Summary:

Hilda Ochoa-Brillembourg, founder of Strategic Investment Group, has created numerous successful investment cases. Drawing on over 30 years of investment experience, she has developed a comprehensive set of principles for successful investing.

In addition, she has mentored more than 20 strategic analysts and fund managers, many of whom have achieved remarkable success—Ray Dalio being one of them. He described Hilda as follows:

Hilda Ochoa-Brillembourg is one of the great investors of the past 30 years.

Hilda Ochoa-Brillembourg is one of the great investors of the past 30 years.

In her new book, Principles of Investing, she deconstructs the alpha strategies commonly used in the investment industry from both theoretical and practical perspectives, and refutes common investment misconceptions that often confuse both novice and experienced investors, helping readers navigate today’s investment environment—including macroeconomic conditions, political factors, and capital market developments.

Reflecting on her 40 years of investment management experience, Hilda has distilled the following 10 lessons and insights.

1. Price is not value.

For a given investor, the value of an asset may be lower or higher than its market price (or fair value), depending on how the asset relates to the investor’s existing portfolio and specific needs—even if the investor agrees with prevailing market forecasts.

Many portfolios contain legacy assets or structures (reflecting client requirements) that cannot be easily or cost-effectively altered.

Financial theory alone is insufficient to explain the relationship between market prices and investors’ utility curves. This relationship results in different ‘fair values’ for the same asset across investors (multiple equilibrium pricing).

An asset has one market price for all buyers, but its relative value differs among them.

Investing is like life: theory can teach you how markets determine asset prices, but it can never tell you whether the price of an asset will match its value once you place it into your own portfolio.

In the eyes of proponents of the efficient market hypothesis, the first lesson may be the most controversial—and perhaps the most relevant—among all my lessons.

The difference between market value and value to an investor helps explain the gap between multiple equilibrium allocations in efficient and inefficient markets, which leads different investors to pay different prices for the same asset.

For a specific buyer, the value of an investment depends on its market price, expected return and risk, as well as its correlation with the marginal investment in the conventional portfolio.

Institutional portfolios rarely start from cash. Once an optimal portfolio structure has been established using cash, it competes with the conventional portfolio.

Any new asset added to a conventional portfolio may hold a different value for your portfolio than it does for other market participants.

Aside from market price, expected return, and risk, the most important factor influencing an asset’s value is its correlation with other assets in the portfolio.

When a specific group of investors (e.g., institutional buyers) rushes en masse into a particular asset class, driving its price excessively high relative to other investors (e.g., endowment funds), those without a strategic rationale for holding the asset should refrain from acquiring it.

2. Focus on Price

The price at which you are willing to purchase an asset is one of the decisive factors determining the level of risk you face by holding that asset.

We can never know the optimal price of an asset, but we can determine whether its price is overvalued. We also know that if an asset’s valuation is at a historical high or deviates from its historical fair value by more than two standard deviations, the risk will be above average.

Post-modern financial theory holds that market prices are not always fair, as behavioral biases can impair investors’ rational decision-making and cause markets to deviate from fair value.

Given enough time, strict adherence to a defined strategy, or simply avoiding particularly poor timing, virtually any investment management style can succeed.

Put simply, as long as you purchase an asset at a reasonable price and allow sufficient time for it to revert to its intrinsic value, nearly all investment management styles can work.

There are, of course, exceptions. Over time, asset prices tend to revert toward their long-term mean. Based on this empirical observation, we find that pure momentum strategies tend to generate more losses than gains over extended periods.

Momentum investing refers to an approach where investors increase positions when security prices are stable or accelerating upward and exit promptly when they detect a reversal in the uptrend.

Momentum strategies are commonly applied to commodities, which often experience significant price volatility. Such investments are unsuitable for fundamental valuation methods like discounted cash flow analysis, as commodities generate no cash flows to discount.

If we can combine momentum strategies with price-sensitivity disciplines, we can effectively implement momentum investing in practice.

If you pay a reasonable price, your investment will generally be relatively safe over time; if you overpay, you may never fully recover your capital.

However, the best course of action at this point may be to hold onto these investments unless they remain significantly overvalued. Your future decisions should be guided by relative valuation metrics.

Many academic theories have sought to demonstrate that investments sensitive to price ("value") are more likely to generate returns than momentum-style investing, as momentum investors often overpay for the assets they purchase.

However, cheap assets sometimes remain undervalued for extended periods (a value trap), and identifying new momentum beyond such traps is crucial to avoiding prolonged entrapment in fundamentally unrecoverable, low-priced assets.

3. Do not bet all your chips

Even with strong evidence, we can never be 100% certain about any outcome. Our experiences with low-probability events—extreme and unexpected occurrences—have validated academic theories of uncertainty.

The probability of such events is extremely low, but if your portfolio is not adequately prepared to withstand them, the consequences could be catastrophic.

Of course, portfolio management should not center on low-probability events, as they are not the most likely outcomes.

We should manage our portfolios prudently so that risks faced under extreme scenarios do not become overwhelming. We must prepare for what might happen, while ensuring that low-probability events do not impair our ability to reinvest in response to more probable developments.

4. Encountering setbacks is inevitable

Although greater diversification increases the likelihood of encountering individual failures, intelligent diversification remains the best approach to risk control. Such failures should have only a minor impact on your portfolio, though they may cause embarrassment or discomfort for decision-makers.

In recent years, theories on fragile versus robust (resilient) structures—developed through observations of biological evolution—have provided valuable insights into addressing this issue.

We need to focus on the controllable vulnerabilities within a robust structure. Emphasizing the diversity and diversification of risks is central.

Although Warren Buffett might disagree, for portfolio managers, numerous small yet attractive investment opportunities are often a key source of both high returns and portfolio resilience.

Diversification allows you to add new asset classes and investment styles—introducing volatility that is diversified in nature—without subjecting the portfolio to excessive swings or highly uncertain outcomes.

For over 60 years, Buffett’s distinctive investment approach has been based on leveraging his brand effect to secure favorable purchase prices when acquiring assets.

At times, investors may have the opportunity to allocate more capital to undervalued assets (large-scale opportunistic plays) or avoid overvalued ones, but such sizable trades—typically involving 5% to 10% of the total allocation to an asset class in a single transaction—should be undertaken only with exceptionally high certainty.

This level of certainty can be assessed by whether the asset’s price deviates from its fair value by a factor of two or more.

5. Fraud is also unavoidable.

The likelihood of fraud occurring in U.S. capital markets is relatively low, but fraudulent activity can never be entirely eliminated; thus, all markets carry risk.

You must guard against fraud. The best safeguards are due diligence and diversification, which help contain exposure to the level of risk associated with a specific asset class (equities or bonds) or a particular manager.

6. We need to mitigate volatility.

Over time, the impact of annual volatility on a portfolio grows geometrically, and most investors tend to significantly underestimate this effect. Portfolio volatility can be measured by calculating the standard deviation of annual returns.

Volatility arises from frequently fluctuating market prices. Losses, on the other hand, result from realized transactions or irreversible capital impairments.

A lack of understanding of compounding and how to adjust for annual volatility may be the primary cause of principal loss. Managing volatility requires distinguishing between expected market returns and risk (beta returns)—a risk that stems from overly active pursuit of excess returns and risk (alpha returns).

7. Adversity can be a gift

Recovering effectively from losses demands as much effort as managing risk prudently. Many senior decision-makers may remain paralyzed for extended periods after incurring losses—often far longer than necessary for recovery.

Worse still, they may abandon their previously held—but now challenged—investment convictions and consequently miss opportunities to stage a comeback.

Our experience confirms behavioral finance’s early findings regarding 'interrupted rationality' and rational decision-making, as well as its insights into the relevance of governance structures in maintaining investment discipline.

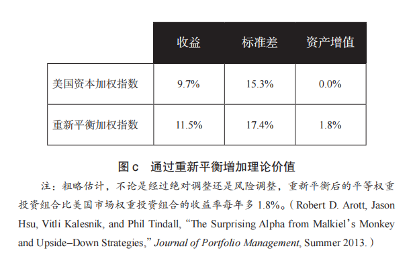

Recovering from losses by rebalancing the portfolio to adhere to the established investment strategy is critical to achieving superior long-term performance. The importance of adjusting portfolio weights through rebalancing to benefit from market volatility is illustrated below:

8. It is difficult for ordinary investors to beat the market, but experts may be able to

Under expert guidance, active management tends to outperform passive management. Passive approaches to investing in market assets are more suitable for inexperienced retail investors.

When formulating a passive investment strategy, investors should pay attention to valuation to avoid buying at elevated prices. If you are dealing with a niche market where competition is constrained by regulation or other factors, an active management approach may yield greater benefits.

In certain markets, persistent and pronounced segmentation creates pricing anomalies—precisely the conditions that experienced, non-dogmatic investors, unencumbered by rigid governance rules or other constraints (some of which are self-imposed), can exploit.

The high-yield bond market is one example, but other markets also suffer from fragmented supply and demand that prevent prices from reaching equilibrium. The mergers and acquisitions market has experienced sustained fragmentation, as has the emerging technology market.

Because unconstrained investors or 'preferred' intermediaries can acquire these assets at relatively modest discounts, such assets can confer a medium- to long-term advantage.

The term 'preferred' intermediaries refers to institutions capable of providing a competitive edge for the future of the assets—through communication and coordination in asset management or specialized management expertise.

In addition to high-yield bonds and hedge funds, private equity and venture capital are also highly fragmented markets. In such markets, many 'preferred' intermediaries can secure pricing advantages.

9. Alpha Lies in the Details

Another simple yet effective way to generate alpha is to 'unpack' the risks you encounter.

For example, a manager’s stock-picking skill may be obscured by a large cash holding (which should have been deployed to take advantage of investment opportunities when they arose).

Using equity futures to hedge the cash exposure—without restricting the manager’s trading discretion—increases market risk exposure.

Some investors may mistakenly dismiss such a manager unless the manager stops holding substantial cash reserves, as this would obscure the manager’s ability to execute decisive trades.

10. Beware of Bad Apples

In many cases, poor governance inflicts greater damage on a portfolio than poor managers do. Markets and managers can recover from cyclical losses (reverting to the mean), but portfolios impaired by flawed governance decision-making processes find it far more difficult to recover from such losses.

Poor governance structures within boards or investment committees typically manifest as follows:

• Frequent turnover of managers.

• Frequent changes in committee membership or staff.

• Overreliance on practices that appeared effective over the past three to five years.

• Sustained negative or zero growth over the past seven years.

• Managers are dismissed due to short-term underperformance.

• Criteria for hiring and firing managers are overly simplistic.

• The process of selecting managers resembles a continuous beauty contest.

• Asset classes are categorized in vertical silos, an approach that overlooks cross-asset investment opportunities.

• Management costs are disproportionately high relative to asset appreciation.

• Conflicts of interest exist among fiduciaries.

In the face of global economic volatility, maintaining consistent portfolio growth remains a formidable challenge for investment institutions and investors alike. Hilda’s ten investment principles may offer valuable guidance in navigating today’s evolving investment landscape.

Editor/Jayden