Caitong Securities analysts noted that the stronger-than-expected nonfarm payroll data reflects a 'temporary distortion' driven by the approaching World Cup boosting the services sector. Currently, the U.S. economy faces severe K-shaped divergence, wage growth is slowing, and purchasing power has turned negative—fundamentals in the real economy cannot withstand further rate hikes. The market may be 'spooking itself,' while the foundation of the tech-driven bull market remains intact.

A stronger-than-expected nonfarm payrolls report has pushed market concerns about a Federal Reserve rate hike to new highs—but this panic over tightening liquidity may largely be the market scaring itself.

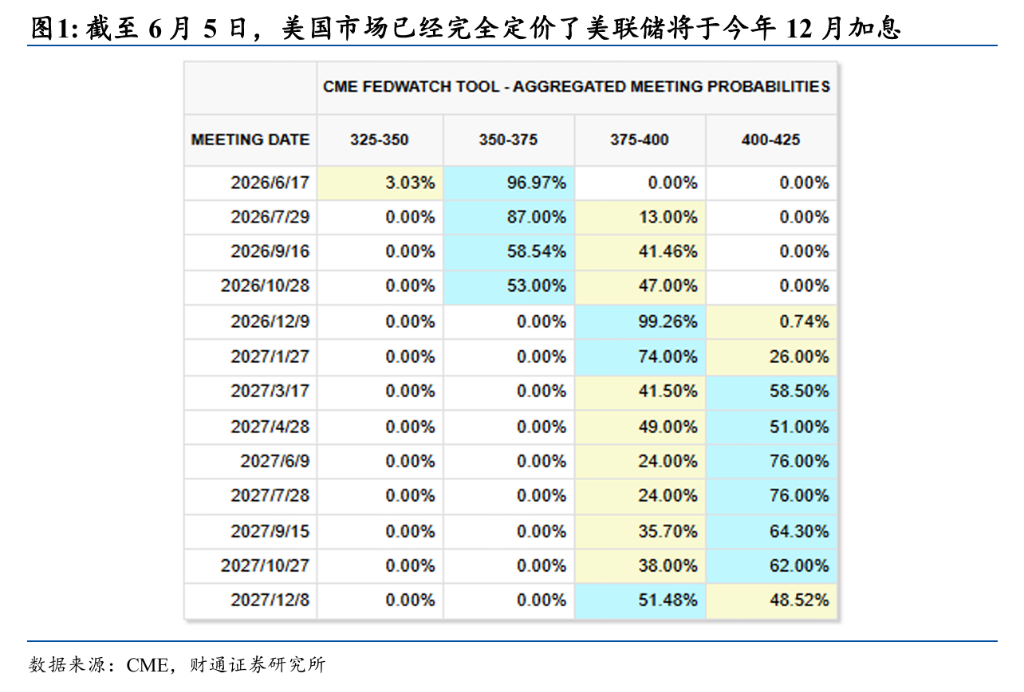

On the evening of June 5 Beijing time, the U.S. Bureau of Labor Statistics reported that nonfarm payrolls increased by 172,000 in May, far exceeding the market expectation of 85,000. Following the release, CME FedWatch indicated that derivatives markets had fully priced in a Fed rate hike starting in December this year. Liquidity-sensitive assets were immediately hit hard: the 10-year U.S. Treasury yield rose by 8.1 basis points in a single day to 4.55%, the Nasdaq index fell by 4.2%, and London spot gold dropped by 3.25%.

In a report dated June 9, Zhang Wei, an analyst at Caitong Securities, argued that the stronger-than-expected nonfarm payroll growth exhibited clear structural peculiarities and should not be interpreted as a signal of broad-based economic overheating. Meanwhile, the U.S. economy continues to experience pronounced K-shaped divergence, and inflation expectations in the real economy show no signs of de-anchoring—conditions that do not meet the prerequisites for triggering a rate hike. Caitong Securities believes that the immediate priority for new Fed Chair Kevin Warsh is to maintain nominal interest rate stability; before advancing broader monetary discipline objectives, he must first play the role of a 'steady anchor' in the short term.

In a report dated June 9, Zhang Wei, an analyst at Caitong Securities, argued that the stronger-than-expected nonfarm payroll growth exhibited clear structural peculiarities and should not be interpreted as a signal of broad-based economic overheating. Meanwhile, the U.S. economy continues to experience pronounced K-shaped divergence, and inflation expectations in the real economy show no signs of de-anchoring—conditions that do not meet the prerequisites for triggering a rate hike. Caitong Securities believes that the immediate priority for new Fed Chair Kevin Warsh is to maintain nominal interest rate stability; before advancing broader monetary discipline objectives, he must first play the role of a 'steady anchor' in the short term.

Notably, ahead of the Federal Open Market Committee’s decision announcement in the early hours of June 18 Beijing time, market concerns over liquidity are unlikely to dissipate quickly. Elevated volatility may persist, with further downside risks possible. However, from a medium-term perspective, neither the liquidity environment nor AI-driven industry trends have materially deteriorated, suggesting the tech bull market is not yet over.

The Illusion Fades: The 'World Cup Effect' Behind the 172,000 Nonfarm Payroll Gain

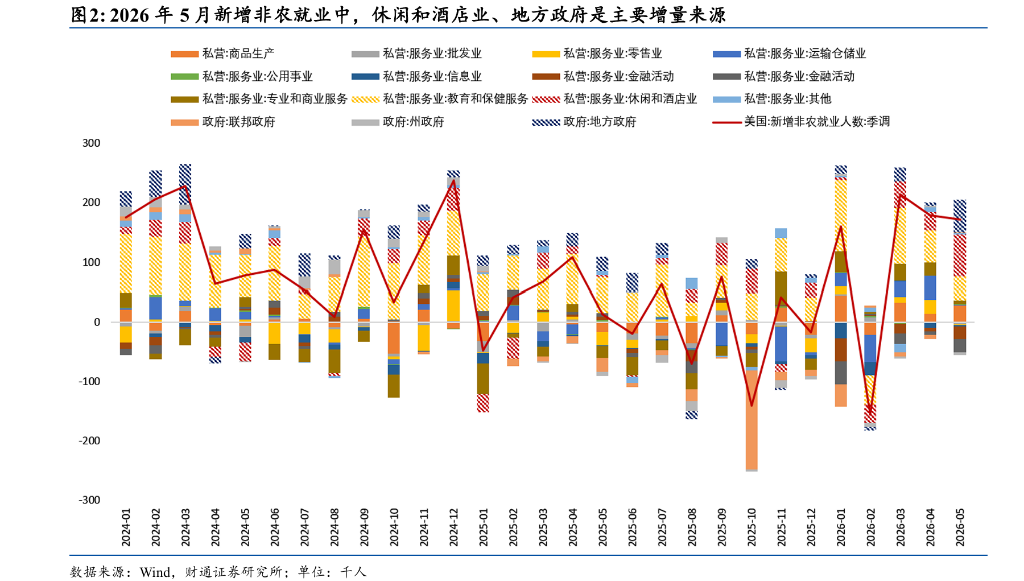

Although the addition of 172,000 nonfarm jobs in May appears impressive at first glance, structural analysis reveals significant short-term distortions. Caitong Securities noted that this employment gain was heavily concentrated in leisure and hospitality (up 70,000) and local government (up 55,000), which together accounted for the vast majority of the increase.

The sharp rise in leisure and hospitality employment is closely tied to the upcoming FIFA World Cup. Hosted jointly by the United States, Canada, and Mexico, this year’s tournament—kicking off on June 11 U.S. time—has expanded from 32 to 48 teams, increasing total matches from 84 to 104. Of these, 78 matches—including the quarterfinals, semifinals, and final—will be held across 11 U.S. cities. The imminent large-scale event has inevitably driven a temporary surge in labor demand in restaurants, hotels, and related service sectors.

Caitong Securities contends that this portion of job growth lacks sustainability, and a preliminary assessment of employment trends will require waiting until after the World Cup concludes. Interpreting this data as evidence of broad labor market strength—and thereby inferring the necessity of a rate hike—is fundamentally unsupported by the underlying numbers.

A Fragile K-Shaped Economy: The Real Economy Simply Cannot Withstand a Rate Hike

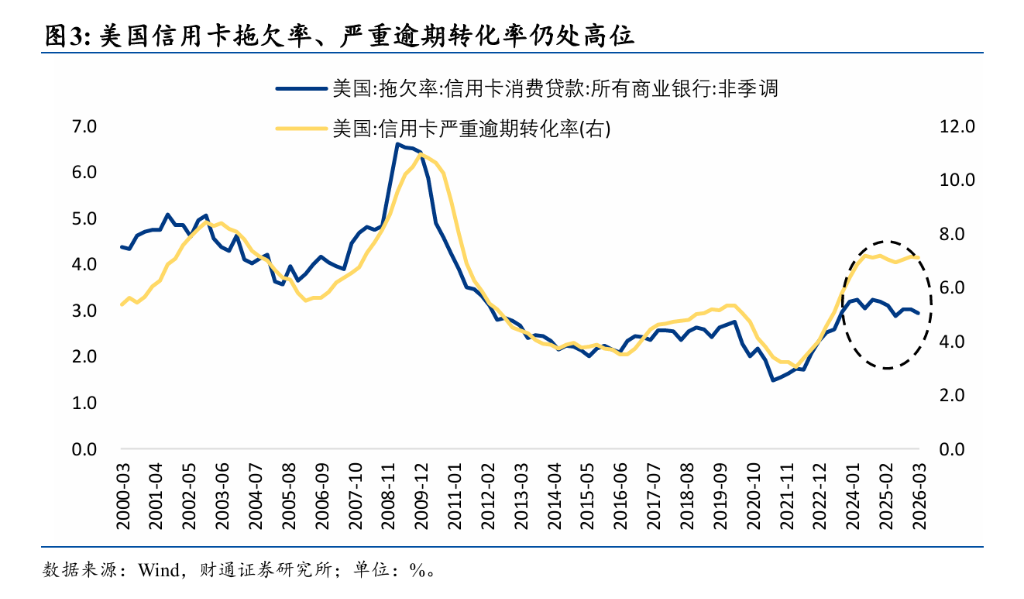

Even setting aside the idiosyncrasies of the nonfarm payroll data, the U.S. economy as a whole is far from a point where rate hikes would be warranted to curb overheating. According to Caitong Securities, the K-shaped economic divergence remains severe—aggregate indicators appear stable, but structural pressures continue to accumulate.

On the credit front, the credit card delinquency rate remained at 2.95% in Q1, while the serious delinquency conversion rate reached a high of 7.12%, both standing at post-pandemic highs. In the housing market, annualized new home sales in April totaled 622,000 units and existing-home sales reached 4.02 million units—both below pre-pandemic levels and showing no meaningful rebound since the Federal Reserve began its easing cycle in September 2024.

Divergence in durable goods consumption is equally pronounced. Bolstered by AI-driven trends, electronics and appliance sales rebounded from a year-over-year growth rate of 3.1% in November last year to 7.6% in April this year. However, sales of automobiles, household appliances, and home furnishings continued to decelerate or even turned negative, declining by 1.4% and 3.6% year-over-year in April, respectively.

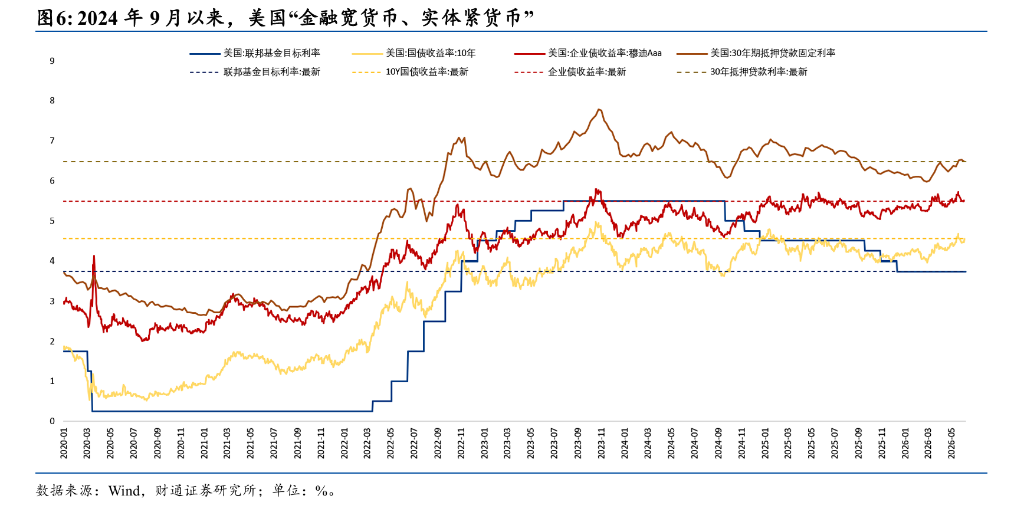

This pattern of 'easy monetary conditions in financial markets but tight financing in the real economy' lies at the heart of K-shaped divergence. The Federal Reserve’s six rate cuts since September 2024 have failed to meaningfully lower financing costs for the real sector, and the spillover effects of the AI boom have yet to reach interest-rate-sensitive traditional sectors. This suggests that the core issue facing the U.S. economy today is structural fragility—not broad-based overheating.

Inflation expectations remain anchored; conditions for rate hikes are absent

From an inflation standpoint, the Federal Reserve also lacks justification to initiate rate hikes. The Fed’s core inflation assessment framework hinges on two criteria: whether inflation exhibits a sustained upward trend and whether long-term inflation expectations show signs of de-anchoring. Neither condition is currently met.

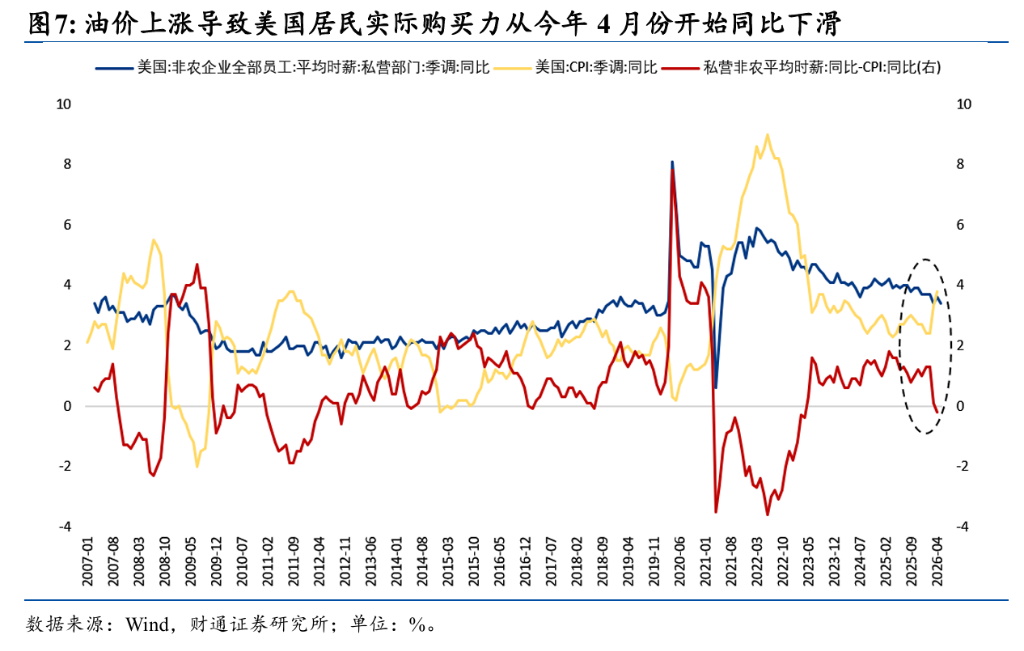

A wage-price spiral has not emerged: Year-over-year growth in private-sector hourly earnings declined from 3.7% in December 2025 to 3.6% in April and further to 3.4% in May this year.

Real purchasing power has turned negative: Driven by rising oil prices following the outbreak of the U.S.-Iran conflict, the U.S. CPI rose 3.8% year-over-year in April (up 1.1 percentage points from December 2025). Subtracting CPI growth from hourly wage growth, real purchasing power for U.S. households turned negative in April (down 0.2% year-over-year), a sharp decline of 1.2 percentage points from December 2025.

Inflation expectations remain firmly anchored: The New York Fed’s May survey showed median consumer inflation expectations at just 3.46% for the 1-year horizon and 3.13% for the 3-year horizon (even slightly below levels during the tariff tensions of April last year), with the 5-year expectation at 3.02%. There are no signs of panic-driven stockpiling—a typical precursor to runaway inflation—in the real economy.

The Fed’s true mandate: Stabilize rates, not tighten

Taken together, the Federal Reserve’s most critical task at present is neither to curb excessive demand nor to combat inflation, but rather to maintain relative stability in nominal interest rates.

On one hand, K-shaped divergence has also extended into capital markets—valuations of technology stocks are highly sensitive to interest rates, as are credit and consumer activities in traditional sectors of the economy. The more fragile the structure, the greater its reliance on a stable interest rate environment. On the other hand, even if the Federal Reserve were to actually raise rates, the tightening impact would fall primarily on the interest-rate-sensitive lower segment of the K-shaped economy (such as consumption and real estate), without curbing the expansion of the AI sector. Such a move would effectively force an already vulnerable economic base to subsidize AI-driven prosperity, thereby further exacerbating structural imbalances. Moreover, if the AI industry’s momentum itself weakens and its spillover effects fail to materialize, the K-shaped economy would begin converging downward from its upper segment, rendering any rationale for rate hikes even less compelling.

Caitong Securities therefore concludes that before Walsh can realize his long-term vision of restoring fiscal and monetary discipline and rebuilding confidence in the U.S. dollar, he must first stabilize the current situation in the near term. Indeed, if capital markets continue driving up nominal U.S. Treasury yields based on unreasonable expectations, the Fed might even need to issue dovish signals—or potentially cut rates—to correct market distortions.

Consequently, the market’s current expectations of rate hikes are largely self-induced fears, and liquidity conditions will not experience substantive tightening. Ahead of the Federal Reserve’s policy decision announcement on June 18, concerns over liquidity could continue weighing on market sentiment, warranting caution against short-term volatility and correction risks. However, viewed over a longer horizon, neither the liquidity environment nor the trajectory of the AI industry has fundamentally changed, leaving the foundation of the tech bull market intact.

Editor/Deng