① Tonight, newly appointed Federal Reserve Chair Kevin Warsh will, for the first time in his role as the Fed’s “helmsman,” review the U.S. labor market’s latest monthly “exam” results; ② whether the nonfarm payroll data will satisfy Warsh—and how it might influence the Fed’s interest rate trajectory entering the “Warsh era”—remains an open question awaiting resolution…

For an extended period, the U.S. labor market has exhibited a pattern of “fewer hires and fewer layoffs.” Following the Trump administration’s tightening of immigration policies, weak labor demand has been offset by a steadily shrinking labor supply.

However, recent data suggest this delicate balance may be shifting positively—some employment indicators are showing early signs of recovery, and there is little evidence so far of an AI-driven “employment apocalypse,” at least not yet.

Against this backdrop, Friday’s upcoming U.S. May nonfarm payrolls report has become a focal point. The report is expected to show a net gain of 85,000 nonfarm jobs in May, with the unemployment rate holding steady at 4.3%. Compared to labor market conditions at the end of last year, this would represent a solid outcome.

Against this backdrop, Friday’s upcoming U.S. May nonfarm payrolls report has become a focal point. The report is expected to show a net gain of 85,000 nonfarm jobs in May, with the unemployment rate holding steady at 4.3%. Compared to labor market conditions at the end of last year, this would represent a solid outcome.

In the first four months of this year, the U.S. added an average of 76,000 jobs per month. While modest by historical standards, this marks a significant improvement compared to last year’s average monthly gain of fewer than 10,000 nonfarm jobs.

And tonight, newly appointed Federal Reserve Chair Kevin Warsh will, for the first time as the Fed’s “helmsman,” review this monthly “exam” report card from the U.S. labor market. Whether the data meet Warsh’s expectations—and how they might shape the Fed’s interest rate path in the emerging “Warsh era”—remains a suspenseful question awaiting resolution…

How does Wall Street view tonight’s nonfarm payroll expectations?

Currently, industry media surveys of institutional economists project that U.S. nonfarm payrolls will increase by 85,000 in May, down from the prior reading of 115,000. Forecasts from investment banks range from a high of 125,000 (Jefferies) to a low of 45,000 (Freedom Finance).

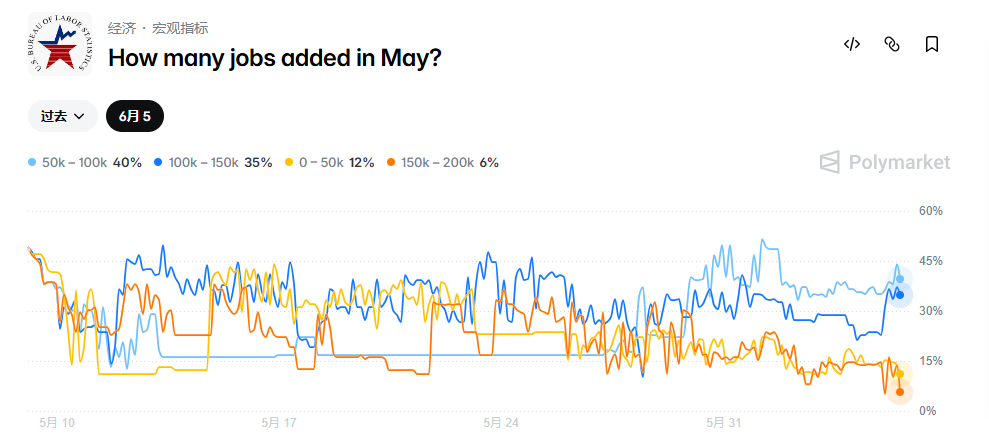

In recent years, with the rise of prediction markets, placing bets on nonfarm payroll outcomes has become a “new pastime” for some market participants. According to Polymarket data, investors in this market estimate the most likely range for tonight’s nonfarm payrolls to be 50,000–100,000 (with a 40% probability), followed by 100,000–150,000 (35% probability).

Regarding other sub-components, industry surveys expect the unemployment rate in May to remain unchanged at 4.3%. The Federal Reserve’s March economic projections had forecast the unemployment rate to rise to 4.4% this year; however, at least for May, rounding suggests the rate may not yet show an increase.

The Chicago Fed's Leading Labor Market Indicator forecasts the unemployment rate at 4.32% in May, down from 4.34% in April, reflecting a slight decline in layoffs and other separations.

Average hourly earnings in May are expected to rise by 0.3% month-over-month (up from 0.2% previously), though the annual rate is projected to slow to 3.4% year-over-year (down from 3.6%).

Of course, according to some Wall Street institutions, one risk to watch for in tonight’s nonfarm payroll data is that, given the labor market was in a state of flux around this time last year, there could be some catch-up declines this month, and overall employment figures may face modest downside risks relative to expectations.

Laura Ullrich, Director of Economic Research at the Indeed Hiring Lab, stated, 'We continue to hear and observe a “low-hiring, low-firing” sentiment—meaning if you have a job, it seems reasonably secure right now. People are continuing this trend of holding tightly onto their jobs. However, if you’re looking for work, it’s an extremely difficult period because hiring volumes are so low. From a macro perspective, we’ll see stagnation, because if people aren’t leaving their positions and businesses aren’t creating new ones, it’s simply a highly stagnant market.'

Among specific investment banks, Goldman Sachs expects only 60,000 nonfarm payroll jobs to be added in May, noting that its 'big-data indicators tracking employment growth' slowed during the month. Adam Schickling, Chief Economist at Vanguard Group, forecasts a mere 20,000 increase in nonfarm payrolls, 'as the unusually warm and dry weather earlier this year likely boosted January–April employment figures beyond normal levels, leading to partial reversal this month.'

Similarly, EY-Parthenon expects nonfarm payrolls to rise by 50,000 in May. According to most current estimates, this gain would be sufficient to keep the unemployment rate broadly unchanged from current levels, albeit with a slight upward bias.

'This phase of employment moderation reflects some unwinding of prior weather-related strength and an ongoing cautious hiring environment,' said Gregory Daco, Chief Economist at EY-Parthenon, in a report. 'We expect the unemployment rate to tick up slightly to 4.4%, consistent with a labor market where both demand and supply are slowing in tandem.'

May Nonfarm Payroll Preview Indicators: Generally Positive but Lingering Concerns Remain

Looking at a series of leading indicators ahead of the nonfarm payroll release, recent U.S. labor market data has been largely encouraging, though some underlying concerns persist.

Undoubtedly, the most impressive U.S. economic indicator released so far this week was the April JOLTS job openings figure published by the Bureau of Labor Statistics—surging by 731,000 to reach 7.618 million, far exceeding the upwardly revised prior level of 6.887 million and marking an increase of 520,000 compared to a year ago. This marks the first time since last June that U.S. job openings have outnumbered unemployed individuals.

This figure exceeded market expectations by a full nine sigma, marking the largest forecast deviation on record. Of course, it is somewhat unfortunate that, as this report reflects conditions in April, it offersnon-farm payroll datalittle reference value for predicting the May data to be released this Friday.

On Wednesday, the closely watched ADP National Employment Report—often dubbed the 'little NFP'—showed that private-sector payrolls added 122,000 jobs last month, the strongest gain since January of last year. The education and health services sector led with 57,000 new positions, followed by trade, transportation, and utilities, which added 36,000 jobs.

However, it should be noted that ADP data excludes government employment, and thus has consistently outperformed the official nonfarm payrolls report since Trump returned to the White House. Nevertheless, these signals remain positive overall.

Initial jobless claims during the reference week for the May nonfarm payrolls report showed little change compared to April levels, averaging 210,000 (versus 215,000 in April), while continuing claims further declined between survey weeks.

Among a range of indicators, the only notably negative signal for the U.S. labor market in May came from Challenger, Gray & Christmas, an employment placement firm. Its report released Thursday showed that U.S. employers announced 97,006 job cuts in May, up 16% from April and the highest level for May since the early days of the pandemic in 2020.

Notably, the U.S. tech sector announced its largest layoff plans in nearly two years in May. Moreover, artificial intelligence (AI) was cited as the primary reason for corporate layoffs for the third consecutive month, with AI-related job cuts announced in May totaling 38,579 positions. Consequently, some industry insiders continue to express concern that the current U.S. labor market dynamic—characterized by low hiring and low layoffs—could deteriorate into a vicious cycle of zero hiring and widespread layoffs. These concerns include the ongoing global energy crisis, fears of an AI bubble, and the uncertain impact of this emerging technology on employment.

How will tonight’s nonfarm payrolls data affect financial markets?

From a policy perspective, any outcome close to the market consensus would almost certainly imply that the Federal Reserve will hold rates steady. Market pricing indicates that the probability of the Fed taking any rate action at itsFederal Open Market CommitteeFederal Open Market Committee (FOMC) meeting on June 16–17 is virtually zero.

That said, the strength or weakness of the data could still influence market expectations regarding the Fed’s rate path toward year-end.

According to JPMorgan’s Market Intelligence division, the importance of Friday’s nonfarm payrolls data has diminished somewhat due to uncertainties surrounding Middle East conflicts—a factor also reflected in lower-than-expected volatility, which in turn affects scenario outcomes. Nevertheless, as JPMorgan’s Andrew Tyler notes, excessively weak data would reignite stagflation concerns, which would be negative for risk assets. Conversely, overly strong data would prompt equities to react to higher bond yields, as inflation worries push yields and bond volatility upward—also unfavorable for equities. In other words, regardless of the outcome, the market reaction may ultimately be negative.

Of course, it is also possible that the data turns out strong while the unemployment rate shows no material change—in which case, equity markets would likely respond positively to the favorable growth outlook. Looking at the broader picture, JPMorgan still believes the economy is on a positive and improving trajectory, and if the Middle East conflict were to end today, the resulting tailwind for consumer sentiment would propel equity markets to new highs. Of course, this is a rather significant assumption, as an Iran war certainly will not end today—and it remains uncertain whether it could even conclude within the next few months.

Below is JPMorgan’s scenario analysis regardingnonfarm payrolls:

May nonfarm payrolls above 130,000: S&P 500 down 1% to up 0.5%; probability 5%

May nonfarm payrolls between 100,000 and 130,000: S&P 500 down 0.25% to up 0.75%; probability 25%

May nonfarm payrolls between 70,000 and 100,000: S&P 500 up 0.5% to 1%; probability 40%

May nonfarm payrolls between 40,000 and 70,000: S&P 500 down 0.75% to flat; probability 25%

May nonfarm payrolls below 40,000: S&P 500 down 1% to 1.5%; probability 5%

Daco of EY-Parthenon stated, 'For the Federal Reserve, a resilient labor market combined with persistently elevated inflation increases the likelihood of a more hawkish, two-sided policy statement at the next FOMC meeting. Officials may emphasize that if inflation proves more persistent, interest rate hikes remain an option.'

Stay ahead on major financial events and discover investment opportunities early! Open Futubull > Market > US Stocks >Financial Calendar/selected macroeconomic data, seize the investment opportunity!

Stay ahead on major financial events and discover investment opportunities early! Open Futubull > Market > US Stocks >Financial Calendar/selected macroeconomic data, seize the investment opportunity!

Editor/Joe