① Many investors are attempting to position themselves ahead of the Federal Reserve’s June 17 decision—the first FOMC meeting under Chair Kevin Warsh—in anticipation of a potential hawkish pivot by the Fed;

② The U.S. Consumer Price Index (CPI) for May, scheduled for release on Wednesday, is likely to serve as the next major catalyst.

After a nervous weekend following 'Black Friday,' Wall Street traders are now concerned that the latest inflation data to be released this Wednesday could show the largest year-over-year increase in U.S. CPI in several years, further intensifying pressure on the Federal Reserve to raise interest rates.

On Friday, unexpectedly robust U.S. nonfarm payroll data pushed yields higher and reinforced market expectations that the Federal Reserve will hike rates by December. The data showed that U.S. nonfarm payrolls rose by 172,000 in May—nearly double the market forecast of 85,000—and the unemployment rate remained steady at a low 4.3%.

On Friday, unexpectedly robust U.S. nonfarm payroll data pushed yields higher and reinforced market expectations that the Federal Reserve will hike rates by December. The data showed that U.S. nonfarm payrolls rose by 172,000 in May—nearly double the market forecast of 85,000—and the unemployment rate remained steady at a low 4.3%.

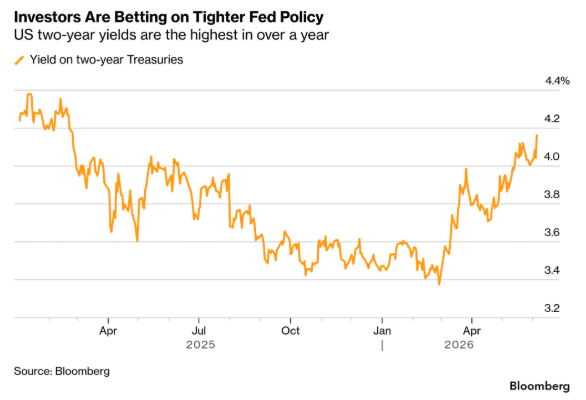

Following the release of the data, the yield on the 10-year U.S. Treasury note—often dubbed the 'anchor of global asset pricing'—surged to 4.55% on Friday, marking a two-week high. The yield on the two-year Treasury note, which is especially sensitive to Federal Reserve policy expectations, reached 4.18%, its highest level since February 2025.

Meanwhile, the tech-heavy Nasdaq Composite Index suffered its largest single-day point decline in history during Friday’s 'Black Friday' sell-off, plunging more than 1,121 points—or 4.2%—marking its steepest one-day percentage drop in over a year.

Currently, many investors are attempting to position themselves ahead of a potential hawkish shift by the Federal Reserve before its policy decision on June 17—the first FOMC meeting under Chair Kevin Warsh. The U.S. Consumer Price Index (CPI) for May, due for release on Wednesday, is likely to serve as the next major catalyst.

Interest rate swaps linked to the report indicate traders expect the year-over-year CPI increase in May to reach approximately 4.3%—the highest level since 2023—as energy prices remain elevated amid the ongoing stalemate in the Iran conflict.

Luigi Buttiglione, CEO of consulting firm LB Macro, stated that the narrative suggesting the Fed would need to cut rates has 'disappeared, killed by the data.' He forecasts the Fed will hike rates by 50 basis points this year, likely beginning in September.

Since late February, global bond markets have undergone a profound shift. At that time, U.S. and Israeli strikes on Iran triggered a spike in oil prices, disrupting market expectations that the Federal Reserve would cut rates in 2026.

With the conflict now in its hundredth day and a durable ceasefire still appearing out of reach, energy prices could rise further and amplify inflation concerns. A resilient U.S. economy is adding headwinds for bond markets and complicating Warsh’s position—he may face pressure from the White House to lower borrowing costs.

‘If Kevin Warsh had originally hoped to cut rates immediately upon taking office, that now appears impossible,’ said Christophe Boucher, Chief Investment Officer at ABN AMRO Investment Solutions. ‘The current labor market is too strong to justify a rate cut.’

Market participants noted that if either Wednesday’s CPI data or Thursday’s PPI figures show any signs of further acceleration in inflation, it could further solidify market expectations that Federal Reserve officials will remove the so-called ‘dovish bias’ from their policy statement.

Over the past weekend, major Wall Street investment banks have already withdrawn their forecasts for rate cuts in 2026.

Last Friday, economists at BNP Paribas predicted the Federal Reserve would hike rates three times starting in December.

David Mericle, Goldman Sachs’ chief U.S. economist, has also completely abandoned his expectation of Fed rate cuts this year, pushing back the timing of the two previously anticipated cuts significantly to June and December 2027.

Goldman Sachs noted that the longer the pause in rate changes lasts, the more it may reinforce the view that current rates are ‘appropriately set.’ Moreover, strong investment demand related to artificial intelligence could provide additional justification for maintaining higher borrowing costs. Therefore, Goldman Sachs stated that holding rates steady remains ‘a viable alternative scenario’ outside its baseline forecast.

Although Goldman Sachs still considers the likelihood of renewed rate hikes limited, it has raised the probability from 10% to 20%. The firm also revised down its forecast for the U.S. unemployment rate this year from 4.6% to 4.4%.

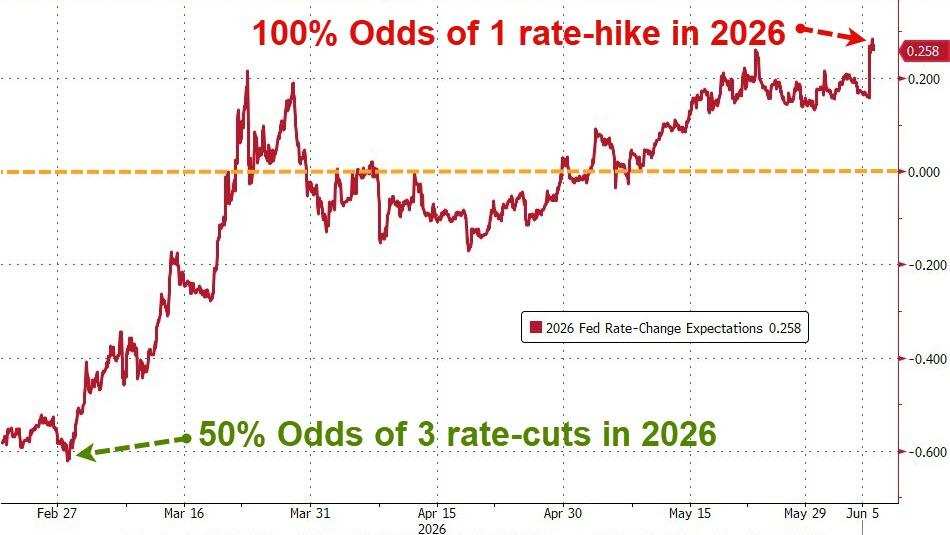

Data from the interest rate swaps market shows that as of last Friday, traders had fully priced in one rate hike by the Federal Reserve during 2026, with the probability of a hike in October briefly reaching around 60%, and a December hike now seen as virtually certain.

Editor/melody