Source: Thought Steel Imprint

Volatility = Risk? Volatility = Return?

1. It is not the wind that moves, but the mind.

Fund A has a long-term annualized return of 15%, but frequently experiences drawdowns exceeding 20% during market corrections; Fund B has a long-term annualized return of 10%, but its drawdown never exceeds 5% during any market correction. Which fund do you consider better?

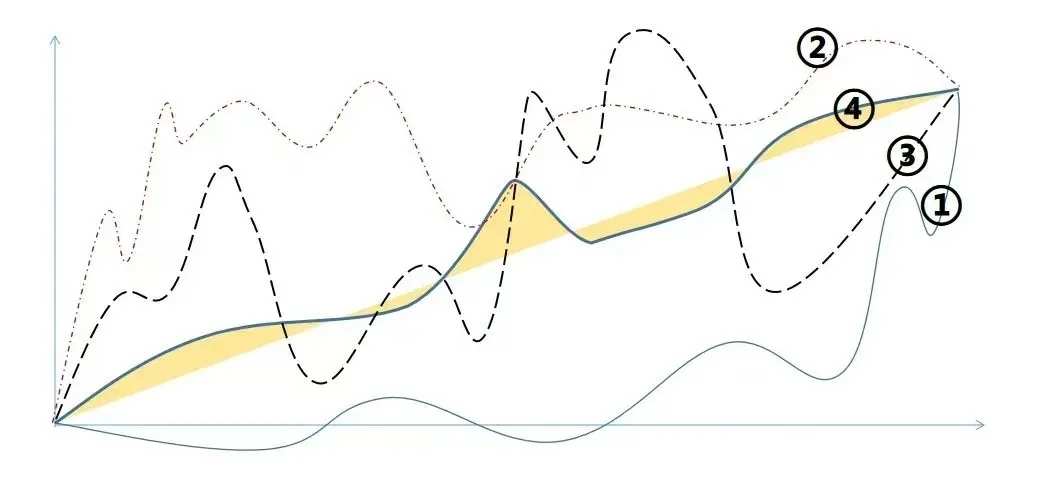

This question resembles the chart below, which I have cited in several previous articles: multiple stocks deliver identical returns, yet ordinary investors find it easier to profit from those with lower volatility.

This question resembles the chart below, which I have cited in several previous articles: multiple stocks deliver identical returns, yet ordinary investors find it easier to profit from those with lower volatility.

Volatility is an issue often overlooked—most investors focus solely on direction, yet many who correctly anticipate market direction still incur losses due to volatility.

Many view 'withstanding volatility' as a psychological trait separate from analytical investment skill—'It is not the wind that moves, nor the banner; it is your mind that moves.' However, in academic circles, volatility is not an abstract matter of sentiment but a concrete form of risk.

Of course, many experienced investment masters oppose the notion that volatility equates to risk. Their views fall into two camps: one holds that volatility is neutral, while the other contends that volatility itself is the source of returns.

Understanding the intrinsic value of a business or asset makes you a competent analyst; only by grasping asset volatility can you become an exceptional investor. This article dissects the concept of 'volatility' across several dimensions.

2. Academic Perspective: Volatility = Risk

The Sharpe ratio—the gold standard for evaluating fund performance—asserts that returns alone are insufficient; one must also assess the level of risk undertaken to achieve those returns.

But how should risk be measured?

From the perspective of traditional financial investment theory, such as Markowitz’s Modern Portfolio Theory, risk is defined as the uncertainty of future returns, which manifests itself as price volatility.

Many people do not agree with equating 'volatility' with 'risk.' Volatility merely reflects temporary price movements, during which investors have not actually incurred losses. However, this view stems from an illusory perception—often associated with 'mean reversion'—created by the term itself. Volatility is assessed retrospectively, but at the moment when a stock price plunges, you cannot know whether it will continue falling or rebound.

At the end of 2013, $Kweichow Moutai (600519.SH)$ Suppose an investor confidently assured you that the company was only experiencing temporary difficulties, that the stock price was merely undergoing short-term volatility, and that both earnings and share price would recover in the future. This investor would undoubtedly demonstrate foresight. However, if he happened to encounter an urgent personal need for cash at that very moment, he would have no choice but to sell at RMB 80 (adjusted price) and bear the loss caused by this volatility.

Similarly, current holders of Moutai shares—even if the stock eventually fulfills their expectations and replicates its stellar performance between 2015 and 2021—will still be forced to sell at today’s prevailing price if they urgently need cash now.

Although investing concerns the future, trading occurs in the present: what appears as a mere process when viewed from the future is, in fact, a definitive outcome when viewed from the present.

Thus, when quantifying risk, the Sharpe ratio uses the standard deviation of historical return volatility. Standard deviation is a statistical measure: if two stocks deliver identical returns, but Stock A exhibits higher volatility than Stock B, Stock A is deemed riskier.

For example, if a fund generates an annualized return of 15%, the risk-free rate is 3%, and the standard deviation of its returns (volatility) is 12%, then its Sharpe ratio is 1, indicating that for every 1% of risk assumed, the fund delivers 1% of excess return.

$Alibaba (BABA.US)$ The volatility over the past 52 weeks is $NetEase (NTES.US)$ twice that of NetEase, you would need to analyze and estimate that Alibaba’s expected return is twice that of NetEase; otherwise, the risk-reward ratio would not be favorable.

Whether or not you accept it, volatility equals risk: the greater the volatility, the higher the risk, and thus a higher expected return is required as compensation. This is the actual pricing principle for major asset classes in modern finance. Consider two examples:

Example 1: Dividend yields of high-dividend stocks are typically higher than bond yields—even for highly stable companies like Yangtze Power. This is precisely because stock price volatility is far greater than bond price volatility. To achieve the same ‘risk-adjusted return,’ Yangtze Power’s dividend yield must exceed the bond yield. The excess portion is called the risk premium, and its quantitative form is volatility.

Example 2: In the earlier example, Fund A has a long-term annualized return of 15%, but during market corrections, it frequently experiences drawdowns exceeding 20%. Fund B has a long-term annualized return of 10%, but during any market correction, its drawdown never exceeds 5%. If you were to calculate the average returns of all investors, you would find that Fund B’s investors achieve significantly higher average returns than those of Fund A.

Losses caused by volatility are very real. Historically, the average return for all investors in A-share funds is most likely negative, because high-return, high-volatility funds often experience ‘net subscriptions at peaks and net redemptions at troughs,’ whereas low-volatility funds may actually see net subscriptions during market lows.

The gap between investors’ actual returns and a fund’s stated annualized return is another manifestation of ‘volatility equals risk.’ Thus, uninformed retail investors focus solely on returns, while professional fund-of-funds (FOF) managers prioritize the Sharpe ratio.

However, Buffett has explicitly rejected the traditional investment view that ‘volatility equals risk.’

3. Practical Perspective: Volatility ≠ Risk

At the 2008 Berkshire Hathaway annual shareholder meeting, Buffett reiterated his view on volatility as risk: ‘When assessing risk, we consider volatility to be meaningless. The only risk that truly matters to us is the risk of permanent loss of capital.’

He explained:

You can find all kinds of good companies that exhibit high volatility and strong profitability, yet this does not make them poor businesses. Conversely, you can also find businesses with very low volatility that are, in fact, quite poor.

Value investing masters, including Howard Marks, have criticized the conventional view that equates volatility with risk, arguing that it oversimplifies reality for the sake of academic convenience.

However, Buffett did not say that 'volatility is not risk.' His point was that volatility is a neutral concept unrelated to risk.

This makes sense: Buffett cares only about a company’s intrinsic value. For long-term investors like him, short-term volatility is merely 'noise'—neutral and not a substantive threat, unless one is forced to sell at a low point.

In fact, Buffett’s understanding of volatility evolved over time. In his early 'cigar butt' phase—referring to buying deeply undervalued stocks of mediocre companies, where even one last puff would justify the price—he essentially profited from downward volatility.

Buffett has emphasized nearly every year in his letters to shareholders that his strategy is simply 'buying at low prices':

In his 1963 letter to shareholders, he wrote: 'Our business is to buy undervalued securities and achieve an average rate of return higher than that of the Dow Jones Industrial Average.'

In his 1965 letter to shareholders, he stated: 'We seek securities trading below their intrinsic value. The greater the margin of safety, the better we can withstand the market’s whims.'

In reality, the early Buffett did not regard volatility as neutral; rather, he saw it as a key source of returns. This principle remains central to multiple investment strategies.

4. Trading Perspective: Volatility = Returns

The notion that 'volatility equals return' should ultimately revert to the perspective that 'volatility equals risk.'

Underlying this perspective is the fact that a large number of investors dislike uncertainty and are averse to volatility—particularly large institutional capital. For instance, do you think sovereign wealth funds or national-level investment entities enjoy volatility? Do social security funds favor volatility? Do insurance funds welcome volatility?

Not only do such risk-averse institutional investors shun volatility, but high-net-worth individuals also tend to be more averse to return volatility than the average person. The psychology behind this is straightforward: wealthy individuals gain relatively little additional utility from earning even more money, whereas ordinary people often feel they have little to lose (though this perception is not entirely accurate) and believe—even correctly—that a modest increase in income could significantly improve their lives.

Due to the Pareto principle (the 80/20 rule), 80% of wealth is held by the top 20% of high-net-worth individuals. Consequently, asset pricing in practice reflects risk-averse characteristics: high-volatility risky assets typically trade at a 'discount.' For example, as previously mentioned, the dividend yield on equities exceeding bond yields implies that stocks are effectively trading at a 'discount' when viewed through the lens of bond-like intrinsic yields.

However, risk itself is objectively real. If subjective risk pricing exceeds objective reality due to risk aversion, it means a portion of the potential return from that risky asset is transferred from risk-averse investors to risk-seeking investors.

The risk one investor seeks to avoid is precisely the return another investor aims to capture—much like the famous line from Petyr Baelish in Game of Thrones: 'Chaos isn't a pit. Chaos is a ladder.'

Thus, 'volatility equals return' is simply the flip side of 'volatility equals risk.'

This form of profit transfer is known as volatility trading.

Risk is a 'commodity' that can be bought and sold. The most typical example is insurance: insurers earn premiums, while policyholders transfer a portion of their total asset returns to insurers in the form of those premiums.

Since volatility equals risk, 'volatility' itself can become a tradable 'commodity.' The most classic example is options.

The pricing of at-the-money options (where the stock price equals the strike price) is related to volatility. For two at-the-money options with identical expiration dates and strike prices but underlying different stocks, the option on the higher-priced stock typically reflects a higher historical volatility. This implies a higher payout ratio for the option buyer (analogous to an insured party), resulting in a higher option premium. Consequently, the option seller (analogous to an insurer) must charge a higher premium to cover the associated risk.

Among the Magnificent Seven, the pricing of at-the-money options (implied volatility) $Tesla (TSLA.US)$ is the highest, $NVIDIA (NVDA.US)$ followed by $Alphabet-C (GOOG.US)$ 、 $Amazon (AMZN.US)$ , then $Apple (AAPL.US)$and$Meta Platforms (META.US)$ , $Microsoft (MSFT.US)$ , with the lowest—precisely reflecting their differing historical volatilities.

Volatility is not some metaphysical concept akin to 'Is it the wind moving, the banner fluttering, or the mind stirring?' Rather, it represents tangible risk and return.

Based on differing attitudes toward volatility, investment strategies can be broadly categorized into two types: directional strategies and volatility-based strategies.

Among traditional equity investors—whether value investors or trend traders—although views on volatility vary (conservative investors dislike volatility, while value investors consider it irrelevant), direction remains paramount. An incorrect directional bet inevitably leads to losses, underscoring that volatility remains an objective source of risk.

However, many strategies generate returns that depend not only on direction but also on volatility.

The dollar-cost averaging (DCA) strategy, with which most investors are familiar, performs best when a "smile curve" emerges—prices first decline and then rise—and part of its return comes precisely from market volatility.

More focused on volatility than DCA is the mean-reversion-based "grid trading" strategy, which purely profits from price fluctuations. In this approach, directional movement is actually detrimental: upward breakouts result in missed opportunities, while downward breakouts lead to permanent losses. Hence, the ideal instruments for grid trading are convertible bonds, which have clear upside caps and downside floors.

In contrast to grid trading is "trend trading," a breakout-focused strategy where both direction and volatility matter equally. The essence of a 'breakout' is volatility constrained within a price range that suddenly expands once the price breaches that range. In commodity futures markets—where one can go long or short—the trader must first correctly identify the directional bias (bullish or bearish) and then assess the speed of the breakout. Getting both right leads to a 'KTV' (a euphemism for substantial profit); getting either wrong results in losses; and getting both wrong lands you in the 'ICU' (a euphemism for severe loss).

Trend trading is thrilling, but pure options traders regard directional bets as meaningless gambling. They seek returns solely from volatility and can use options combinations to hedge away directional exposure—even neutralizing delta (price sensitivity)—leaving only pure volatility exposure.

Even among strategies that trade volatility, risk and return profiles differ: grid trading prefers stable, moderate volatility—not too high, not too low—whereas options-based volatility strategies have distinct approaches for rising or falling volatility. What they fear most is stagnant volatility or misjudging the direction of volatility changes.

5. Volatility is the essence of the financial world.

First, let us recap the key points of this article:

Volatility itself is not risk; true risk lies in 'permanent loss.' However, volatility is the manifestation of risk: it triggers investors’ fear and behavioral biases, turning potential risk into realized losses—and creating profit opportunities for counterparties.

This gives rise to three perspectives on volatility:

Risk-averse investors equate volatility with risk and seek to avoid it.

Risk-seeking investors believe that volatility equals return and is something to be embraced.

Value investors view volatility as neutral, holding that investment risk stems solely from permanent losses caused by business operational risks.

All three perspectives can support profitable strategies; the key lies in understanding what is predictable and what is not:

Institutional investors, through multi-asset portfolios and robust research and analysis, believe returns are controllable, but investor sentiment is not—thus they opt to control volatility;

Investors seeking high returns believe they can manage their psychology amid prolonged losses and significant drawdowns and are willing to bet on both direction and volatility to achieve higher returns, thus embracing volatility more actively.

Value investors hold that market volatility is uncontrollable, while the ability to assess intrinsic business value can be improved, leading them to adopt a neutral and detached attitude toward short-term price fluctuations.

Regarding volatility itself, it is also essential to distinguish between what is predictable and what is not:

Some investors believe that predicting the magnitude of volatility is difficult, but its direction is relatively easier to anticipate—for example, according to the pendulum theory—leading to various timing strategies based on mean reversion and trend following;

Other investors contend that volatility direction is hard to predict, but changes in volatility levels follow discernible patterns, prompting them to design directionally neutral volatility trading strategies.

When it comes to leveraging volatility, one must also differentiate between what is predictable and what is not:

Some investors believe that when faced with market volatility, people exhibit certain inherent behavioral patterns—many of which constitute cognitive biases—and that numerous strategies have been developed to exploit these biases, colloquially referred to as 'harvesting retail investors.'

Other investors argue that precisely because of these behavioral biases exhibited in response to volatility, abundant trading opportunities are created; however, recognizing their own susceptibility to such biases, they have developed quantified strategies that are either automatically executed or even capable of autonomous learning.

Thus, volatility is not an anomaly but rather intrinsic to the financial world—it reminds us that the world is in constant flux and compels us to distinguish clearly between what we can control and what we cannot, as well as what we can judge and what lies beyond our judgment.

Editor/Jayden