Wall Street traders expect a strong jobs report to be released on Friday, but it may not be enough to calm their nerves as market attention has shifted toward inflation.

Zhitong Finance APP noted that Wall Street traders expect a strong jobs report on Friday. However, this may not be enough to calm markets, as oil price shocks triggered by war are increasingly shifting investor focus toward inflation.

Although equity markets have repeatedly hit record highs, largely ignoring elevated crude oil prices for months, beneath the calm surface, concerns are mounting over how long inflationary pressures will persist and what actions the Federal Reserve will take in response.

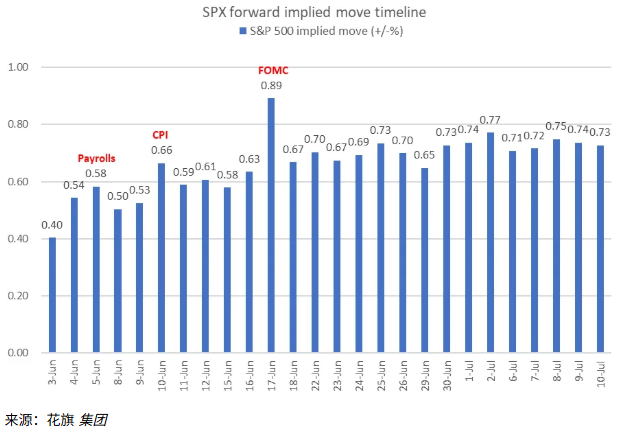

According to data compiled by Citigroup, traders anticipate the Federal Reserve’s interest rate decision on June 17 will be the most significant event facing the S&P 500 over the next month, followed by the Consumer Price Index (CPI) report scheduled for release on June 10. Options markets are pricing in a 0.6% move for the benchmark index on Friday, which would make it one of the calmest nonfarm payroll days in months.

According to data compiled by Citigroup, traders anticipate the Federal Reserve’s interest rate decision on June 17 will be the most significant event facing the S&P 500 over the next month, followed by the Consumer Price Index (CPI) report scheduled for release on June 10. Options markets are pricing in a 0.6% move for the benchmark index on Friday, which would make it one of the calmest nonfarm payroll days in months.

Larry Benedict, CEO of The Opportunistic Trader, a financial markets research firm, stated, “Jobs data has become less important to traders because all eyes have shifted back to inflation indicators and how they might influence interest rates. Strong employment figures present another dilemma for the Fed, as officials attempt to prevent the economy from overheating.”

Traders are closely watching Friday’s employment data for clues on whether the labor market and wage growth continue to strengthen following April’s modest rise in consumer spending. Based on the median forecast from a survey of economists, the market consensus expects nonfarm payrolls to increase by 85,000. The unemployment rate is likely to remain steady at 4.3%, while average hourly earnings are projected to rise by 0.3% month-over-month.

The resilience of the labor market comes against a backdrop of persistently high inflation eroding household incomes and pushing the savings rate to its lowest level in nearly four years—a situation leaving traders grappling with uncertainty as they try to forecast the Fed’s interest rate path.

Bond traders are currently pricing in an interest rate hike this year, reflecting market conviction that newly appointed Fed Chair Kevin Warsh will need to act swiftly to combat inflation.

Forward Guidance on Interest Rate Path

Friday’s employment report will be the final monthly labor market update before Fed officials enter their pre-meeting blackout period. Stuart Kaiser, U.S. equity trading strategy head at Citigroup, noted that the S&P 500’s implied volatility of 0.6% for the day is below the average realized volatility of 0.7% observed on employment report days over the past year.

Federal Reserve Governor Christopher Waller described the labor market as stabilizing. Although investors require evidence that this trend continues, the CPI report now appears to outweigh jobs data in importance when traders assess the trajectory of borrowing costs.

Last week, Federal Reserve Governor Lisa Cook signaled that accelerating inflation is currently a greater policy concern than the labor market. On Tuesday, Cleveland Fed President Beth Hammack, who holds a voting seat on monetary policy this year, said that a more restrictive interest rate level may be needed to combat inflation risks.

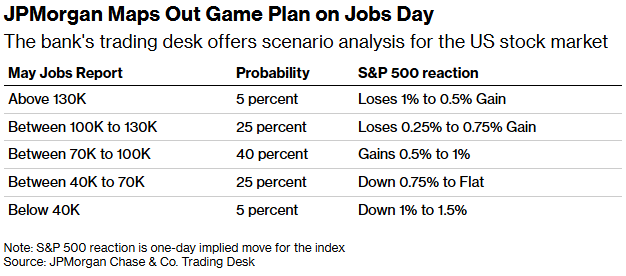

Andrew Tyler, Global Head of Market Intelligence at JPMorgan, stated in a report on Tuesday that if the economy adds fewer than 40,000 jobs in May, the S&P 500 could decline by as much as 1.5%. However, he estimated the probability of such an outcome at only around 5%.

Tyler noted that if last month’s job gains fall between 70,000 and 100,000—the scenario JPMorgan’s trading desk considers most likely—the S&P 500 is expected to rise by 0.5% to 1%.

JPMorgan’s Expectations for Payroll Growth and Market Volatility

With economic growth remaining resilient and volatility staying low, traders perceive little risk in the coming weeks. The Cboe Volatility Index (VIX), often referred to as the 'fear gauge,' is currently well below the key level of 20, which typically signals rising market stress.

However, ample potential catalysts for market turbulence remain. As the first-quarter earnings season draws to a close, investors are searching for new substantive drivers to sustain the bull market, following the S&P 500’s surge of over $11 trillion in market capitalization since the end of March.

Investors remain wary of an overheated jobs report, as it could signal excessive economic strength, leading to a pause or delay in interest rate cuts and raising concerns about persistently entrenched inflation.

Daniel Kirsch, Head of Options at brokerage Piper Sandler & Co., said traders are generally comfortable with payroll growth of around 100,000.

He added that if the data were to decline significantly below that level for several consecutive months, the options market might begin shifting its focus back from inflation to hiring trends. “Traders are currently more afraid of the risks posed by higher inflation and interest rates,” Kirsch said. “Therefore, the market can absorb any slightly positive news on employment.”

Editor/Deng