HSBC believes the key issue regarding the Strait of Hormuz may not be 'when it reopens,' but rather to what extent normal operations can be restored. If transit remains subject to long-term management, the crude oil supply gap could persist until 2027, potentially requiring oil prices to stay in triple-digit territory to suppress demand. While alternative pipelines can alleviate crude export bottlenecks, they cannot resolve transportation challenges for refined products and LNG. Inventories will continue to decline, but the notion of 'hitting bottom in a few weeks' is not the base case; the real pressure point may only emerge in the fourth quarter of this year.

$Brent Last Day Financial Futures (AUG6) (BZmain.US)$Oil prices have fallen by nearly USD 20 per barrel cumulatively since mid-May, as markets bet on a breakthrough in U.S.-Iran negotiations. However, a ceasefire is one thing; restoring pre-conflict freedom of navigation through the strait is another.

The latest research report from HSBC’s commodities research team, led by analyst Kim Fustier, poses a central question:

“Market discussions need to shift from when the strait will ‘reopen’ to what the state of restored transit will actually look like—and if managed transit persists, what constitutes a plausible ‘new normal.’”

Under this framework, if the Strait of Hormuz is neither fully closed nor fully open—but instead remains in a state of partial reopening over the long term—the oil market deficit could extend into 2027. If transit volumes fail to recover to at least 60% of normal levels, oil prices may need to remain in the triple-digit range (in USD) to rebalance the market by curbing demand.

Alternative pipelines can ease some of the pressure but cannot eliminate the problem entirely. Pipelines in Saudi Arabia and the UAE can reroute some crude exports around the Strait of Hormuz; however, refined products and LNG lack similarly straightforward alternative routes. Inventories are not an infinite buffer either. According to estimates, inventory drawdowns could continue through the summer and only approach so-called 'tank bottoms' in the fourth quarter.

A peace agreement does not equate to a full restoration of maritime passage.

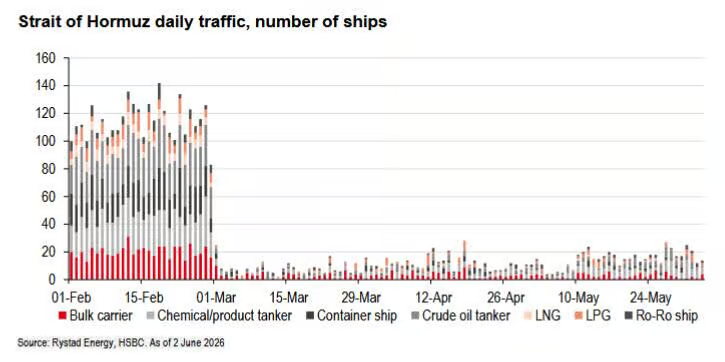

The market’s implicit pricing logic assumes that once the U.S. and Iran reach an agreement, transit through the Strait of Hormuz will revert to its pre-conflict state. Yet over the past several months, Iran has already established a management framework around the strait.

According to Xinhua News Agency, in May this year, Iran announced the establishment of the 'Persian Gulf and Strait Administration' to assert sovereign control over this waterway. Subsequently, on May 28, the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) imposed sanctions on the entity: even entering into a 'safe passage agreement' with Iran—without involving any payment—constitutes a violation of U.S. sanctions.

This has created a deadlock: transiting without payment carries risks, while paying violates U.S. sanctions.

There are already signs that some industry participants are coming to terms with this reality. In May, tankers from Saudi Aramco and Abu Dhabi National Oil Company (ADNOC) passed through the Strait; two Very Large Crude Carriers (VLCCs) bound for Japan successfully transited; a South Korean tanker made its first passage after coordination with Iran; and a Greek shipping company even publicly stated, 'If paying a fee facilitates transit, we would rather pay it.'

Daniel Yergin, Vice Chairman of S&P Global, described the current situation as: 'a gray zone—neither fully closed nor fully open.' Lloyd's List also noted that an increasing number of industry participants believe the pre-crisis state of free navigation may never be fully restored.

What might the Strait’s 'new normal' look like: oil prices may need to remain in triple digits as long as deficits persist

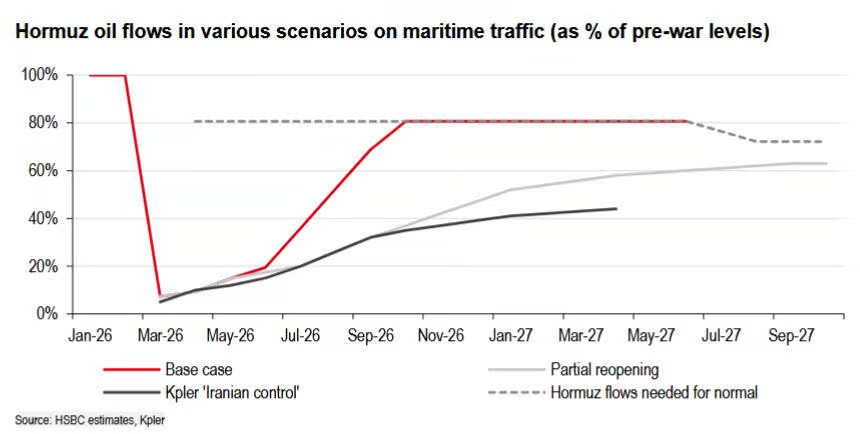

Analysts’ base case scenario assumes the Strait reopens by mid-June and linearly returns to normal levels over the following three and a half months. However, the study also presents an alternative ‘partial reopening’ pathway—in which Iran retains control, allowing only gradual and incomplete recovery of traffic flows.

For the crude oil market, Hormuz does not necessarily need to return to 100% capacity, as pipelines can absorb part of the flow. However, if the recovery ratio remains too low, the supply gap will still be difficult to contain.

Several third-party institutions have modeled this scenario as follows:

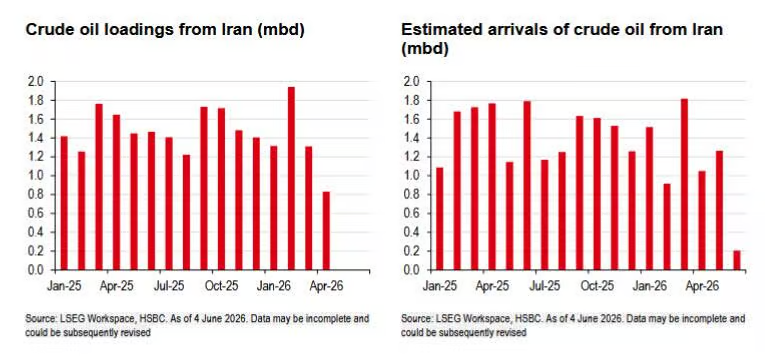

In its 'Iran-controlled' scenario published on April 29, Kpler projected that transit volumes could recover to 40% of prior export levels by the end of 2026 and stabilize at around 45% by the end of 2027. Friction would stem from approval procedures, mandatory routing through Iranian waters, and potential payments to Iran’s Islamic Revolutionary Guard Corps for passage.

In its 'narrow agreement' base-case scenario released on May 26, Rystad Energy forecast that crude flows through Hormuz would recover to approximately 10 million barrels per day (about two-thirds of pre-conflict levels) by the end of 2026, with an additional 5 million barrels per day rerouted via pipelines.

On June 3, Daniel Yergin, Vice Chairman of S&P Global, stated that Strait transit could become stuck in a 'gray zone—neither fully closed nor fully open.' U.S. sanctions on the 'Persian Gulf Strait Authority' could create a deadlock: without payment, transit becomes difficult or dangerous; yet shipowners fear U.S. sanctions if they do pay.

Lloyd's List’s assessment: pre-crisis freedom of navigation may not fully return. The eventual state could be an Iran-controlled 'managed strait,' featuring mechanisms such as identity checks, tiered access by nationality, and toll collection; with transit volumes recovering to roughly 60%–70% of pre-conflict levels.

This is the tipping point for oil prices.

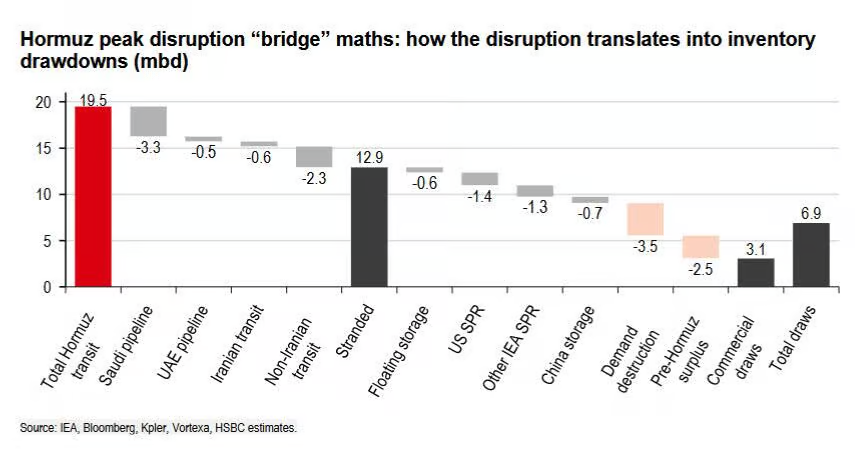

If recovery is only 40%–45%, the shortfall will persist until 2027. If Strait of Hormuz flows return to approximately 9 million barrels per day (bpd), and combined with alternative pipeline exports, total Gulf exports would reach about 14 million bpd—still leaving a gap of 5–5.5 million bpd compared to pre-war levels. Global inventories cannot decline indefinitely, implying that demand destruction must increase by an additional ~2 million bpd beyond the current 3–4 million bpd.

A 60% recovery would improve the situation but remain challenging. By mid-2027, if Hormuz flows rebound to 12 million bpd and are supplemented by alternative pipelines, total Gulf exports would reach 15–16 million bpd. In the second half of 2027, following the commissioning of the UAE’s pipeline expansion, total exports could rise further to 17.8 million bpd—but a deficit of approximately 2 million bpd would still remain.

Closing this gap requires either a portion of the demand destruction becoming permanent or faster supply growth—for example, accelerated production from U.S. shale.

Conclusion: As long as the market remains in deficit (i.e., recovery stays below 60%), oil prices must stay in triple digits to continuously suppress demand and drive market rebalancing.

Alternative pipelines are being expanded, but they cannot solve all the problems.

Gulf oil producers are not waiting passively for the Strait to reopen; instead, they are accelerating the expansion of onshore alternative routes:

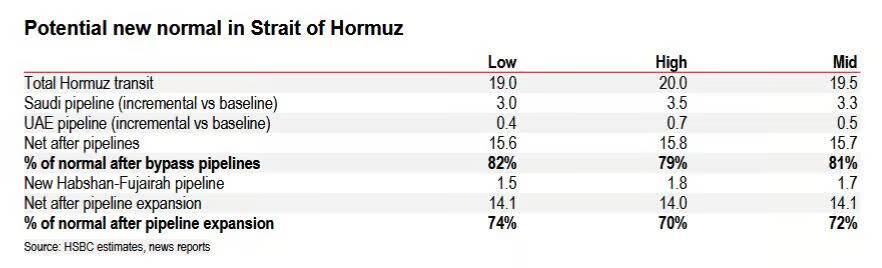

Saudi Arabia’s East-West Pipeline (capacity: 7 million bpd): Has been operating at full capacity since mid-March, enabling an additional 3–4 million bpd of exports via Yanbu Port on the Red Sea.

UAE’s ADCOP Pipeline (to Fujairah Port outside the Strait): Current capacity is 1.5 million bpd, but actual throughput has already reached 1.8 million bpd. On May 14, ADNOC announced an accelerated expansion plan targeting more than double the capacity—to over 3 million bpd—by 2027. The project is currently 50% complete.

Combined, these two pipelines offer structural capacity of approximately 5–6 million bpd. Analysts estimate that if Hormuz flows recover to 14 million bpd (roughly 70%–75% of pre-war levels) and both pipelines operate at full capacity—including the expanded ADCOP pipeline—most of the Middle East’s crude export capacity could be restored.

Moreover, additional projects are underway: Iraq is constructing a new 700–800 km pipeline with a capacity of 2.2–2.5 million barrels per day, extending from Basra to Haditha and then onward through Syria, Jordan, and Turkey for export to the Mediterranean; Kuwait is currently negotiating pipeline cooperation with Saudi Arabia and the UAE, as it currently has virtually no alternative routing options, and its oil exports have nearly reached zero.

However, there is a critical limitation: newly built crude oil pipelines can only address crude export issues and cannot resolve transportation challenges for refined products (gasoline, diesel, jet fuel) and LNG—these require dedicated infrastructure that pipelines cannot replace.

Inventory 'bottoming out' will not occur within a few weeks.

Inventories represent the second key driver in this pricing dynamic.

While some market participants believe global inventories are about to hit rock bottom, analysts’ estimates suggest a different timeline.

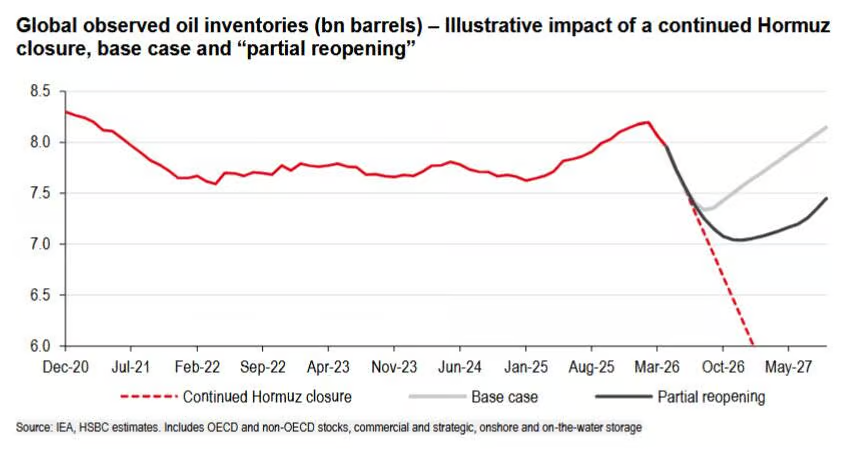

Observable global inventories are projected to decline from approximately 7.95 billion barrels in April to around 7.5 billion barrels in June and further to about 7.4 billion barrels in July—reaching their lowest level in over a decade.

Under the baseline scenario (full reopening of the Strait), global inventories would bottom out at approximately 7.3 billion barrels in August and begin recovering from September onward, ending the year about 630 million barrels below the February peak of 8.2 billion barrels.

In a 'partial reopening' scenario, global inventories would continue declining to roughly 7.0 billion barrels by December 2026—about 1.2 billion barrels below the February peak—and would not recover to June 2024 levels until September or October 2027.

Regarding the precise timing of the inventory trough, analysts have conducted calculations using the United States as an example: historically, the U.S. National Petroleum Council defined 300 million barrels as the 'minimum operating requirement' for crude inventories (approximately 78% of commercial inventories at the time). Applying the same ratio to current U.S. commercial crude inventories of 434 million barrels (as of the week ending May 29), the corresponding minimum would be approximately 337 million barrels. At the current drawdown rate, U.S. inventories would bottom out around October 2026, while global inventories would reach their trough around year-end 2026.

This stands in clear contrast to assessments by certain market participants:

Jeff Currie of Carlyle Group believes U.S. inventories could reach minimum operational levels by summer (July).

On May 28, Neil Chapman, Executive Vice President of Exxon Mobil’s upstream business, stated on CNBC that the world is “approaching unprecedentedly low inventory levels… we’ll get there in two or three weeks.”

On May 21, Fatih Birol, Executive Director of the International Energy Agency (IEA), stated: “If the situation does not improve, we could enter a red alert zone in July or August.”

HSBC’s stance is that inventories falling to the lower end of the five-year range do not in themselves constitute an “imminent crisis signal”; the real pressure point will not emerge until the fourth quarter of this year.

Demand destruction remains insufficient, and price pressures persist.

Demand-side responses have so far been relatively muted. OECD demand has declined only slightly, with weakness concentrated primarily in Asia (South and Southeast Asia) and the Middle East. U.S. gasoline and diesel demand is flat year-on-year, while Europe’s main road fuel demand has seen only a modest decline—largely driven by reduced petrochemical feedstock demand, which stems more from supply constraints than from price-induced factors.

Vitol estimates current demand losses at 4–5 million barrels per day, higher than the IEA’s previous estimate of 2–3 million barrels per day.

If the Strait of Hormuz remains under “partial control” for an extended period, the only path to market rebalancing will be for prices to rise sufficiently high—and remain so—to continuously suppress demand until supply and demand are realigned.

Editor/melody