① Although the Federal Reserve is certain not to raise interest rates this month, it may begin laying the groundwork for a future policy shift; ② The interest rate projections in the Fed’s quarterly 'dot plot' may soon cease to 'forecast' rate cuts—and the dot plot itself could even vanish into the annals of history…

Caixin News, June 5 (Editor: Xiaoxiang) — The interest rate projections in the Federal Reserve’s quarterly 'dot plot' may soon cease to 'forecast' rate cuts—and the dot plot itself could even vanish into the annals of history…

At that point, markets will have to determine whether Kevin Warsh, the Fed’s new chair, truly is the inflation hawk he has long claimed to be. If the answer is 'YES,' this would undoubtedly deliver a heavy blow to some investors.

The new Fed chair is currently working diligently to articulate his policy stance and is thoroughly consulting with his staff ahead of presiding over his first monetary policy meeting later this month. However, any briefings or recommendations he receives regarding the current policy trajectory are unlikely to offer an easy solution.

The new Fed chair is currently working diligently to articulate his policy stance and is thoroughly consulting with his staff ahead of presiding over his first monetary policy meeting later this month. However, any briefings or recommendations he receives regarding the current policy trajectory are unlikely to offer an easy solution.

On one hand, the investment frenzy ignited by artificial intelligence (AI) has been striking; on the other, the three-month-long war in Iran is exerting intense upward pressure on energy prices. The interplay of these two forces has already pushed inflation far above the Fed’s stated target. Compounded by an impending reshuffle within the Fed’s policymaking committee, this confluence of uncertainties has thoroughly rattled the futures market.

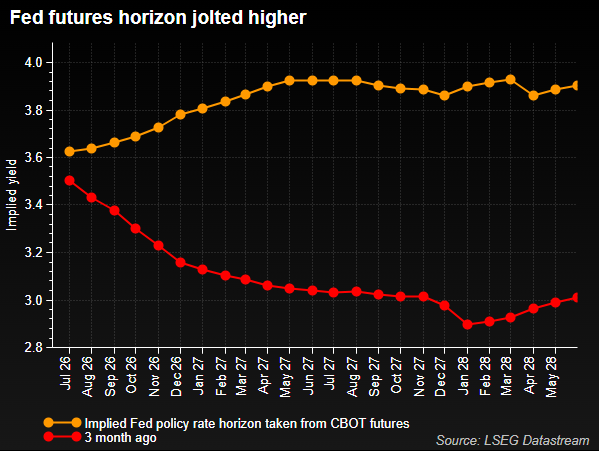

Currently, interest rate markets have priced in a rate hike as the Fed’s next move, which could occur as early as the end of this year.

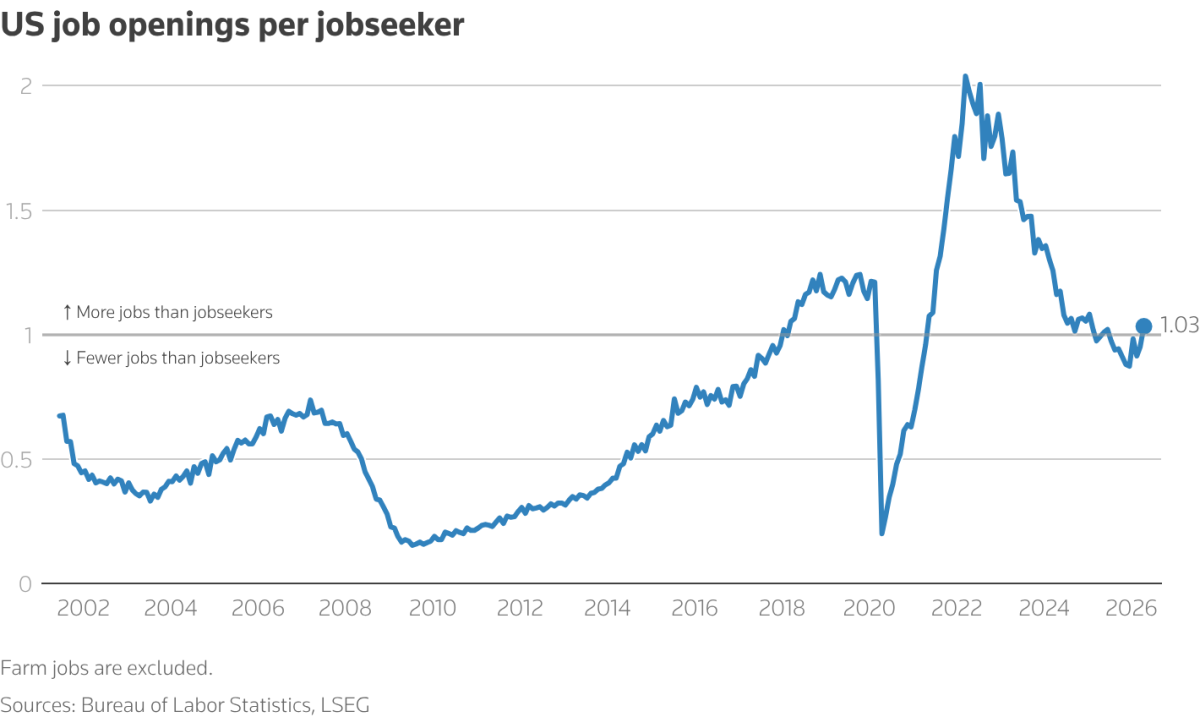

In recent months, one of the few remaining arguments available to Fed doves has been the possibility of cracks emerging in the labor market—the other half of the Fed’s dual mandate alongside inflation—which could be exacerbated by AI-related layoffs or spending cutbacks by energy-sector firms.

But so far, there is little evidence of such weakness. On the contrary, the labor market continues to demonstrate remarkable resilience, even showing signs of strengthening against the odds—surface-level data strongly support this trend, including the sharp surge in job openings in April and the unexpected addition of 122,000 private-sector jobs in May.

The nonfarm payrolls report for May, due for release this Friday, will serve as the most direct test of the veracity of this labor market strength.

The Federal Reserve’s 'tightening transformation' may begin as early as this month.

It is worth noting that although the Federal Reserve has absolutely no chance of raising interest rates this month, it may begin laying the groundwork for a future policy pivot.

In addition to closely watching for any subtle hints from Wallsh during the press conference, markets will also scrutinize whether the Fed removes the previous statement’s reference to being 'inclined toward further easing.' At the last FOMC meeting, three policymakers already voted in favor of dropping that language, and recently, at least one previously dovish member of the Board—Waller—surprisingly joined their ranks.

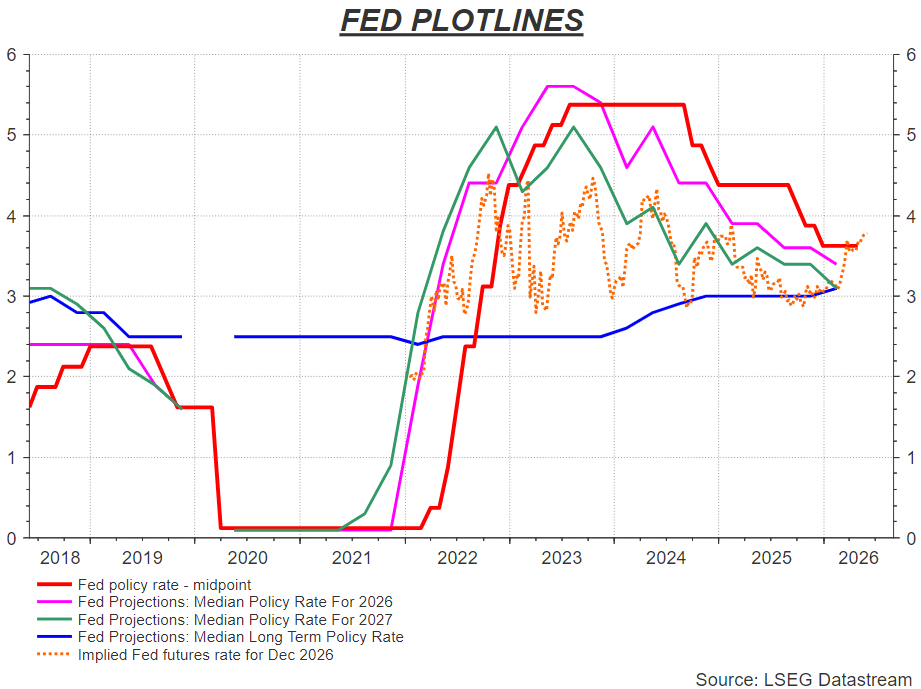

However, the economic projections updated quarterly by Federal Reserve officials—particularly the 'dot plot' that reveals policymakers’ projected interest rate path over the coming years—may attract the most attention. In March, Fed officials’ dot plot forecast one rate cut this year and another in 2027.

Yet, given the barrage of tentative signals from Fed officials since March, that single rate cut expected this year could very well be erased entirely from the dot plot. Whether the anticipated 2027 rate cut disappears as well—or whether the dot plot even shifts toward market expectations of rate hikes—could deliver the biggest shock to markets.

Ironically, Wallsh’s aversion to so-called forward guidance could lead him to push for abolishing the dot plot altogether. On this point, he may not stand alone; such a move could gain some internal support within the Fed—even from his predecessor and current Fed Governor Powell, who has repeatedly cautioned investors against placing undue faith in the dot plot.

Should the Fed completely eliminate any mention of further easing from its policy outlook and then effectively 'turn off the lights and walk away,' leaving markets to infer the policy path solely from incoming macroeconomic data, this could undoubtedly trigger more aggressive and volatile swings in interest rate markets in the second half of this year.

Will the 'hawkish-dovish two-faced' Wallsh need to first show his hawkish side?

Of course, some investors may still cling to a faint illusion—hoping that the U.S.-Iran conflict ends soon, thereby restoring the path toward monetary easing, or believing that the squeeze on real household incomes caused by the energy crisis will effectively dampen consumer demand and consequently bring other goods prices back under control.

However, a growing number of market participants now clearly recognize that the winds may have shifted decisively!

Tim Duy, macroeconomist at SGH, argues that the inflationary consequences triggered by soaring energy prices have now outweighed their negative impact on economic growth. The Federal Open Market Committee is undergoing a rapid and significant shift in stance, as members increasingly realize that the last rate cut implemented in December was, in fact, a pivotal mistake.

“Recognizing the growing risks posed by monetary policy, Federal Reserve officials are swiftly shifting to a hawkish stance, paving the way for rate hikes,” he said. “If Walsh remains the same Walsh as before, he would opt for an earlier rate hike. Of course, no one knows yet which Walsh will actually take the stage.”

This remark alludes to Walsh’s long-standing reputation as a monetary hawk, despite having adopted a dovish tone when seeking a position under a president who favors low interest rates.

Notably, Walsh has this week hired Paul Winfree, former budget director under Trump and economist at The Heritage Foundation, as one of his two advisors to assist with his transition into the role of Fed chair. Winfree is prominent in political and economic circles and personally authored the Federal Reserve reform section of the conservative manifesto 'Project 2025' in 2023. His reform blueprint explicitly includes a proposal to eliminate the Fed’s statutory mandate of 'maximum employment,' aiming instead to refocus the central bank exclusively on combating inflation.

Regardless, although Walsh’s actual stance on monetary policy after formally assuming office remains unknown, his assessment of the current economic situation is unlikely to align with the widespread prior assumption—that a Trump-nominated candidate would naturally lean dovish. Moreover, Trump has already made it clear that he would grant Walsh full autonomy in decision-making.

Currently, driven forcefully by the AI investment frenzy, the U.S. real economy and capital markets are exhibiting signs of overheating. Despite facing significant headwinds ahead—including energy crises, geopolitical turbulence, and tariff barriers—an increasing number of observers are openly questioning: what rationale could the Federal Reserve possibly have left for considering monetary easing?

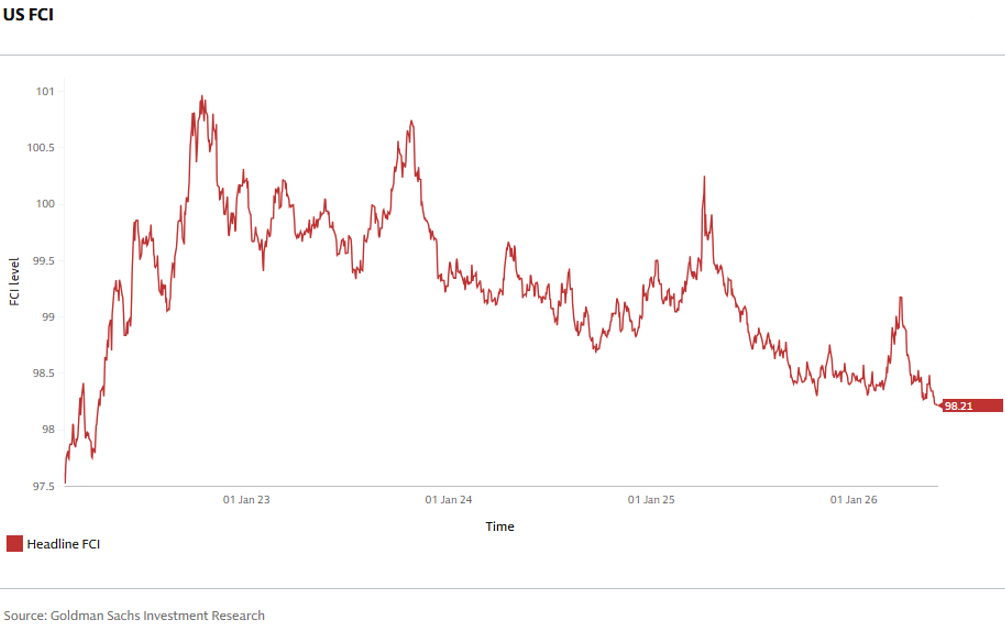

Although credit conditions have tightened somewhat in recent weeks, the Goldman Sachs U.S. Financial Conditions Index—which measures overall financial ease—has fallen to its most accommodative level in four years amid the stock market’s sharp rally. Meanwhile, Citigroup’s U.S. Economic Surprise Index has surged to its highest level in three years.

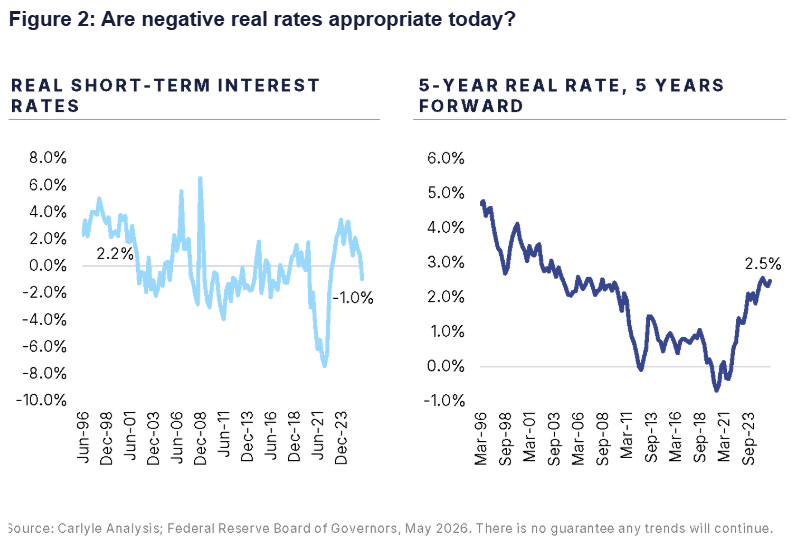

Reflecting on the Federal Reserve’s historic mistake during the late 1990s internet bubble—when it cut rates recklessly—Jason Thomas, Chief Strategist at Carlyle, remarked pointedly: “Injecting rate-cut stimulus during periods of highly concentrated capital expenditure unleashes a far more aggressive and potent boost than in virtually any other macroeconomic context.”

Thomas compared today’s scale of technology-related capital spending directly with that of the 'internet bubble' era and sharply noted that, after adjusting for inflation, current real short-term interest rates are over 300 basis points lower than they were back then. He concluded that the Fed “should have abandoned its deeply entrenched bias toward loose monetary policy long ago.”

All indications suggest that the policy reassessment and disruptive restructuring Walsh is poised to undertake may prove far more radical than the market has previously anticipated.

Editor /rice