Qunce Technology is a leading supplier of advanced IC packaging substrates in mainland China, specializing in the R&D, manufacturing, and sales of IC substrates.

Zhitong Finance APP learned that, according to an announcement by the Hong Kong Stock Exchange on June 8, Suzhou Qunce Technology Co., Ltd. (referred to as Qunce Technology) has filed a listing application with the Main Board of the Hong Kong Stock Exchange, with CITIC Securities serving as its sole sponsor.

Company Profile

According to the prospectus, Qunce Technology is a leading supplier of advanced IC packaging substrates in mainland China, focusing on the R&D, manufacturing, and sales of IC substrates. Based on data from Frost & Sullivan, by revenue, Qunce Technology was the largest IC substrate company in both the FCBGA substrate market and the FCCSP substrate market in mainland China in 2025, with market shares of 25.3% and 13.4%, respectively. Additionally, by revenue, Qunce Technology was the second-largest IC substrate company in mainland China in 2025, with a market share of 12.5%.

According to the prospectus, Qunce Technology is a leading supplier of advanced IC packaging substrates in mainland China, focusing on the R&D, manufacturing, and sales of IC substrates. Based on data from Frost & Sullivan, by revenue, Qunce Technology was the largest IC substrate company in both the FCBGA substrate market and the FCCSP substrate market in mainland China in 2025, with market shares of 25.3% and 13.4%, respectively. Additionally, by revenue, Qunce Technology was the second-largest IC substrate company in mainland China in 2025, with a market share of 12.5%.

The parent company of Qunce Technology, ASE Group of Taiwan, entered the IC substrate market in 1997 and has been deeply engaged in this industry for nearly 30 years, amassing substantial expertise. As a global leader in IC substrates, ASE Group has consistently ranked first worldwide by revenue for many consecutive years. Qunce Technology's Suzhou manufacturing base is the first in mainland China to offer a fully integrated, end-to-end IC substrate production capability at a single site, enabling it to produce the complete range of FCBGA, FCCSP, and CSP substrates, thereby streamlining procurement and facilitating the development of advanced, multi‑technology products. Meanwhile, Qunce Technology's Huangshi production facility handles the front‑end processes for FCBGA substrates, supporting the Suzhou base. In addition, Qunce Technology has built a third state-of-the-art, smart‑manufacturing plant in Kunshan. According to Frost & Sullivan, Qunce Technology is the first company dedicated to helping customers in mainland China achieve mass production of FCBGA substrates.

Qunce Technology's IC substrates are categorized into three types: FCBGA substrates, FCCSP substrates, and CSP substrates. During the historical reporting period, the company's revenue was primarily derived from the sale of FCBGA substrates.

Qunce Technology's Suzhou production base covers an area of over 174,000 square meters and comprises one FCCSP/CSP substrate manufacturing facility and two FCBGA substrate manufacturing facilities. The Huangshi production base, with a floor space exceeding 50,000 square meters, primarily handles the front-end production processes for FCBGA substrates, thereby supporting the operations at the Suzhou site. Qunce Technology manufactures products along two main production lines: one dedicated to FCBGA substrates, and the other to FCCSP and CSP substrates. Due to differences in product technology and specifications, the equipment used in the FCCSP/CSP substrate facilities is not interchangeable with that in the FCBGA substrate facilities. The company's key production equipment includes chemical copper plating lines, direct‑image lithography exposure systems, vertical continuous copper plating lines, solder‑ball placement machines, and electronic test equipment.

Financial Information

Income

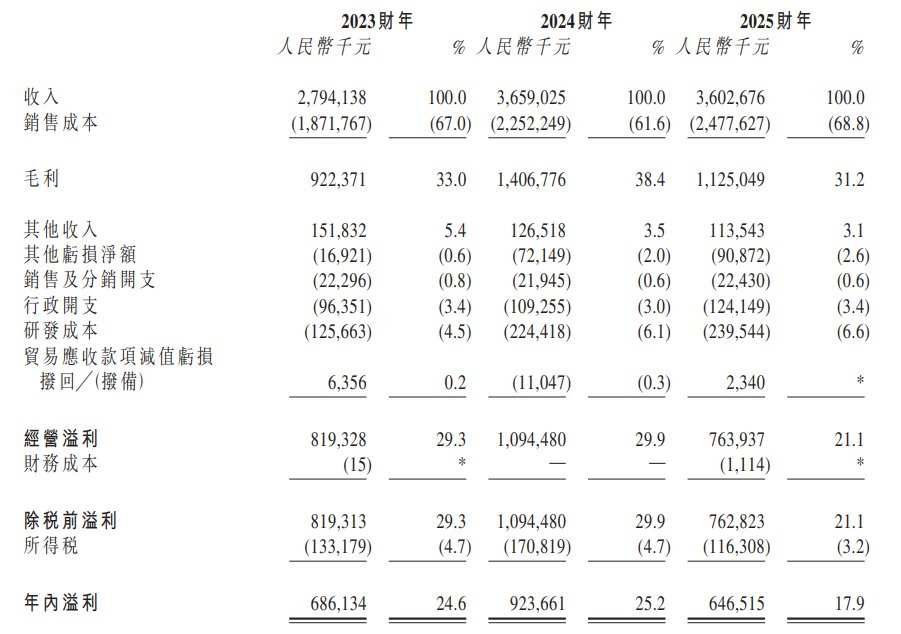

In fiscal years 2023, 2024, and 2025, the company reported revenues of approximately RMB 2.794 billion, RMB 3.659 billion, and RMB 3.603 billion, respectively.

Gross profit margin

In fiscal years 2023, 2024, and 2025, the company's gross profit margins are expected to be approximately 33%, 38.4%, and 31.2%, respectively.

Profit for the year

In fiscal years 2023, 2024, and 2025, the company reported net profits of approximately RMB 686 million, RMB 924 million, and RMB 647 million, respectively.

Industry Overview

Driven by the rapid advancement of AI computing power, the widespread adoption of advanced packaging technologies, and robust demand from key end‑application markets, the global IC substrate market has maintained steady growth, emerging as one of the fastest‑growing segments within the semiconductor industry. Mainland China is among the world's leading demand centers for IC substrates, with a growth rate exceeding the global average. Under the dual impetus of supply‑chain self‑reliance and the trend toward domestic industrialization, the pace of domestic substitution continues to accelerate. Local manufacturers have made significant progress in the mid‑to‑high‑end product segments and, through capacity expansion, technological upgrades, and quality improvements, are steadily strengthening their position within the global supply chain.

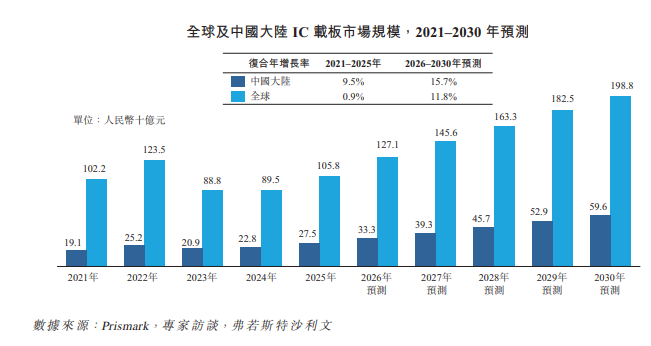

Over the historical period, both the global and mainland China IC substrate markets have expanded, with the mainland Chinese market posting a growth rate that outpaced the global average. From 2021 to 2025, the global market size grew from RMB 102.2 billion to RMB 105.8 billion, at a compound annual growth rate (CAGR) of 0.9%; during the same period, the mainland Chinese market expanded from RMB 19.1 billion to RMB 27.5 billion, with a CAGR of 9.5%. Looking ahead to 2026–2030, the global market is projected to increase from RMB 127.1 billion to RMB 198.8 billion, reflecting a CAGR of 11.8%; meanwhile, the mainland Chinese market is expected to grow from RMB 33.3 billion to RMB 59.6 billion, at a CAGR of 15.7%. As demand continues to expand and the domestic supply ecosystem matures, the mainland Chinese market is anticipated to maintain a growth trajectory that surpasses the global trend.

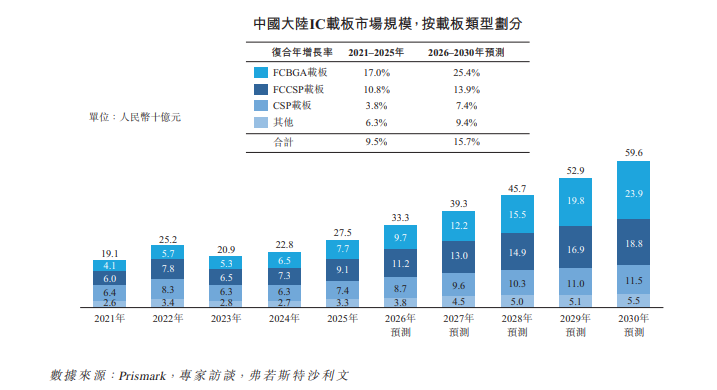

The IC substrate market in mainland China continues to grow, with a steadily diversifying product mix. By substrate type, FCBGA substrates have posted the most robust growth among major categories, with their market size expanding from RMB 4.1 billion in 2021 to RMB 7.7 billion in 2025, reflecting a compound annual growth rate (CAGR) of 17.0%. The FCBGA substrate market is projected to further expand to RMB 23.9 billion by 2030, with a CAGR of 25.4% from 2026 to 2030. This segment is expected to become the primary driver of overall IC substrate market growth.

The FCCSP substrate market size grew from RMB 6.0 billion in 2021 to RMB 9.1 billion in 2025, with a compound annual growth rate (CAGR) of 10.8% from 2021 to 2025; it is projected to reach RMB 18.8 billion by 2030, reflecting a CAGR of 13.9% from 2026 to 2030. Meanwhile, the CSP substrate market expanded from RMB 6.4 billion in 2021 to RMB 7.4 billion in 2025, posting a CAGR of 3.8% over the same period; it is expected to grow to RMB 11.5 billion by 2030, with a CAGR of 7.4% from 2026 to 2030. Driven by the rapid expansion of FCBGA substrates, the structure of China's IC substrate market is anticipated to shift further toward higher‑end products, with increasingly pronounced trends toward structural upgrading.

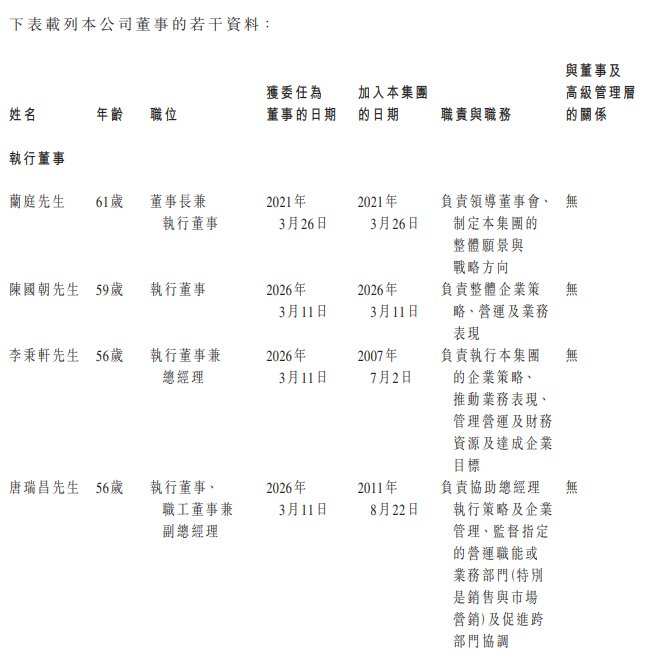

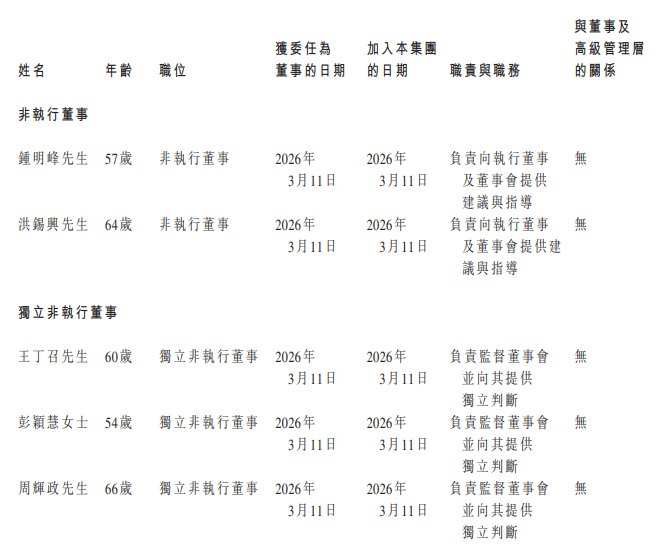

Board of Directors Information

The company's board of directors currently comprises nine directors, including four executive directors, two non-executive directors, and three independent non-executive directors. The board is responsible for the management and operation of the company's business and exercises all relevant general powers. Directors serve a term of three years and are eligible for re-election.

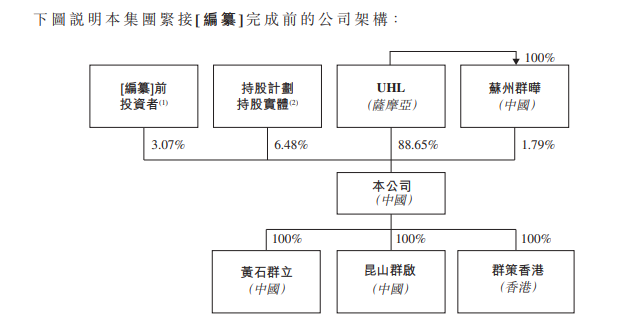

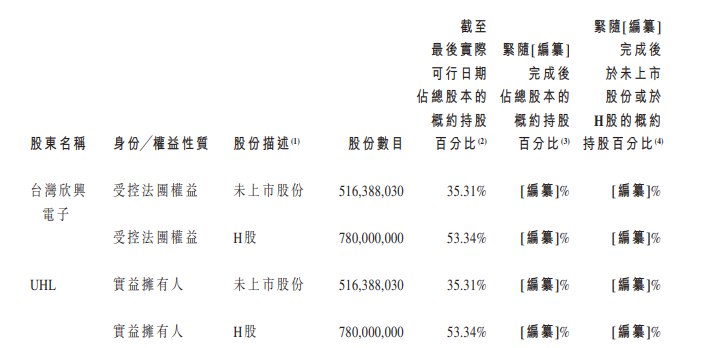

Equity Structure

China's Taiwan-based Unimicron Technology, UniBest, Hemingway, UMTC, UniWonderful, UHL, and Suzhou Qunye will serve as the company's controlling shareholders. UHL is approximately 89.43% owned by Taiwan's Unimicron Technology and about 10.57% owned by LDTaiwan. UniBest Holding Limited, a limited liability company incorporated in Samoa on January 5, 2009, is a wholly owned subsidiary of and the controlling shareholder of Taiwan's Unimicron Technology.

Brokerage Team

Sole Sponsor: CITIC Securities

Corporate Legal Counsel: DeJin Law Firm, AllBright Law Offices, Holman Fenwick Willan LLP, PwC Business Law Firm

Sponsor's Legal Counsel: Osborne Clarke, Tongshang Law Firm

Auditor and Reporting Accountant: KPMG Accounting Firm

Independent Industry Consultant: Frost & Sullivan (Beijing) Co., Ltd., Shanghai Branch

Compliance Advisor: Bosi Financing Co., Ltd.