Elon Musk's 'space computing dream' is moving from science fiction toward economic modeling, but the numbers don’t add up easily. According to a recent SemiAnalysis report, deploying equivalent GPU clusters in space currently costs 3.6 times more than on Earth, with claims of 'free solar power' and 'free cooling' significantly overstated. Under baseline assumptions, cost parity may not be achieved until 2040. However, the real bottleneck for AI expansion lies not in power but in chips. Ground-based data center capacity additions are expected to peak by 2028, while chip production continues to scale—potentially accelerating cost parity to the early 2030s.

The narrative around space-based data centers is gaining traction. While Elon Musk’s vision for orbital computing isn't entirely divorced from economic logic, SemiAnalysis estimates that its realization hinges not on surface-level claims like 'free energy in space,' but on multiple practical constraints: chip availability, launch costs, thermal management systems, and the reliability of lifespan and maintenance.

Elon Musk has frequently discussed orbital computing this year. In February, during the Dwarkesh Podcast, he predicted that within five years, the annual AI computing capacity operating in space could surpass the total cumulative capacity ever deployed on Earth, citing a potential scale of 'hundreds of gigawatts per year.' SpaceX also stated in its S-1 filing on May 20 that its long-term goal is to launch 100 gigawatts of computing capacity into space annually, arguing that space-based computing will significantly expand AI computational scale and improve token economics.

In a deep-dive report published on June 3, SemiAnalysis noted that deploying AI data centers in orbit using current technology remains substantially more expensive than terrestrial alternatives. For example, a 30.5kW B300 cluster scheduled for deployment in 2026 would incur a total project capital cost of $4.1 million in space versus $1.4 million on the ground. When annualized into monthly total cost of ownership (TCO), space deployment amounts to approximately $100,900 per month compared to about $27,700 per month on Earth.

In a deep-dive report published on June 3, SemiAnalysis noted that deploying AI data centers in orbit using current technology remains substantially more expensive than terrestrial alternatives. For example, a 30.5kW B300 cluster scheduled for deployment in 2026 would incur a total project capital cost of $4.1 million in space versus $1.4 million on the ground. When annualized into monthly total cost of ownership (TCO), space deployment amounts to approximately $100,900 per month compared to about $27,700 per month on Earth.

According to the analysis, under baseline assumptions, levelized computing costs between space- and ground-based data centers may reach parity only around 2040. By the early 2030s, space-based data centers could still cost roughly 30% more than terrestrial ones—but this premium might already be low enough to open a window for initial large-scale deployments. In its 'Musk scenario,' where ground-based data center expansion becomes constrained while chip manufacturing capacity continues to grow, cost parity for space computing could arrive as early as the beginning of the 2030s.

Right now, putting computing power into orbit still doesn’t make financial sense.

Using the 2026 B300 cluster as a reference point, the gap is strikingly clear.

A 30.5kW B300 cluster comprising 16 GPUs incurs a total project capital expenditure of approximately $4.1 million when deployed in space, compared to about $1.4 million for terrestrial deployment. Converted into monthly total cost of ownership, space deployment costs $100,925 per month versus $27,724 per month on the ground.

Reframed using a metric more common in cloud services:

Space deployment TCO: $8.64/hour/GPU

On-premises deployment TCO: $2.37 per GPU-hour

Space-based deployment LCOC: $10.91 per GPU-hour

On-premises deployment LCOC: $2.49 per GPU-hour

LCOC is a more accurate reflection of true compute costs than TCO, as it incorporates availability, redundancy, and fault tolerance. On-premises clusters require only about a 5% cost premium, whereas space-based clusters—due to radiation effects and the inability to perform on-site repairs—require approximately a 26% cost uplift.

The cost gap is not primarily in the GPUs themselves. Capital expenditures (CapEx) for IT equipment are nearly identical: approximately $981,000 for space-based deployment versus $986,000 for on-premises. The difference lies in the 'data center' infrastructure itself.

Capital expenditures for space-based data center infrastructure amount to approximately $3.1 million, compared to just $382,000 for on-premises facilities. Of this, launch costs alone account for $1.6 million. More critically, asset lifespans differ significantly: space-based data center infrastructure is depreciated over 5 years, while ground-based infrastructure uses a 15-year depreciation schedule. As a result, the per-GPU-hour capital cost for space-based deployment is $6.29, versus only $0.36 for on-premises—a difference of roughly 17x.

This also explains why 'free solar energy' does not automatically translate into 'cheap compute.' While electricity costs are significant in terrestrial data centers, they are not the sole driver of total cost of ownership (TCO). For space-based operations, launch costs, thermal management, structural design, power systems, asset lifespan, and reliability dominate the cost structure.

The notions of 'free solar power' and 'free cooling' are often oversimplified.

The four most common optimistic arguments for space-based data centers largely need to be reevaluated.

First, low Earth orbit (LEO) does not provide 24/7 sunlight. The International Space Station and most Starlink satellites operate in LEO, orbiting Earth approximately 15 times per day, and receive direct sunlight only about 60% of the time on average. Although the theoretical solar irradiance is 1,361 W/m², a LEO data center may capture only around 800 W/m² when averaged over 24 hours. During eclipse periods, batteries must supply 100% of the IT load.

Sun-synchronous orbits—particularly those near the dawn-dusk terminator—are better suited for data centers. Such orbits can remain sunlit for most of the time, but may still experience eclipse periods of up to 35 minutes per day. Reduced battery requirements do not mean they disappear entirely.

Second, space is cold, but that does not mean heat dissipation is free. Ground-based data centers rely on air and water systems to carry away heat, whereas in space, there is virtually no medium for convective cooling—radiation is the only option. The International Space Station’s radiator system, for example, can reject only 70 kW of heat with a surface area of 325 **** meters, at a cost of $340 million to $500 million. Although this system uses older technology and is expensive, it illustrates a key fact: thermal management is one of the primary structural constraints for orbital computing capacity.

Third, while light travels faster in a vacuum, this does not guarantee low latency for end users. Low Earth orbit (LEO) satellites circle the Earth approximately 15 times per day, and their visibility window over any given ground station typically lasts only 5 to 7 minutes. Missing this window forces data to be relayed via inter-satellite links or rerouted through other gateways. For instance, a satellite serving U.S. users while positioned over the Indian Ocean could introduce 30 to 80 milliseconds of one-way latency due to multiple inter-satellite hops. Additionally, optical ground links are susceptible to atmospheric interference, necessitating a globally distributed network of ground stations.

Fourth, space is not without 'capacity constraints.' Dawn-dusk sun-synchronous orbits represent only a narrow subset of LEO—not an infinite parking lot. Estimates of total LEO capacity range from 100,000 to over 1 million satellites, but sun-synchronous orbits require specific altitude-inclination relationships, commonly concentrated between 600 and 800 kilometers. The subset truly suitable for continuous solar exposure—the dawn-dusk orbits—is even narrower. As for the Sun-Earth Lagrange Point L1, while it does offer persistent sunlight, the round-trip light path between Earth and L1 is approximately 3 million kilometers, resulting in a round-trip light-time delay of about 10 seconds, rendering it impractical for latency-sensitive applications.

Ground-based power supply may become tight, but not so constrained that moving to space becomes the only option.

For space-based data centers to become a 'must-have' solution, the prerequisite is not merely tight terrestrial power supply, but rather the exhaustion of all available layers of ground-based power supply.

This framework divides new ground-based power supply into four layers:

Grid-connected power supply

Repurposing Bitcoin mining facilities and existing electrified land

Behind-the-meter generation, i.e., self-contained power sources

Industrial capacity and workforce expansion

The first layer is grid interconnection, which appears cheapest on paper, with infrastructure costs ranging from approximately $12 million to $15 million per MW. However, the real issue is the interconnection queue. In PJM’s Northern Virginia region, the actual grid interconnection timeline is approaching seven years. Grid reliability margins across U.S. ISO regions have declined from 70.2 GW in 2021 to an estimated 18.3 GW in 2025, narrowing further to 15.9 GW in 2026, turning negative by 2027, and resulting in a cumulative shortfall of approximately 40 GW by 2030. While this sounds dire, grid interconnection is not the only path available on the ground.

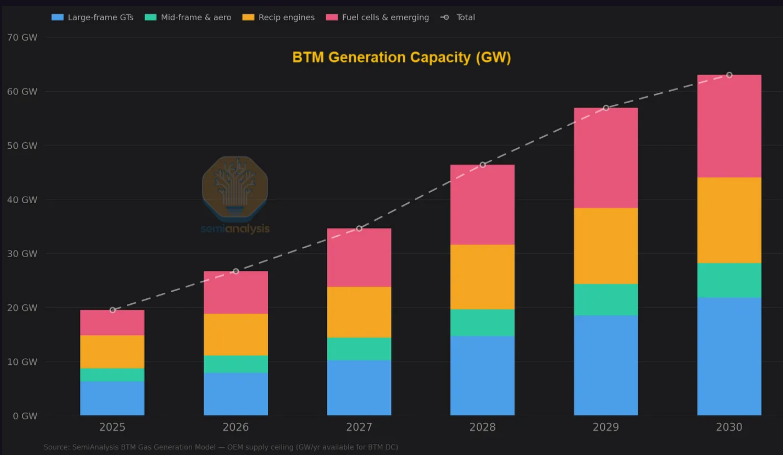

The second layer involves retrofitting existing power assets, with cryptocurrency mining facilities representing the most typical conversion case. Projects by Core Scientific, IREN, Cipher Mining, Applied Digital, TeraWulf, and others are expected to deliver approximately 2 GW of contracted retrofitted capacity by the end of 2026, rising to about 5 GW by the end of 2027. Overall, already energized sites and retrofitted locations could contribute 8–10 GW of near-term supply, including roughly 8 GW cumulatively from converted crypto mining sites by 2028. Costs range from approximately $10 million to $15 million per MW—comparable to or even lower than grid interconnection solutions.

The third layer is behind-the-meter generation. Previously viewed as a last resort, it has now become a viable option. The rationale is straightforward: AI cloud contracts can generate annual revenues of approximately $12 million to $13 million per MW of critical IT load. Bringing 200 MW online six months earlier could yield a net present value of $400 million to $500 million. As long as compute demand remains robust, building dedicated generation capacity—even at higher capital expenditure—is economically justifiable.

The levelized cost of behind-the-meter generation ranges from approximately $110 to $170 per MWh. In major U.S. markets, grid electricity prices may already reach around $150 per MWh. By 2028, behind-the-meter generation could account for half of all new power capacity additions for AI data centers—a share that stood below 7% in 2025. Confirmed behind-the-meter critical IT capacity is projected to reach approximately 26 GW by the end of 2030, with undisclosed projects potentially adding even more.

The fourth layer represents harder industrial bottlenecks: transformers, grain-oriented electrical steel, copper, gas turbines, construction labor, and cooling equipment. Lead times for large power transformers are lengthy, and copper prices have risen nearly 20% over the past year. Modularization and digitalization can reduce on-site labor requirements by more than 50%, but as compute infrastructure scales into the hundreds of gigawatts, skilled labor hours will become a binding constraint. Once this layer is engaged, costs exceed $20 million per MW—the exact magnitude depending on how rapidly the industry attempts to extract additional capacity.

Therefore, terrestrial supply is not infinite. However, it is not a single-layer system that will hit a hard ceiling imminently. For space-based solutions to become competitive, they must wait until terrestrial deployment progresses through all four layers and costs rise significantly.

What is truly constraining AI expansion first is chips—Terafab is the key variable.

Space-based data centers cannot resolve the most upstream bottleneck: without chips, there are no clusters.

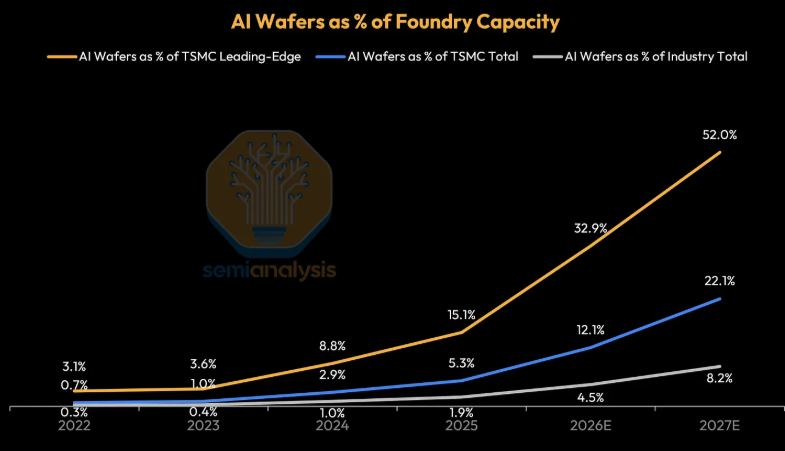

The current constraint has already shifted from data center capacity to semiconductor manufacturing, particularly Taiwan Semiconductor’s N3 advanced process node, as well as HBM and DRAM capacity. AI-related demand is projected to consume nearly 60% of Taiwan Semiconductor’s N3 output in 2026 and approximately 86% in 2027, effectively crowding out capacity for smartphones and CPUs.

Memory capacity is equally tight. HBM consumes approximately three times the wafer capacity per bit compared to standard DRAM. The share of AI-related demand in total DRAM wafer capacity is expected to rise from 12% in 2023 to around 70% by 2027.

This is harder to scale up rapidly than power generation. Power projects have multiple technological pathways—grid-connected land-based facilities, gas turbines, and behind-the-meter generation can all help alleviate pressure. In contrast, advanced fabs require cleanroom construction first, followed by equipment installation and then process validation. Capital is not the only constraint; time and accumulated process expertise are equally binding. A more realistic window for meaningful relief appears to be 2032–2034 rather than 2027–2029.

Musk clearly recognizes the chip bottleneck. SemiAnalysis notes that this is precisely the context behind the Terafab Initiative.

When announcing Terafab in March 2026, Musk described it as a '1-terawatt-per-year compute factory.' Tesla, SpaceX, and xAI will jointly build it in Austin, with a budget of USD 20–25 billion. The initial target is 100,000 wafers per month, eventually scaling to 1 million wafers per month—roughly equivalent to 70% of Taiwan Semiconductor’s current global output. The project scope includes logic, memory, mask-making, advanced packaging, and testing, with approximately 80% of compute capacity allocated to space applications and 20% to terrestrial uses.

SemiAnalysis believes that even partial achievement of Terafab’s goals would constitute a meaningful success. However, the targets themselves are extremely ambitious: its Foundry Model shows that global 300mm foundry capacity will exceed 4 million wafers per month in 2025. If Terafab reaches 1 million wafers per month, it would represent 24% of global foundry capacity or 68% of Taiwan Semiconductor’s capacity.

The greater challenge lies in process intellectual property (IP) and memory. SemiAnalysis argues that Tesla lacks manufacturing IP—GAA transistor design, interconnects, lithography, etch recipes, and yield engineering are all held by incumbent players. If Terafab eventually achieves volume production, a more realistic path would likely be an integrated fab operating on licensed process nodes rather than developing advanced nodes from scratch.

Storage is even more challenging. HBM, LPDDR, and NAND each correspond to different manufacturing processes, and the IP is concentrated among $Samsung Electronics (005930.KR)$ 、 $SK Hynix (000660.KR)$and$Micron Technology (MU.US)$ manufacturers, among others. SemiAnalysis believes that long-term supply agreements or co-investment with existing DRAM manufacturers represent a more realistic path forward.

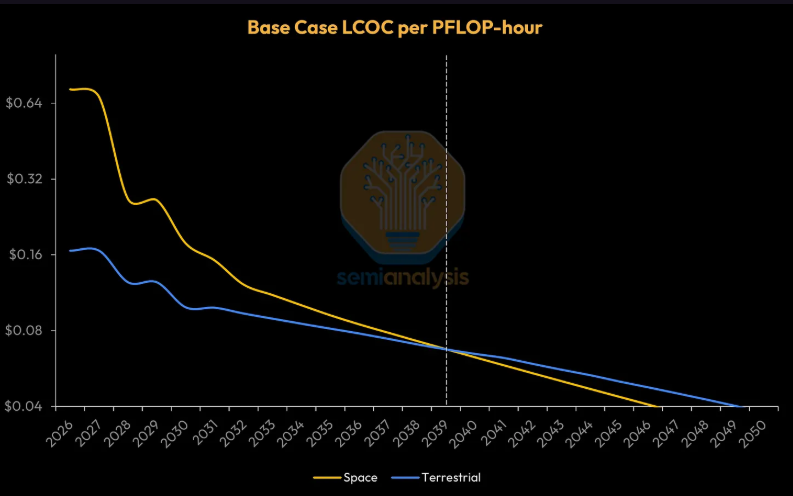

When will it go to space? Baseline scenario: around 2040; aggressive scenario: early 2030s

SemiAnalysis’s baseline scenario assumes that key engineering challenges—such as radiation effects and GPU reliability—will be sufficiently mitigated by around 2040, major cost components like launch, radiators, and solar power will achieve significant economies of scale, and both AI demand and chip capacity will grow substantially.

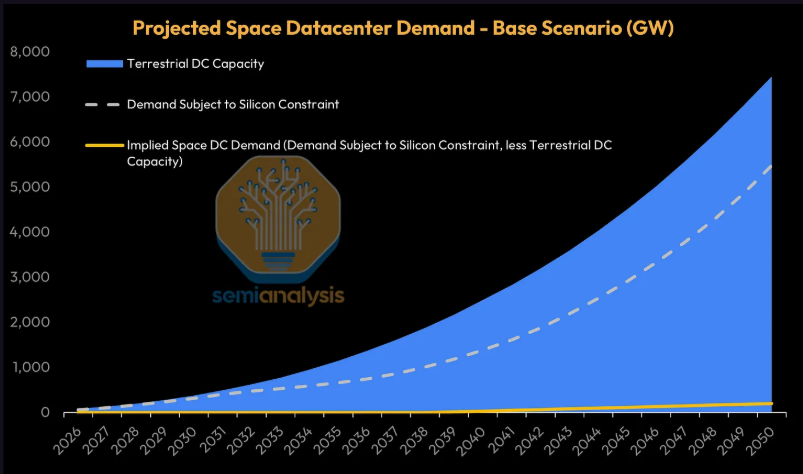

Under this scenario, the cost gap between space-based and terrestrial data centers—more than fourfold in 2026—will gradually narrow and reach parity around 2040. Beyond that point, the levelized cost of compute in space could fall below that on Earth.

However, this does not mean that commercial deployment of space-based data centers will not occur until 2040. SemiAnalysis states that by the early 2030s, space-based data centers could be only about 30% more expensive than terrestrial ones, potentially opening a window for the first large-scale deployments.

Another more aggressive 'Elon Musk scenario' assumes that new terrestrial data center capacity will peak in 2028 and remain constrained at low levels for decades, while chip manufacturing continues to expand. In this case, space becomes the only viable alternative for large-scale AI data center deployment, with a potential market reaching hundreds of gigawatts annually and approaching cost parity with terrestrial solutions by the early 2030s.

In other words, the commercialization timeline for space-based computing capacity depends on the relative pace of two trends: how quickly space systems can reduce costs, and how severely terrestrial data centers become constrained.

Investors should monitor five key validation points

SemiAnalysis’s conclusion implies that space-based AI data centers should not be simplistically viewed as merely a launch-capacity story or solely a power arbitrage play. Rather, it is a systems engineering challenge spanning semiconductors, power infrastructure, aerospace manufacturing, and data center economics.

First, whether advanced logic and HBM capacity can break through current bottlenecks. If chips remain the limiting factor, both space and terrestrial deployments will be constrained.

Second, whether launch costs can decline significantly. SemiAnalysis notes that SpaceX envisions Starship eventually reducing launch costs from the current Falcon 9 range of approximately $1,400–$1,800 per kilogram to around $250 per kilogram—an essential prerequisite for the cost curve of space-based data centers.

Third, whether radiators, solar arrays, and battery systems can achieve cost reductions at scale. Thermal management is not a peripheral issue but a core engineering constraint for orbital computing.

Fourth, how reliability and maintenance challenges will be addressed. On Earth, roughly 3% to 6% of GPUs in data center clusters experience failures each year requiring human intervention. Space deployments will need to resolve this through robotics, higher component reliability, over-provisioning, or a combination of these approaches.

Fifth, whether terrestrial data centers truly remain constrained over the long term. Under SemiAnalysis’s baseline scenario, even if space-based and terrestrial solutions reach cost parity, terrestrial capacity remains relatively abundant—making space deployment a matter of preference or optimization rather than necessity. Only if regulatory, permitting, grid, and industrial capacity constraints persistently suppress terrestrial expansion will space transition from an option to a requirement.

Therefore, Musk’s 'space-based computing power dream' is not without a viable path forward, but its key lies not in slogans, but in the cost curve. According to the SemiAnalysis model, the true inflection point is not today, nor will it arrive solely through rocket reusability; it requires simultaneous progress in chips, launch systems, thermal management, solar power, and on-orbit operations. The baseline estimate points to cost parity around 2040, while the more aggressive projection suggests approaching parity as early as the early 2030s.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/joryn