The eurozone economy is entering a typical phase of 'stagflationary pressures,' characterized by continued contraction in economic activity, weakening demand, cooling labor markets, and renewed upward pressure on input costs and output prices.

Zhitong Finance APP learned that S&P Global's latest report on the Eurozone Composite PMI for May 2026 indicates that the Eurozone economy is entering a typical 'stagflationary pressure' zone—characterized by continued contraction in economic activity, weakening demand, cooling labor markets, yet rising input costs and output prices. The PMI data shows that the Eurozone’s private sector activity index contracted at its weakest pace in 18 months in May, primarily due to weaker demand for goods and services—a key gauge of economic health—which has weighed down the Composite PMI output for two consecutive months, while cost pressures have risen to their highest level in over three years.

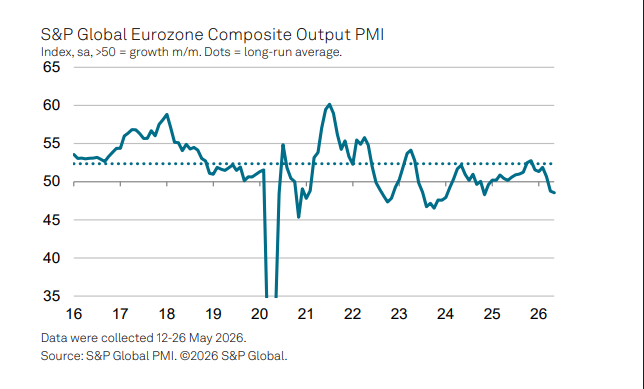

The Eurozone Composite PMI Output Index declined to 48.5 in May from 48.8 in April, marking its lowest reading in 18 months and remaining below the critical 50-point threshold for the second straight month, signaling an accelerated pace of contraction in private sector activity. Chris Williamson, Chief Business Economist at S&P Global, noted that unless there is a marked improvement in June, the PMI points to a risk of a quarter-on-quarter GDP contraction of approximately -0.2% in Q2.

Stagflation alarm bells ring in the Eurozone! Middle East geopolitical tensions may drag down Q2 GDP.

Stagflation alarm bells ring in the Eurozone! Middle East geopolitical tensions may drag down Q2 GDP.

S&P Global’s Eurozone Composite PMI Output Index fell to 48.5 in May from 48.8 in April, the lowest reading since November 2024, though slightly above the preliminary estimate of 47.5. The overall Services PMI edged up modestly to 47.7 from 47.6, outperforming the preliminary estimate of 46.4. Readings below the 50.0 mark indicate a contraction in economic activity.

Chief Business Economist Chris Williamson stated: 'With Eurozone business activity declining for the second consecutive month in May, the likelihood of an economic contraction in the second quarter appears increasingly pronounced. Unless there is any significant shift in June, the PMI data suggests a quarterly GDP decline of 0.2%.'

Total new orders have declined for three consecutive months, with the drop in May being the second-largest since November 2024. Weaker overseas demand was a greater drag, as export orders slid at the fastest pace so far this year.

The deterioration was concentrated in the Eurozone’s two largest economies. Private sector activity contracted in both Germany and France, while Italy and Spain recorded modest expansions.

Input costs rose at the fastest pace in three and a half years, while prices charged to customers climbed to a 38-month high—marking the third consecutive month of accelerating output price inflation. Earlier this week, data released on Tuesday showed that Eurozone inflation unexpectedly jumped to 3.2% in May, significantly above the European Central Bank’s 2% target. With geopolitical conflict in the Middle East sharply driving up global energy prices—including oil and natural gas—and the Strait of Hormuz remaining blockaded, further upward pressure on Eurozone inflation is expected.

According to data from the International Energy Agency (IEA), Iran’s closure of the Strait of Hormuz may have already removed approximately 1 billion barrels of oil supply from the market—the largest supply disruption in history.

Since the Iran conflict began in late February, the Strait of Hormuz has effectively been blockaded, severing one of the world’s most critical shipping routes for crude oil, natural gas, and refined fuel products to global customers. This has significantly driven up energy prices and intensified inflation concerns among global investors.

Citi released a research report stating that if the long-term peace negotiations between the United States and Iran remain difficult, leading to the prolonged blockade and control of the Strait of Hormuz, the international oil price benchmark—Brent crude oil prices—may rise further from their recent noticeable pullback around the $100 mark, potentially even setting new phase highs.

The European Central Bank has noted that both upside risks to inflation and downside risks to growth have intensified, placing policymakers in a difficult position. Some economists suggest that the ECB’s June meeting will be closely watched and could result in a 25-basis-point rate hike, raising the benchmark interest rate to 2.25%. However, other economists argue that the ECB should proceed cautiously with any rate increase, given signs of economic stagnation and weakening consumer confidence.

As the PMI data showed a decline in new business in the Eurozone, firms reported that spare capacity could continue to rise. The pace of job losses accelerated to its fastest rate in five and a half years, although the scale of layoffs remained modest. Meanwhile, backlogs of work were cleared at the fastest pace in 14 months, indicating that firms are not completing more work due to capacity expansion but rather because insufficient new orders are causing unfinished business to dwindle rapidly.

The survey report also showed that business confidence has recovered modestly compared to April, but remains weak by historical standards and is still far below the level seen before the outbreak of the Middle East conflict.

Stalling Growth and Resurgent Inflation: Energy Shocks Fracture the European Economy

Notably, signs of softening have also begun to emerge in the eurozone labor market. Private-sector employment in the eurozone declined further in May, with the pace of job cuts reaching its fastest in five and a half years. Although the overall magnitude remains moderate, the direction is critically significant: service-sector employment resilience has been one of the main pillars underpinning persistent inflation in the eurozone; now, cooling labor demand suggests wage pressures may ease going forward, but it will also further dampen household income expectations and consumption sentiment. Service-sector employment posted its first decline since January 2021—a complex signal for the European Central Bank (ECB): while it helps contain medium-term inflation, it also implies that further rate hikes would amplify downside economic risks.

The pricing data represent the most policy-sensitive aspect of the entire report. Input cost inflation accelerated further in May, reaching its highest level in three and a half years; output price inflation climbed to a 38-month high and marked its third consecutive month of acceleration. According to S&P Global’s data report, input cost pressures remain the strongest since late 2022. Chris Williamson even warned this could indicate inflation approaching 4% in the coming months. This aligns with Eurostat’s latest figures: headline inflation in the eurozone is estimated to have risen to 3.2% in May from 3.0% in April, with energy prices continuing to act as a key driver.

Demand-side indicators are also increasingly weakening. The report shows that new orders for goods and services in the eurozone declined for the third consecutive month, with the pace of contraction moderating slightly from April but still marking the second-steepest drop since November 2024. New export orders presented an even clearer drag, as private-sector export orders fell at their fastest pace so far this year. This indicates that the Middle East conflict, energy price shocks, global trade uncertainty, and weakening external demand are collectively weighing on eurozone firms’ order books through the export channel.

In terms of macroeconomic policy implications, this PMI report has placed the European Central Bank (ECB) in a difficult dilemma characterized by simultaneous economic slowdown and rising inflation. At its April meeting, the ECB held all three key interest rates unchanged and explicitly stated that both upside inflation risks and downside growth risks have intensified. However, if the cost pressures reflected in the PMI continue to transmit to final consumer prices, markets will further price in the likelihood that the ECB must raise rates to prevent inflation expectations from becoming unanchored. The challenge lies in the fact that the PMI simultaneously signals weakness across demand, employment, orders, and business confidence; overly tight monetary policy could effectively amount to 'raising rates during an economic downturn.' Consequently, eurozone assets will undoubtedly remain constrained by 'stagflation discounts,' with bond markets facing heightened inflation risk and rising term premiums, while European equities will likely favor defensive sectors, companies with strong ability to pass through energy costs, and those exhibiting stable cash flows. Cyclical consumer goods, export-oriented manufacturing, and highly leveraged industries will continue to face pressure.

Editor/Deng