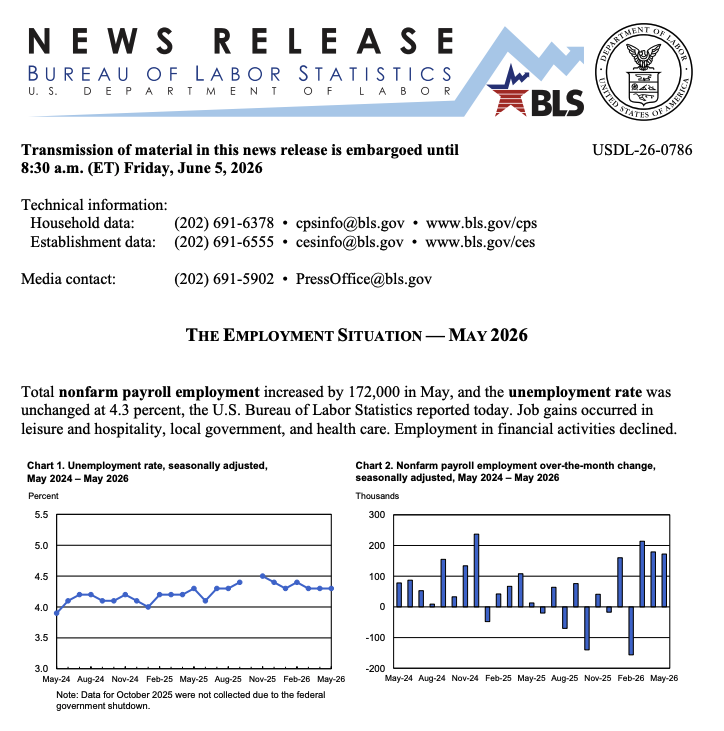

① U.S. nonfarm payrolls rose by 172,000 in May, far exceeding market expectations of 85,000, with upward revisions of a combined 93,000 for the prior two months, driving the strongest three-month employment gain in over two years; ② The robust labor data has fully dispelled market hopes for a rate cut this year, with markets now fully pricing in a 25-basis-point rate hike by the Federal Reserve by year-end, triggering a surge in U.S. Treasury yields, a drop in gold prices of over $50, and downward pressure on technology stocks.

Caixin News, June 5 (Editor: Shi Zhengchen) – On Friday evening Beijing time, the U.S. Bureau of Labor Statistics released May’s nonfarm payroll report, which vastly exceeded pre-release forecasts.

The report showed that nonfarm payrolls increased by a net 172,000 in May, significantly surpassing analysts’ consensus forecast of an 85,000 increase; the unemployment rate remained unchanged at 4.3%, in line with expectations.

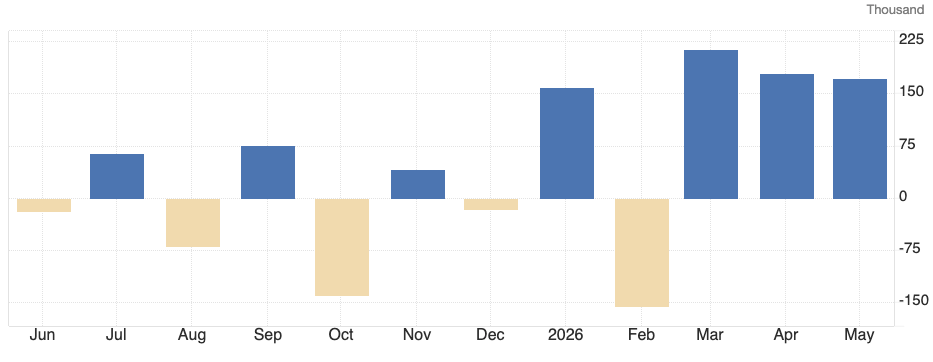

The latest report also substantially revised upward employment figures for the prior two months: March payrolls were revised up from an increase of 185,000 to 214,000, and April’s from 115,000 to 179,000, amounting to a combined upward revision of 93,000. Together with May’s data, this marks the strongest three-month employment gain in over two years.

The latest report also substantially revised upward employment figures for the prior two months: March payrolls were revised up from an increase of 185,000 to 214,000, and April’s from 115,000 to 179,000, amounting to a combined upward revision of 93,000. Together with May’s data, this marks the strongest three-month employment gain in over two years.

(U.S. employment data over the past three months has been exceptionally strong; source: tradingeconomics)

In pre-release economist surveys, the highest forecast for May nonfarm payrolls was only 125,000. The actual figure far surpassed even this upper-bound estimate—excluding the additional 93,000 upward revision to the prior two months’ data. In other words, economists studying the U.S. economy have underestimated the pace of job growth for three consecutive months.

The report indicated that May’s employment gains were concentrated in leisure and hospitality, local government, and healthcare sectors.

Leisure and hospitality added 70,000 jobs, far above its 12-month average monthly gain of 14,000. Local government employment rose by 55,000 in May, while the healthcare sector added 35,000 positions.

Meanwhile, financial sector employment declined by 22,000 in May, bringing the total reduction since the recent peak in May 2025 to 107,000. Additionally, the report highlighted the ongoing impact of artificial intelligence on hiring: employment in the information sector—including software publishers and social media companies—declined again in May, marking the 16th drop in the past 17 months.

The nonfarm payroll report also showed that 'wage growth continues to lag behind inflation,' with average hourly earnings rising 0.3% month-over-month and 3.4% year-over-year. By comparison, the Consumer Price Index (CPI) rose 3.8% year-over-year in April; the May CPI figure will be released next week.

Persistently stronger-than-expected U.S. employment data also means that newly appointed Federal Reserve Chair Kevin Warsh now faces the decision of when to raise interest rates, with rate cuts no longer on the policy table for this year.

Following the release of the nonfarm payrolls report, data from the interest rate swaps market shows traders have fully priced in a 25-basis-point Fed rate hike by year-end, and the probability of a hike as early as October has risen to nearly 60%.

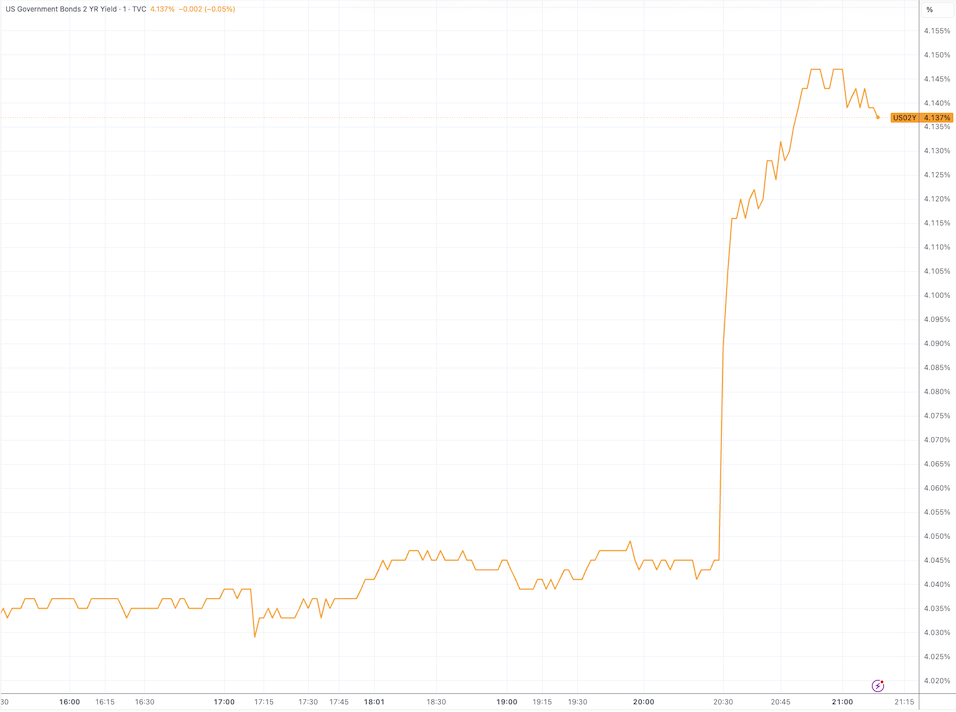

As of this writing, yields across all maturities of U.S. Treasury securities have risen sharply. The two-year Treasury yield increased by 9 basis points to 4.13%, while the 10-year Treasury yield rose by 6 basis points to 4.53%.

(Minute-by-minute chart of U.S. two-year Treasury yield, source: TradingView)

Spot gold plunged more than $50 in a short period, with its latest quote hovering around $4,420 per ounce. Spot silver’s intraday loss widened to 3%. U.S. stock index futures extended their declines slightly, with the recently strong technology sector showing intensified weakness.

Following the data release, Christopher Hodge, Chief U.S. Economist at Natixis, stated: “If it wasn’t already clear before, it certainly is now: the dovish tilt evident in the Fed’s May statement will be formally removed in June, and the dot plot projections suggesting rate cuts this year will dwindle to almost none—or possibly disappear entirely.”

According to the schedule, Kevin Warsh will chair his first policy meeting on June 16–17. Markets widely expect the Fed to hold the benchmark interest rate steady at this meeting, but attention has now shifted to how Warsh will balance prevailing expectations for rate hikes against sentiment from the White House.

Editor/Rocky