① Barclays forecasts that capital expenditures by major cloud providers will reach USD 1.16 trillion by 2028; ② as capital spending approaches consuming all operating cash flow, debt issuance alone will be insufficient to sustain AI expansion in the long term, prompting tech giants to adopt additional financing tools such as equity offerings and convertible bonds; ③ Barclays believes Google’s large-scale fundraising does not reflect liquidity stress but rather a proactive balance sheet optimization, a strategy other tech giants may also adopt.

Caixin News, June 10 (Editor: Xia Junxiong) — In its latest research report, Barclays noted that as artificial intelligence (AI)-related capital expenditures continue to grow substantially, even $Alphabet-C (GOOG.US)$ 、$Microsoft (MSFT.US)$、 $Meta Platforms (META.US)$ 、$Amazon (AMZN.US)$such mega-cap technology companies have begun proactively diversifying their financing channels.

The bank stated that equity financing, convertible bonds, and other equity-linked financing instruments are gradually becoming essential components of capital allocation in the AI era.

AI-related capital expenditures are heading toward the trillion-dollar scale

AI-related capital expenditures are heading toward the trillion-dollar scale

Barclays believes the market continues to underestimate the scale of AI infrastructure investment over the coming years.

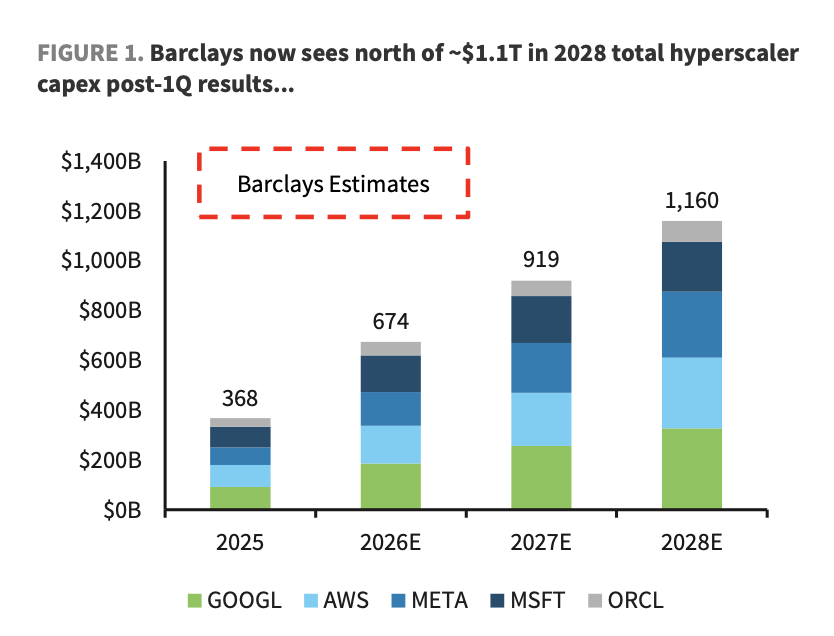

According to its forecast, $Alphabet-C (GOOG.US)$ Alphabet, the parent company of $Amazon (AMZN.US)$ 、 $Meta Platforms (META.US)$ 、 $Microsoft (MSFT.US)$ and$Oracle (ORCL.US)$ and other major hyperscale cloud providers will see their capital expenditures rise from approximately $368 billion in 2025 to $674 billion in 2026, reaching $919 billion in 2027 and further increasing to approximately $1.16 trillion in 2028.

(Barclays’ forecast for capital expenditures by the five major cloud providers)

This forecast is significantly higher than the market consensus. Barclays estimates that by 2028, capital expenditures by these cloud providers will exceed the market’s consensus expectation by approximately 26%.

Operating cash flow pressure is intensifying

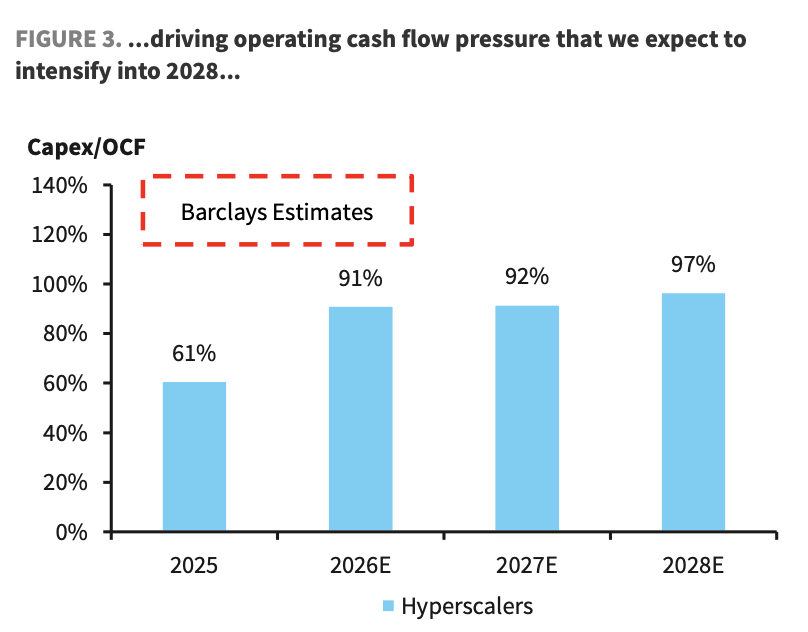

According to Barclays’ calculations, the ratio of capital expenditures to operating cash flow for major cloud providers will rise from 61% in 2025 to 91% in 2026, 92% in 2027, and reach 97% by 2028.

(Barclays' forecast of capital expenditure as a share of cash flow for cloud giants)

This implies that by around 2028, these companies will need to allocate nearly all of their operating cash flow to fund capital expenditures.

By contrast, the market generally expects this ratio to decline to approximately 77% by 2028. Barclays considers this expectation overly optimistic, arguing that future cash flow pressures will be significantly higher than currently perceived by the market.

In other words, even though these technology firms continue to demonstrate strong profitability, the pace of AI-related investment growth has already begun to outstrip their internal cash generation capacity.

Bond market absorption capacity is limited

Over the recent period, the investment-grade bond market has become a key financing channel for tech giants to support AI-related capital expenditures.

Barclays forecasts that in 2026, investment-grade bond issuance by these hyperscale cloud providers will have already exceeded USD 200 billion, potentially reaching approximately USD 240 billion for the full year.

This scale is highly unusual for non-financial corporations and even surpasses the annual bond issuance volume of major U.S. banks.

However, even if the bond market remains willing to supply funding, issues are beginning to emerge.

Debt financing can address immediate funding needs but will continuously erode companies’ future borrowing capacity. When the AI investment cycle extends over several years or longer, reliance solely on bond financing is clearly suboptimal.

As a result, an increasing number of technology companies are turning to project financing, asset securitization, GPU-backed loans, and joint ventures or partnerships to diversify the pressure of capital expenditures.

Why has Google suddenly launched a large-scale equity financing?

Google’s recent large-scale financing is a key case discussed in the Barclays report.

Google recently raised USD 84.75 billion in equity capital to fund the construction of global computing infrastructure.

Its financing structure includes USD 16.75 billion in three-year mandatory convertible preferred shares, a simultaneous offering of USD 18 billion in Class A and Class C common stock, a USD 40 billion at-the-market (ATM) equity offering program, and a USD 10 billion private placement directed exclusively to Berkshire Hathaway.

Many investors’ immediate reaction was: Is Google short on cash? However, Barclays’ answer is no.

The bank emphasized that Google is not issuing equity because it cannot access debt financing. On the contrary, the bond market remains willing to provide it with substantial low-cost funding.

The report notes that Google’s decision to raise equity capital is primarily driven by three factors.

First, equity financing broadens funding sources. Companies are no longer solely reliant on the investment-grade bond market but instead utilize a combination of debt, equity, convertible bonds, and structured financing, thereby reducing dependence on any single channel.

Second, equity financing improves the balance sheet. By increasing equity capital, lowering leverage, and enhancing credit metrics, the company can continue to access bond financing in the future without jeopardizing its credit rating or driving up its cost of capital.

Finally, and most importantly, equity financing can provide a cushion for debt investors. Given the lengthy investment cycle in AI and the continued uncertainty around end-market demand, greater equity capital can bolster creditors’ confidence and alleviate market concerns about extreme downside scenarios.

Convertible bonds serve as a bridge between debt and equity.

Among equity instruments, Barclays places particular emphasis on the role of convertible bonds.

Convertible bonds sit between straight debt and common equity. For issuers, they provide access to capital without immediate dilution of existing shareholders’ equity; for investors, they offer both the defensive characteristics of bonds and the potential upside from future stock price appreciation.

Convertible bonds have long been a commonly used financing instrument in innovative sectors, and the U.S. convertible bond market has now clearly tilted toward the AI value chain, spanning semiconductors, software, data center infrastructure, crypto-related platforms, e-commerce, and mobility sectors.

The U.S. convertible bond market is also expanding rapidly.

As of this year, U.S. convertible bond issuance has reached approximately USD 78 billion, marking the strongest start since 2003. The total market size has grown from roughly USD 315.5 billion to USD 471.5 billion, reaching a record high.

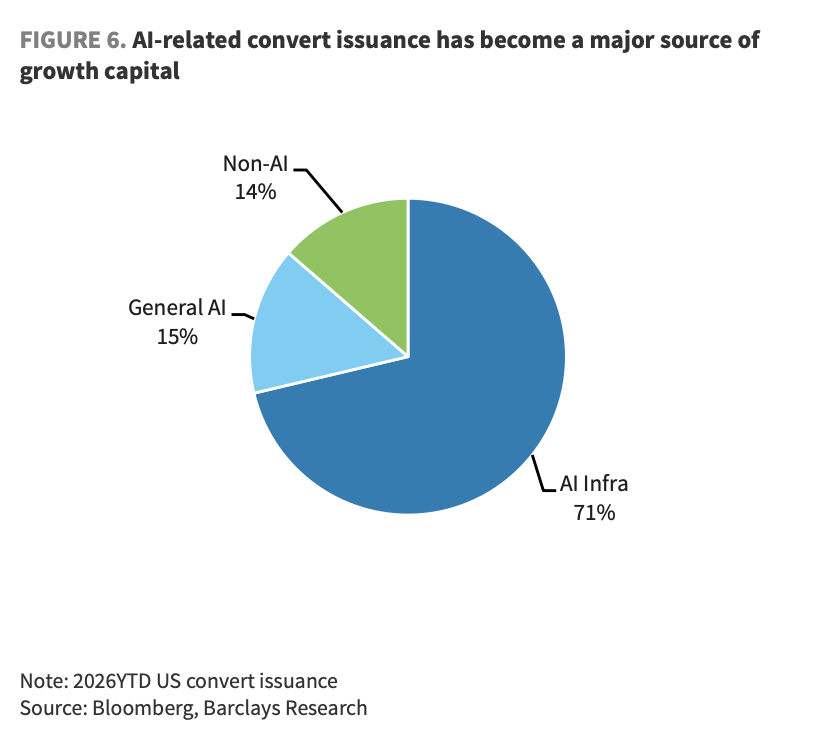

Meanwhile, AI has become the primary driver of growth in the convertible bond market.

According to Barclays, 71% of new U.S. convertible bond issuance this year is linked to AI infrastructure, 15% to general-purpose AI, and only 14% to non-AI projects.

(Breakdown of new U.S. convertible bond issuance by category this year)

Mandatory convertibles may become a future trend.

Among the various convertible bond products, Barclays is particularly bullish on mandatory convertibles.

Unlike conventional convertible bonds, mandatory convertibles must be converted into equity after a specified period, making them closer to equity financing.

For corporations, their key advantage lies in receiving credit rating treatment akin to equity while avoiding the immediate issuance of a large volume of common shares. Both Google and Oracle have recently adopted this structure.

In contrast, zero-coupon convertibles—which have grown popular in recent years—may reduce financing costs but remain fundamentally debt-like instruments and do not serve to strengthen credit profiles.

Therefore, for tech giants undertaking long-term AI investments, mandatory convertibles offer greater strategic value than zero-coupon convertibles.

Who will be the next issuer?

As fellow hyperscale cloud providers, will Meta, Microsoft, and Amazon follow Google and Oracle in adopting more equity-linked financing instruments?

Note: According to the Financial Times last Friday, Meta is considering an equity offering worth tens of billions of dollars. However, Meta has denied the accuracy of this report.

Barclays believes that if AI investment continues to expand over the coming years, the likelihood of Meta, Microsoft, and Amazon issuing equity, mandatory convertibles, or other equity-linked securities will rise significantly.

In the bank's view, this would not be regarded as financing stress, but rather as indicative of a new capital management paradigm.

Editor/Deng