Summary

With the June FOMC meeting approaching, Waller’s debut is drawing significant attention. His views on the U.S. economy, inflation, AI, and monetary policy stance could all serve as key signals for the next phase of market positioning. This article focuses specifically on the likelihood and conditions under which Waller might advocate for an early rate hike.

I. Key Considerations: Will Waller Push for an Early Rate Hike?

(I) Waller’s Policy Philosophy: From 'Data Dependency' to 'Leaning Against the Wind'

(I) Waller’s Policy Philosophy: From 'Data Dependency' to 'Leaning Against the Wind'

Waller has criticized Powell’s 'data-dependent' decision-making approach and plans to implement reforms aimed at reducing the Federal Reserve’s influence on markets. In the Fed’s view, the ideal inflation environment is one in which households and markets 'benignly ignore' the existence of inflation, and the optimal policy practice is one where markets 'benignly ignore' the Fed and monetary policy altogether. Clearly, current conditions fall far short of this ideal.

Under Waller, the Fed may return to the Volcker-Greenspan tradition of 'leaning against the wind.' Waller argues that data dependency introduces lags into monetary policy and causes markets to overreact to minor data fluctuations. He contends that the Fed should not be constrained by short-term data noise but instead base its judgments on longer-term economic narratives. In other words, if the Fed’s actions are not dictated by short-term data, markets will also stop being driven by such data, potentially leading to lower volatility.

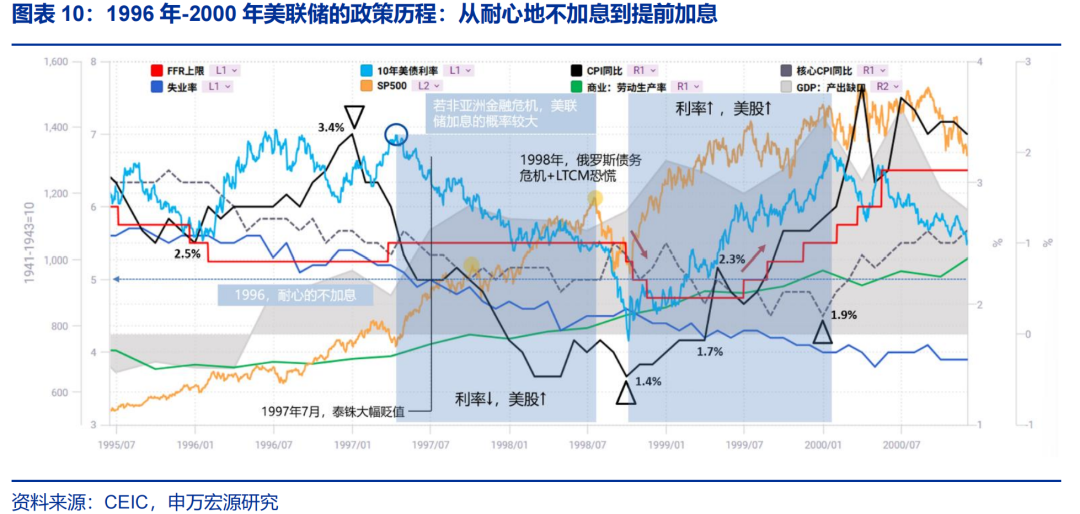

(II) Historical Precedents of 'Leaning Against the Wind': Greenspan’s Shift from Opposing Rate Hikes to Implementing 'Early Hikes,' 1996–2000

'Leaning against the wind' works both ways: during tightening cycles, the inflation threshold triggering a rate hike is lower; during easing cycles, the inflation threshold required to justify a rate cut is higher. The Fed’s objective is to stay ahead of the curve. During the Volcker-Greenspan era, the Fed implemented preemptive rate hikes in 1984, 1987, 1994, 1999, and 2004—typically when CPI year-over-year inflation had just rebounded above 2%, or when markets began pricing in inflation, as reflected in rising 10-year Treasury yields or breakeven inflation rates.

In 1996, Greenspan opposed raising rates based on his expectation that technological progress would boost productivity. Through discussions with businesses and analysis of granular data, he anticipated that the information technology revolution would raise potential GDP growth and lower the natural rate of unemployment, thereby enabling high growth, low unemployment, and low inflation simultaneously. Consequently, he rejected internal FOMC recommendations (from Governors Meyer and Yellen) in 1996 to hike rates by 25 bps on the grounds that unemployment had fallen too low. History later vindicated Greenspan’s judgment.

In June 1999, amid resurgent inflation and signs of 'irrational exuberance' in equity markets, the Fed implemented an early rate hike. At the time of the hike, headline CPI had risen from 1.7% to 2.3% year-over-year, while core CPI continued to decline. The output gap was widening, and the unemployment rate kept falling. Greenspan recognized that wealth effects from asset price inflation were translating into tangible demand pressures. To prevent inflation from retracing the path of the 1970s, he opted for front-loading rate hikes—even at the risk of bursting the stock market bubble.

(III) Will Waller Pursue an Early Rate Hike? Monetary policy is easier to tighten than to ease, and the midterm elections impose a temporal constraint that may delay action.

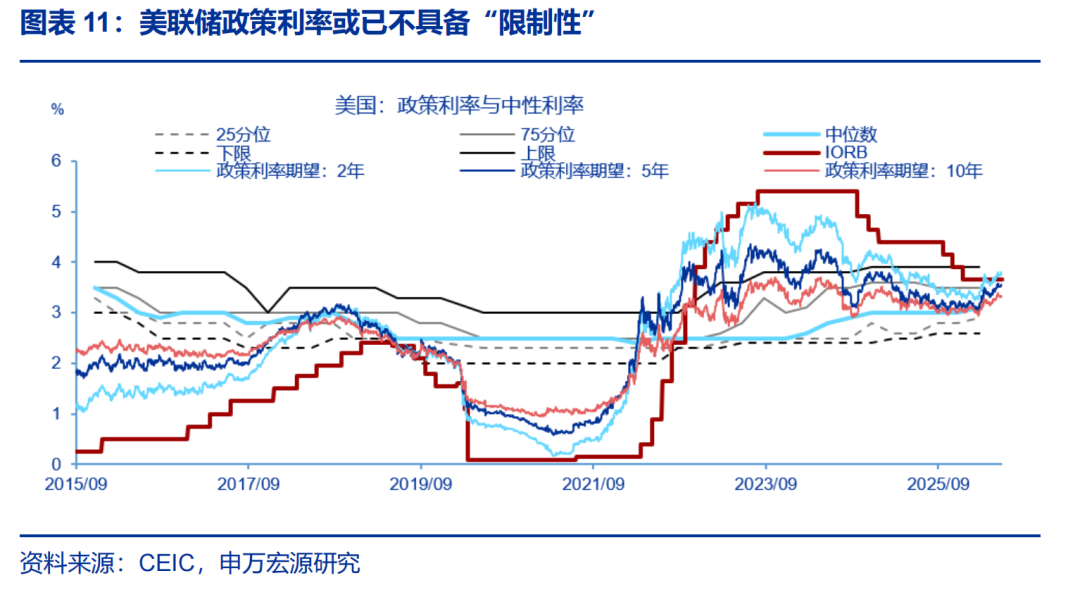

The Federal Reserve’s rate-cutting cycle may have already 'ended prematurely.' Currently, the real policy rate has turned negative, while economic growth remains resilient, implying that the policy rate is no longer restrictive—and may even be accommodative. According to estimates from multiple models, the U.S. neutral interest rate is likely around 3.4%; markets have already priced in an expected Fed policy rate of 3.77% over the next two years. Moreover, financial conditions remain relatively loose.

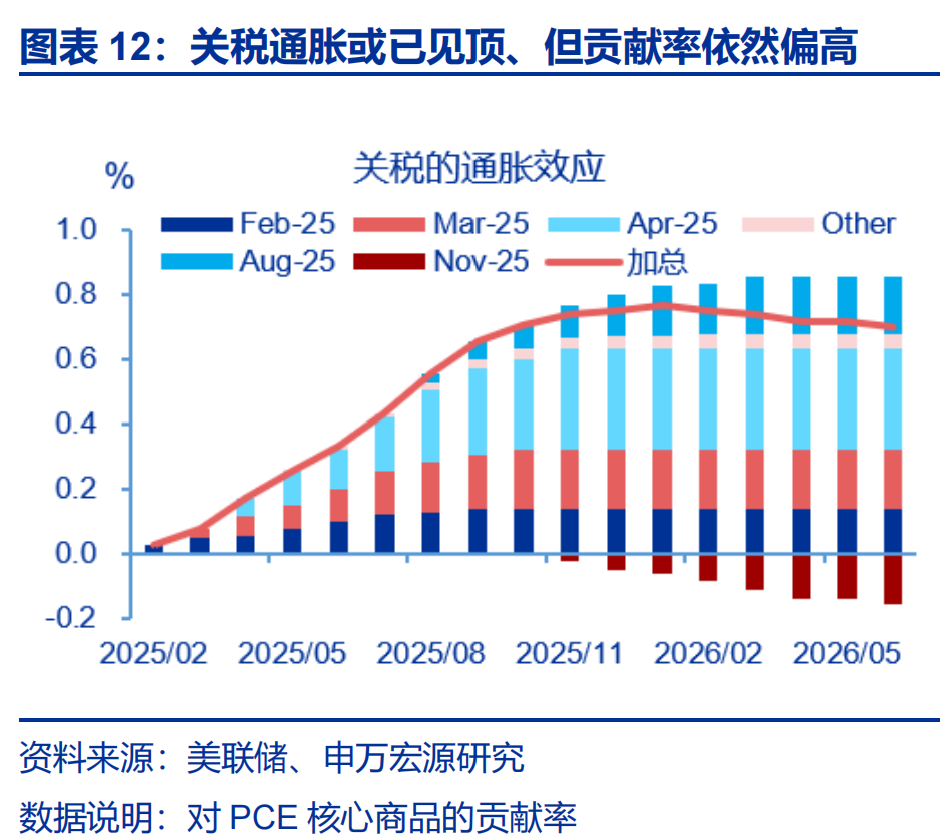

On the macro front, inflationary pressures continue to trend upward, and the labor market has stabilized and is marginally tightening, suggesting that monetary policy is more likely to tighten than ease. U.S. inflationary pressures stem from three sources: (1) oil-driven inflation, (2) tariff-induced inflation, and (3) AI-related inflation—all of which exhibit a degree of persistence. Since the beginning of the year, nonfarm payrolls have rebounded significantly, and the risk of rising unemployment appears manageable, making it unlikely that conditions for rate cuts in 2024–2025 will materialize.

The stability of inflation expectations may be the key area where FOMC members seek consensus despite differences. AI-related capital expenditures and oil prices are two critical variables. In the short term, given the reality of a 'K-shaped' economy and the one-off nature of certain inflation drivers, the Fed’s current 'patience'—refraining from raising rates—is reasonable, though time-limited. If medium- to long-term inflation expectations continue to rise, the probability of rate hikes after the midterm elections will increase significantly.

Risk Warning

Oil prices have risen above expectations; Kevin Warsh’s policy stance is relatively hawkish; U.S. economic slowdown has exceeded expectations.

Report Body

U.S. Maynonfarm payrollsSignificantly exceeding expectations, this has triggered a 'tightening trade' in the markets. With the June FOMC meeting approaching, Chair沃什's debut is drawing considerable attention; his views on the U.S. economy, inflation, AI, and monetary policy stance could all become key factors guiding market positioning in the next phase. This article focuses on the possibility and conditions for沃什 to raise interest rates earlier than expected.

I. Will Waller advocate an 'early rate hike'?

(I) Waller’s Policy Philosophy: From 'Data Dependency' to 'Leaning Against the Wind'

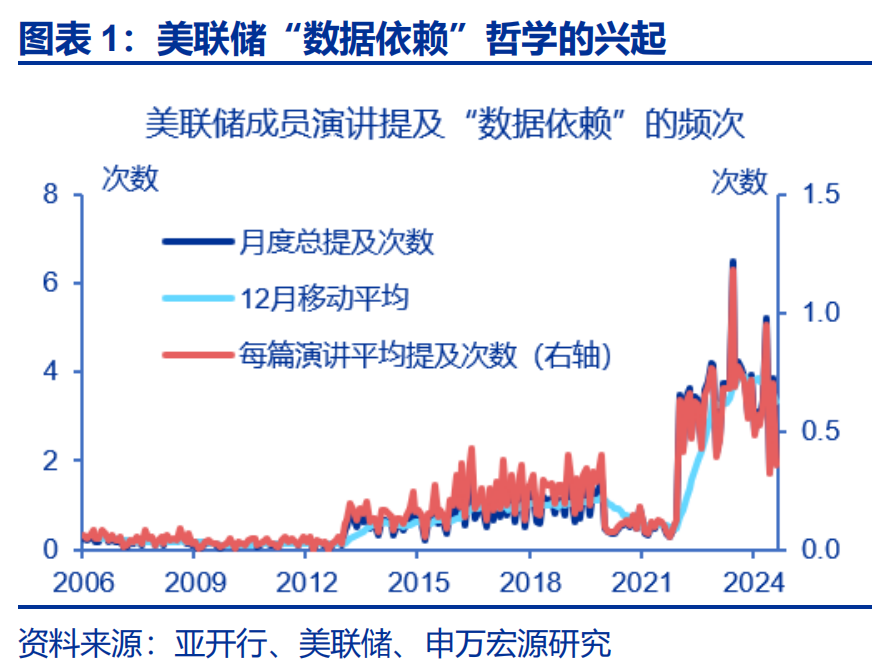

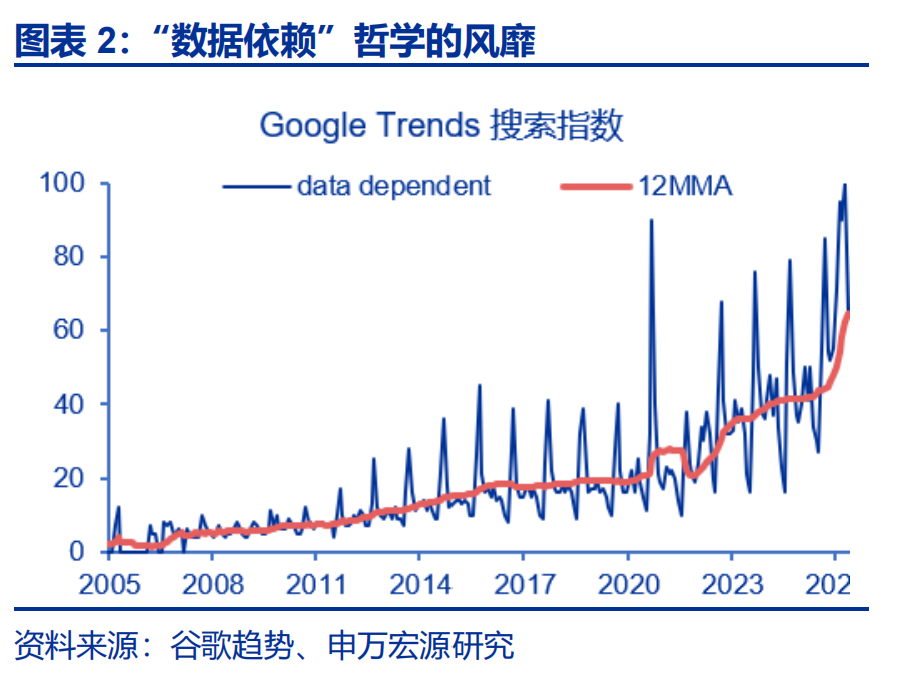

In the Fed’s view, the ideal inflation environment is one in which households and markets 'benignly ignore' the existence of inflation, and the optimal policy practice is one where markets 'benignly ignore' the Fed and monetary policy altogether. Since the Fed began hiking rates in 2022, U.S. economic data—primarily inflation and nonfarm payrolls—as well as every move by the Fed and speeches by FOMC members, have kept financial markets on edge. While this is certainly tied to shifting macroeconomic conditions, Waller believes the Fed should have implemented 'reforms' to reduce its role as a source of market volatility.

Markets may need to readjust to Waller’s era of a 'lean against the wind' policy philosophy. Unlike Powell’s era of 'data dependence,' Waller’s Fed is likely to favor a 'lean against the wind' approach. Waller argues that the data-dependent framework renders monetary policy backward-looking, causing the Fed to respond sluggishly to structural shifts—for example, the March 2022 rate hike was significantly 'behind the curve,' forcing the Fed into a 'catch-up' mode early in the hiking cycle. Alternatively, it can lead to overreactions to temporary shocks, as evidenced by the 'stop-go' pattern observed in the current easing cycle.

This approach causes financial markets to overreact to minor data fluctuations, even though such data often carry substantial estimation errors. He contends that the Fed should not be constrained by short-term data noise but should instead base its judgments on longer-term economic narratives. In other words, if the Fed’s actions are not dictated by fleeting data, markets will also avoid being driven by them, potentially reducing volatility.

In fact, the Fed’s policy philosophy has never been static; the debate between data dependence and leaning against the wind is essentially old wine in new bottles. Data dependence is inherently procyclical and stands in binary opposition to 'leaning against the wind.' Broadly speaking, the Fed’s monetary policy frameworks can be categorized into two types:

First is the alternating 'go-stop' monetary policy (i.e., discretionary policy). Policymakers employing this approach generally believe inflation stems from real shocks rather than monetary phenomena. Its theoretical foundation lies in Keynesianism, and operationally it follows the Phillips curve, viewing full employment as the primary objective of monetary policy, while price stability is left to income policies. This 'go-stop' monetary policy is procyclical because, according to the Phillips curve, the only way to reduce inflation is by increasing unemployment.

Second is rule-based monetary policy. It emphasizes establishing credibility in monetary policy, anchoring inflation expectations, stabilizing the price level, and reducing inflation volatility—for example, by adjusting the federal funds rate to achieve a target growth rate for the money supply. Its theoretical foundations are the quantity theory of money and rational expectations theory, corresponding to a vertical Phillips curve. The classic articulation of this view is Milton Friedman’s assertion: 'Inflation is always and everywhere a monetary phenomenon.' Rule-based monetary policy acts 'against the wind' and emphasizes preemption—nipping any incipient inflationary pressures that might exceed the target 'in the bud.'

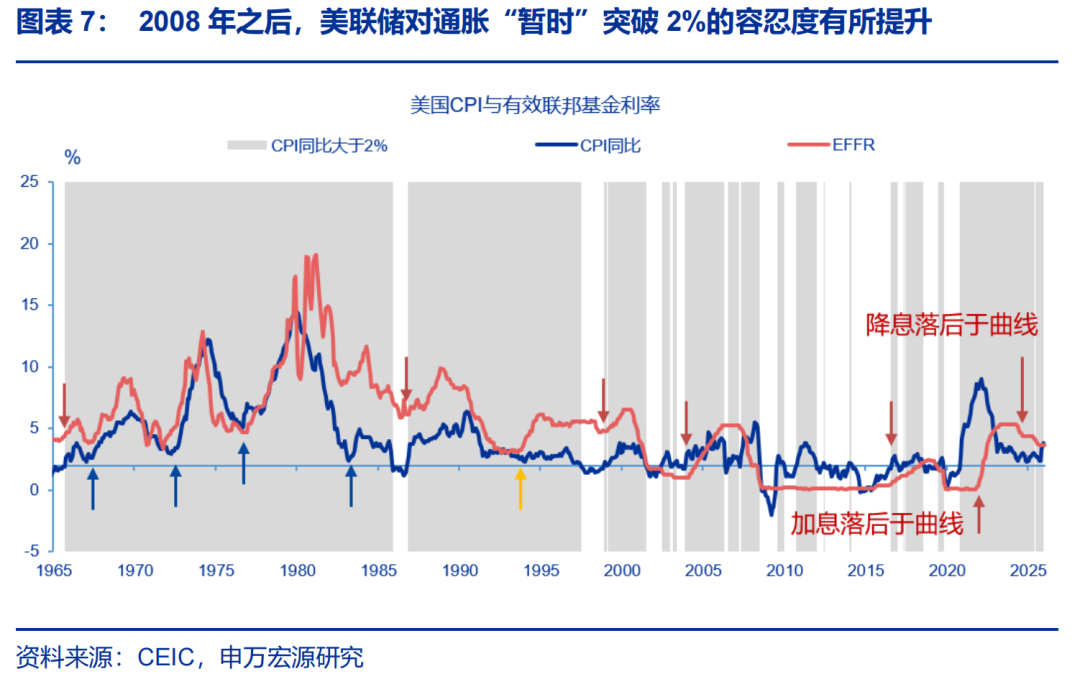

Generally speaking, 'leaning against the wind' rules place greater emphasis on upside inflation risks, whereas discretionary rules focus more on downside growth risks. From the perspective of the output gap, a 'leaning against the wind' rule calls for raising interest rates as soon as the output gap turns positive—the Bank of Japan still considers a positive output gap a key indicator of whether inflationary pressures are sustainable. In contrast, the 'go-stop' rule waits until the economy shows clear signs of overheating before hiking rates. Prior to 2008, a common trigger for the Federal Reserve to raise rates was when year-over-year CPI rose above 2% from below or reversed direction while already above 2%. After 2008, the Fed significantly increased its tolerance for inflation exceeding the 2% threshold.

Waller may revive the Martin-Volcker-Greenspan tradition by reinstating a 'leaning against the wind' rule and restoring the Fed’s reputation as an 'inflation fighter.' This stance is not simply or statically 'hawkish' or 'dovish'; rather, it shifts from rigidity to flexibility and from data dependence to a more autonomous approach: being hawkish earlier when necessary, dovish earlier when appropriate, and neutral—practicing 'wu wei' (non-intervention)—when conditions warrant. Thus, what Waller changes is the timing and magnitude of policy moves, not their direction.

This carries two implications for future Fed policy: First, in the short term, although inflationary pressures appear to be rising, if Waller deems them 'transitory,' he may choose to look through the inflation spike, maintain a neutral policy stance, and temper market expectations for rate hikes. Second, over the medium term, once inflationary pressures are confirmed to be persistent, Waller may no longer wait for additional data before initiating rate hikes.

(2) Historical Examples of 'Leaning Against the Wind': 1996–2000, Greenspan Shifted from 'Patiently Holding Rates Steady' to 'Preemptive Hikes'

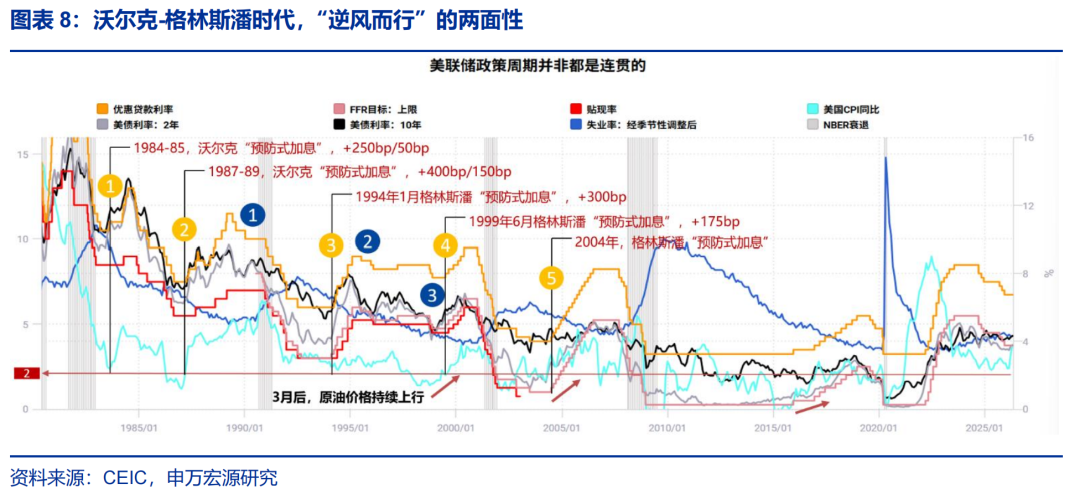

It is important to emphasize that 'leaning against the wind' is bidirectional, not unidirectional: during tightening cycles, the inflation threshold triggering rate hikes is lower; during easing cycles, the inflation threshold triggering rate cuts is higher. The Federal Reserve aims to stay ahead of the inflation curve. During the Volcker-Greenspan era, the Fed implemented 'leaning against the wind' tightening in 1984, 1987, 1994, 1999, and 2004—typically when year-over-year CPI rebounded and just surpassed 2%, or when markets began pricing in inflation, reflected in rebounds in the 10-year Treasury yield or breakeven inflation rates.

Conversely, the Fed pursued 'leaning against the wind' easing in 1989, 1995, and 1998. In 1989, the main driver was economic cooling following prior rate hikes—even though inflation remained on an upward trajectory. In 1995, the catalyst was the Mexican debt crisis, and in 1998, it was the Russian debt crisis and the collapse of Long-Term Capital Management (LTCM), which triggered market panic.

Given the backdrop of technological revolution, the Federal Reserve’s monetary policy practices under Greenspan from 1994 to 2000 may offer valuable insights. This article primarily examines the following four cases: (1) the inflation scare and preemptive rate hikes from February 1994 to February 1995; (2) the period of unchanged interest rates from 1996 to 1998; and (3) the preemptive rate hikes beginning in June 1999.

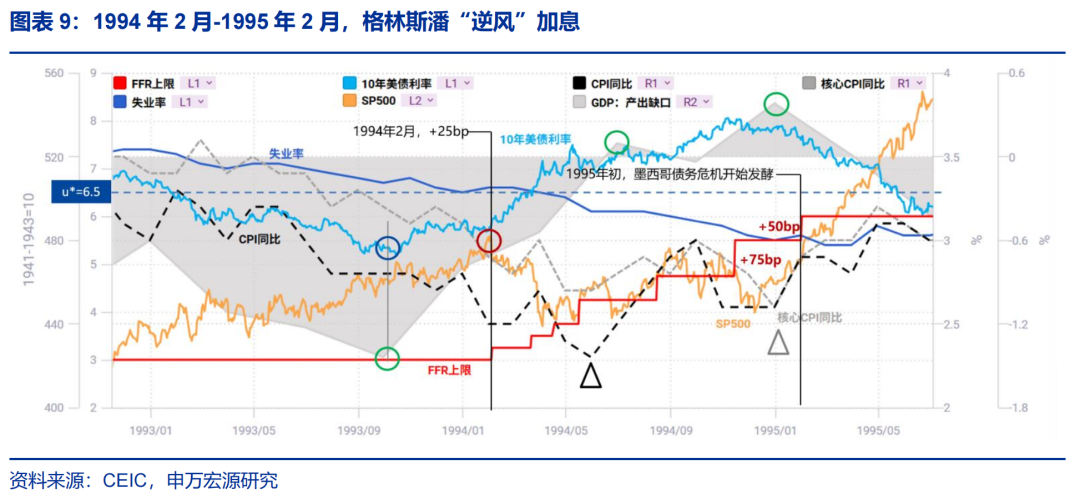

(1) From February 1994 to February 1995, the Fed raised rates seven times in anticipation of an inflation rebound ('leaning against the wind'), lifting the federal funds rate (FFR) upper bound from 3% to 6% (+300 bps in total). The U.S. economy began recovering in Q4 1993, and the 10-year Treasury yield bottomed out and started rising. Ahead of the February 1994 FOMC meeting, some members recommended a 50 bps hike, but Greenspan insisted on caution and opposed tightening, stating it was 'not yet time to make that decision.' The rise in real interest rates did not impede the strong economic recovery or the buildup of inflation expectations. At the February and March meetings, Greenspan tested the waters with modest 25 bps hikes each time.

However, indicators such as capacity utilization, supplier delivery times, the output gap, the unemployment gap, and the 10-year U.S. Treasury yield all suggest that the economy was overheating. Consequently, starting in May, the Federal Reserve increased the pace of rate hikes to either 75 or 50 basis points, continuing until its final 50-basis-point hike in February 1995.

This was a classic case of 'leaning against the wind.' The Fed raised rates even as inflation continued to decline. The year-over-year CPI bottomed out in May 1994 at 2.3%, while core CPI stood at 2.7% year-over-year. However, the 10-year Treasury yield had already reached its trough as early as October 1993. Greenspan’s sharp policy pivot triggered a significant market correction, with the S&P 500 declining nearly 9% from February to April (from 482 to 439), only fully recovering around the time of the Fed’s final rate hike in February 1995.

During his 1994 congressional testimony, Greenspan described the approach of raising rates only after inflation had already risen as 'backward-looking adjustment' (Hazel, A History of U.S. Monetary Policy by the Federal Reserve, pp. 306–307). Greenspan believed that a positive output gap or a tightening labor market was closely linked to rising inflation expectations.

(2) From February 1996 to September 1998, despite a persistently positive output gap and continuously falling unemployment, the Federal Reserve kept interest rates unchanged. In 1996, U.S. CPI rose year-over-year from 2.5% to 3.4%, while core CPI declined steadily from 3.0% to 2.6%; the unemployment rate fell from 5.6% to 5.4%; and the 10-year Treasury yield rose from 5.6% to 7%, remaining elevated thereafter.

Thus, voices within the FOMC supporting rate hikes were persistent. However, Greenspan argued that gains in labor productivity would break the empirical regularity of the Phillips curve. He insisted that monetary policy should exercise 'forbearance' rather than raise rates solely based on 'excessively low unemployment.'

Through direct engagement with businesses and analysis of granular data, Greenspan anticipated that the information technology revolution would raise potential economic growth and lower the natural rate of unemployment, enabling the economy to simultaneously achieve high growth, low unemployment, and low inflation. Consequently, he rejected internal FOMC proposals in 1996—such as those from Governors Meyer and Yellen—to raise rates by 25 basis points on the grounds that unemployment had fallen too low. In hindsight, Greenspan proved correct. By 1997, as unemployment dipped below 5%, Greenspan began signaling future rate hikes, but the Asian financial crisis prompted him to maintain patience.

Greenspan later acknowledged that between 1997 and 1998, concerns about U.S. dollar appreciation somewhat constrained the FOMC’s willingness to raise rates, as higher rates could accelerate capital outflows from Asia. Moreover, the Asian financial crisis was also expected to dampen external demand to some extent.

(3) In June 1999, driven by persistently rebounding inflation and the stock market’s 'irrational exuberance,' the Federal Reserve initiated 'preemptive rate hikes,' raising the federal funds rate (FFR) target ceiling from 4.75% to 6.5% (+175 basis points) by May 2000. This tightening cycle was preceded by precautionary rate cuts totaling 75 basis points from September to November 1998, primarily in response to market turmoil triggered by Russia’s debt default and the collapse of Long-Term Capital Management (LTCM). However, the shock proved transitory. After the Fed’s second consecutive rate cut in October 1998, markets began pricing in a recovery, with both U.S. equities and Treasury yields rising in tandem. Bolstered by the Fed’s precautionary easing, strong corporate earnings, and robust GDP growth, the U.S. equity market moved toward a bubble.

When the Fed began hiking rates in June 1999, the macroeconomic backdrop was as follows: crude oil prices pushed CPI year-over-year up from 1.7% in March–April to 2.3%, though core CPI continued its downward trend. The economy was overheating, with the output gap widening and unemployment continuing to fall. Greenspan recognized that wealth effects stemming from asset price inflation were translating into tangible demand pressures. To prevent inflation from reverting to the patterns of the 1970s, he opted for a 'front-loaded tightening' strategy—even if it risked bursting the equity bubble.

(III) Will Waller Pursue an Early Rate Hike? Monetary policy is easier to tighten than to ease, and the midterm elections impose a temporal constraint that may delay action.

There is currently significant divergence in market views regarding Walsh’s monetary policy stance. On one hand, it is questionable whether his hawkish stance during his tenure as a Fed governor and around the time of his 2017 nomination can be directly applied to the present context; on the other hand, his more dovish posture surrounding this current nomination may also not be representative. Since his nomination, Walsh has deliberately avoided articulating a specific monetary policy position and has remained entirely silent since his confirmation.

Regarding whether Walsh will advocate for an 'early rate hike' in the second half of the year, the current 'state' of the Federal Reserve’s policy rate and its reaction function remain a sound analytical starting point. First, the Fed’s policy rate is no longer restrictive—in fact, it is somewhat accommodative. The March Summary of Economic Projections indicates a nominal long-run neutral rate of 3.1% (1.1% real rate + 2% inflation target). The 1.1% estimate for the real neutral rate is relatively conservative; given declining savings rates, rising AI-related capital expenditure demand, and persistently high fiscal deficits, a further upward shift in the neutral rate is highly probable.

According to multi-model composite estimates, the neutral rate may be around 3.4%, slightly below the Interest on Reserve Balances (IORB) rate of 3.65%. Markets have already priced in an expected Fed policy rate of 3.77% over the next two years. The current effective policy rate has already turned negative (with April U.S. CPI expected to exceed 4%), and financial conditions remain relatively loose.

Second, if forward-looking policy considerations are emphasized, the key issue is how to assess current U.S. inflationary pressures. We believe these pressures stem primarily from three sources: (1) energy-driven inflation; (2) tariff-induced inflation; and (3) AI-related inflation. While oil-driven inflation is largely one-off, significant uncertainty remains regarding Strait of Hormuz shipping access and the medium-term trajectory of oil prices. Tariff-driven inflation has recently been the main reason why PCE inflation has consistently exceeded CPI inflation. The Fed estimates that by early 2026, tariffs could contribute up to 0.8 percentage points to core PCE inflation. Although tariff effects may have already entered a downward phase, their contribution to inflation is likely to remain elevated for some time.

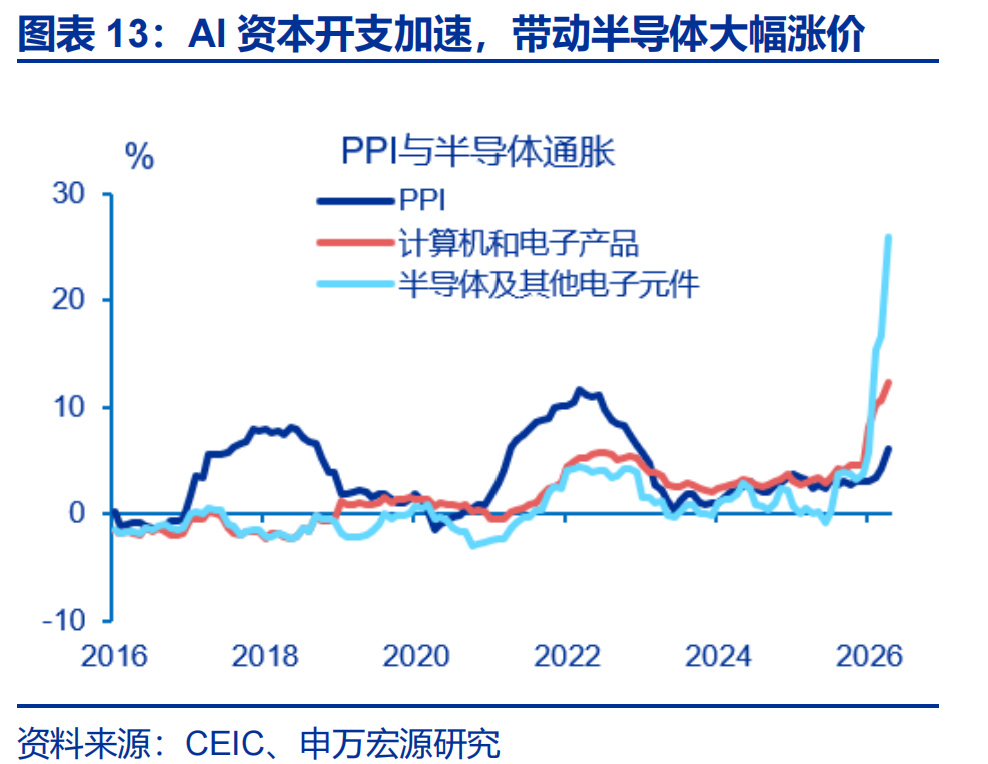

AI-related capital expenditures have already driven sharp price increases in semiconductors and other capital goods. Coupled with accelerating deployment on the application side, the scope of these price increases is likely to broaden further. The PCE diffusion index is already at historically elevated levels, indicating that U.S. reflationary pressures stem from the confluence of multiple factors.

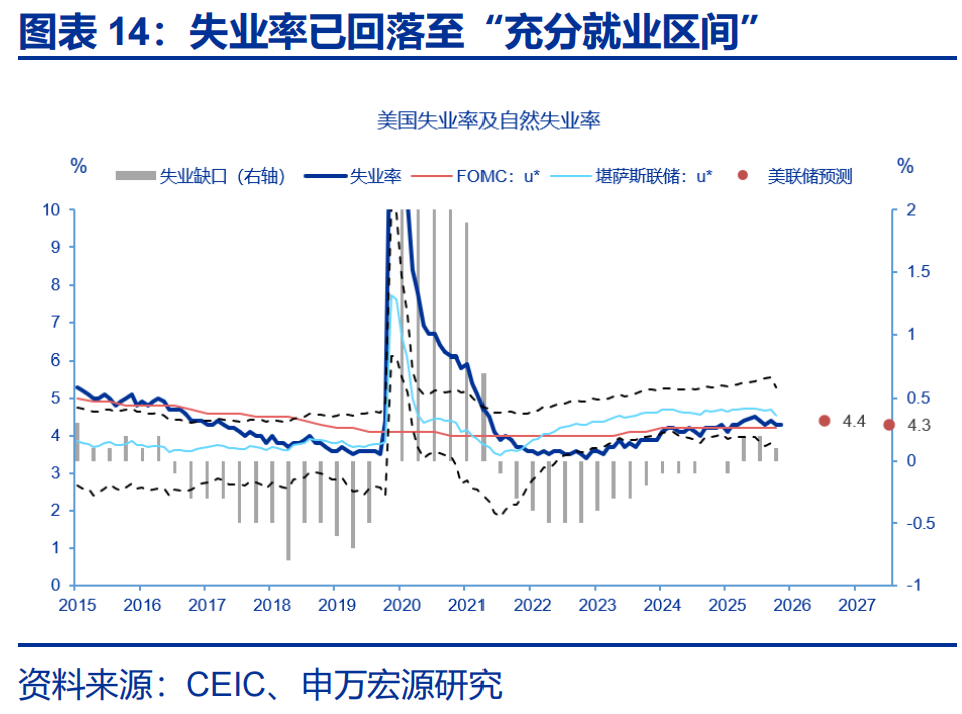

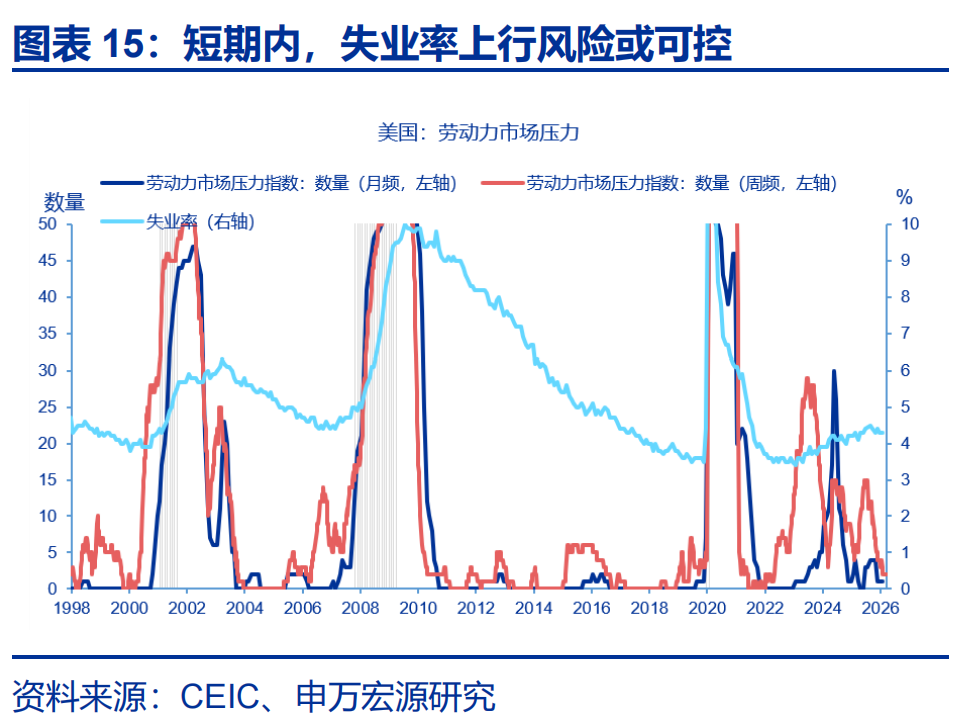

Third, the labor market is already at full employment and may even be tightening marginally, making it unlikely that an unexpected rise in unemployment will trigger another Fed rate cut—repeating the 2024–2025 easing path. Nonfarm payroll growth appears to have emerged from the near-zero growth trend observed in the second half of 2025, and the unemployment rate has declined from a peak of 4.6% to 4.3%, aligning closely with the estimated natural rate. According to the unemployment rate diffusion index across the 50 states, near-term upside risks to unemployment appear contained. Considering both labor market conditions and cyclical sector performance, the U.S. economy may currently be in a state of 'mid-air refueling'—the output gap has remained positive for 19 consecutive quarters since Q2 2021. AI-driven capital spending is fueling both volume and price gains in cyclical sectors. If we apply the empirical models used by the Fed during the Volcker–Greenspan era, the Fed 'should' hike rates preemptively.

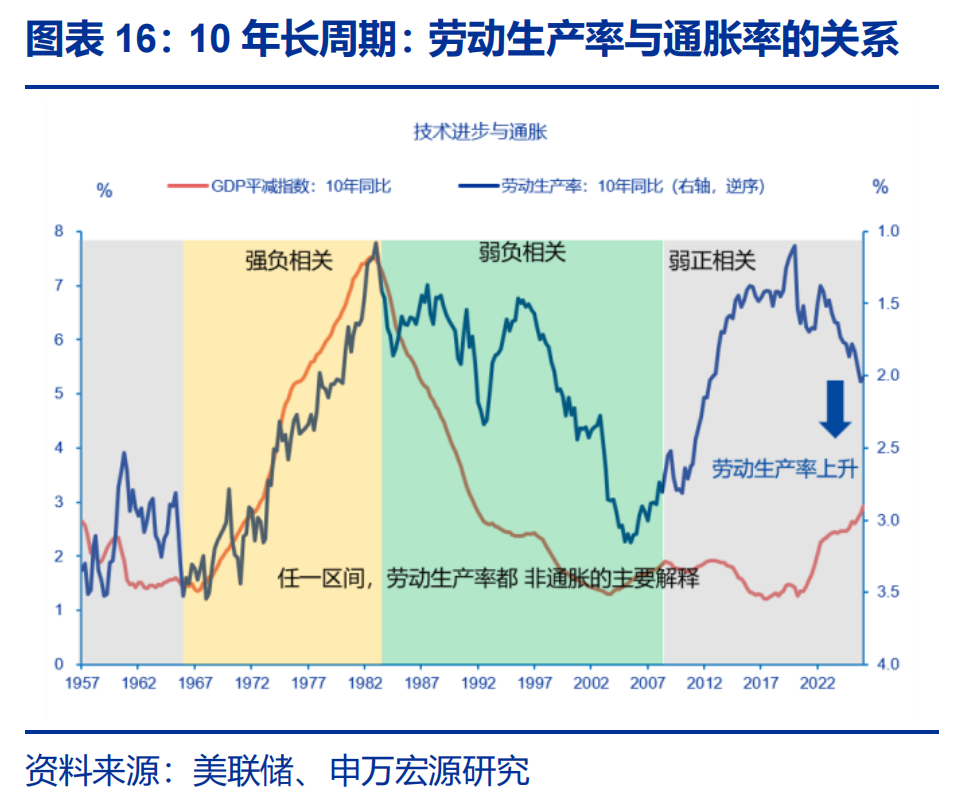

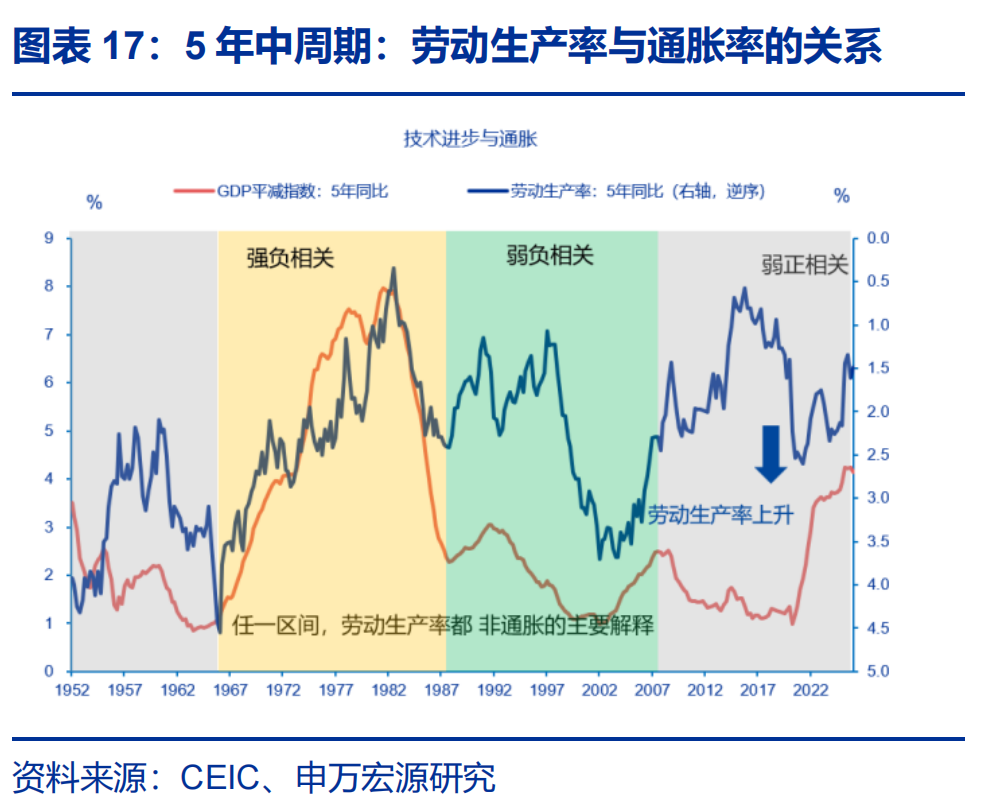

Fourth, could AI-driven gains in labor productivity lead the Fed to 'look through' inflation and maintain patience without hiking rates? We lean toward viewing this as merely a secondary argument, and one that currently lacks strong persuasive power. Based on 10-year year-over-year comparisons, the turning point in U.S. labor productivity growth has already been confirmed.

However, the relationship between labor productivity growth and inflation cannot be simplistically reduced to 'technological progress is deflationary.' In the short term, the inflationary impact of AI-related capital spending is evident. Salem Abo-Zaid (2026) estimates that from 2007 to 2025, AI contributed on average approximately 0.2% to U.S. inflation, with this effect trending upward in recent years. Goldman Sachs also estimates that AI could add about 0.3% to core PCE inflation over the coming year.

In the long run, first, there is a prolonged and unstable lag between technological progress and labor productivity gains; second, the relationship between labor productivity growth and inflation is unstable: whether higher productivity leads to lower inflation depends on the relative dynamics between wage growth and productivity growth. Empirically, even during the late 1960s to early 1980s—when the two variables exhibited a strong negative correlation—the rise in inflation was not caused by declining productivity; rather, oil supply shocks were the common driver behind both phenomena.

In summary, based on the current level of the policy rate and the Fed’s reaction function, monetary policy is more likely to tighten than ease. However, considering the economy’s 'K-shaped' divergence and the nature of current inflation drivers—either one-off events, past their peaks, or insensitive to interest rates (e.g., AI-related inflation)—the Fed’s decision to maintain patience and hold rates steady is reasonable, akin to the Greenspan-era episode in 1996.

The differences are as follows: (1) Walsh has not yet established authority within the FOMC, and it is uncertain whether he can persuade members to vote in favor of his proposals; (2) the 1990s were an era of globalization, whereas today is an era of deglobalization—the disinflationary effect of technological progress may be significantly diminished, casting doubt on whether the conditions for Walsh’s “marking the boat to find the sword” approach are sufficient. Indeed, we cannot even be certain whether Walsh’s policy stance is hawkish, neutral, or dovish. In the short term, the stability of medium- to long-term inflation expectations may be the key basis for consensus among FOMC members, regardless of their individual hawkish or dovish leanings. Thus, the oil price anchor remains a critical variable.

This study finds the following:

1. Markets may need to reacquaint themselves with Walsh’s ‘policy philosophy’—shifting from Powell’s ‘data dependence’ back to the Volcker-Greenspan tradition of ‘leaning against the wind.’ Walsh argues that the Federal Reserve should not be constrained by short-term data noise but should instead base its judgments on longer-term economic narratives. If the Fed’s actions are not dictated by short-term data fluctuations, markets will likewise avoid being driven by such data, potentially leading to lower volatility.

2. Leaning against the wind requires the Federal Reserve to act earlier when it should be hawkish, act earlier when it should be dovish, and maintain neutrality—‘governing through non-action’—when a neutral stance is appropriate. This carries two implications for future Fed policy: First, in the short term, although inflationary pressures are trending upward, if Walsh views these pressures as ‘transitory,’ he may choose to look through inflation and maintain a neutral policy stance. Second, in the medium term, if inflationary pressures prove persistent, Walsh may no longer wait for additional data before raising rates.

3. The Federal Reserve’s rate-cutting cycle may have already ‘ended prematurely.’ The real policy rate is no longer restrictive—in fact, it may be somewhat accommodative. Inflationary pressures continue to trend upward, while the labor market has stabilized and is showing signs of tightening at the margin, implying that monetary policy is more likely to tighten than ease. U.S. inflationary pressures stem from three sources: (1) crude oil-driven inflation; (2) tariff-induced inflation; and (3) AI-related inflation—all of which exhibit some degree of persistence. Since the beginning of the year, nonfarm payroll employment has rebounded significantly, and the risk of rising unemployment appears contained, making it unlikely that conditions triggering Fed rate cuts will materialize in 2024 or 2025.

4. The stability of inflation expectations may be the key point of convergence for FOMC members despite their differing views, with AI-related capital expenditures and oil prices serving as two critical variables. In the short term, given the reality of a ‘K-shaped’ economy and the transitory nature of certain inflation drivers, the Fed’s patience in refraining from rate hikes is reasonable—but time-limited. If medium- to long-term inflation expectations continue to rise, the probability of post-midterm-election rate hikes will increase significantly.

Risk Warning

1. The structural level of crude oil prices has risen more than expected. With the Russia-Ukraine conflict still unresolved and heightened geopolitical instability in the Middle East, the structural level of oil prices may rise beyond expectations, thereby increasing the risk of stagflation in the global economy.

2. Walsh’s policy stance may lean ‘hawkish.’ If oil prices remain structurally high over the long term, driving up medium- to long-term inflation expectations, Walsh’s monetary policy stance could become more hawkish.

3. The U.S. economy could slow down more than expected. The labor market remains in a state of ‘low-growth equilibrium,’ risks in private credit markets have yet to be fully resolved, and consumption sustained by drawing down savings is unlikely to be sustainable.

Editor/melody