Deutsche Bank believes the market has underestimated Broadcom's long-term potential: order visibility now extends into 2028, which in itself sends a positive signal. The bank forecasts AI-related revenue of $125 billion for fiscal year 2027—above the company’s own guidance—and projects it will surge to $190 billion in 2028, which represents the true core of Broadcom’s AI narrative.

$Broadcom (AVGO.US)$ It delivered an impressive quarterly report, with strong AI business momentum carrying through to its guidance for the next quarter—but CEO Hock Tan held firm on long-term targets, declining to raise Broadcom’s AI revenue forecast for fiscal year 2027. The market responded immediately with a sell-off, sending Broadcom shares plunging nearly 14% at the U.S. market open today. However, Wall Street analysts were quick to weigh in: this was a misjudgment, they argued, as Broadcom’s true growth potential will only be fully realized beyond 2027.

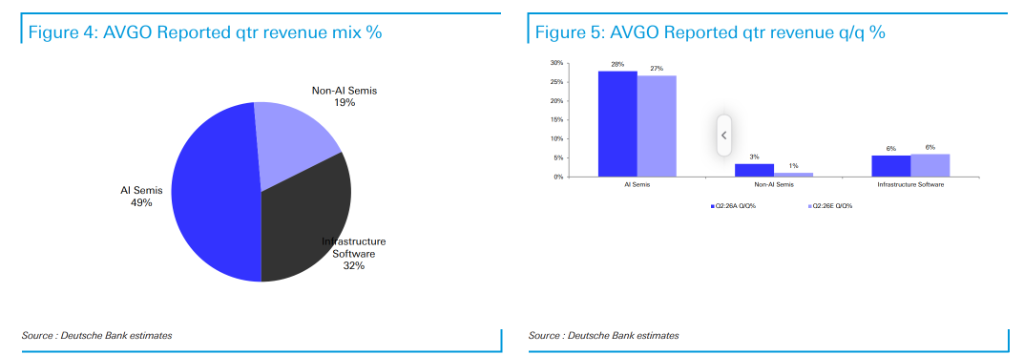

According to the latest earnings report, Broadcom’s AI revenue for Q2 of fiscal year 2026 (ended April 2026) reached $10.8 billion, up 145% year-over-year and 28% quarter-over-quarter. Total revenue came in at $22.187 billion, a 48% year-over-year increase, both figures exceeding market expectations. Guidance for the third fiscal quarter remains robust: total revenue of $29.4 billion (up 33% sequentially and 84% year-over-year), with AI revenue projected at $16 billion (up 48% sequentially and 210% year-over-year).

However, according to Citi analyst Atif Malik, the $16 billion AI revenue guidance fell short of his own estimate of $17.5 billion and below the consensus market expectation of $16.3 billion. Simultaneously, Hock Tan merely reaffirmed—without raising—the existing target of 'over $100 billion' in AI revenue for fiscal year 2027, directly triggering investor disappointment.

However, according to Citi analyst Atif Malik, the $16 billion AI revenue guidance fell short of his own estimate of $17.5 billion and below the consensus market expectation of $16.3 billion. Simultaneously, Hock Tan merely reaffirmed—without raising—the existing target of 'over $100 billion' in AI revenue for fiscal year 2027, directly triggering investor disappointment.

One detail overlooked by the market may hold the key: Hock Tan revealed that Broadcom’s visibility into AI demand has extended from 'through 2027' three months ago to 'through 2028.' Second-quarter bookings surpassed $30 billion, and AI revenue is expected to double between the first and second halves of fiscal year 2026, reaching approximately $56 billion for the full year—and entering fiscal year 2027 'well above' the $100 billion target.

In a post-earnings research note, Deutsche Bank analyst Ross Seymore sharply raised Broadcom’s price target from $430 to $515, maintaining a Buy rating and explicitly framing the recent pullback as a 'buying opportunity.' He attributed the lack of an upward revision to long-term guidance primarily to 'management’s conservative stance, rather than factors such as market share loss or delays in data center build-outs,' and forecasted Broadcom’s AI revenue for fiscal year 2027 at $125 billion (approximately 25% above the company’s current guidance), rising further to roughly $190 billion in fiscal year 2028. Deutsche Bank also raised its calendar-year 2027 revenue and EPS forecasts by about 15% each.

All earnings metrics beat expectations—the only 'miss' was the long-term target.

Core metrics for the second fiscal quarter exceeded expectations across the board: total revenue of $22.187 billion, above the consensus estimate of $22.053 billion; AI revenue of $10.8 billion, up 145% year-over-year; non-GAAP earnings per share of $2.44, surpassing the consensus of $2.39; and adjusted gross margin of 77.1%, slightly ahead of the expected 76.9%. Within segment performance, networking chip revenue totaled $4.304 billion (up 144% year-over-year), while computing offload/accelerator revenue reached $6.496 billion (up 146% year-over-year).

Third-quarter guidance also strengthened broadly: total revenue of $29.4 billion, above the prior consensus of $28.3 billion. The Infrastructure Software segment is guided to grow 24% sequentially, primarily benefiting from VMware’s exposure to server CPU demand under core-based pricing, a trend the company expects to persist beyond the third fiscal quarter.

Yet the core source of market disappointment boils down to one point: although Hock Tan expressed 'greater confidence' in the fiscal year 2027 target, he declined to provide a higher specific figure. For investors anticipating a 'jaw-dropping' outlook, his silence was interpreted as a risk signal.

Analysts: Conservatism, Not Weakening Fundamentals

Ross Seymore of Deutsche Bank offered a markedly different interpretation.

In his view, the extension of visibility from 'through 2027' to 'through 2028' within just three months is itself a significant positive signal; second-quarter bookings exceeding $30 billion and the trajectory for AI revenue to double between the first and second halves of fiscal 2026 both point to sustained strong demand. Hock Tan’s previous target of 'over $100 billion' was already conservative—Deutsche Bank’s forecast now stands at $125 billion.

Ross Seymore believes Broadcom’s leadership in XPUs (custom acceleration chips) and networking switches will continue to translate into substantial revenue and earnings-per-share growth. In his research note, he wrote that as AI revenue growth significantly outpaces operating expense expansion, operating margins are expected to remain stable overall, if not slightly improve.

Atif Malik of Citi adopted a relatively cautious stance but maintained a Buy rating and a $500 price target. He noted that the AI guidance for the third fiscal quarter fell short of Citi’s expectations, and the operating margin guidance of 67% for the same quarter was below Citi’s estimate of 68.6% and the consensus market expectation of 67.5%. Key points to watch during the upcoming earnings call include supply chain updates, gross margin implications, and VMware renewal trends. Citi also positioned its valuation at the lower end of the recent 20–40x range to reflect heightened competitive risks.

The real explosion: The truly explosive figures begin only after 2027

According to Deutsche Bank’s forecast, Broadcom’s AI revenue trajectory is projected at approximately $56 billion in fiscal 2026, around $125 billion in fiscal 2027, and roughly $190 billion in fiscal 2028.

On a company-wide basis, Deutsche Bank forecasts total revenue of approximately $105.8 billion in fiscal 2026 (up 66% year-over-year), about $179.8 billion in fiscal 2027 (up 70% YoY), and roughly $246.8 billion in fiscal 2028 (up 37% YoY). Non-GAAP EPS is projected at approximately $18.30 in fiscal 2027 and about $21.80 in fiscal 2028.

In the earnings release, Hock Tan described demand for AI-driven XPUs and networking as 'almost impossible to meet,' with visibility into major customers’ custom chip requirements now extending into 2028. Analysts’ logic is therefore clear: the market is disappointed by fixating on the outdated '$100 billion' target, overlooking the leap from $125 billion to $190 billion—that is the true core of Broadcom’s AI investment narrative.

Gross margins face near-term pressure, but operating margins are expected to remain robust

The main negative signal from this earnings report stems from the gross margin outlook.

Adjusted gross margin for the third fiscal quarter is guided to decline by approximately 3 percentage points sequentially, primarily due to the continued increase in AI revenue as a share of total revenue (AI revenue is expected to account for about 78% of semiconductor revenue in the third fiscal quarter). Deutsche Bank believes this structural dilution effect from AI will persist.

However, Ross Seymore believes that the rapid growth in AI revenue will significantly outpace the expansion of operating expenses, more than offsetting the drag from declining gross margins on operating margin, which is expected to remain broadly stable or even improve slightly.

Another noteworthy detail concerns capital returns: the company distributed approximately $3 billion in dividends this quarter but repurchased only about $600 million in shares—significantly below its usual level—and repaid approximately $1.25 billion in debt. Deutsche Bank assesses that the company may be proactively accumulating cash to meet the capital expenditure needs driven by rapidly growing AI demand.

Two major institutions maintain their Buy ratings, characterizing the recent pullback as a buying opportunity.

Deutsche Bank raised its price target from $430 to $515 (an increase of approximately 20%), implying about 23x non-GAAP EPS for calendar year 2027, and maintained its Buy rating. Ross Seymore explicitly stated that the long-term investment thesis remains unchanged and that the current pullback represents a rare buying window.

Citi maintained its $500 price target (implying approximately 20x FY2028 EPS) and Buy rating. Atif Malik noted that Citi estimates roughly 35% to 40% of Broadcom’s revenue comes from Google, its largest customer, and highlighted that this high customer concentration risk warrants ongoing attention.

Editor/Lambor