Trump said a U.S.-Iran deal could be reached “within two or three days,” while the U.S. Energy Secretary noted that vessel traffic through the Strait of Hormuz is “increasing very significantly,” causing Brent crude to fall nearly 5%. U.S. stocks plunged during trading, with the Nasdaq 100 Index extending its losses to 3.22%, the Philadelphia Semiconductor Index dropping 7.25%, Marvell Technology falling over 13%, Arm Holdings declining 10.7%, and Lumentum down 10.6%.

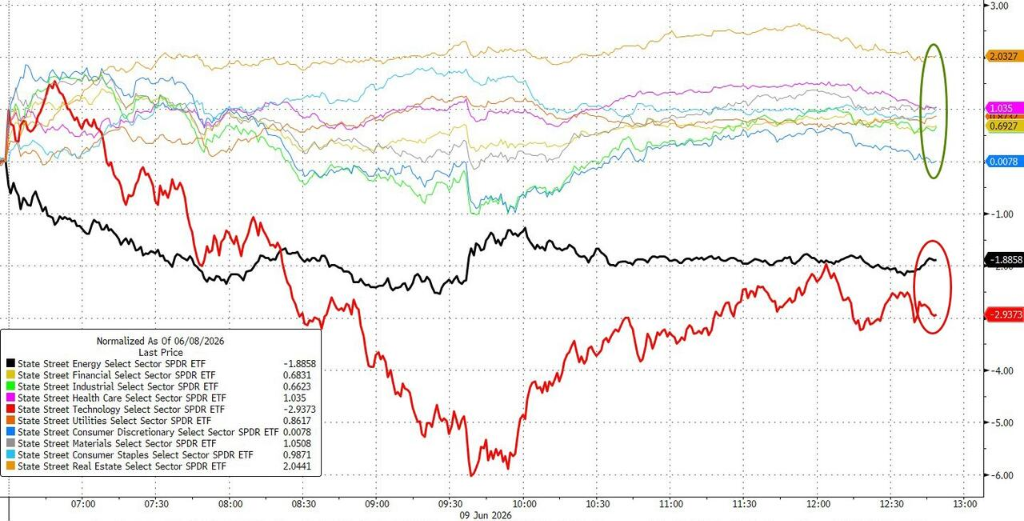

Technology stocks came under renewed pressure, prompting capital rotation into more economically sensitive and defensive sectors such as consumer goods. The selling pressure on tech stocks further weighed on gold and cryptocurrencies, while bonds and the U.S. dollar held up relatively well.

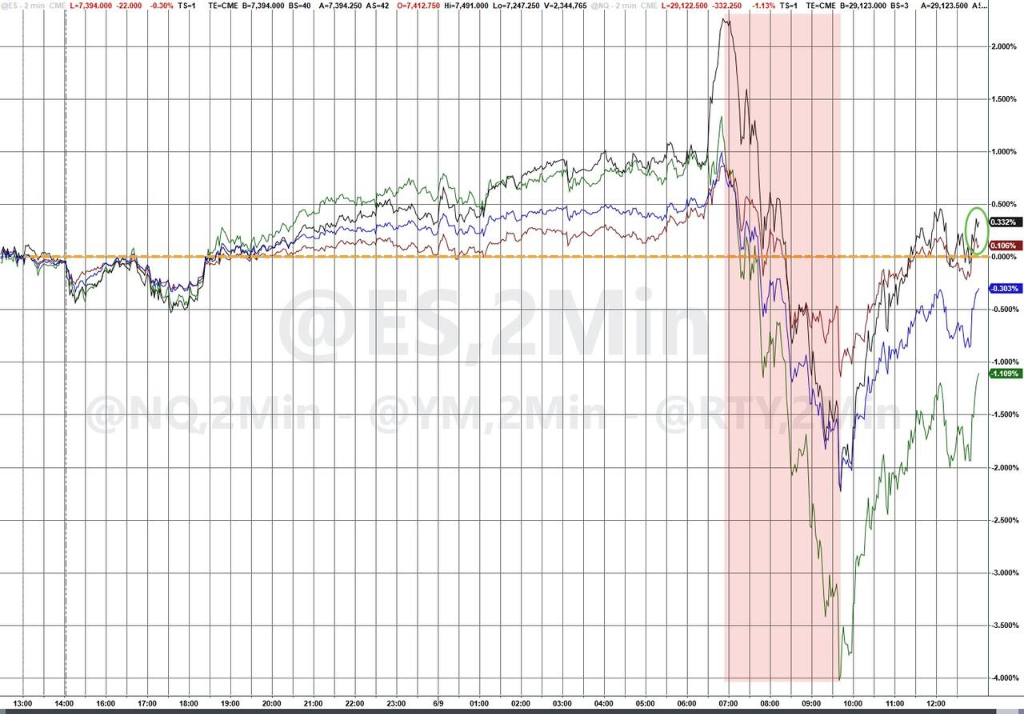

U.S. equities remained volatile on Tuesday, with the S&P 500 declining 0.3% and the Dow Jones Industrial Average posting a modest gain of 0.2%. Intraday volatility was pronounced, as the Nasdaq Composite plunged by nearly 4% at its lowest point, and the Philadelphia Semiconductor Index tumbled as much as 8.6% during the session.

Tuesday’s market decline lacked a clear single catalyst, but traders cited several potential explanations during the session:

Tuesday’s market decline lacked a clear single catalyst, but traders cited several potential explanations during the session:

Apple (AAPL) declined following its annual Worldwide Developers Conference (WWDC), which disappointed investors;

Broadcom’s large-scale special-purpose financing deal intensified market skepticism regarding the monetization path for AI;

Previously high-momentum technology stocks quickly retreated again after recouping Friday’s losses, creating a double technical setback.

AI-related sectors suffered broad-based declines. Goldman Sachs’ AI-themed basket fell by 427 basis points, the data center theme dropped 559 basis points, and the optical theme slid 800 basis points—deviating by 2.3 standard deviations from the mean.

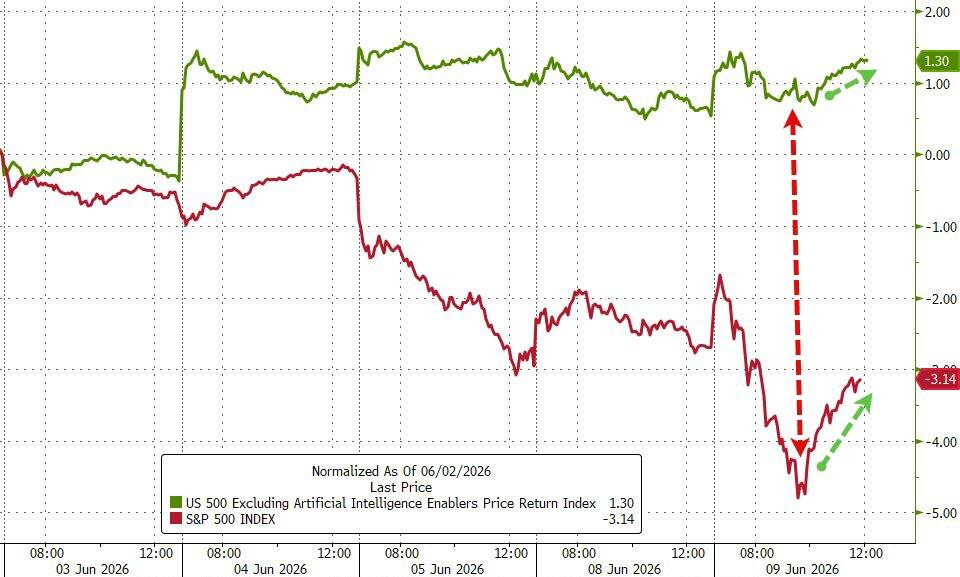

The ratio of Goldman Sachs’ S&P 500 basket excluding AI stocks to the S&P 500 index itself has moved above its 50-day moving average over the past five trading days, signaling that capital outflows from AI-themed assets are forming a trend.

The performance divergence between technology stocks and non-AI sectors has widened over the past five trading days to the largest gap since the trend began.

Existing home sales data released that day came in strong, which the market interpreted as a sign of improving consumer confidence, prompting capital flows from technology stocks into consumer-related sectors; only the technology and energy sectors posted declines.

The S&P 500 Equal Weight Index has also outperformed the market-cap-weighted index, indicating broadly positive market breadth.

Bloomberg macro strategist Michael Ball noted:

While a full-blown risk-off sentiment had not yet emerged by Tuesday, warning signs were already appearing—the one-sided nature of AI-driven momentum trades is fading, and dip-buying behavior is becoming more cautious.

Michael Ball further outlined a potential risk pathway through which sector rotation could evolve into systematic selling:

If the outperformance of the equal-weight index and defensive sectors persists, the broader market may absorb this rotation. The risk lies in the possibility that selling pressure among crowded ‘winner’ stocks becomes self-reinforcing, potentially triggering a wider market decline and ultimately evolving into a genuine correction.

Meanwhile, market attention has swiftly shifted to upcoming data releases and events: Wednesday’s U.S. May CPI report and this week’s SpaceX IPO.

SpaceX IPO approaches, raising concerns over 'portfolio reshuffling' amid new supply pressure

SpaceX’s impending IPO is viewed as a significant factor amplifying market volatility.

The IPO has received oversubscription from institutional investors, with orders several times the number of shares offered, targeting a valuation as high as $1.75 trillion and aiming to raise $75 billion—set to become the largest IPO in history.

Anthony Saglimbene of Ameriprise stated that while a transaction of this scale is positive in the long term, it raises a fundamental near-term question about funding sources:

Where will the money come from? Some of the demand could stem from cash on hand, and some from new retail participation, but institutional investors engaging in trades of this scale may also need to trim existing positions—particularly those 'winner' stocks that have already accumulated substantial unrealized gains.

Bret Kenwell of eToro also noted:

While the leadership of tech stocks is certainly welcome, a broader-based rally extending into other sectors would be more constructive. When market leadership remains concentrated in just one corner of the tech sector, the foundation of the market becomes more fragile.

Some strategists remain optimistic about the market cycle. Robert Edwards of Edwards Asset Management views the upcoming wave of large IPOs as 'the adrenaline pushing the bull market toward its peak,' though it does not yet signal the arrival of euphoric sentiment.

Oil prices plunged and then rebounded sharply, with renewed tensions involving Iran once again disrupting markets.

Oil prices swung significantly on Tuesday. Early in the day, Trump stated that negotiations with Iran were 'in the final stages of a very, very good deal,' which pushed Brent crude lower and drove WTI crude below the $90-per-barrel mark at one point.

However, Trump later posted on social media that Iran had shot down a U.S. Apache helicopter patrolling the Strait of Hormuz and declared, 'America must respond,' causing oil prices to surge immediately thereafter.

Iran then issued further statements warning that 'foreign military forces near Iran face risks,' prompting oil prices to climb even higher for a time.

Nevertheless, WTI crude futures closed down more than 3% at around $88.50 per barrel, retreating to levels last seen in early May, making the energy sector one of the worst-performing segments of the stock market that day.

In post-market commentary, Rich Privorotsky, head of Goldman Sachs’ Delta Desk, noted that the oil market currently appears to be in a brief stalemate between Iran and Israel. Physical markets are being weighed down by weak Asian demand, releases from strategic reserves, and rerouted shipping routes, resulting in a dynamic equilibrium.

He stated:

I don't believe this is a sustainable equilibrium. At some point, inventories, freight rates, or physical availability will begin to send warning signals.

U.S. Treasuries remained relatively stable, while gold and Bitcoin faced synchronized selling pressure.

U.S. Treasuries stayed relatively calm amid stock market volatility, with yields edging slightly lower. The 10-year Treasury yield declined by 4 basis points to 4.52%, while the 30-year yield retreated to around 5.00%.

Monty Gandhi, interest rate strategist at SMBC Group, stated:

U.S. Treasuries benefited from short-covering, and were further supported by falling oil prices and market expectations of a mild core inflation reading on Wednesday.

Market expectations for a rate hike in 2026 have cooled slightly, but still fully price in at least one increase.

Precious metals and cryptocurrencies were simultaneously sold off, which the market interpreted as some investors seeking liquidity ahead of the anticipated SpaceX IPO pricing.

Spot gold fell 1.7% to $4,257.71 per ounce, breaking below its 200-day moving average and retracing toward March lows—the deepest drop below the moving average since November 2022.

Bitcoin briefly dipped below $60,000 during the session and closed down 2.3% at approximately $62,000.

The yen weakened again, with USD/JPY rising back above the 160 level, reigniting market concerns about potential intervention by Japanese authorities.

On Tuesday, the Nasdaq technology index in the U.S. stock market closed down nearly 1.5%, while the semiconductor index declined by more than 1.9%.

U.S. benchmark indices:

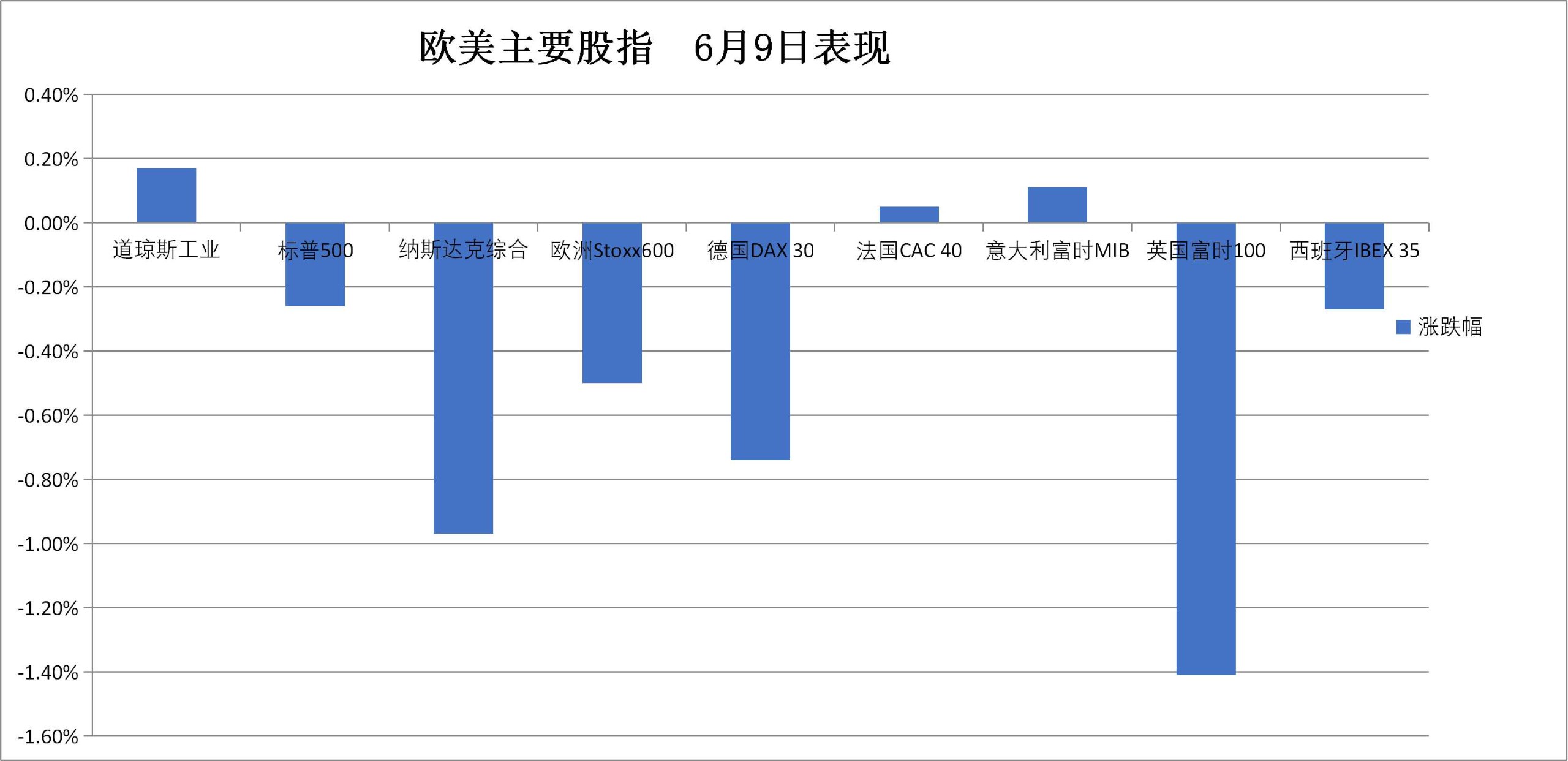

The S&P 500 Index fell 19.08 points, or 0.26%, closing at 7,386.65 points.

The Dow Jones Industrial Average rose 86.10 points, or 0.17%, closing at 50,872.11 points.

The Nasdaq Composite declined 250.841 points, or 0.97%, to close at 25,678.822 points. The Nasdaq 100 Index dropped 329.759 points, or 1.12%, ending at 29,084.499 points.

The Russell 2000 Index gained 0.41%, closing at 2,867.023 points.

The CBOE Volatility Index (VIX) rose 5.02%, closing at 19.87.

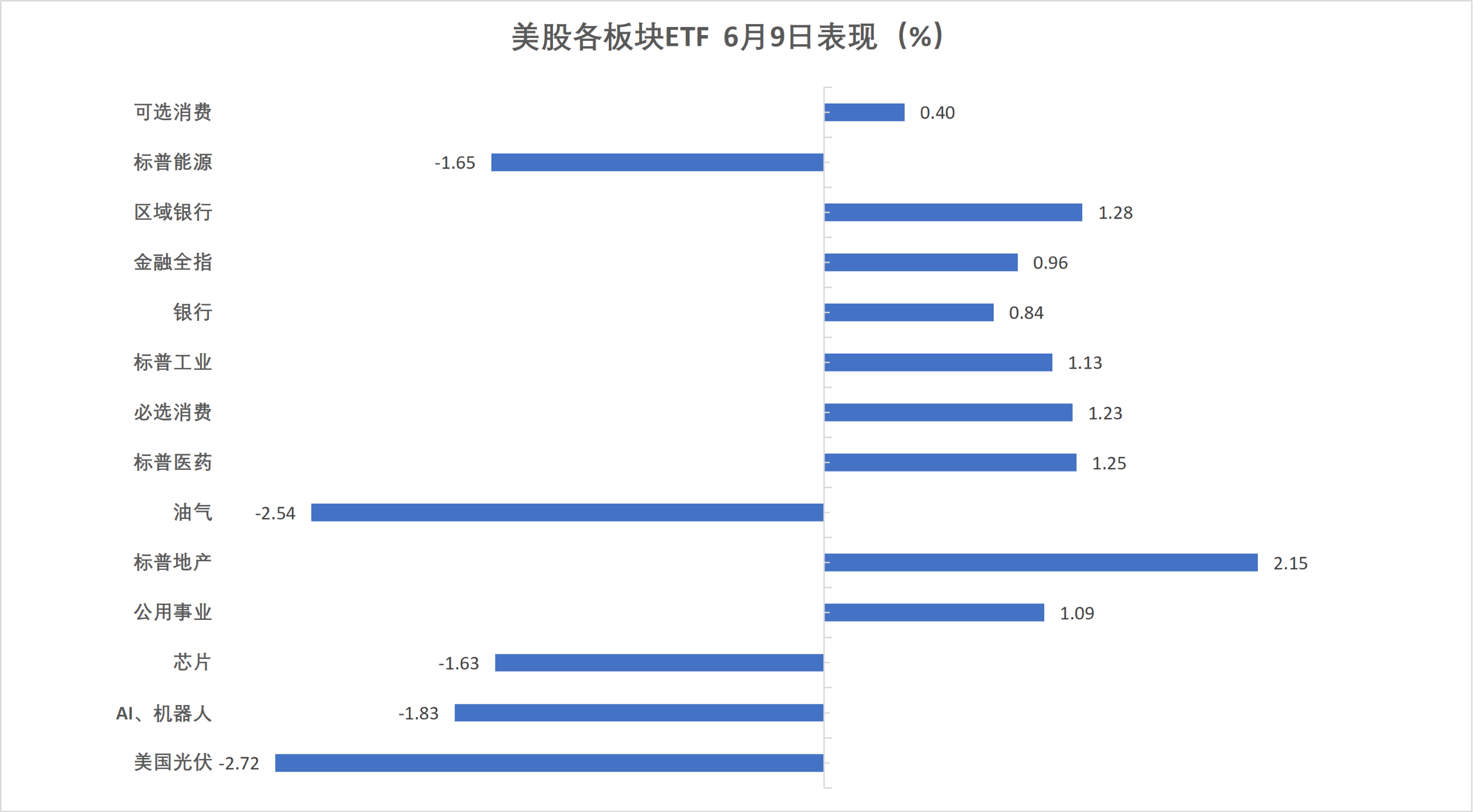

U.S. stock sector ETFs:

Most U.S. equity sector ETFs closed higher, with the Global Airlines ETF up 3.10%. Biotechnology, banking, healthcare, regional banking, consumer staples, and utilities ETFs rose by as much as 1.46%.

Mag 7:

The Wind U.S. Magnificent 7 Index declined 1.24%.

$Alphabet-A (GOOGL.US)$ up 0.26%, Meta down 0.14%, $NVIDIA (NVDA.US)$ down 0.22%, Amazon down 0.42%, Microsoft down 2.02%, Tesla down 3%, Apple down 3.64%.

Chip Stocks:

$PHLX Semiconductor Index (.SOX.US)$ closed down 248.883 points, or 1.93%, at 12,657.81.

Taiwan Semiconductor ADR up 0.26%, AMD down 3.02%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed down 0.39% at 6,298.64.

Among popular Chinese ADRs, $Pony AI (PONY.US)$ closed down 3.7%, $NIO Inc (NIO.US)$ , Li Auto down 2.7%, ASE Technology Holding down 1.4%, Meituan, NetEase, Baidu, and Tencent all up more than 1%.

Other individual stocks:

$Circle (CRCL.US)$ down 1.75%.

Gaming stocks rose against the broader market trend, $DraftKings (DKNG.US)$ rose more than 11%

European stocks closed down 0.5%, with Nokia falling about 7%, Standard Chartered and Ericsson dropping 6.3%, and STMicroelectronics declining more than 5.9%. The UK stock market closed down 1.4%, while Generali Group rose over 2% to a new record closing high, and BE Semiconductor Industries gained 2.2%, approaching its all-time closing high.

Pan-European stocks:

The pan-European STOXX 600 Index closed down 0.50% at 618.64 points.

The Eurozone's STOXX 50 Index closed down 0.21% at 6,049.74 points, having earlier hit an intraday high of 6,149.17 points during the initial U.S. trading session before sharply reversing course.

Major Stock Indexes Around the World:

Germany's DAX 30 Index closed down 0.74% at 24,433.06 points.

France's CAC 40 Index closed up 0.05% at 8,203.43 points.

The UK's FTSE 100 Index closed down 1.41% at 10,227.33 points.

Sector and individual stock performance:

Among Eurozone blue-chip stocks, Siemens Energy closed down 5.92%, Infineon fell 3.30%, Schneider Electric declined 2.61%, SAP dropped 2.15%, and Eni fell 1.60%, marking the fifth-largest decline.

Among all constituents of the STOXX Europe 600 Index, Nokia fell 6.99%, Hochtief AG dropped 6.48%, OMV declined 6.39%, Standard Chartered Group slid 6.31%, and Ericsson decreased by 6.27%.

International oil prices closed down by approximately 3%, as Trump's Energy Secretary noted an increase in vessel traffic through the Strait of Hormuz.

Crude Oil:

WTI crude oil futures for July delivery settled down $3.10, or 3.40%, at $88.20 per barrel.

Brent crude oil futures for August delivery settled down $2.80, or 2.97%, at $91.45 per barrel.

Abu Dhabi Murban crude oil futures declined 3.85% to settle at $88.36 per barrel.

Natural Gas:

NYMEX July natural gas futures settled at $3.14 per million British thermal units (MMBtu).

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Stephen