SpaceX's trillion-dollar IPO represents the most ambitious capital spectacle in modern global financial history. It has forcibly redirected investors’ attention away from purely virtual algorithms and cloud-based models toward an era of 'heavy-industrial computing'—defined by starships, rocket launch towers, ultra-large-scale energy storage batteries, space-based laser routing systems, and nuclear power generation units. Yet behind the dazzling fireworks of its trillion-dollar valuation lie an astonishing rate of capital burn, an extremely concentrated corporate governance structure, and legal pitfalls riddled with massive related-party transactions and unresolved litigation.

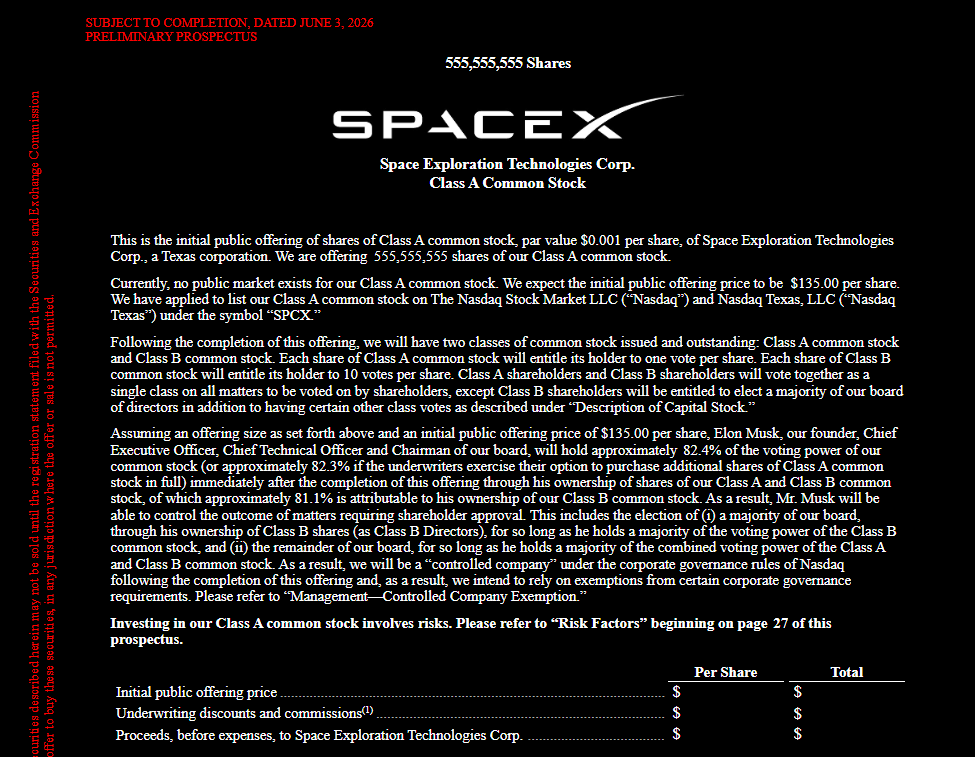

On June 4, $Space Exploration Technologies (SPCX.US)$ has just concluded its highly anticipated global roadshow.

According to the company’s latest S-1/A amendment to its registration statement filed with the U.S. Securities and Exchange Commission (SEC) on June 3, 2026, SpaceX will finalize its IPO pricing on June 11 and officially list on the Nasdaq exchange on June 12 under the ticker symbol “SPCX.”

As the largest initial public offering in the history of global capital markets, SpaceX’s debut is not only a record-breaking fundraising event but also represents Elon Musk’s vertically integrated vision—combining aerospace technology, low-Earth-orbit broadband constellations, geopolitical influence, and cutting-edge artificial intelligence (AI)—delivered to global investors in the form of a colossal prospectus.

As the largest initial public offering in the history of global capital markets, SpaceX’s debut is not only a record-breaking fundraising event but also represents Elon Musk’s vertically integrated vision—combining aerospace technology, low-Earth-orbit broadband constellations, geopolitical influence, and cutting-edge artificial intelligence (AI)—delivered to global investors in the form of a colossal prospectus.

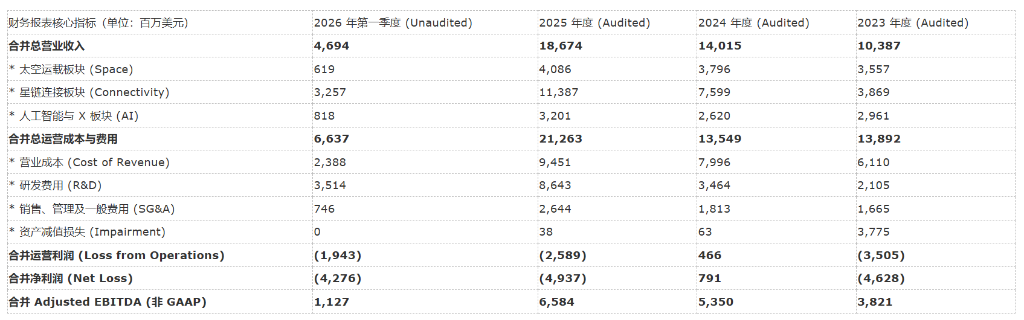

Restructured financial statements show that Starlink generated $11.38 billion in revenue in 2025, becoming the company’s core cash cow. However, due to heavy capital expenditures on Starship launch tower construction and a 1.0-gigawatt-scale ground-based computing cluster, the company reported a GAAP net loss of $4.937 billion for the full year 2025. With an initial free float of only 4.2%, coupled with Nasdaq-100’s accelerated inclusion rule (effective after 15 days) and a triple-weighting effect, the listing is expected to trigger significant equity dislocation and Short Gamma volatility in the tech sector during its early trading days in June.

SpaceX's trillion-dollar IPO represents the most ambitious capital spectacle in modern global financial history. It has forcibly redirected investors’ attention away from purely virtual algorithms and cloud-based models toward an era of 'heavy-industrial computing'—defined by starships, rocket launch towers, ultra-large-scale energy storage batteries, space-based laser routing systems, and nuclear power generation units. Yet behind the dazzling fireworks of its trillion-dollar valuation lie an astonishing rate of capital burn, an extremely concentrated corporate governance structure, and legal pitfalls riddled with massive related-party transactions and unresolved litigation.

This article will analyze the capital structure, financial data, and AI physical stack of this trillion-dollar IPO based on hundreds of pages of official S-1/A filings, audit reports, roadshow materials submitted by SpaceX, as well as liquidity assessments andTechnical Analysisanalyses from major Wall Street investment banks, including BNP Paribas, Goldman Sachs, Morgan Stanley, among others.

Capital Structure and Valuation Assessment: Reshaping the Global Financial Coordinate System

SpaceX’s listing will push the global capital market’s coordinate system into a new dimension, whether measured by absolute fundraising amount, implied valuation, or dilution leverage.

1. Offering Mechanism, Share Distribution, and Dilution Logic

The prospectus discloses that SpaceX plans to offer approximately 555.6 million shares of Class A common stock at an expected offering price of $135.00 per share. Without considering the underwriters’ exercise of the over-allotment option (Green Shoe), the base offering size amounts to $75 billion. Additionally, the company has granted the joint bookrunners—a syndicate led by Goldman Sachs, Morgan Stanley, BofA Securities, Citi, and JPMorgan—the right to purchase up to an additional 83,333,333 shares of Class A common stock within 30 days. If the Green Shoe option is exercised in full, total gross proceeds will reach $86.25 billion (with net proceeds of approximately $85.7 billion).

This scale is nearly three times that of Saudi Aramco’s 2019 IPO ($29.4 billion) and decisively surpasses all prior U.S. records—several times larger than Visa’s 2008 offering ($19.7 billion) and Facebook’s 2012 IPO ($16 billion).

Regarding its share capital structure, SpaceX underwent a 5-for-1 stock split (the '2026 Stock Split'), effective May 4, 2026. Following the offering, the number of outstanding shares of Class A common stock will amount to 7,380,196,910 (or 7,463,530,243 if the over-allotment option is exercised in full), while Class B common stock—carrying 10 votes per share—will total 5,695,668,265 shares. There will be no outstanding shares of Class C common stock (non-voting).

Based on an offering price of $135.00 per share:

Direct market capitalization: The aggregate market value directly attributable to the base Class A and Class B shares is approximately $1.765 trillion.

Fully diluted implied fair valuation: When accounting for potential dilutive instruments such as unexercised options and restricted stock units (RSUs), the prospectus discloses a hypothetical fully diluted market capitalization of up to $1.785 trillion.

According to the dilution schedule in the financial statements, as of March 31, 2026—prior to this IPO—the company’s book value per share was merely $2.25. After giving effect to the offering and deducting underwriting discounts and estimated offering expenses of approximately $55 million, the pro forma net tangible book value per share will increase to $7.85. This implies that:

Immediate dilution for new investors: External investors purchasing shares in the IPO at $135.00 per share will experience immediate dilution of $127.15 per share relative to the net tangible book value upon settlement.

Significant paper gain for insiders: Pre-IPO shareholders, led by Elon Musk, will see an immediate, non-cash increase in the net tangible book value of their holdings by $5.60 per share.

2. Absolute voting control under a dual-class share structure

As a legally designated 'controlled company,' SpaceX’s governance structure is heavily influenced by Elon Musk personally. Its Class B common stock carries 10 votes per share and may be voluntarily converted into Class A common stock at any time on a 1:1 basis.

As disclosed in the 'Beneficial Ownership' section of the prospectus:

Elon Musk’s shareholding structure: Elon Musk, individually and through trusts (including the Elon Musk Revocable Trust and EM 2024 GRAT-A Trust, of which he is trustee), collectively holds 849,494,440 Class A shares and 5,219,053,075 Class B shares (representing 91.6% of all outstanding Class B shares).

Voting power proportion: Following the completion of this IPO, Elon Musk will hold 82.4% of the aggregate voting power exclusively (which would be marginally diluted to 82.3% if the Green Shoe option is exercised in full).

Board election monopoly: Under the new charter, holders of Class B shares are entitled, as a separate class, to elect 51% of the board seats (i.e., “Class B directors”). This privilege remains effective as long as at least one Class B share remains outstanding. Given that Elon Musk holds an absolute majority of Class B shares, he has exclusive control over the appointment, removal, and replacement of these 51% of directors. Furthermore, his roles as CEO and Chairman of the Board are stipulated in the company’s charter as being removable only upon approval by a majority vote of Class B shareholders.

3. Sophisticated lock-up period and timed release mechanism

To prevent market supply-demand imbalances caused by the issuance of such a massive volume of new shares, the prospectus and lead underwriter Goldman Sachs have established an exceptionally complex lock-up arrangement (Lock-Up Agreements). Most notably, these include ‘staged automatic release’ (Timed Automatic Releases) provisions tailored to different shareholder groups:

Elon Musk and core management team: Committed to a full 366-day lock-up period. The 7.8 billion shares held by them (approximately 60% of the total shares outstanding post-IPO) are subject to no early release provisions and are ineligible for any exemptions tied to market recovery conditions.

Ordinary pre-IPO shareholders holding less than 10% and certain institutional investors: Their shares fall into two categories—‘180-day standard lock-up’ and ‘long-cycle lock-up.’ To avoid a cliff-like sell-off upon expiration of the 180-day period, the underwriters have designed the following release roadmap:

Phase One (post-Q2 earnings release): On the second trading day following the release of the quarterly financial results for the period ended June 30, 2026 (i.e., the ‘first earnings announcement date’), 20% of the shares subject to the 180-day lock-up (approximately 911.5 million shares) will be automatically released.

Phase Two (price-triggered release): If, during the 10 consecutive trading days surrounding the first earnings announcement date (inclusive), the closing price of Class A shares exceeds $175.50 (i.e., more than 30% above the $135 offering price) on at least five trading days, an additional 10% of locked-up shares (approximately 455.8 million shares) will be automatically released on the second trading day following the first earnings announcement date.

Calendar-based staged releases: On the 70th, 90th, 105th, 120th, and 135th days following the filing of the prospectus, 7% of the locked-up shares will be incrementally released on each respective date.

Final Lock-up Expiry: On the 180th day following the IPO prospectus filing, all remaining tradable shares will be released.

Through-the-Looking-Glass Financial Audit: The 'Money Printing' of Low-Earth Orbit Starlink vs. the Capital Black Holes of AI Compute and Star Wars

Understanding SpaceX’s financial statements hinges on recognizing its unique changes in consolidation scope. Given Elon Musk holds absolute controlling interests in SpaceX, xAI, and X Corp. (formerly Twitter), under U.S. GAAP provisions governing “Common Control Transactions,” both SpaceX’s acquisition of xAI in February 2026 and xAI’s acquisition of X Holdings (parent company of the X platform) in March 2025 are accounted for as a “Change in Reporting Entity” in the financial statements.

This means that the historical financial data presented in the prospectus does not reflect SpaceX’s standalone launch business alone, but rather incorporates a retrospective recast of the net assets and income statements of SpaceX, xAI, and the X platform since 2023.

(Summary financial overview table below)

1. Segment-Level Breakdown: Starlink’s Profitability Facade and the R&D Black Hole

Space Launch Segment (Space): High-Margin Government Contracts vs. Starship’s Heavy Capital Expenditures

The space launch segment serves as SpaceX’s technological flagship. However, because it allocates over 70% of Falcon 9 launch capacity free of charge to internally deploy its Starlink constellation—without recognizing segment revenue, and instead capitalizing launch costs directly onto the balance sheet as “In-Orbit Satellite Assets” to be depreciated over time—the segment appears financially as low-revenue-growth with high R&D deficits.

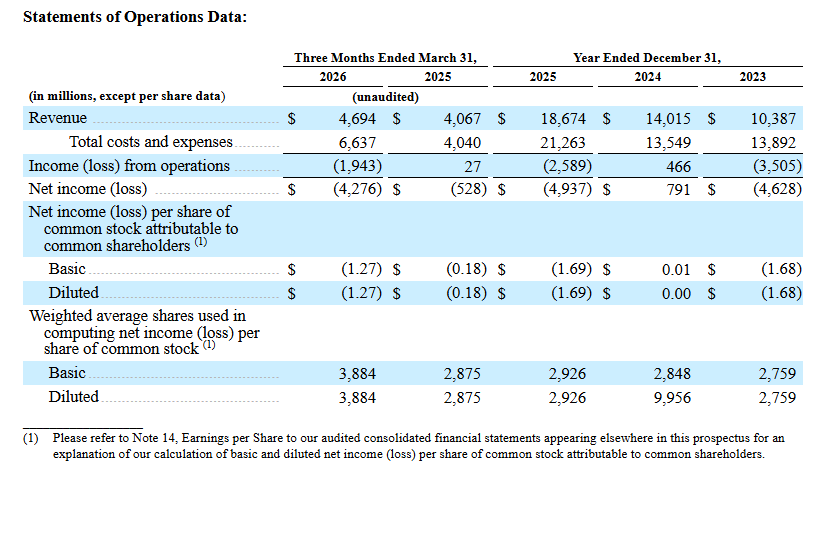

Revenue composition: Segment revenue was USD 4.086 billion in 2025, slightly up from USD 3.796 billion in 2024. Q1 revenue stood at USD 619 million. This revenue is entirely derived from NASA contracts for International Space Station cargo/crew transport, Department of Defense National Security Space Launch (NSSL) missions, and a limited number of commercial satellite customers.

Source of losses: The segment reported an operating loss of USD 657 million in 2025, primarily driven by the massive capital consumption of the Starship program. R&D expenses allocated to this segment reached USD 3.004 billion in 2025, and in Q1 2026 alone, another USD 930 million was invested over just three months.

Starlink Connectivity Segment: A Monopolistic 'Cash Cow' in Global Satellite Communications

Starlink is currently SpaceX’s healthiest and most significant cash flow engine, exhibiting the strongest increasing marginal returns:

Surge in Users and Economies of Scale: As of the end of Q1 2026, Starlink reported 10.3 million active subscribers, up 105.9% year-over-year from 5 million in the same period of the prior year.

Financial Breakout: In 2025, Starlink generated revenue of USD 11.387 billion (a 49.8% year-over-year increase), accounting for 60.9% of the group’s total revenue. Its Segment Adjusted EBITDA climbed to USD 7.168 billion, with operating profit reaching USD 4.423 billion and an operating margin of 38.8%.

Downward Pressure on ARPU: Notably, as the high-ARPU North American market approaches saturation, Starlink’s expansion into lower-purchasing-power regions such as Latin America, Asia-Pacific, and Africa has driven its average monthly revenue per user (ARPU) into a downward trend—declining from an average of USD 91 per month in 2024 to USD 81 in 2025, and further dropping to USD 66 in Q1 2026.

Significant Improvement in Terminal Manufacturing Costs: This ARPU decline has been offset by a sharp reduction in hardware costs. Through highly integrated in-house production, the average manufacturing cost of the Starlink Kit satellite antenna terminal has cumulatively decreased by 59% since 2022, with current production capacity operating at a highly efficient rate of 200,000 units per week.

Artificial Intelligence and X Platform Segment (AI): Illusory Valuation from Consolidation and Substantial Losses

This segment has almost entirely inherited the heavy asset base associated with xAI’s large-model training and X platform operations:

Revenue Stagnation: In 2025, the AI segment generated USD 3.201 billion in revenue (a modest 22.1% increase from USD 2.620 billion in 2024), primarily from advertising sales on the X platform, X Premium subscription services, and data licensing by xAI. Notably, due to a mass exodus of major advertisers from the X platform between 2024 and 2025, advertising revenue declined by USD 1.00 billion year-over-year (p. 219).

Quagmire of Compute Expenditures: Owing to substantial depreciation of on-premises data centers and high electricity costs, the segment incurred an operating loss of USD 6.355 billion in 2025. GPU hardware amortization, cloud capacity leasing, and power expenses drove R&D expenditures to USD 5.064 billion and selling, general & administrative (SG&A) expenses to USD 1.827 billion, resulting in a Segment Adjusted EBITDA loss of USD 1.237 billion.

Trillion-Dollar AI Physical Stack: The Union of Earth’s Largest Compute Cluster and Orbital Infrastructure

During its roadshow presentations, Elon Musk emphasized to institutional investors not SpaceX’s launch vehicle technology, but rather the heavy-industrial-grade “AI Physical Stack” he personally spearheaded. The prospectus provides detailed disclosures on SpaceX’s post-acquisition integration of xAI, outlining a closed-loop physical compute infrastructure combining gigawatt-scale terrestrial data centers with orbital computing capabilities.

1. COLOSSUS Terrestrial Compute Centers and Anthropic’s $10 Billion Lease Agreement

SpaceX currently owns and operates the world’s largest terrestrial AI computing infrastructure—the COLOSSUS and COLOSSUS II compute centers (located in Memphis, Tennessee, and Southaven, Mississippi, respectively).

Compute Capacity: The combined power allocation of this cluster reaches 1.0 gigawatt (GW). COLOSSUS Phase I successfully integrated 100,000 NVIDIA H100 processors into a 130-megawatt (MW) power grid within just 122 days by retrofitting an old factory facility. COLOSSUS Phase II connected 110,000 next-generation GB200 processors with 210 MW of power in only 91 days, followed by another 110,000 GB300 processors paired with 220 MW of power in just 64 days. This deployment speed represents a decisive competitive advantage compared to the industry benchmark of two years for greenfield development.

Anthropic’s $10 Billion Compute Super-Order: Disclosed under “Subsequent Events” in the prospectus is a pivotal agreement that strongly supports valuation: In May 2026, SpaceX signed a Cloud Services Agreement with generative AI unicorn Anthropic. To secure sufficient compute capacity for training its next-generation models, Anthropic agreed to pay SpaceX a fixed monthly service fee of $1.25 billion from May 2026 through May 2029—a total contract value of $45 billion—for leasing approximately 325,000 NVIDIA GPUs within the COLOSSUS II cluster. This virtually risk-free cash flow stream has effectively silenced external criticism that SpaceX’s AI segment was purely capital-intensive without revenue generation.

2. Cursor (Anysphere)’s $60 Billion Merger Option and Terafab’s Semiconductor Closed Loop

Cursor Strategic Integration: On April 19, 2026, SpaceX signed a Compute Partnership and Call Option Agreement (P289) with Anysphere, the parent company of AI coding leader Cursor. Under the agreement, SpaceX will provide GPU compute resources to jointly develop autonomous agent models for Vibe Coding; simultaneously, SpaceX obtained an exclusive right to acquire Cursor within 30 days following its IPO at a pre-agreed valuation of $60 billion, fully payable through the issuance of Class A common stock.

The ‘Terafab’ Chip Consortium: To fundamentally mitigate supply constraints on advanced GPUs, SpaceX, Tesla, and semiconductor giant Intel (which officially joined in April 2026) co-invested to establish Terafab, a joint venture for chip manufacturing. Its long-term strategic objective is to build a mega-scale, vertically integrated wafer fabrication facility encompassing photomask design, logic and memory chip wafer production, and advanced 3D packaging (leveraging Intel’s advanced packaging technologies), targeting an annual output capacity of 1 terawatt (TW) of computing hardware. It will design two primary chips: one optimized for Tesla’s Optimus robots and Full Self-Driving (FSD) edge inference, and another specifically radiation-hardened (Space-Hardened) for high-performance orbital computing in harsh cosmic radiation environments.

3. Orbital AI Computing: The Ultimate Vision Beyond Terrestrial Power Grid Constraints

The prospectus devotes considerable space to arguing that, due to the slow pace of global power grid development (with U.S. electricity generation posting a compound annual growth rate below 3% in recent years) and severe environmental and water resource constraints, the unrestricted expansion of terrestrial AI computing capacity will inevitably hit a ceiling within the next few years. SpaceX’s ultimate solution: move data centers into orbit.

Solar Power and Boundless Computing: AI satellites in space face the sun directly, unimpeded by Earth’s atmosphere, achieving solar power generation efficiency more than five times that of terrestrial solar panels. SpaceX is designing a new architecture for AI computing satellites based on its Starlink V3 satellite platform (core V3 satellite design has been completed). Each satellite will carry highly integrated computing boards, extremely large deployable solar arrays, and high-efficiency liquid-cooled radiators for thermal management, with the goal of achieving a computational power density of 100 kilowatts (kW) per metric ton of payload.

Fully Autonomous Space-Based Routing Network: SpaceX has already deployed over 23,000 space-based laser communication terminals across its satellite constellation, forming a fully closed-loop, laser-based space mesh network that operates entirely independently of terrestrial internet infrastructure. In the future, tens of thousands of AI computing satellites will use high-speed inter-satellite lasers to directly route and distribute computing tasks to end users on the ground, creating a fully proprietary, globally covered, ultra-low-latency, decentralized interplanetary computing grid.

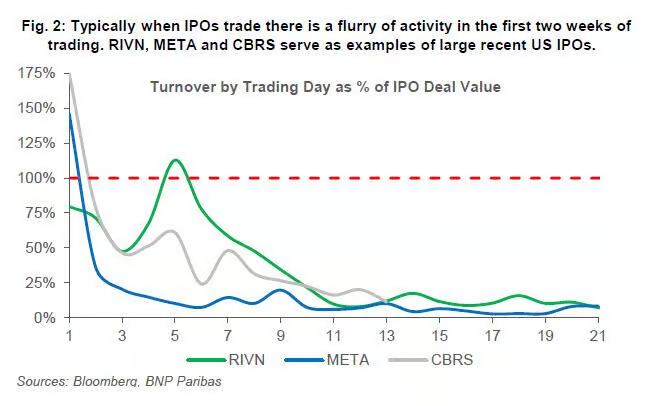

Wall Street Index Reallocation: The Clash Between Fast-Track Inclusion and Rejection Mechanisms

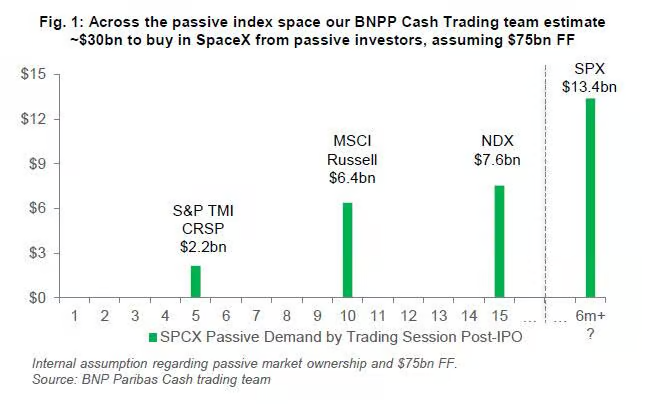

With an implied market capitalization of USD 1.78 trillion and a fundraising amount of USD 75 billion, SpaceX’s entry is akin to dropping a massive boulder into an otherwise balanced ecological pond. According to a Kickstart-themed research report by BNP Paribas, SPCX’s listing will trigger an unprecedented 'short gamma' effect on the equity ownership structure and liquidity pool of the U.S. stock market.

1. Ultra-Fast Inclusion in the Nasdaq-100 and 3x Weighting Leverage

To attract this core asset, the Nasdaq exchange has made sweeping concessions at the institutional level:

Waiver of Free-Float Threshold: For large-cap stocks, the standard requirement that freely tradable shares must constitute at least 10% of total shares outstanding has been waived (SpaceX’s offering represents only 4.2% of its total shares).

15-Day Fast Track and 3x Weighting Multiplier: SpaceX will be automatically added to the Nasdaq-100 Index just 15 trading days after listing. Additionally, when calculating its index weight, its actual free-float market capitalization of USD 75 billion will be multiplied by a factor of three—effectively treating SpaceX as having a tradable market cap of USD 225 billion for index rebalancing purposes.

First-Month Buying Surge: BNP Paribas’s cash equities desk estimates that Nasdaq-100 index funds will be forced to purchase approximately USD 8 billion worth of Class A common shares (P17) in the secondary market during the first week following inclusion.

2. Conservative Gatekeeping by the S&P 500

In contrast to Nasdaq’s ‘green light across the board,’ the S&P Dow Jones Indices—the official administrator of the S&P 500, the most central benchmark for the U.S. equity market—issued a formal announcement on June 4, 2026, explicitly rejecting any ‘fast-entry’ mechanism for large-cap IPOs.

Strict one-year seasoning requirement: The S&P indices reaffirmed that newly listed companies must trade continuously on public markets for a full 12 months (a 1-year seasoning period) and report GAAP profitability across four consecutive quarters. Consequently, given SpaceX’s current substantial accounting losses and its listing duration of less than one year, it will be entirely ineligible for inclusion in the S&P 500 until at least June 2027.

Divergent expectations among investment banks: This statement from S&P immediately prompted hedge funds—which had previously anticipated a short squeeze-driven price surge fueled by dual-index buying pressure post-IPO—to reassess their valuation premiums, significantly flattening the expected speculative volatility during SpaceX’s initial trading period.

3. Retail Investor ‘Dry Powder’ Sell-Off and ‘Short Gamma’ Risk

Retail capital reallocation: From late 2025 through early 2026, U.S. retail investors accumulated enormous unrealized paper gains during the semiconductor super bull market, concentrated primarily in individual stocks such as NVIDIA (NVIDIA), Micron Technology (MU), and SNDK, as well as in the 3x leveraged long semiconductor ETF (with assets under management exceeding USD 25 billion, representing a delta exposure equivalent to USD 75 billion in underlying assets).

Capital drainage effect: BNP Paribas simulations indicate that if retail investors collectively succumb to fear-of-missing-out (FOMO)-driven euphoria and liquidate semiconductor positions to redirect capital toward SpaceX, it would trigger cascading arbitrage-driven repricing in secondary markets. For every USD 1 billion in leveraged semiconductor fund positions retail investors unwind, underwriters and market makers would be forced to sell approximately USD 3 billion worth of underlying tech stocks to rebalance delta hedges in their options books—resulting in a broad-based ‘capital drain’ from large-cap tech equities already trading at elevated valuations.

Corporate Governance, Related-Party Transactions, and Legal Pitfalls

Beneath the spotlight of this trillion-dollar spectacle lie exceptionally complex legal controversies and corporate governance deficiencies in U.S. securities history—creating fertile ground for future short sellers and shareholder litigation attorneys.

1. Dual Conflicts of Interest Under Elon Musk’s Absolute Control

Given that Elon Musk is the sole controlling shareholder of SpaceX and simultaneously serves as CEO and the largest individual shareholder of Tesla, the scale of related-party transactions across his personal business empire has become staggering:

Major Tesla purchases: According to the “Related Party Transactions” section of the prospectus, xAI and X Platform—both under SpaceX—purchased industrial-grade Megapack energy storage batteries from Tesla valued at $506 million and $191 million in 2025 and 2024, respectively, for the construction of the Memphis computing center (P407). Additionally, in 2025, SpaceX spent $131 million purchasing Tesla-produced Cybertruck pickup vehicles for base support operations.

The Valor Equity sale-leaseback controversy: Antonio J. Gracias, a SpaceX board member and major shareholder, is also the head of private equity giant Valor Equity Partners. The prospectus revealed a significant disclosure:

Starting from the end of 2025, SpaceX (specifically through its xAI subsidiary CTC Property) entered into three substantial sale-leaseback agreements with Valor Equity for data center equipment.

Agreements I, II, and III stipulated undiscounted minimum lease payment obligations of $6.986 billion, $6.633 billion, and $6.587 billion, respectively (totaling over $20 billion) (P408–P409).

Given Gracias’s position on SpaceX’s board and his substantive involvement in pricing decisions, these transactions have been classified by SpaceX’s internal audit as “material related-party transactions.” Moreover, because the lease terms heavily favor the lessor, they were not recognized as genuine “asset sales” for accounting purposes but instead recorded as “failed sale-leaseback debt.” At the end of 2025, the company’s balance sheet reflected an increase of $4.052 billion in long-term liabilities due to this transaction; in the first quarter of 2026, following the execution of Transaction II, this liability surged further by $5.365 billion.

2. Elon Musk’s personal exposure to massive pending litigation and associated provisions

In Note F of the financial statements accompanying the prospectus, SpaceX made substantial legal expense provisions related to a portfolio of significant lawsuits it faces:

Litigation loss provisions: As of December 31, 2025, the company had accrued an estimated litigation loss provision of $530 million (P611). Due to reassessments or developments in certain unresolved disputes during the first quarter, this provision was adjusted downward to $399 million as of March 31, 2026.

Primary sources of litigation disputes:

SDBN and SOMI European GDPR Class Actions: Two Dutch advocacy funds have filed a class action lawsuit in the Amsterdam District Court on behalf of over 11 million European users against platform X, alleging serious violations of the EU’s General Data Protection Regulation (GDPR) concerning MoPub ad exchanges and backend data collection practices. The combined claims seek damages potentially amounting to several billion euros. The Amsterdam District Court has scheduled critical hearings from April 2, 2026, to May 27, 2026.

Copyright and Right of Publicity Litigation Over Grok’s Unauthorized Image Generation: Since January 2026, xAI has faced two major class action lawsuits in California (Jane Doe 1 Case, filed March 16, 2026) stemming from widespread user abuse of Grok’s newly launched “Unhinged” image generation mode, which was used to create explicit synthetic images of celebrities. Plaintiffs allege that xAI knowingly facilitated and participated in these infringements and demand disgorgement of illicit profits along with substantial punitive damages.

NAACP Environmental Lawsuit: On April 14, 2026, the National Association for the Advancement of Colored People (NAACP) filed suit in Mississippi federal court, accusing the COLOSSUS II computing center of illegally operating large-scale natural gas turbine generators without completing a full environmental review, thereby allegedly violating the Clean Air Act. The plaintiffs are seeking a preliminary injunction ordering the immediate shutdown—“power-off and halt operations”—of the facility. If granted, such an injunction would deal a devastating blow to COLOSSUS’s model training capabilities.

Cash on Hand and Mandatory Debt Repayment: Allocation of IPO Proceeds

As a capital-intensive heavy industrial and computational behemoth with voracious cash consumption, SpaceX maintains exceptionally robust liquidity reserves on its balance sheet, yet it also carries staggering leverage pressures:

Cash Reserves: As of March 31, 2026, the company held USD 15.852 billion in unrestricted cash and cash equivalents and USD 7.823 billion in short-term marketable securities, resulting in total liquid assets exceeding USD 23.6 billion.

USD 20 billion bridge loan with mandatory IPO repayment obligation: In March 2026, to settle the high-interest syndicated debt incurred from the merger with xAI, SpaceX entered into an unsecured bridge loan agreement for up to USD 20.00 billion with a banking consortium led by Goldman Sachs (the SpaceX Bridge Loan, bearing an annual interest rate of 4.58%, p.164).

Under the hard mandatory repayment provision of this bridge loan, SpaceX is required to allocate all net proceeds from this IPO toward full repayment of the bridge loan principal and interest within six months of closing the offering. This indicates that, although the fundraising amount ranges from USD 75 billion to USD 85 billion, at least USD 20 billion will be directly used to repay the bank bridge facility and will not be available as free operating capital thereafter.

Conclusion

SpaceX’s trillion-dollar IPO represents the most ambitious capital spectacle in modern global financial history. It forcefully redirects investor attention away from purely virtual algorithms and cloud-based models toward an era of 'heavy-industrial mega-computing'—defined by Starship spacecraft, rocket launch towers, ultra-large-scale energy storage batteries, space-based laser routers, and nuclear power generators.

Admittedly, the low-Earth-orbit Starlink constellation has already demonstrated extraordinary monopolistic cash-generating capacity, and Elon Musk’s strategic alliance with industry giants such as Anthropic paints a grand commercial vision. Yet behind the dazzling fireworks of a trillion-dollar valuation lie jaw-dropping burn rates, an extremely concentrated corporate governance structure, and treacherous legal undercurrents rife with massive related-party transactions and pending litigation. Following this historic IPO listing, whether Musk can fully unlock the dimension of space-based AI computing before terrestrial computational resources run dry will be put to the ultimate test—with Wall Street placing trillions of dollars of real money on the line.

Source:Official Documents

Editor/joryn