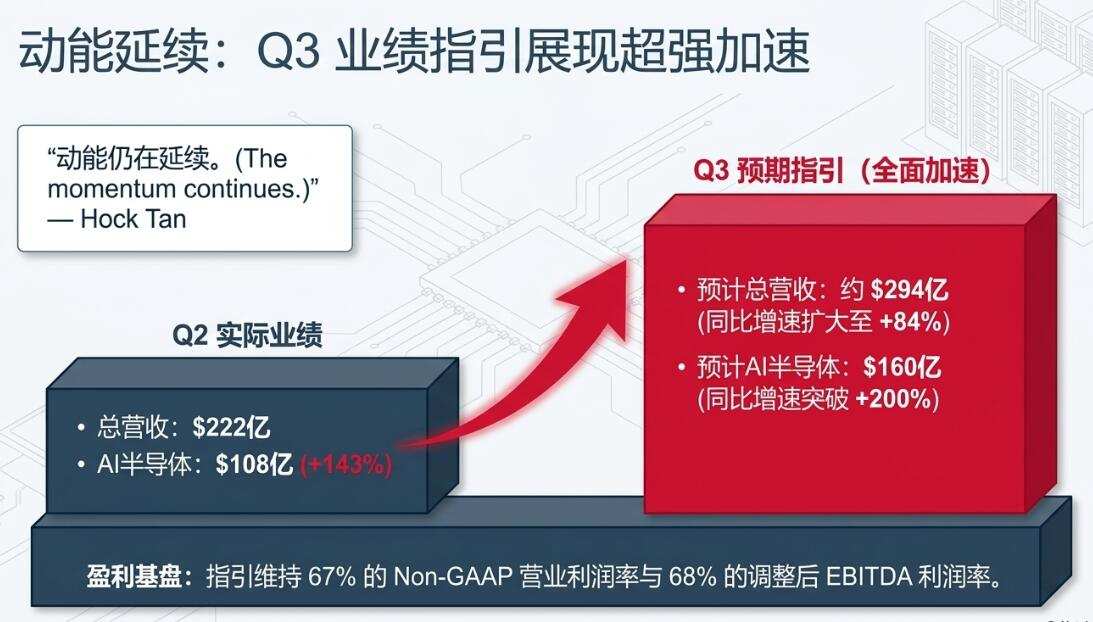

In the second fiscal quarter, Broadcom reported its highest year-over-year revenue growth in nine years, with EPS rising 54% year-over-year and AI semiconductor revenue increasing by over 140%, though both figures slightly exceeded analysts’ expectations. For the third fiscal quarter, Broadcom guided AI semiconductor revenue to grow more than twofold year-over-year to $16 billion, which is still 7% below the consensus expectation. Broadcom’s CEO stated that AI chip sales for the current fiscal year are expected to reach $56 billion, nearly 3% below the consensus forecast. In 2027, Broadcom plans to deploy 1.3 GW of computing capacity for OpenAI and deliver its first 1 GW of capacity to Meta in the second half of the year.

A leading manufacturer of AI-customized chips $Broadcom (AVGO.US)$ once again delivered double-digit revenue growth for the quarter, but its guidance for AI chip revenue—closely watched by the market—fell short of expectations, causing its stock price to decline after several days of sharp gains.

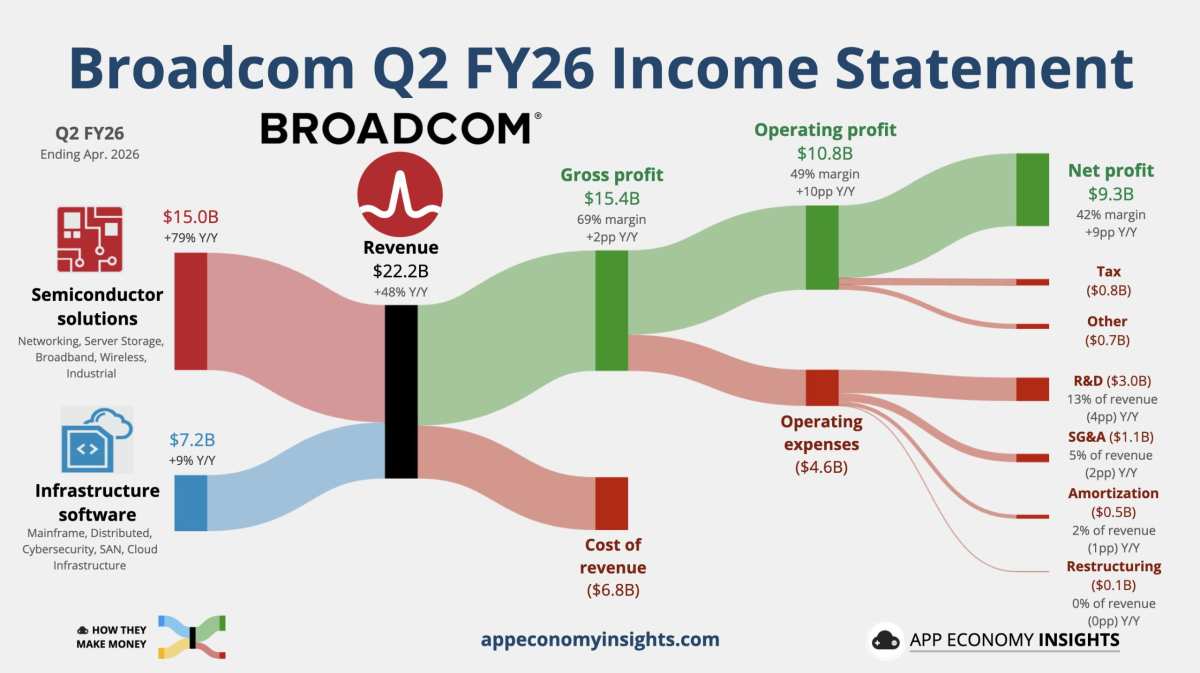

After U.S. markets closed on Wednesday, May 3 (Eastern Time), Broadcom reported that for its second fiscal quarter of 2026 (the “Q2”), which ended May 3, 2026, net revenue surpassed $22 billion for the first time in a single quarter—slightly above analyst expectations—and rose approximately 48% year-over-year, nearly 1.7 times the growth rate of the prior quarter. Revenue from its Semiconductor Solutions segment, which directly benefits from surging AI demand, increased by nearly 80% year-over-year. On a non-GAAP basis, adjusted earnings per share (EPS) rose more than 50% year-over-year, both figures exceeding Wall Street expectations.

Broadcom forecast third-quarter (Q3) revenue of approximately $29.4 billion, about 2.8% above analyst expectations, reflecting continued strong demand for AI infrastructure, custom chips, and software services. However, this guidance was less impressive than before; three months ago, Broadcom’s Q2 revenue outlook had exceeded analyst expectations at the time by 7.2%.

Broadcom forecast third-quarter (Q3) revenue of approximately $29.4 billion, about 2.8% above analyst expectations, reflecting continued strong demand for AI infrastructure, custom chips, and software services. However, this guidance was less impressive than before; three months ago, Broadcom’s Q2 revenue outlook had exceeded analyst expectations at the time by 7.2%.

Of greater concern to the market, Broadcom’s Q3 AI semiconductor revenue guidance stood at $16 billion—more than tripling year-over-year—but still about 7% below the analyst consensus. Given that, prior to the earnings release, Broadcom’s share price had already surged more than 65% from its late-March lows, gained roughly 40% year-to-date, and added over $300 billion in market capitalization within just five trading days through Tuesday, investors had been betting on a blowout earnings report that significantly exceeded expectations across the board.

During the post-earnings conference call, Broadcom CEO Hock Tan stated that the company expects AI chip sales for the full fiscal year to reach $56 billion—a figure nearly 2.8% below the analyst consensus of $57.6 billion.

After the earnings release, Broadcom's share price—which had already declined by nearly 0.5% on Wednesday—quickly extended its losses. Analysts noted that the sharp drop was not due to weak results per se, but rather because market expectations for Broadcom had been extremely high; any guidance falling short of an 'explosively' strong upside surprise could trigger profit-taking.

In other words, Broadcom’s earnings report confirmed that demand for AI remains robust, yet it failed to provide sufficiently compelling new information to justify the valuation following its recent surge. For a stock like Broadcom’s, which has already rallied sharply, merely exceeding consensus estimates may not be enough to convince investors that further significant upside remains—especially when its AI-related revenue guidance came in below the consensus forecast.

Q2 Revenue Growth Hits Nine-Year High, But EPS and Revenue Beat Margins Remain Modest

Broadcom reported adjusted Q2 revenue of $22.19 billion, setting another record high for a single quarter—about $60 million above market expectations, representing a modest beat of approximately 0.3%. Revenue grew roughly 48% year-over-year, a significant acceleration from the prior quarter’s 29% growth rate, marking the strongest quarterly growth since the fiscal quarter ended January 31, 2017.

Broadcom’s adjusted Q2 EPS rose 54% year-over-year to $2.44, outpacing the prior quarter’s 28% growth. Analysts had expected $2.39, resulting in an EPS beat of about 2.1%.

From the data, Broadcom’s earnings quality remains solid, with both revenue and profit slightly exceeding market expectations. However, given the stock’s recent strong rally and the market’s high expectations for its AI business, this degree of outperformance is not particularly 'impressive.'

This is also a key reason behind the post-market share price pressure: the earnings report contained no significant flaws, but it also failed to substantially surpass the market’s already optimistic assumptions.

Notably, prior to the earnings release, the options market had priced in an expected one-day volatility of approximately 7.8% following the report—above the historical average—indicating that investors anticipated significant price swings. Under these conditions, results that merely modestly beat consensus estimates could easily trigger profit-taking.

The continued strength of the semiconductor business was the most critical highlight of the earnings report.

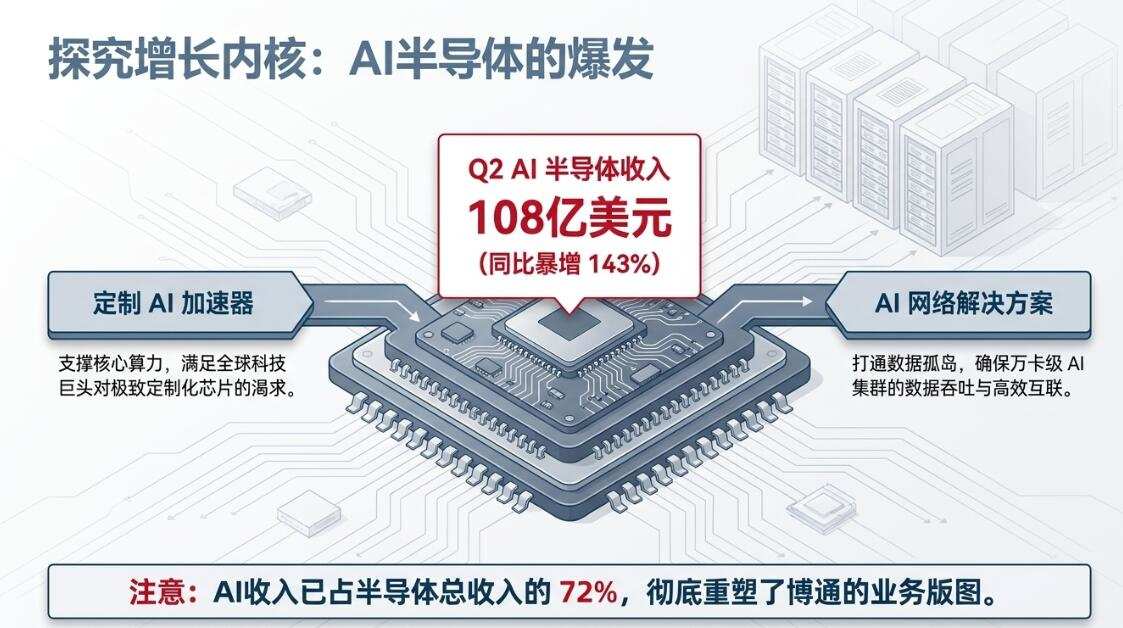

In the second quarter, Broadcom’s semiconductor solutions segment—including ASICs—generated revenue of $15.01 billion, up 79% year-over-year, significantly accelerating from the previous quarter’s 52% growth. This exceeded the market expectation of $14.65 billion by approximately 2.5%. The segment accounted for roughly 68% of total company revenue and remains Broadcom’s most important growth engine.

This segment also represents the core of the market’s focus on AI. Rather than simply replicating NVIDIA’s GPU model, Broadcom is deeply engaged in co-developing custom ASIC/XPU chips with major cloud providers and maintains a dominant position in data center networking chips and Ethernet switch chips.

In the second quarter, Broadcom’s AI-related semiconductor revenue reached $10.8 billion, surging approximately 143% year-over-year and slightly ahead of the market’s estimate of around $10.7 billion. This figure represents nearly half of the company’s total revenue and accounts for roughly 70% of semiconductor solutions segment sales. Even based solely on the disclosed semiconductor revenue, demand for Broadcom’s AI hardware and network infrastructure remains robust, showing no signs of the slowdown that some investors had feared.

However, the higher the proportion of AI-related revenue, the greater the market’s expectations for growth elasticity. Previously, investors were willing to pay a premium for 'rapidly growing AI business'; now, following Broadcom’s significant stock price appreciation, the market increasingly demands evidence that 'AI growth is accelerating further, order visibility is extending, and new customers or stronger guidance are emerging.' This has clearly raised the bar for evaluating the earnings report.

The software business provides a stable foundation, but investor attention remains firmly focused on semiconductors and AI.

According to Broadcom’s earnings report, infrastructure software revenue—including VMware—was approximately $7.18 billion in the second quarter, with year-over-year growth improving from 1% in the prior quarter to 9%. However, its share of total revenue declined from 39% to 32%.

Following its acquisition of VMware, the infrastructure software business has become a significant contributor to Broadcom’s revenue and cash flow. Its importance lies in providing more stable and predictable subscription- and enterprise software-based income, smoothing out semiconductor cycle volatility, and enhancing the company’s overall earnings resilience.

However, the market reaction this time indicates that investors currently price Broadcom primarily based on its AI semiconductor business. Even though the software segment is stable, it is insufficient to offset investor demands for high growth elasticity from AI and strong semiconductor guidance.

In other words, the software business forms the 'foundation' of Broadcom’s valuation, while AI semiconductors act as the 'lever' driving short-term stock price fluctuations.

For the current fiscal quarter, AI semiconductor revenue guidance implies year-over-year growth of more than twofold, yet still falls short of expectations.

In terms of guidance, Broadcom expects third-quarter revenue of approximately $29.4 billion, representing year-over-year growth of about 84%. This guidance exceeds the market consensus estimate of $28.61 billion by roughly $790 million, or approximately 2.8%.

In absolute terms, this represents a strong outlook. The third-quarter revenue guidance implies growth of over 32% compared to the record-high level achieved in the second quarter. If Broadcom delivers on this guidance, it would demonstrate continued momentum in AI infrastructure demand, semiconductor shipment cadence, and software business integration.

The primary concern raised by the guidance centers on AI semiconductors—the core growth driver. Broadcom forecasts third-quarter AI semiconductor revenue of approximately $16 billion, up more than 200% year-over-year, which remains below the analyst consensus estimate of $17.2 billion, with some more optimistic buy-side expectations even higher.

The sharp post-market decline in Broadcom’s share price suggests the market is not questioning whether Broadcom’s AI business is growing, but rather repricing it: whether the pace of growth is sufficient to justify the rapidly elevated share price and valuation seen in recent weeks.

For Broadcom today, the market cares not just about 'beating expectations,' but 'by how much.' Ahead of the earnings release, Broadcom’s stock price had already priced in fairly robust performance assumptions. Many investors were effectively trading not against the sell-side consensus estimate, but against higher 'buy-side expectations' or 'whisper numbers.'

By 2027, Broadcom plans to deploy 1.3 GW of computing capacity for OpenAI and an initial 1 GW for Meta.

During a post-earnings conference call with analysts, Broadcom CEO Hock Tan revealed that arrangements Broadcom has reached with Apollo and Blackstone will help OpenAI meet its demand for AI computing power. Through this collaboration, the company plans to deploy over 20 gigawatts (GW) of computing capacity by 2028.

Broadcom has already begun delivering chips to OpenAI and is progressing as scheduled toward mass production later this year. During the call, Tan noted that Broadcom has signed contracts to deploy 1.3 GW of computing capacity in 2027. This order forms part of an agreement the company reached with OpenAI last year, under which Broadcom committed to deploying a total of 10 GW of computing capacity for OpenAI by 2029.

In addition, Broadcom also plans to deploy 3 GW of computing capacity for Meta by the end of 2028. Tan disclosed that the first 1 GW of this order will begin delivery in the second half of next year.

Q3 total revenue guidance is strong—why is the market still finding fault?

Broadcom’s Q3 total revenue guidance will set a new single-quarter record and exceed market expectations. This guidance itself is positive, indicating that the company’s overall business continues to demonstrate stronger-than-expected momentum.

However, AI semiconductors are currently the core narrative driving Broadcom’s stock price. Investors are buying Broadcom not merely because it is a semiconductor and software giant, but because it is viewed as one of the most significant AI chip beneficiaries outside of NVIDIA.

Broadcom has signed and expanded long-term collaborations with clients such as Google, Anthropic, and Meta to supply custom AI accelerators and networking chips. The market is betting that these multi-year orders will quickly translate into quarterly revenue and drive continued upward revisions for AI semiconductor performance.

This earnings report confirms that this trajectory remains intact, though the pace of revenue recognition may not be as rapid as the most optimistic investors anticipated. There is a timing gap between long-term orders, customer capital expenditures, supply chain deliveries, and quarterly revenue recognition—meaning that even with high growth in AI-related business, quarterly guidance could fall short of elevated expectations.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/joryn