Morgan Stanley acknowledges that near-term CPO volume shipments have fallen short of expectations, forecasting optical engine shipments in 2027 to reach only 6–7 million units. However, it remains optimistic about explosive growth starting in 2028. The firm also explicitly refutes claims that 800V mass production will be delayed until 2028, stating that supply chain research indicates 800V racks are still on track for rollout in the second half of 2026.

In response to a market-moving report from a well-known semiconductor research firm, Morgan Stanley offered a cautious assessment.

According to Zhui Feng Trading Desk, on June 9, SemiAnalysis released a report stating that $NVIDIA (NVDA.US)$ mass-volume shipments of native 800V DC solutions will be delayed until after 2028, and it has also revised downward its shipment forecasts for CPO-related switches, directly triggering a sharp decline in the U.S. photonic communications sector. NVIDIA has reportedly denied the aforementioned claims.

Morgan Stanley’s Greater China hardware and semiconductor team promptly responded, largely agreeing with SemiAnalysis on CPO but holding a diametrically opposite view regarding the 800V timeline.

Morgan Stanley’s Greater China hardware and semiconductor team promptly responded, largely agreeing with SemiAnalysis on CPO but holding a diametrically opposite view regarding the 800V timeline.

On CPO, Morgan Stanley estimates global optical engine shipments in 2027 will only reach 6–7 million units, significantly below the market consensus of 20–30 million units, suggesting continued near-term sentiment pressure. However, it maintains an Overweight rating on key CPO-related stocks, expecting explosive CPO growth to begin in 2028, with the long-term investment thesis unchanged.

Regarding 800V, Morgan Stanley explicitly stated that this report contradicts information gathered from its supply chain checks, affirming that mass production of 800V DC power cabinets remains on track and has not been interrupted.

CPO: Acknowledges Delay, But Long-Term Thesis Remains Intact

In a report published on June 10, Morgan Stanley’s Greater China semiconductor team provided a systematic forecast on the near-term ramp-up pace of CPO adoption.

Morgan Stanley expects that, considering Taiwan Semiconductor’s capacity expansion plans and current yield rates, global optical engine shipments in 2027—including both scale-up and scale-out solutions—will amount to only 6–7 million units.

Manufacturing bottlenecks are the primary constraint.

$Taiwan Semiconductor (TSM.US)$ plans to expand its photonic integrated circuit (PIC) production capacity to 10,000 wafers per month by the first quarter of 2027. However, the current yield for system-on-integrated-chips (SoIC) remains at only 50% to 60%, with downstream assembly yields even lower, ranging from 20% to 50%. The combination of these two bottlenecks significantly constrains final shipment volumes.

Morgan Stanley noted that current market expectations for optical engine shipments are as high as 20–30 million units, significantly exceeding its own estimates. This expectation gap will continue to weigh on near-term sentiment in the CPO segment.

The period from 2026 to 2028 will be a transitional phase during which pluggable optical modules, CPO/NPO optical solutions, and copper interconnects coexist. The industry mainstream will remain at 1.6T/3.2T products, and widespread CPO adoption will still require time.

Nevertheless, Morgan Stanley maintains its Overweight rating on core CPO-related names such as Taiwan Semiconductor, asserting that the long-term growth thesis for CPO remains intact and that explosive growth will commence from 2028 onward.

800V: Supply Chain Survey Contradicts SemiAnalysis

On the issue of 800V DC power architecture, Morgan Stanley’s Greater China hardware team has taken a clearer stance.

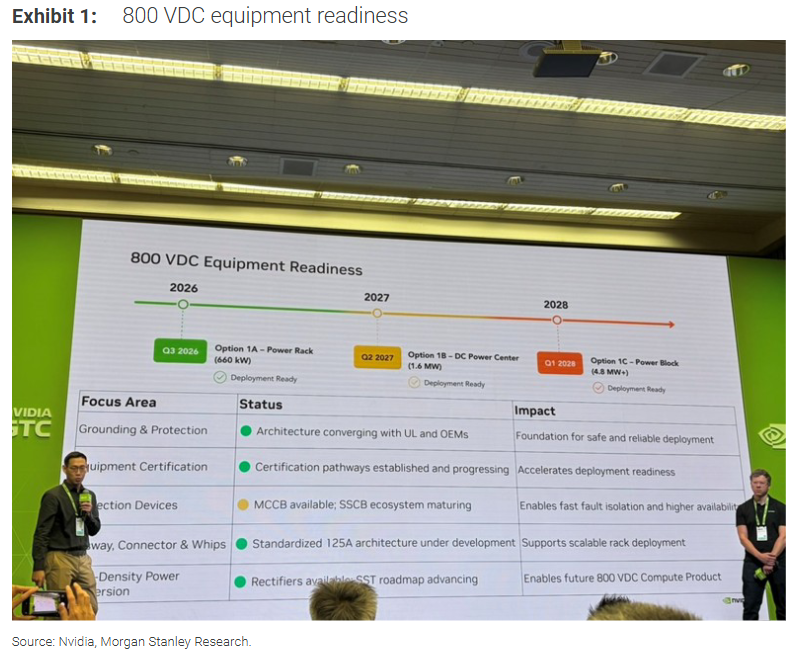

According to Morgan Stanley, NVIDIA stated at the GTC conference in Taipei that development of 800V DC technology is progressing steadily, with 800V DC power racks expected to reach production readiness in Q3 2026. This statement is not entirely contradictory to SemiAnalysis’s claim that 'large-scale shipments will be delayed until after 2028'—'production readiness' and 'mass ramp-up' represent two distinct milestones.

A noteworthy incremental insight from Morgan Stanley’s report is that Delta Electronics is poised to become the first vendor to mass-produce standalone 800V DC power racks, with initial deliveries to a leading North American hyperscale cloud service provider expected in Q4 2026.

However, Morgan Stanley also cautioned that initial shipment volumes will be limited, as the development of 800V DC protection components, UL certification, and the establishment of key industry safety standards will all take time to materialize.

The substantive disagreement between the two reports lies in the trajectory of the ±400V DC solution.

SemiAnalysis contends that ±400V will proceed as planned, continuing to serve cloud providers’ in-house ASIC deployments and coexisting with 800V over the long term. In contrast, Morgan Stanley’s supply chain survey indicates that major hyperscale cloud service providers have already shifted their R&D focus from ±400V to 800V. Given the same group of cloud providers and deployment window, these two assessments cannot both be correct—a divergence that will directly impact the power supply chain landscape and vendor positioning.

Market Impact: Expectation Gaps and Validation Milestones

The recent sell-off triggered by the SemiAnalysis report reflects the market's high sensitivity to the ramp-up timelines of two key AI infrastructure technology pathways.

Morgan Stanley’s response has provided some support for 800V-related stocks; however, the confirmed expectation gap in the CPO segment suggests that sentiment in this sector is unlikely to recover quickly in the near term.

Three key validation milestones lie ahead:

First, whether Delta Electronics’ first batch of 800V power racks for Q4 2026 will be shipped on schedule and to which customers;

Second, whether ±400V sidecar orders materialize by year-end and, if so, which supplier receives them—this will directly test the accuracy of each camp’s assessment of cloud providers’ preferred technical pathway;

Third, NVIDIA’s latest public commentary on the 800V architecture and the product timeline for Rubin Ultra/Kyber generations.

Amid current divergence in market information, actual order placements and certification progress will serve as the ultimate indicators of the true pace of adoption for these two technological pathways.

Editor/Deng