Recently,Tencent (00700.HK)Announced the issuance of USD 2.45 billion and RMB 15 billion in notes under its global medium-term note program with a maximum aggregate principal amount of USD 30 billion.

At first glance, this appears contradictory to its ample cash flow—by the end of March 2026, Tencent held RMB 533.665 billion in cash and time deposits, sufficient to cover its total debt of approximately RMB 386.8 billion, and generated over RMB 100 billion in net cash inflow from operating activities in the first quarter.

However, frequent bond issuances by tech giants are not driven by a lack of funds, but rather by a deep-seated 'ammunition anxiety.' Today, as AI large models grow exponentially in parameter scale, even internet behemoths with the strongest 'cash cow' businesses prefer to retain their own cash for daily operations or shareholder returns, opting instead for ultra-low-coupon debt financing to fund substantial hardware procurement costs. This strategy not only optimizes financial costs but also secures critical resources early in the escalating infrastructure arms race for AI.

The Hidden Financing Battle Among Giants: 'Ammunition Anxiety' Behind Robust Cash Flows

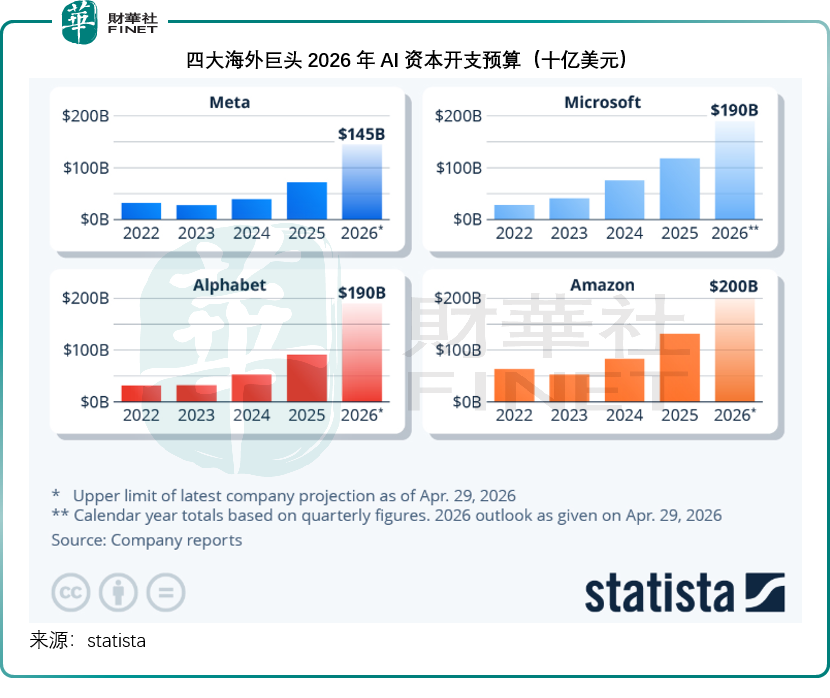

This trend is spreading globally. In 2026,Microsoft (MSFT.US)、$Amazon(AMZN.US)$、Google-A (GOOGL.US)、$Meta Platforms(META.US)$ the combined AI-focused capital expenditures of the four major tech giants could reach USD 725 billion, up 77% year-over-year, with more than 80% of funds precisely allocated to intelligent computing centers and in-house chip development.

This trend is spreading globally. In 2026,Microsoft (MSFT.US)、$Amazon(AMZN.US)$、Google-A (GOOGL.US)、$Meta Platforms(META.US)$ the combined AI-focused capital expenditures of the four major tech giants could reach USD 725 billion, up 77% year-over-year, with more than 80% of funds precisely allocated to intelligent computing centers and in-house chip development.

Domestically, ByteDance’s annual AI capital expenditure plan may reach several hundred billion yuan,$Alibaba-W (09988.HK)$and it has also announced plans to invest at least RMB 380 billion over the next three years to strengthen its domestic AI computing infrastructure.

Beyond corporate market-driven investments, governments worldwide are leveraging fiscal resources to mobilize private capital and reinforce national AI sovereignty. The United States is building national supercomputing centers through its 'Starship Gate' initiative; the European Union has launched a EUR 200 billion AI industrial framework; the United Kingdom unveiled its 'Sovereign Compute Strategy,' centered on an GBP 1.1 billion AI hardware program; and countries such as South Korea and Canada have implemented dedicated AI fiscal budgets focused on chips, computing power, and support for SME AI transformation.

At the domestic level, leveraging the 'East Data West Computing' strategy, provincial and municipal governments continue to roll out intelligent computing support funds worth hundreds of billions of yuan. The three major telecom operators will allocate over RMB 90 billion in capital expenditures related to computing power this year, further enhancing the nationwide integrated computing network. At the recent press conference launching the '15th Five-Year Plan' series, the National Development and Reform Commission (NDRC) also stated that this year will prioritize expanded effective investment initiatives in 'AI+' infrastructure and other key areas, aiming to establish long-term mechanisms for project construction, implementation, and operational maintenance.

Meanwhile, global industrial collaboration organizations, computing power alliances, and semiconductor supply chain enterprises are simultaneously increasing their complementary capital investments, addressing gaps in AI industry chain support through joint factory construction, co-development of technologies, and shared computing resources, thereby establishing a tripartite synergy among enterprises, governments, and institutions with comprehensive, intensified investment in AI.

To seize the opportunities presented by AI development, not only Tencent but also other major corporations are taking advantage of the low-interest-rate environment to lock in low-cost funding to meet high capital expenditure requirements.

For example,Google-A (GOOGL.US)This year, it launched its largest-ever combined equity and bond financing package, including a multi-currency bond issuance totaling USD 32 billion—featuring an ultra-long-dated sterling-denominated bond with a 100-year maturity issued in February—potentially earmarked for capital expenditures on AI data centers, servers, and self-developed chips. In June, it announced a record-breaking equity offering of up to USD 84.75 billion, with Berkshire Hathaway—under new leadership following Buffett’s departure as CEO—committing USD 10 billion specifically for expanding AI computing infrastructure.

In March of this year,$Amazon(AMZN.US)$It has issued nearly USD 37 billion in bonds and EUR 14.5 billion, subsequently entering the Swiss franc bond market for the first time in May with CHF 2.82 billion raised, followed by another CAD 14 billion raised in June—the largest single corporate bond transaction in Canadian history. Meta Platforms has issued approximately USD 25 billion in new bonds in the first half of this year, and its long-term debt outstanding at the end of 2025 has already increased by USD 30 billion compared to the beginning of the year. Oracle (ORCL.US) has also raised over USD 30 billion in financing this year.

On the domestic front,$Alibaba-W (09988.HK)$in the second half of last year, referencing its subsidiary,$Ali Health(00241.HK)$it issued HKD 12 billion in zero-coupon exchangeable bonds linked to ordinary shares, and in September issued USD 3.2 billion in zero-coupon convertible unsecured senior notes. Baidu also conducted multiple financings last year, with total proceeds potentially reaching hundreds of billions of renminbi.

These internet giants all possess strong, proven 'cash cow' businesses rooted in their leadership positions within niche segments and maintain sound financial conditions; nonetheless, they are raising low-cost capital through debt issuances to pave the way for future AI development.

Industry Chain Mapping: A Comprehensive Representation of Core Hong Kong-Listed Assets

Massive capital expenditures are cascading down the industrial chain, reshaping the investment landscape of Hong Kong’s tech ecosystem. In this boom, the Hong Kong stock market has attracted a large number of new economy and new technology companies, as well as leading A-share firms listing in Hong Kong—collectively forming the core assets of the AI industrial chain:

1) Upstream: Materials, components, semiconductor equipment, and foundry services

The upstream segments—materials, components, and semiconductor equipment—are currently the most robust and earliest to realize tangible returns.

With the rapid iteration cycles of AI servers, specialty electronic materials, advanced ceramic substrates, and MLCCs (multilayer ceramic capacitors) are experiencing simultaneous growth in both volume and pricing. In this space, Honghe Technology (603256.SH), an A-share-listed supplier of low-dielectric electronic fabrics for AI servers, and Sanhuan Group (300408.SZ), which specializes in high-performance electronic ceramics, optical communication substrates, and MLCCs, have both filed listing applications with the Hong Kong Stock Exchange.

Leading foundry players in mature process nodes$SMIC (00981.HK)$and$Huahong Hongli (01347.HK)$are operating at full capacity, deeply capturing domestic substitution demand; while leading semiconductor equipment manufacturers $ASMPT(00522.HK)$ are fully benefiting from the expansion driven by HBM and advanced packaging. Meanwhile, domestic high-end GPU chip companies$Biren Technology (06082.HK)$、TianShu ZhiXin (09903.HK)continue to secure local computing power procurement orders, accelerating the domestic substitution of high-end chips.

2) Midstream: Hardware equipment, optical communications, servers, and IDC computing infrastructure

In midstream segments—including hardware assembly, optical communications, and IDC computing infrastructure—capital expenditures are being converted into concrete hardware procurement. Among these,$Yangtze Optical Fibre and Cable Joint Stock Limited Company (06869.HK)$With a decade-long streak of holding the world’s largest market share and its forward-looking “AI-2030” strategy, it has established the “digital lifeline” of the AI era through core technologies such as hollow-core fiber optics;Lenovo Group (00992.HK)As the leading ODM for AI servers, it is deeply integrated with major cloud providers;$KBT Group (00148.HK)$and$KBTL (01888.HK)$It has built a robust moat by virtue of its position as the global leader in copper-clad laminates;$Guanghe Technology (01989.HK)$provides computing accelerator cards indirectly through its ODM customers.

Meanwhile, companies such as Zhongji Xuchuang (300308.SZ)—a leading optical communications firm holding long-term orders for high-end 800G/1.6T optical modules (planning a Hong Kong listing)—Dongshan Precision (002384.SZ), which specializes in high-frequency PCBs for AI servers (already filed for listing), and AidiTech, focused on high-speed fiber optic connectors (already filed), are perfectly aligned with the ultra-high bandwidth requirements of next-generation intelligent computing centers.

3) Downstream: Large Models, Industry Applications, Smart Devices, and Robotics

If upstream players are the “water sellers,” then downstream segments—such as large models, industry applications, and smart devices—are the true “token factories” defining the digital economy era.

Hong Kong-listed native large model companies$Zhipu(02513.HK)$and$MINIMAX-W(00100.HK)$are accelerating enterprise commercialization, with economies of scale gradually emerging. In terms of service ecosystems,Tencent (00700.HK)、$Alibaba-W (09988.HK)$andBaidu Group-SW (09888.HK)leveraging its full-stack AI capabilities, it has achieved integrated deployment across models, computing power, and application scenarios. Platform-oriented companies such as$Kuaishou-W (01024.HK)$、$Meituan-W(03690.HK)$、$JD.com-SW (09618.HK)$, enabling industries to indirectly benefit through AI algorithm-driven operational optimization, cost reduction, and efficiency enhancement. Additionally, the robotics segment remains highly active,$DoThink(02432.HK)$、$Ubtech Robotics (09880.HK)$alongside the public listings of numerous robotics companies such as Xian Gong Intelligence, further enriching the downstream investment landscape with concrete opportunities.

4) Standalone Enabling Segment: Power and Telecommunications Utilities

In the standalone enabling utilities segment, the 24/7 high-load operation of AI computing centers has generated stable and substantial incremental electricity demand.China Resources Power (00836.HK)、China Power International Development (02380.HK)、Datang Power (00991.HK)、Huaneng Power International, Inc. (00902.HK)core listed entities continue to implement green power and dedicated power supply partnerships for intelligent computing centers, offering both low-volatility defensive characteristics and valuation recovery potential. On the telecommunications infrastructure front,$China Mobile(00941.HK)$、$China Telecom (00728.HK)$、China Unicom (00762.HK)continued investment in intelligent computing clusters is making computing power leasing a second growth curve for these firms, while also enabling telecom service providers to capture AI-related upside through new service offerings and usage-based billing models (e.g., token-based pricing and AI network service packages).

Critical Reflections Beneath the Prosperity

Despite its promising outlook, investors should remain vigilant about an inherent paradox in the industry’s development.

Persistent shortages and rising prices of upstream materials, chips, and components—combined with persistently high construction costs for midstream computing infrastructure—could drive up costs across the entire value chain and pass them downstream. If end-user pricing for AI application services and smart terminal products becomes too high, it will significantly dampen willingness to pay among both government-enterprise clients and consumers, preventing user demand from scaling and obstructing downstream commercialization. Under pressure on profitability, downstream players may become unable to sustainably absorb midstream computing costs and upstream hardware procurement expenses, ultimately failing to generate real value.

This represents the most significant pain point facing AI development. Currently, valuations for equities linked to the mid- and upstream segments of the industrial chain are exceptionally high, driven by the massive capital expenditure budgets anticipated from the downstream application segment and the existing capacity gap in mid- and upstream supply chains, which has created opportunities for price increases and upward momentum in sector sentiment.

However, as midstream and upstream sectors increase capacity investment and expand production—leading to falling prices—if end-user monetization capabilities fall short of expectations and demand from these segments declines, it will adversely affect their profitability, potentially triggering contraction, intensified competition, or even elimination, resulting in a reassessment of their valuations.

In the near term, the following risks warrant caution:

First is the underlying concern of 'overcapacity.' Historically, every technological revolution has been accompanied by excessive investment. If the commercial monetization pace of AI applications lags behind the expansion of computing power infrastructure, the industry could face temporary overcapacity and price wars by 2027.

Second is geopolitical and supply chain risk. Access to advanced chips and export controls on manufacturing equipment remain a Damocles’ sword hanging overhead, potentially forcing domestic firms to incur higher adaptation costs and temporarily weighing on profit margins.

Lastly, there is macro liquidity volatility. The Federal Reserve’s interest rate policy directly impacts the discount rate (denominator) for global technology stocks. Although markets currently price in rate cuts, a resurgence in inflation that drives up financing costs would sharply increase financial pressure on capital-intensive companies.

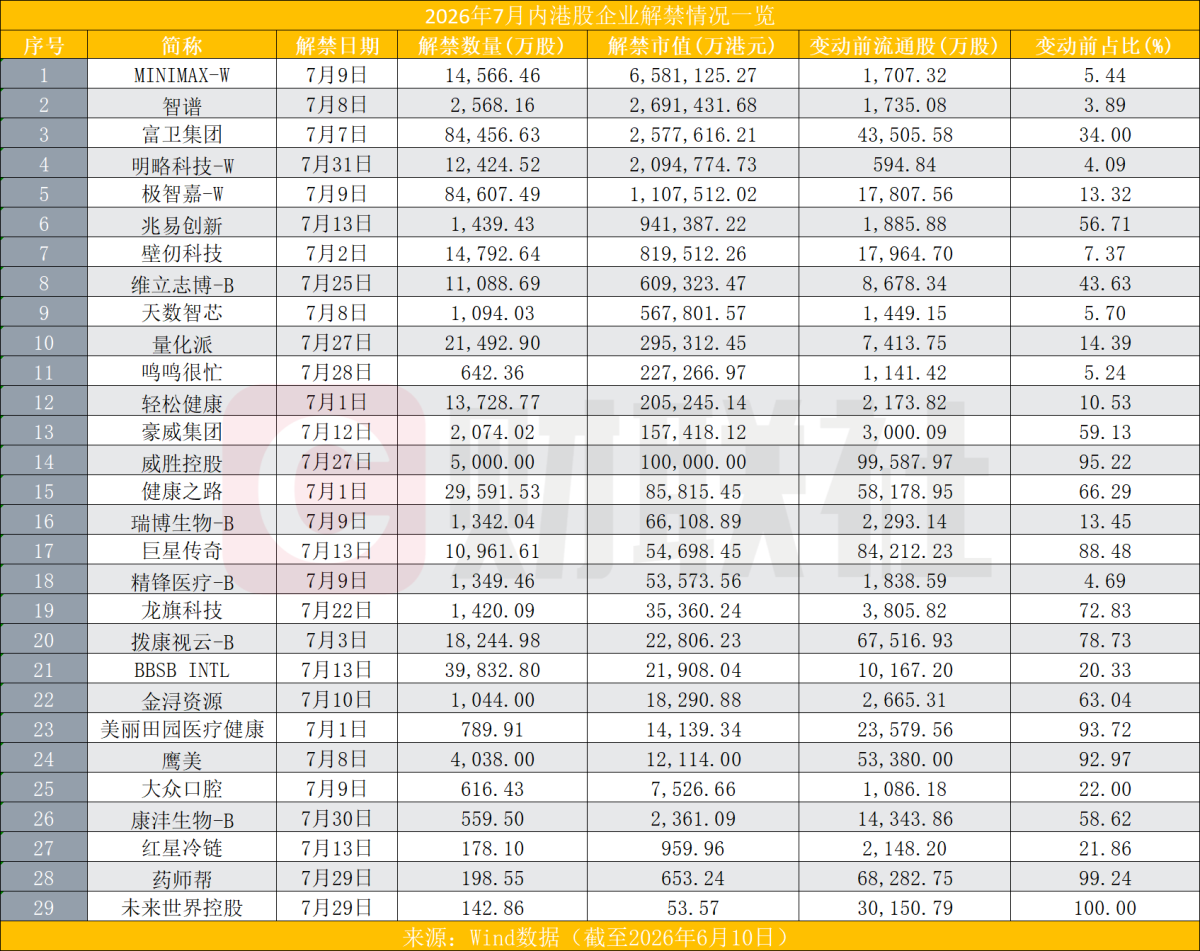

Moreover, restricted shares of numerous companies along the AI industry chain will be unlocked en masse in July. According to Wind data, 29 Hong Kong-listed companies are scheduled to have their lock-up periods expire in July. Among them,$Zhipu(02513.HK)$、$MINIMAX-W(00100.HK)$rank among those with the largest market value of unlocked shares. July 9 will see the highest concentration of share unlocks for the month, with a total of five Hong Kong-listed companies lifting restrictions on their shares that day. Apart from MiniMax,Dazhong Dental (02651.HK)、$Geekplus-W (02590.HK)$、RiboBio-B (06938.HK)、Jingfeng Medical-B (02675.HK)will unlock 6.1643 million shares, 846 million shares, 13.4204 million shares, and 13.4946 million shares, respectively.

In summary, the AI investment surge expected in 2026 represents a highly certain industrial trend. For investors positioning in Hong Kong-listed equities, the key lies in identifying true 'pick-and-shovel' beneficiaries—those positioned to capture global capital expenditure tailwinds—and internet giants capable of leveraging AI to reduce costs, enhance efficiency, and reshape their business models. Staying committed to core assets amid volatility may prove to be the optimal strategy in this wave.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/melody