In the second fiscal quarter, Ciena reported a 40% year-over-year increase in revenue and a 290% increase in EPS, both accelerating above expectations. The company’s revenue guidance ranges for the third fiscal quarter and the full fiscal year are both above market expectations, with the midpoint of the full-year guidance at the high end of its previously provided range. However, the degree of upside surprise is modest, offering limited excitement, and the margin guidance for the third fiscal quarter remains largely flat compared to the prior quarter.

Ciena, a star in the optical communications industry and a beneficiary of the AI data center infrastructure boom, reported stronger-than-expected results for its last fiscal quarter and raised its full-year revenue guidance—but failed to impress equity investors who had already priced in exceptionally high expectations.

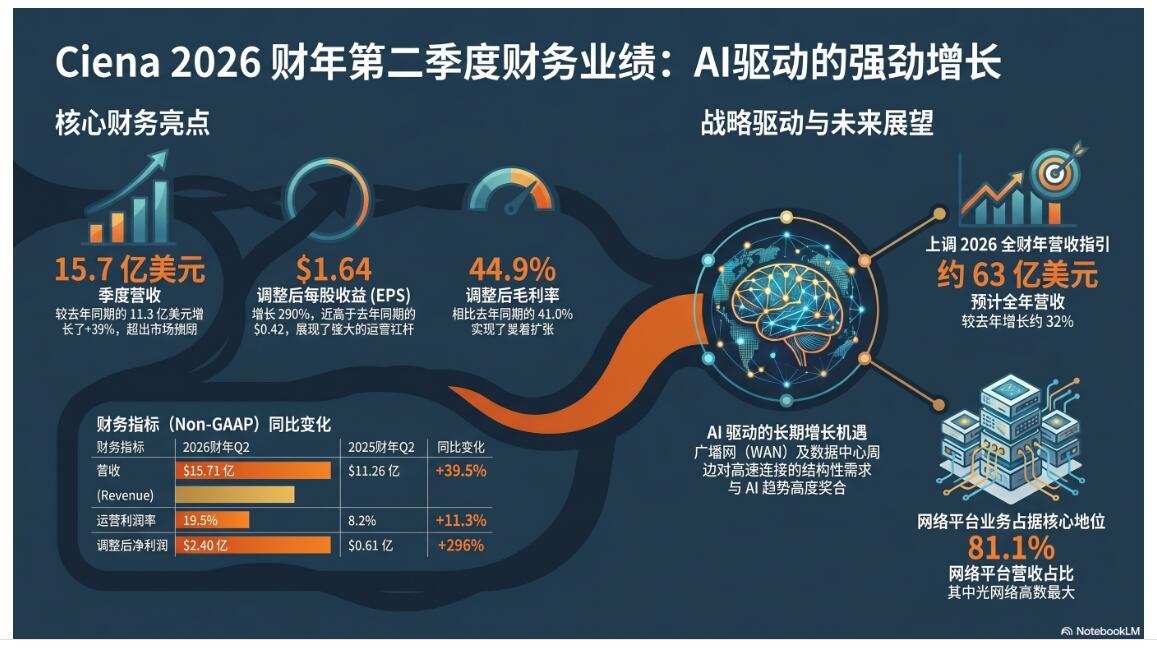

On Thursday, April 4 (U.S. Eastern Time), Ciena reported that for the second fiscal quarter of fiscal year 2026 (the “second quarter”), which ended May 2, 2026, revenue rose nearly 40% year-over-year to $1.57 billion—approximately 4.7% above market consensus expectations.

Profitability was even more impressive. Ciena’s adjusted gross margin for the second quarter increased to 44.9% from 41% a year earlier, while its adjusted operating margin surged more than twofold to 19.5% from 8.2% in the prior-year period. Driven by strong revenue growth, an improved product mix, and operating leverage, adjusted earnings per share (EPS) jumped nearly 290% year-over-year to $1.64—over 12% above analyst estimates.

Profitability was even more impressive. Ciena’s adjusted gross margin for the second quarter increased to 44.9% from 41% a year earlier, while its adjusted operating margin surged more than twofold to 19.5% from 8.2% in the prior-year period. Driven by strong revenue growth, an improved product mix, and operating leverage, adjusted earnings per share (EPS) jumped nearly 290% year-over-year to $1.64—over 12% above analyst estimates.

In terms of guidance, Ciena projected third-quarter (the “third quarter”) revenue of $1.575 billion to $1.675 billion and full fiscal-year 2026 revenue of $6.2 billion to $6.4 billion. At the midpoint of the new range, full-year revenue would represent approximately 32% year-over-year growth, with the new midpoint aligning with the high end of its previous guidance range. Both the current-quarter and full-year guidance ranges exceed market expectations.

Following the earnings release, Ciena’s stock not only failed to reverse Wednesday’s decline on Thursday but accelerated downward, closing down nearly 13.7%. This wiped out its cumulative gains over the past month, turning them negative, although the stock is still up more than 120% year-to-date.

Analysts believe the sell-off was not due to weak results—in fact, both performance and guidance were robust. A more plausible explanation is that markets had already priced in high expectations for AI, data center interconnectivity, and optical networking demand. Although the results were solid, they were insufficient to justify further re-rating, prompting investors to take profits and reassess the trajectory of future growth and margin expansion potential.

Both revenue and EPS beat expectations, primarily driven by surging demand and improved delivery execution.

Ciena’s second-quarter revenue came in at $1.57 billion, $70 million above the consensus estimate of $1.5 billion, with year-over-year growth accelerating to nearly 40% from 33% in the prior quarter. For a network equipment provider, this pace of growth is notably strong, reflecting improvements on both the demand and delivery fronts.

Company management attributed the strong performance to robust demand across its product portfolio and effective execution amid a complex supply chain environment. In other words, growth was not driven by a single product or customer but reflected broad-based demand across multiple product lines, including optical networking and routing & switching.

In the second quarter, Ciena’s adjusted EPS reached $1.64, exceeding the consensus estimate of $1.46 by $0.18. Year-over-year EPS growth accelerated to 290% from 111% in the prior quarter. With rapid revenue growth accompanied by meaningful improvements in both gross and operating margins, profit elasticity significantly outpaced top-line growth—making this one of the most notable highlights of the earnings report.

Profit margins have improved significantly, and operating leverage is being realized.

In Q2, Ciena reported an adjusted gross margin of 44.9%, up 3.9 percentage points from 41.0% in the same period last year; its adjusted operating margin was 19.5%, an increase of 11.3 percentage points from 8.2% a year earlier.

This indicates that the company is not relying on low pricing to boost revenue, but rather achieving a better product mix and higher operational efficiency at a larger revenue scale. While revenue grew by 40%, adjusted EPS surged nearly 290%, reflecting a classic operating leverage effect: as fixed costs are spread over a larger revenue base, profit growth significantly outpaces revenue growth.

However, margins could also be a point of concern for the stock price decline. The company’s guidance for Q3 adjusted gross margin is approximately 45%, essentially flat compared to Q2’s 44.9%; adjusted operating margin is expected to range between 19% and 20%, with a midpoint close to the 19.5% reported in the second fiscal quarter.

In other words, while the earnings report shows a substantial improvement in profitability, the market may have been looking for further upside, whereas the company’s near-term guidance suggests more of a ‘high-level stabilization.’

Optical networking remains the primary growth engine, while routing and switching is growing even faster.

From a business segment perspective, Optical Networking remains Ciena’s largest source of revenue. In Q2, this segment generated approximately $1.1 billion in revenue, up roughly 42% year-over-year, accounting for about 70% of the company’s total revenue.

This reflects strong ongoing demand from cloud providers and telecom operators for high-capacity optical transport equipment amid global network infrastructure upgrades. With data traffic surging due to AI training and inference workloads, capacity requirements for data center interconnects, metro networks, and long-haul transmission links continue to rise—positioning Ciena, as a leading optical networking equipment supplier, to benefit from this investment cycle.

The Routing and Switching segment is growing even faster. Revenue from this segment reached $174.2 million in Q2, nearly doubling year-over-year. Although its scale remains much smaller than that of the Optical Networking business, its high growth rate indicates that Ciena’s expansion is not solely dependent on traditional optical transport products—its routing and switching offerings are also gaining traction with customers.

Full-year guidance has been raised, though the degree of outperformance is relatively modest.

Ciena expects third-quarter revenue to range between $1.575 billion and $1.675 billion, with a midpoint of $1.625 billion—approximately $70 million, or about 4.5%, above the market consensus estimate of $1.555 billion.

Full-year revenue guidance has been raised to $6.2 billion–$6.4 billion, with a midpoint of $6.3 billion, surpassing the market consensus of $6.183 billion and implying year-over-year growth of approximately 32%. This is undoubtedly a positive signal for the company’s fundamentals, indicating management’s continued confidence in demand and execution for the second half of the year.

However, from a market trading perspective, the full-year guidance midpoint is only about 1.9% above the consensus estimate. Given that the stock price had already priced in strong expectations for AI-driven network demand, investors may view this as a solid earnings report—but not one compelling enough to justify further valuation upside. Especially when the market had already front-run improvements in orders, revenue, and margins, a simple 'beat and raise' may no longer be sufficient.

Share repurchases continue, but they are not the key driver of the stock price

Ciena continued its share repurchase program in the second quarter, disclosing repurchases totaling approximately $83.1 million. Buybacks typically provide some support to earnings per share (EPS) and signal management’s willingness to return capital to shareholders.

However, Ciena’s current share price reaction is primarily driven by growth expectations and valuation metrics. For companies positioned within the AI networking infrastructure investment chain, the market focuses more on whether orders and revenue can sustain high growth over the coming quarters and whether margins can hold steady or even expand further. The impact of buybacks on short-term trading sentiment is relatively limited.

Why the sharp stock decline: Not due to poor results, but excessively high expectations

Following its earnings announcement, Ciena’s stock closed down nearly 14%—an outcome that appears contradictory to its ‘better-than-expected results and raised guidance,’ yet is not uncommon under market pricing dynamics.

The stock price may have already reflected highly optimistic expectations. Themes such as AI data centers, optical network upgrades, and cloud providers’ expanding capital expenditures have attracted significant investor interest in recent periods. As a key beneficiary of these trends, Ciena saw its valuation and market expectations elevated accordingly. In such an environment, delivering ‘good’ results merely meets expectations; only ‘exceptionally strong’ results could drive further upside.

Although guidance was raised, the degree of surprise was modest. The third-quarter revenue midpoint exceeded expectations by roughly 4.5%, and the full-year revenue midpoint was only about 1.9% above consensus. While this is positive for fundamentals, it may fall short of the ‘excess’ needed to sustain already elevated market sentiment.

Margin guidance indicates short-term marginal improvement or stabilization. Compared with the adjusted operating margin in Q2, the Q3 guidance range does not show a clear further expansion. Investors may be concerned that the strongest phase of this margin recovery has already been realized this quarter, and future performance will likely involve maintaining elevated levels rather than continuing rapid upward momentum.

The network equipment industry remains inherently cyclical. Ciena benefits from growth in optical networking and data traffic, but its customer base—including telecom operators, cloud service providers, and enterprise clients—may exhibit fluctuating capital expenditure patterns. The market’s sell-off following strong earnings may partly reflect growing investor focus on the sustainability of growth: after this year’s robust revenue acceleration, whether a similar growth trajectory can be maintained next year still requires further validation through new orders and customer demand.

Thus, this decline appears more like 'profit-taking and valuation reassessment amid high expectations' rather than a rejection of Ciena’s fundamentals. The earnings report itself shows improving demand, revenue, margins, and full-year outlook; however, stock prices reflect forward-looking expectations. When the market has already priced in high optimism, even a strong earnings report may trigger a sharp correction if it falls short of being 'exceptional.'

Editor/Stephen