Jefferies analysts raised their 2030 copper price target to $17,636 per tonne, the most aggressive forecast on Wall Street, stating bluntly, “We are not bullish enough on copper.” The rationale stems from accelerating demand driven by AI data center construction and grid upgrades, coupled with underperformance in supply from two major global mines. Goldman Sachs simultaneously significantly raised its copper price forecast, while JPMorgan and HSBC have also turned increasingly bullish.

Jefferies analyst Christopher LaFemina recently wrote in a note to clients: "It turns out we weren’t bullish enough on copper." He promptly raised his 2030 copper price target sharply to $8 per pound, equivalent to $17,636 per tonne—currently the highest copper price forecast on Wall Street.

For reference, the latest COMEX copper price is approximately $6.34 per pound, while LME copper trades around $13,583 per tonne. This means LaFemina’s 2030 target price is roughly 30% higher than current levels.

Before joining Jefferies, LaFemina spent over a decade covering metals and mining at Lehman Brothers and Barclays, making him one of Wall Street’s most seasoned metals analysts. In his report, he stated outright: "We currently hold the highest copper price forecast on Wall Street because we see robust U.S. industrial demand and persistently tight supply."

Before joining Jefferies, LaFemina spent over a decade covering metals and mining at Lehman Brothers and Barclays, making him one of Wall Street’s most seasoned metals analysts. In his report, he stated outright: "We currently hold the highest copper price forecast on Wall Street because we see robust U.S. industrial demand and persistently tight supply."

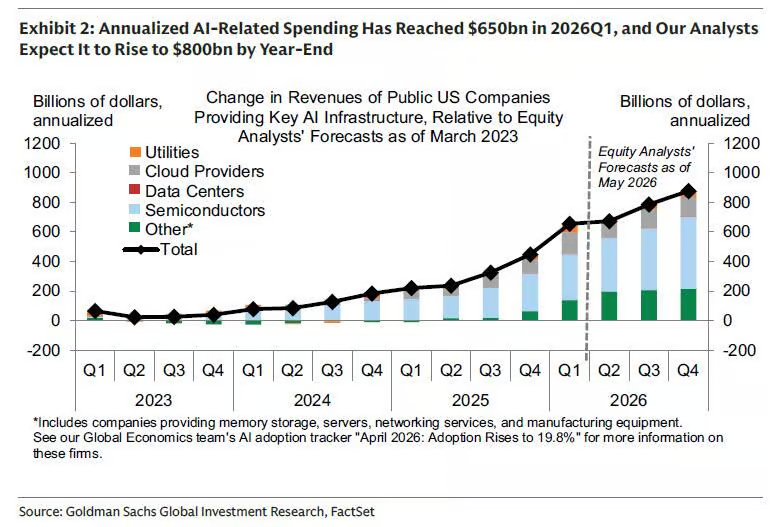

Copper is the clearest beneficiary of the AI spending boom.

LaFemina’s core thesis is straightforward: massive construction of AI data centers, coupled with what he calls the “powering up America” theme—grid and infrastructure upgrades—will drive a meaningful acceleration in copper demand.

Goldman Sachs previously estimated that hyperscalers’ AI-related capital expenditures will surge to $800 billion this year. These investments ultimately translate into physical infrastructure, for which copper remains an irreplaceable core material in power transmission.

LaFemina’s view is that copper—and aluminum—prices still have significant room to rise before they meaningfully weigh on the macroeconomic outlook.

Supply side: Two major mines falter simultaneously

Demand is one side of the equation; supply is the other. A team led by Goldman Sachs analyst Aurelia Waltham noted that the recovery in copper mine supply this year has clearly lagged expectations.

The firm lowered its 2026 global copper mine supply forecast by 350,000 tonnes, representing about 1.5% of total global mined supply. Of this, Indonesia’s Grasberg mine and the Kamoa-Kakula mine in the Democratic Republic of Congo together account for roughly 200,000 tonnes of the reduction, with both operations not expected to return to full capacity until 2028.

Meanwhile, U.S. copper imports in the first half of 2026 exceeded expectations, further tightening the supply-demand balance in markets outside the United States. Goldman Sachs now expects U.S. copper inventories to accumulate by 900,000 metric tons in 2026 (up from its previous forecast of 550,000 metric tons)—a result of companies front-loading purchases ahead of anticipated tariff implementation.

Goldman Sachs has therefore raised its LME copper price forecasts for end-2026 and the 2027 average to $13,735 and $13,800 per metric ton, respectively—significantly higher than its prior estimates of $12,465 and $12,150.

Goldman Sachs outlines three scenarios, with price ranges spanning from $12,600 to over $14,000.

The firm also presents three price scenarios, covering the key uncertainties currently facing the market:

Scenario 1: Continued blockade of the Strait of Hormuz. A decline in demand is roughly offset by supply reductions stemming from sulfur shortages, but a sharp contraction in global risk appetite could push LME copper prices down to a fundamental level of approximately $12,600,support level, before recovering upward thereafter.

Scenario 2: The U.S. announces copper tariffs (effective January 2027). If tariffs are announced in June 2026 and take effect in January 2027, companies will accelerate imports in the second half of 2026, driving copper prices above $14,000. However, once tariffs are formally implemented and imports cease, prices in 2027 would subsequently decline.

Scenario 3: A clear announcement that no copper tariffs will be imposed. Import demand fades, leading markets outside the U.S. back into surplus, and the average copper price in 2027 could fall to $12,800.

Wall Street’s outlook has largely converged.

In addition to Jefferies and Goldman Sachs, HSBC told clients last week: “Metals prices are broadly in an upward cycle, with certain commodities supported by supply disruptions triggered by Middle East conflicts and strong structural demand.” The bank also warned that commodities face a “super squeeze” risk.

JPMorgan analysts also informed clients that copper’s upward cycle is being driven by tightening supply, accelerated grid investment, demand from AI data centers, and broader industrial electrification.

From Jefferies and Goldman Sachs to HSBC and JPMorgan, major Wall Street metals research teams are converging on the view that copper is entering a new phase of structural supply tightness, potentially opening room for LME copper prices to rise.