accelerated to a four-month high, and production rebounded in tandem, with nearly all manufacturing subsectors reporting growth. The ISM Manufacturing New Orders Index stood at 56.8 in May, exceeding the forecast of 54.8 and up from April’s reading of 54.1.

New orders accelerated to a four-month high, and production rebounded in tandem, with nearly all manufacturing subsectors reporting growth. The ISM Manufacturing New Orders Index stood at 56.8 in May, exceeding the forecast of 54.8 and up from April’s reading of 54.1.

Beneath the strong headline figures, however, inflationary pressures are intensifying, as the conflict in Iran drives up oil prices and raw material costs. The ISM Manufacturing Prices Paid Index came in at 82.1 in May, below the expected 85 but slightly down from April’s 84.6. Although the ISM price component edged lower, it remains near its highest level since 2022.

The ISM Manufacturing Employment Index rose to 48.6 in May, above the forecast of 48.4 and up from April’s 46.4. While employment conditions improved somewhat in May, the index still indicates a continued decline in employment. The government’s monthly jobs report is scheduled for release on Friday.

Last week’s data showed that the Federal Reserve’s preferred inflation gauge rose 3.8% year-over-year in April—nearly double the central bank’s target and the fastest pace since 2023—suggesting that persistent cost pressures could further transmit to consumer prices.

Stockpiling and AI demand boost orders

Nearly all manufacturing industries reported growth this month, including printing, textiles, electrical equipment, and plastics, with only wood products contracting.

Behind the recovery in manufacturing demand lies a degree of short-term stockpiling behavior. Some customers placed advance orders to hedge against anticipated future price increases, artificially inflating current order volumes to some extent. Meanwhile, ongoing investment in AI infrastructure has driven higher demand for related electronic components.

A manufacturer of computers and electronic products commented in the ISM survey: "Prices for multiple product categories continue to rise—partly due to strong demand for electronic components driven by data center construction, and partly because the war in Iran has reduced the supply of oil and petroleum-based products."

The chemical products industry reported that sales in April continued to grow by 15%, but raw material costs have broadly increased, and fuel surcharges in import-export logistics have risen significantly. "We remain cautiously optimistic about the outlook, provided that global economic conditions stabilize and the conflict in Iran is resolved."

Import and export indices expanded in tandem in May, with the inventory sub-index rising to a one-year high.

The conflict in Iran and oil prices constitute core cost risks.

Although oil prices have retreated from their peak, they remain substantially above pre-war levels, eroding manufacturers’ profit margins across the board and prolonging supply chain cycles. The ISM Supplier Deliveries Index remains at its highest level since 2022, reflecting the persistent disruption to logistics efficiency caused by war-related disturbances.

Industries across the board reported significant cost pressures in the survey.

The transportation equipment sector stated: "The conflict in Iran has begun to exert a direct and negative impact on supply chain costs, with oil prices and related commodity prices continuing to rise."

The food, beverage, and tobacco products industry noted that diesel costs are severely impacting profitability, while uncertainty surrounding tariff refund policies has created confusion.

The machinery industry warned that the Middle East conflict is causing shipment delays and uncertainty, adding, "Persistently high gasoline prices and inflation will inevitably affect our procurement decisions."

Editor/Liam