The Strait of Hormuz has been blockaded for over three months, cutting off more than 10 million barrels per day of Middle Eastern crude oil supply and causing the most severe oil supply shock in modern history.

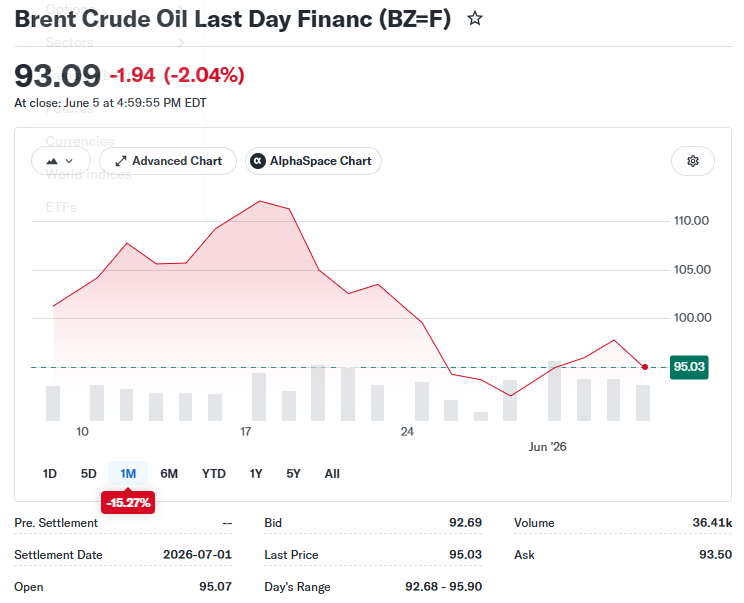

The Strait of Hormuz has been blockaded for over three months, cutting off more than 10 million barrels per day of Middle Eastern crude oil supply and causing the most severe oil supply shock in modern history. However, Brent crude has fallen from its record high above $140 at the onset of the Iran conflict to below $100, and the industry's earlier pessimistic forecast of $200 has not materialized.

"People thought it would be much worse," U.S. President Trump said on Friday. "Today I saw $96 a barrel—people thought it would hit $300."

The Iran conflict has now lasted nearly 100 days. On the 5th, Trump declared that Iran’s military capabilities had been 'completely destroyed.' The very next day, U.S. forces conducted another round of airstrikes on parts of Iran, prompting Tehran to retaliate with missile strikes on U.S. Air Force bases in Kuwait and facilities of the U.S. Fifth Fleet in Bahrain.

The Iran conflict has now lasted nearly 100 days. On the 5th, Trump declared that Iran’s military capabilities had been 'completely destroyed.' The very next day, U.S. forces conducted another round of airstrikes on parts of Iran, prompting Tehran to retaliate with missile strikes on U.S. Air Force bases in Kuwait and facilities of the U.S. Fifth Fleet in Bahrain.

Amid alternating periods of fighting and negotiations, a series of emergency measures are enabling the global oil market to absorb this supply shock with greater resilience than expected.

Maria Angelicoussis, CEO of Angelicoussis Group—the world’s largest Greek shipowner—stated:

"After more than three months of conflict, the world has demonstrated unexpected resilience. Commodity prices have risen by 50% to 60%, and Asian LNG prices have surged by 90%, yet they have not reached the astronomical levels that at least I personally anticipated."

Three forces have kept oil prices in check

From the demand side, China—the world’s largest crude oil importer—saw its May crude imports plunge by nearly 40% compared to last year’s average (according to Vortexa), a decline sufficient to offset one-third to one-fifth of the supply lost due to the conflict. Underlying factors include China halting its recent strategic petroleum reserve build-up, coal-to-chemicals capacity substituting part of petrochemical output, and surging electric vehicle sales suppressing gasoline consumption.

According to estimates from Kpler and Energy Aspects, Chinese refinery runs in May–June dropped to approximately 13 million barrels per day—the last time throughput was this low was in early 2020, compared with an average of 14.8 million barrels per day last year.

$ING Groep (ING.US)$Warren Patterson, Head of Commodities Strategy, stated, "China’s significant pullback from the crude oil market has played a pivotal role in global market rebalancing, helping to cap oil prices."

While demand-side contraction occurred, supply also demonstrated unexpected resilience—primarily driven by the United States.

Thanks to the shale oil revolution launched over a decade ago, the U.S. has become a net exporter of crude oil and refined products. This abundant domestic energy supply underpins Trump’s confidence in confronting Iran militarily. Since the conflict began in late February, the U.S. has further solidified its role as the world’s most critical swing supplier, with crude and fuel exports in May exceeding the prior-year average by more than 2 million barrels per day.

The Trump administration pledged to release 172 million barrels from the Strategic Petroleum Reserve (SPR), executing the drawdown faster than anticipated—releasing as much as 1.4 million barrels per day in a single week last month, nearly half of which was shipped to Europe and other overseas destinations.

Washington played another card: granting partial sanctions waivers on Russian crude, making it easier for India to ramp up purchases. In May, Russia’s average crude exports to India—the world’s third-largest crude importer—reached 1.76 million barrels per day, a 63% increase compared to February.

Alternative export routes provided additional cushioning. Saudi Arabia transported crude via its East-West pipeline to the Red Sea, while the UAE moved crude through pipelines to Fujairah Port outside the Persian Gulf. Governments also coordinated a historic joint release of strategic reserves, and pre-existing supply surpluses in the market absorbed part of the shock.

Although commercial vessel traffic through the Strait plummeted from nearly 100 ships per day before the conflict to just two or three, a limited number of vessels continue to transit—either through intergovernmental arrangements or increasingly covert methods. According to an official familiar with U.S. Central Command operations, nearly 1,000 commercial vessels have entered or exited the Strait over the past two months.

Buffers are being depleted

These emergency measures have stabilized oil prices, but the buffers themselves are being exhausted.

Global oil inventories are declining at a record pace. Greg Sharenow, head of commodities portfolio management at Pacific Investment Management Company (PIMCO), who oversees nearly $24 billion in assets, issued a blunt warning: "Every week, the system tightens by 70 to 80 million barrels. This cannot go on indefinitely. Within the next few months—at the latest—you’ll face a system that may have lost its elasticity because buffers have been severely depleted."

Domestic conditions in the United States are equally tight. Last week, total U.S. crude oil inventories fell to their lowest level in over two decades, with stocks at the key storage hub of Cushing approaching operational minimums. Strategic reserves are nearly depleted, and fuel inventories are at critically low levels just as summer driving season approaches. Domestic refiners are running at maximum capacity to meet demand, competing with exports for crude supply and pushing up the premium of U.S. crude over Middle Eastern grades in Asia.

"We don’t have the capacity to sustain export levels like this," said Sharenow.

Will prices soar from here?

Trump’s persistent calls for peace talks have somewhat capped oil prices. Brent crude futures open interest has dropped to its lowest level since last August, as heightened market volatility has forced traders to reduce risk exposure. Expectations of a peaceful resolution—and the resulting price plunge—have driven many long-position holders out of the market, leaving only those willing to trade small positions over short time horizons.

However, the prospects for peace talks remain uncertain. Pavel Molchanov, an analyst at Raymond James, noted that the 'minimum threshold' for restoring shipping through the Strait would be at least 20 vessels transiting per day for a full consecutive week—'which is unrealistic before a durable U.S.-Iran reconciliation is reached, and that timeline keeps getting pushed back.'

An article in TIME magazine highlighted an uncomfortable reality: even if negotiations succeed, the best possible outcome would merely be the re-opening of the Strait—which had been unimpeded before the conflict—alongside a nuclear deal no more comprehensive than the 2015 Iran nuclear agreement. After a hundred days of fighting, the most optimistic scenario is simply returning to square one.

Most traders view the timing of China’s return to pre-conflict levels of Iranian crude imports as a key variable for oil price direction. Yet even if answers emerge for all these issues, the market still faces an unavoidable supply gap.

Tom Baker, head of Vitol’s Bahrain-based unit at the world’s largest independent oil trader, said at a conference this week:

"Virtually everyone expects a solution to be just around the corner. But no matter how quickly production capacity recovers, you still face a gap—call it what you will—of 1 billion barrels of oil that have already vanished."

Global spare supply is rapidly diminishing. According to Sharenow, this buffer could be exhausted within the next few months—at which point even a relatively minor supply disruption would be sufficient to trigger a sharp price spike.

Editor/Rocky