The well-known financial blog QTR's Fringe Finance warned in a post: Do not treat this downturn as yet another opportunity to buy the dip. Current valuation levels, the Federal Reserve’s predicament, and the fragility of market structure are fundamentally different from the 'every dip gets rescued' environment that investors have grown accustomed to over the past 15 years.

U.S. stocks faced heavy selling pressure on Friday, with the Nasdaq index dropping approximately 3.3% by midday.$Bitcoin (BTC.CC)$It simultaneously plunged to around $60,000—down roughly 16% over the past five trading days and about 42% over the last 12 months. Those who had been insisting for months that 'valuation doesn’t matter' suddenly started asking what was going on.

The well-known financial blog QTR's Fringe Finance warned in a post: Do not treat this downturn as yet another opportunity to buy the dip. Current valuation levels, the Federal Reserve’s predicament, and the fragility of market structure are fundamentally different from the 'every dip gets rescued' environment that investors have grown accustomed to over the past 15 years.

A 3% decline is still far from 'cheap.'

The article provides a basic benchmark: in 2023—just three years ago—the Nasdaq stood more than 59% below its current level.

The article provides a basic benchmark: in 2023—just three years ago—the Nasdaq stood more than 59% below its current level.

Valuation metrics are even more troubling. The current Shiller Cyclically Adjusted Price-to-Earnings (CAPE) ratio stands at 42.7x, compared with a historical mean of just 17.38x and a median of 16.09x—more than double the century-long average and approaching the all-time high of 44.19x recorded in December 1999 at the peak of the dot-com bubble. He cautioned, 'That era was not known for rational pricing or strong forward returns.'

The Buffett Indicator is equally unsettling. U.S. equity market capitalization currently stands at approximately $75.4 trillion against an annualized GDP of about $31.8 trillion, yielding an indicator reading of 237%. Historically, whenever this metric has reached such extreme levels, investors have ultimately discovered—sometimes painfully—that valuation does matter.

A 3% drop may appear severe on social media, but against the backdrop of historically extreme valuations, it barely amounts to a scratch.

What makes this time different?

Over the past 15 years, every meaningful market downturn has been accompanied by an expectation that the Federal Reserve would eventually step in with rate cuts, liquidity injections, or some form of monetary 'painkiller.' Today, that safety net has grown much thinner.

The article notes that the Federal Reserve is caught in a dilemma: inflation remains stubbornly elevated, so aggressive rate cuts risk reigniting inflationary pressures, while maintaining a tight stance could further weigh on the economy. 'The market may be urgently seeking a rescue, but inflation may not allow it.' This is a scenario investors haven’t faced in a long time.

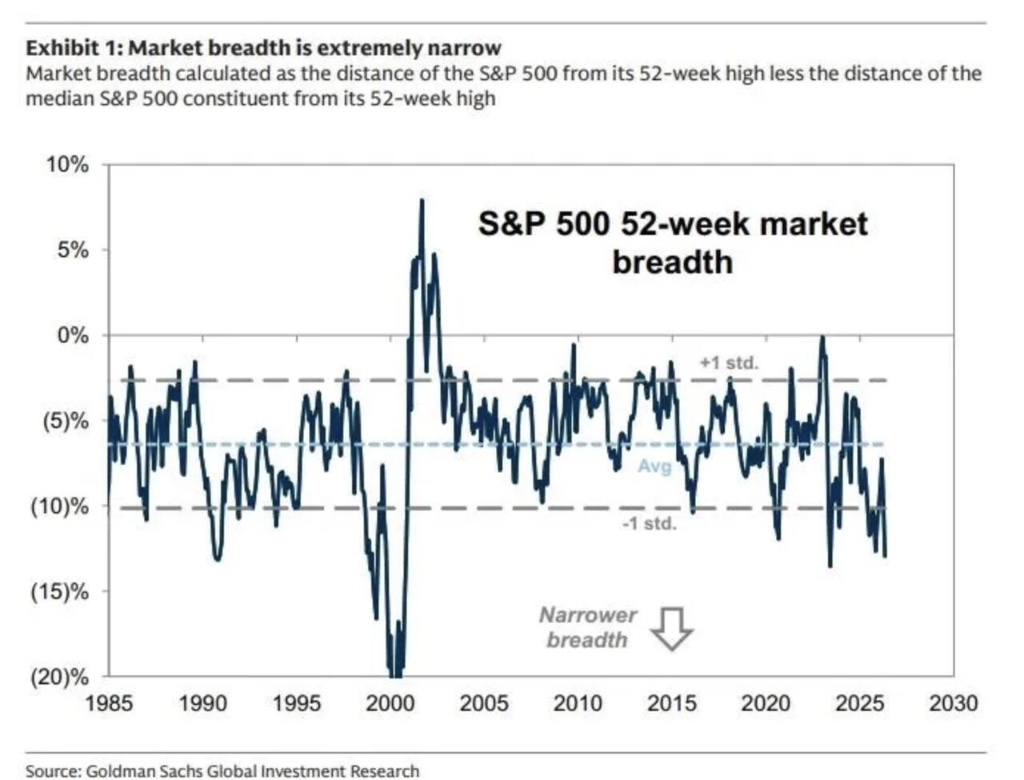

Structural vulnerabilities in this market cycle are also intensifying. Beneath the surface of headline index levels, market breadth is far less healthy than bulls would like to admit—with a small number of stocks shouldering a disproportionate share of gains. QTR previously recommended that investors holding the S&P 500 ETF (SPY) also monitor the equal-weight ETF (RSP) to obtain a more accurate gauge of overall market conditions.

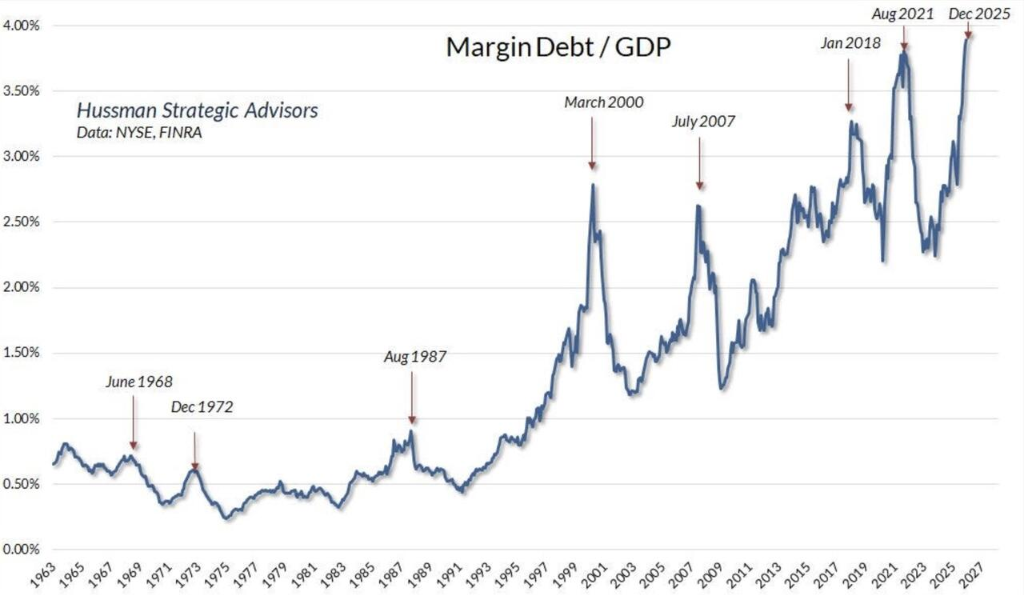

Leverage and margin debt have expanded system-wide, with options-driven cash flows becoming a key source of market support. Market makers’ gamma effect suppresses volatility during rallies, creating an illusion of stability—but the same mechanism can operate in reverse: as positions begin to unwind, liquidity evaporates rapidly, leverage is pared back, and momentum traders rush for the exits, turning 'a steady stair-step climb into an elevator-like plunge.'

QTR has long viewed Bitcoin as the 'tip of the risk-appetite spear'—the first asset to surge when liquidity is abundant and speculation runs high, and the first to crack when risk appetite fades. In October last year, he listed cryptocurrencies among the ten market sectors warranting heightened vigilance and advised investors to closely monitor the other nine: 'Markets rarely confine problems indefinitely to one corner of the casino.'

The article concludes by emphasizing that this does not imply a crash is imminent. However, given valuations approaching historical extremes, a Federal Reserve constrained by inflation, and a fragile market structure, one should not assume every dip is a 'gift.' That mindset worked well in an era of lower valuations, ample liquidity, and a Fed ready to intervene—but those conditions no longer exist today.

The author warns that, at current leverage levels, it would take little catalyst to trigger a leveraged sell-off capable of redefining investors’ perception of what constitutes a 'sharp decline.'

Editor/Rocky