Rich Privorotsky of Goldman Sachs warned that as market positions, leverage, and AI-related capital expenditures have become deeply intertwined, the inherent cyclical risks within this ecosystem have grown increasingly difficult to ignore; any disruption to the AI spending cycle would lay bare the market’s fragility.

The AI investment frenzy is accumulating systemic vulnerabilities.

Goldman Sachs partner Rich Privorotsky has issued a warning that as market positioning, leverage, and AI-related capital expenditures become deeply intertwined, the inherent cyclical risks within this ecosystem have become increasingly difficult to ignore. Should the AI spending cycle experience any disruption, market fragility will be laid bare.

The immediate trigger for market concern was data center developer Crusoe’s decision to pause a 1.8-gigawatt data center project in Wyoming—halted at the request of its client, whose identity remains undisclosed. Privorotsky noted that in a market where nearly all asset valuations are tied to AI capital expenditure, even an isolated project delay or reprioritization is sufficient to compel investors to reassess their assumptions about future demand.

The immediate trigger for market concern was data center developer Crusoe’s decision to pause a 1.8-gigawatt data center project in Wyoming—halted at the request of its client, whose identity remains undisclosed. Privorotsky noted that in a market where nearly all asset valuations are tied to AI capital expenditure, even an isolated project delay or reprioritization is sufficient to compel investors to reassess their assumptions about future demand.

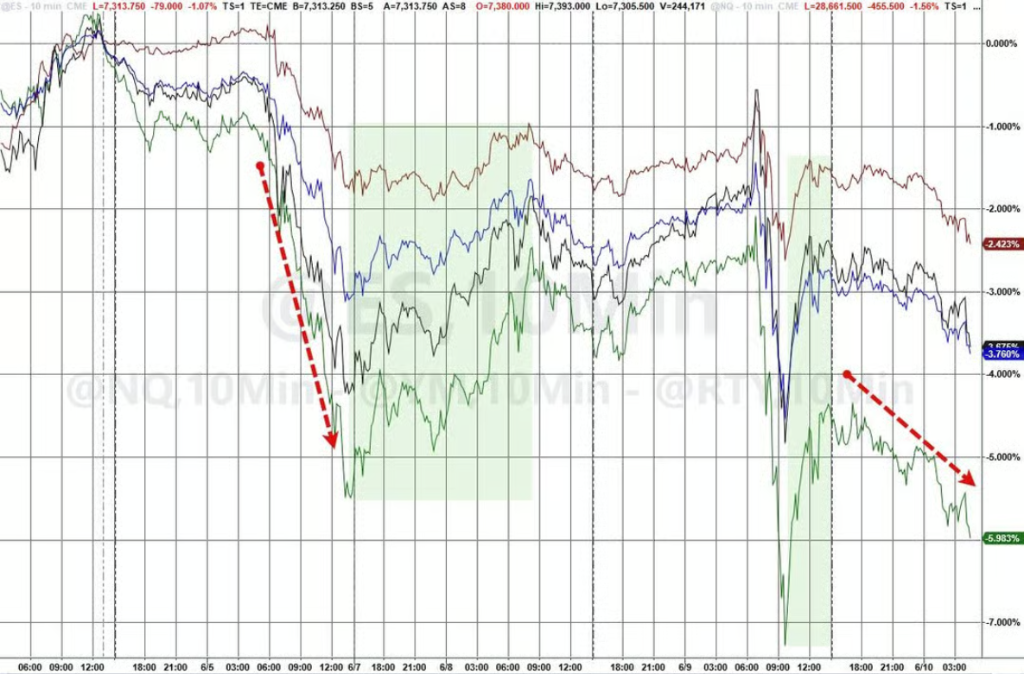

Meanwhile, the Nasdaq Composite Index has declined by approximately 6% since last Thursday’s close, significantly underperforming both bonds and crude oil. Privorotsky warned that current market momentum returns are at the 90th percentile over the past five years, total exposure stands at the 99th percentile, financing spreads are widening due to leveraged demand, and retail participation through leveraged ETFs remains substantial—all of which render the market highly sensitive to any shifts in the AI spending cycle.

Data Center Project Paused; AI Demand Assumptions Under Scrutiny

The Crusoe Wyoming project drew attention because of its unique design—to bypass grid constraints by using 900 megawatts of behind-the-meter power, specifically tailored to address the power supply challenges of AI computing infrastructure.

Given that the project was halted during its early development phase and the client’s identity remains undisclosed, Privorotsky explicitly stated that drawing macroeconomic conclusions from this incident would be a mistake.

However, the symbolic significance of this event cannot be overlooked.

In the prevailing market narrative, investments in AI hardware and data centers serve as the core pillar supporting technology stock valuations. Any signal suggesting slowing demand, project delays, or shifting client priorities is amplified and interpreted broadly by the market.

Privorotsky’s assessment is that while an isolated incident does not constitute a trend, in a highly crowded positioning environment, the market’s tolerance for such signals has diminished considerably.

AI Ecosystem Divergence: Dual-Track Coexistence of Frontier Intelligence and Local Models

Privorotsky envisions an emerging "bimodal world": on one end, cutting-edge models—and eventually superintelligence—accessible via centralized cloud infrastructure at high cost; on the other, a largely free, open, and increasingly capable local AI layer handling the vast majority of everyday tasks. He anticipates that, in the final configuration, routine work will be performed on local or open-source models, while complex reasoning and difficult problem-solving will be delegated to high-end cloud-based systems.

There remains fundamental disagreement about what this bifurcation implies for the AI investment cycle.

The optimistic interpretation holds that the overall pie will continue expanding, driving broad-based growth in demand for edge computing, data centers, storage, power, and networking. The pessimistic view contends that most economically valuable tasks may already—or soon will be able to—run on existing hardware, implying that the actual inflection point in demand could lag significantly behind the timeline embedded in current valuations. Privorotsky notes that the debate is increasingly less about model quality per se and more about where inference computation will ultimately occur.

Cyclical Risks Accumulate as Leverage Amplifies Vulnerability

Privorotsky’s concern about the current market structure centers on a core judgment: AI spending has become the market system’s "long leg"—it is the primary driver of hardware investment, a significant contributor to GDP growth, and a key pillar supporting overall market performance. This highly concentrated dependency has created a self-reinforcing cycle whose fragility is becoming increasingly difficult to ignore.

He specifically highlights that the substantial embedded and synthetic exposures created by leveraged products have led to a severe undervaluation of market hedging instruments. In his view, holding gamma—the convexity exposure inherent in options—offers far greater practical utility in current portfolio management than most investors recognize. While this risk is not new, markets are accelerating toward it rather than proactively avoiding it.

The AI-Investment-Driven Economy Is "Overheating"

At the macro level, Privorotsky turns his attention to U.S. CPI data.

Data released Wednesday by the U.S. Bureau of Labor Statistics showed that the Consumer Price Index (CPI) rose 4.2% year-over-year in May, the highest level since early 2023, in line with market expectations.

Privorotsky emphasized that the relatively mild official data cannot obscure the strong underlying inflationary pressures: rising energy costs, nearly $1 trillion in AI-related corporate investment, and a U.S. fiscal deficit amounting to approximately 6% to 7% of GDP collectively constitute structural drivers of inflation.

His assessment is that this is an investment-driven economy operating at an overheated pace, and unless the productivity gains from AI are sufficiently substantial, inflation will persist as a byproduct over the long term.

Editor/Lee