Wednesday’s upcoming CPI release is expected to approach 4.2%, bond markets have already priced in a rate hike, yet Trump is loudly calling for cuts—the first FOMC meeting under new Fed Chair Kevin Warsh has become a decisive battleground among these three forces.

The wording of the policy statement, the trajectory of the dot plot, and shifts in risk distribution—these three signals will simultaneously reveal whether he can hold the Fed’s last line of defense for central bank independence between White House pressure and market credibility.

Kevin Warsh, the newly appointed Chair of the Federal Reserve, is facing his most challenging policy test since taking office: inflation is expected to breach 4% this week, bond markets have already priced in expectations of rate hikes, and Trump has publicly pressured the Fed to cut rates just ahead of its policy meeting. The outcome of this three-way tug-of-war will determine whether Warsh can chart an independent policy course between White House preferences and market credibility.

The U.S. Consumer Price Index (CPI) for May will be released this Wednesday, with market expectations pointing to a year-over-year increase of 4.2%, up from April’s 3.8% and significantly above the Federal Reserve’s 2% policy target. Meanwhile, Friday’s robust May employment report triggered sharp declines in tech stocks and pushed bond yields higher, as market concerns about runaway inflation have shifted from mere expectations to tangible asset price pressures.

The U.S. Consumer Price Index (CPI) for May will be released this Wednesday, with market expectations pointing to a year-over-year increase of 4.2%, up from April’s 3.8% and significantly above the Federal Reserve’s 2% policy target. Meanwhile, Friday’s robust May employment report triggered sharp declines in tech stocks and pushed bond yields higher, as market concerns about runaway inflation have shifted from mere expectations to tangible asset price pressures.

In an interview with NBC’s 'Meet the Press' on Sunday, Trump stated explicitly: "There is no reason whatsoever to raise rates. We should actually be cutting them." He added, "Kevin is doing a great job, and I hope he follows his own judgment," but immediately followed up by saying that when a country is performing well, it "shouldn’t be punished with immediate rate hikes."

While offering Warsh considerable public deference, these remarks clearly conveyed the White House’s policy preference. The Federal Reserve will hold its next interest rate decision meeting on June 16–17, marking Warsh’s first FOMC meeting as Chair.

Inflationary pressure has become a 'settled issue.'

Market tolerance for inflation is rapidly narrowing. Robert Tipp, Chief Investment Strategist at PGIM, said on Monday: "Inflation is no longer a question—it is now an accepted reality." He noted that Fed officials had previously hoped inflation would subside on its own, "but that assumption has not materialized."

Energy prices are a key driver of current inflationary pressures. The conflict involving Iran has persisted for over 100 days, and oil prices have risen by approximately 60% year-to-date. Economists note that its impact is now more evident on inflation than on growth, reshaping the Fed’s policy calculus.

Neil Dutta, Head of Economic Research at Renaissance Macro Research, wrote in a client note on Monday that a 'preemptive rate cut' by the end of 2025 appears "unnecessary" in the current economic environment. He argued that short-end Treasury yields will continue to rise because "the labor market weakness that initially justified rate cuts now seems absent."

Bond markets are front-running the Fed—rate hike expectations are already priced in.

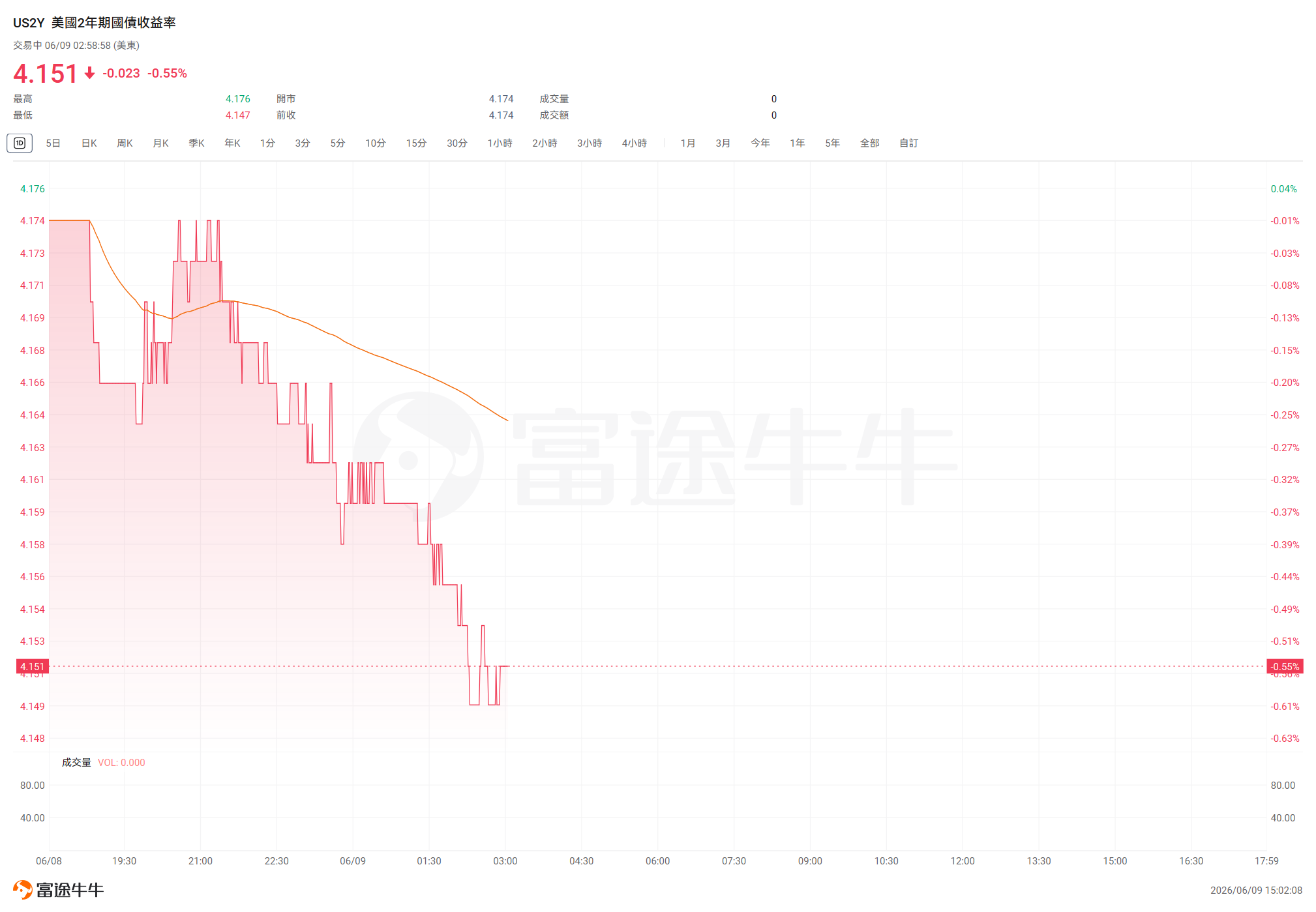

Bond markets have moved ahead of the Fed’s policy. The most rate-sensitive$U.S. 2-Year Treasury Notes Yield (US2Y.BD)$4.151%, above the Fed’s current policy rate ceiling of 3.75%.$U.S. 10-Year Treasury Notes Yield (US10Y.BD)$stood at 4.552%,$U.S. 30-Year Treasury Bonds Yield (US30Y.BD)$has rebounded above the 5% mark once again.

Tipp stated that the market would not resist the Fed’s approach of 'raising rates very gradually and prudently to ensure price stability,' as 'higher interest rates have already been partially priced in by the market.'

Brad Conger, Chief Investment Officer at Hirtle & Co., noted that if the Fed ultimately chooses to hike rates, longer-dated Treasuries could actually benefit. 'It would signal that the Fed is not unilaterally dovish,' he said, 'and the market would respond positively to that.'

The AI narrative has become the stock market’s last line of defense.

Despite elevated inflation and interest rate risks, equity investors remain firmly focused on artificial intelligence themes. On Monday, semiconductor stocks staged a broad rally,$Marvell Technology (MRVL.US)$up approximately 9.6%,$Micron Technology (MU.US)$up approximately 9.9%, with Samsung as a major holding.$iShares MSCI South Korea ETF (EWY.US)$rose by approximately 6%,$PHLX Semiconductor Index (.SOX.US)$gaining more than 5% overall, partially offsetting the decline triggered by Friday's employment data shock.

However, Conger remains cautious. 'Our biggest concern is the AI capital expenditure cycle,' he said. If yields on longer-dated Treasuries rise further, it would increase financing costs for AI infrastructure in debt markets—a challenge large tech firms have only recently begun addressing by considering equity financing as a supplement. 'Given the intensity of current sentiment, even minor developments could shift the narrative from euphoria to a rush for the exits,' he added.

Waller’s Debut: Three Signals Will Determine Policy Shift

Michael Gapen, Chief U.S. Economist at Morgan Stanley, remarked, 'One key outcome of the meeting will be assessing how closely Waller aligns with hawkish views.' Analysts will closely monitor three dimensions: whether the policy statement removes language indicating a 'dovish bias,' whether the dot plot reflects expectations for rate hikes, and whether the risk balance tilts toward inflation concerns. If all three signals emerge simultaneously, it would mark a significant pivot away from the Fed’s easing cycle that began in late summer 2024.

Fed officials have now entered their blackout period. Following the release of the statement on June 17, Waller will hold his first press conference since assuming office. Markets also anticipate that he will deliver clear signals regarding reforms to the Fed’s communication framework—a central pledge during his campaign for the Fed chairmanship.

Waller can no longer avoid the decision before him: his inaugural policy statement—balancing inflation data, bond market pressures, and White House expectations—will serve as the first test of his independence in the eyes of observers.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/melody