The Nasdaq fell by 2%, the S&P 500 dropped 1.6% to a five-week low, and the Dow Jones Industrial Average declined by 1.87%. Following its earnings release, Oracle’s stock plummeted by over 6%. The Philadelphia Semiconductor Index fell 3.6% on the day. The Magnificent Seven once again significantly underperformed the broader market, with a cumulative decline of nearly 8% over the past seven trading sessions. Spot gold plunged 4.4% to $4,075.40 per ounce, breaking below its March low and marking its lowest closing price since November 2025.

Although core inflation has shown modest signs of easing—providing some breathing room on the interest rate front—the escalating U.S.-Iran conflict has triggered a sharp surge in crude oil prices, heightening inflation concerns.

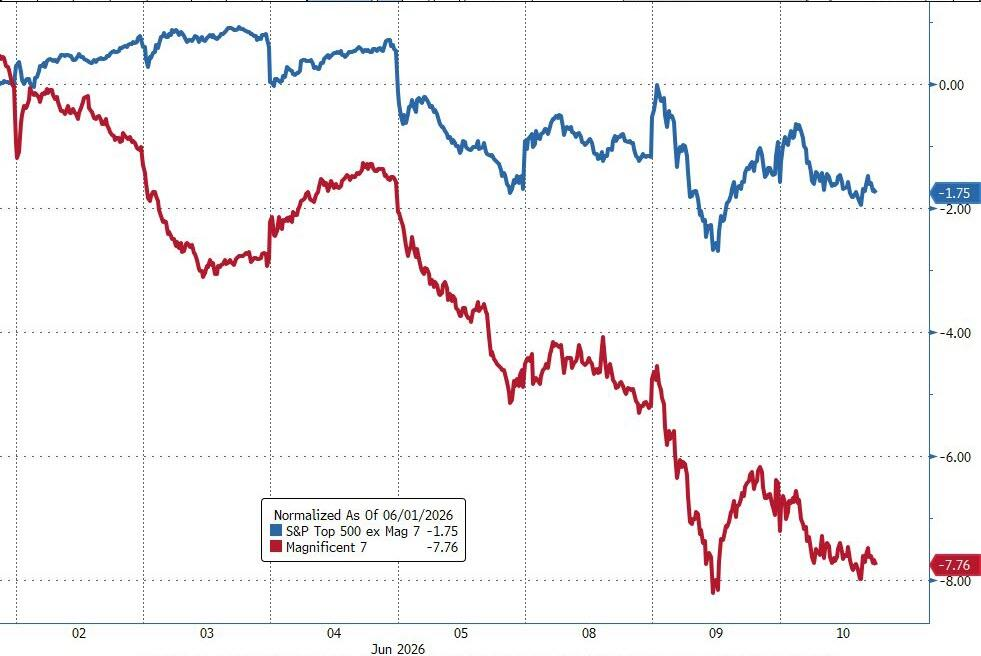

Meanwhile, capital is accelerating its exit from AI and semiconductor giants perceived as overvalued, dragging the Nasdaq down by 2% and pushing the S&P 500 to a five-week low. In after-hours trading following its earnings release, Oracle’s shares tumbled by more than 6%.

Additionally, liquidity drying up, margin calls, and the impending massive IPO drawdown effect have triggered broad-based deleveraging across asset classes, sending gold prices crashing by more than 4%.

Additionally, liquidity drying up, margin calls, and the impending massive IPO drawdown effect have triggered broad-based deleveraging across asset classes, sending gold prices crashing by more than 4%.

Tensions in Iran escalate as oil prices stabilize above $90

After the U.S. and Iran exchanged missile strikes overnight, Trump posted on social media warning that “Iran must pay a price for delaying negotiations,” and at 11:45 a.m. local time further declared that the U.S. would resume strikes against Iran “very forcefully.”

According to CCTV International News, U.S. Defense Secretary Hegseth stated that U.S. Central Command would be “very busy” on the evening of June 10 (Eastern Time), as American forces would “strike Iran heavily” that night and “bomb key facilities inside Iran.”

Moreover, a sharp drop in Cushing crude inventories and significant draws from the Strategic Petroleum Reserve (SPR) briefly accelerated upward momentum in oil prices. Trump later noted on his social media platform that over 100 million barrels of crude were already transiting the Strait of Hormuz, slightly tempering the rally.

WTI crude futures settled at $90.41 per barrel on the day, up approximately 2.5%; Brent crude also struggled to fall below the $90 threshold.

Fawad Razaqzada, Global Macro Market Analyst at StoneX, stated:

As Trump warned that Iran must pay a price for delaying negotiations, oil prices moved higher again, and our risk bias for crude oil price forecasts remains tilted to the upside.

Tech stocks continue to deleverage, revealing signs of crowding risk in AI-related trades.

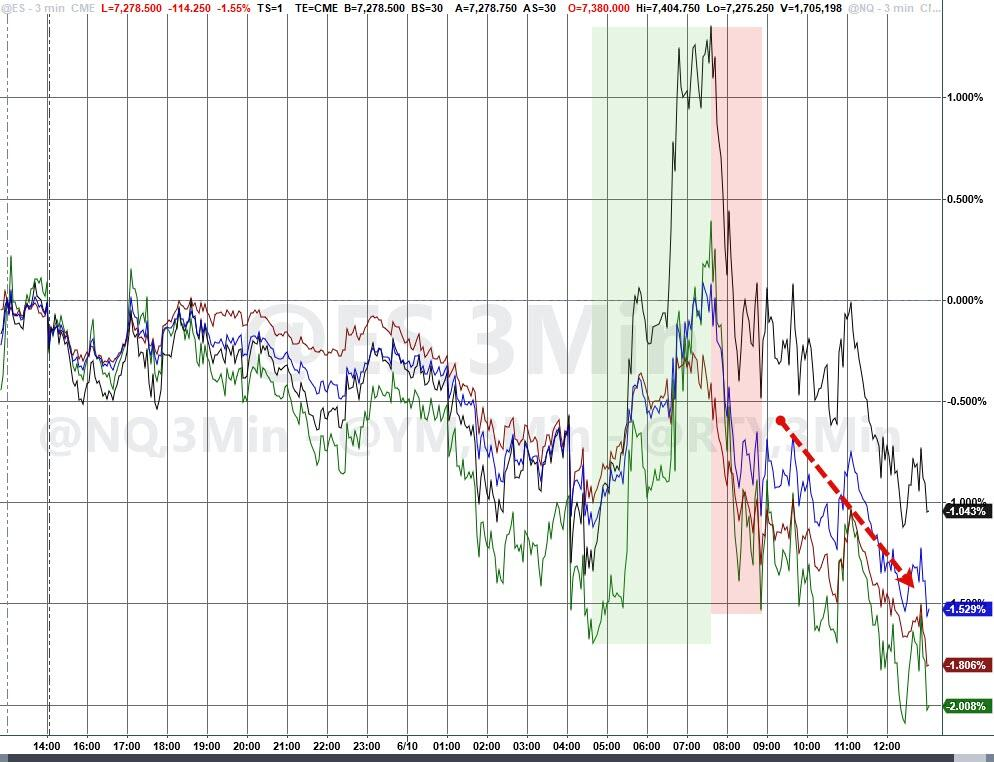

U.S. equities followed a pattern similar to yesterday’s early session: opening weakly, then rebounding after the U.S. market opened, only to suffer a sharp sell-off around 10:30 a.m. ET.

Highly crowded semiconductor and AI-related positions saw accelerated unwinding today, dragging the Nasdaq down by 2%, pushing the S&P 500 to a five-week low with a 1.6% decline, and sending the Dow Jones Industrial Average down 1.87%.

Goldman Sachs’ trading desk noted that markets are clearly in a 'geopolitical risk-on' mode, with energy and other bond-like equities outperforming, while tech, derivatives, and industrial sectors posted significant losses.

The Philadelphia Semiconductor Index fell 3.6% on the day. The Mag 7 once again significantly underperformed the broader market, posting a cumulative loss of nearly 8% over the past seven trading sessions.

$NVIDIA (NVDA.US)$ The stock price has retraced 16% from its recent high, breaking below the 50-day moving average—the first time it has done so since April 8—and the round-number $200 level has become a key technical support closely watched by the market.

Goldman Sachs’ derivatives team pointed out that retail trading activity and options pricing reflect persistently elevated market expectations, while institutional investors have expressed clear concerns about the speed of this rebound and the market’s concentrated positioning in AI-related assets.

Goldman Sachs’ Privorotsky offered a particularly blunt characterization of the current market structure:

All positions are highly correlated with AI spending, and this cyclicality has become increasingly difficult to ignore. Should the AI spending cycle be disrupted, the resulting vulnerability would be evident.

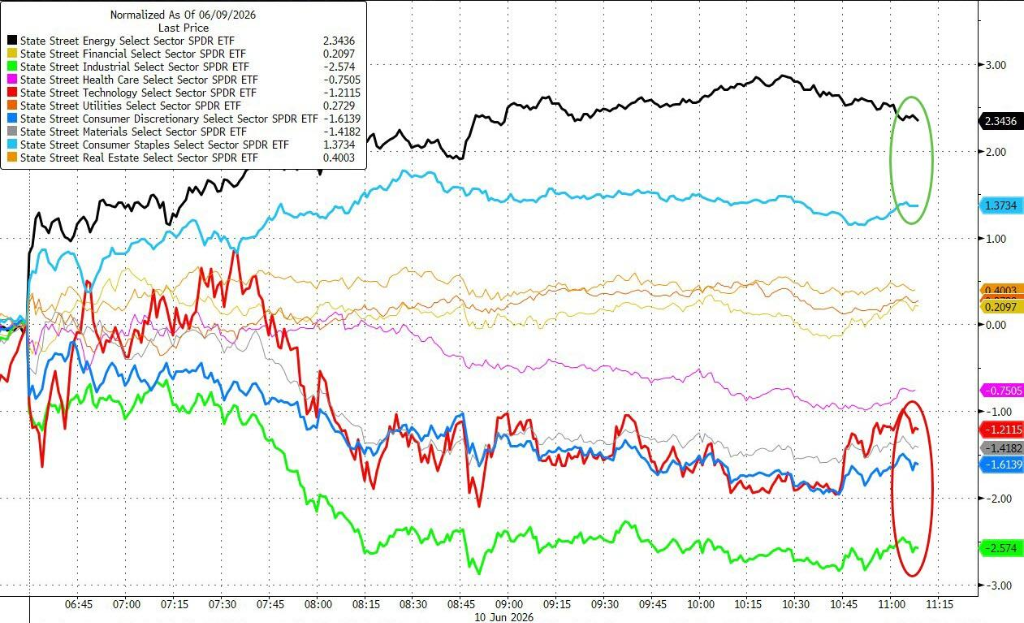

Jonathan Krinsky, chief technical strategist at BTIG, noted that since the S&P 500 hit a record high of 7,609 on last Tuesday (June 2), the benchmark index has declined by approximately 4% to around 7,300.

However, during this period, six of the ten sectors still posted positive returns, with healthcare, consumer staples, REITs, and financials each rising more than 2%, while the technology sector dropped by over 10%.

Jonathan Krinsky stated:

“This is essentially a momentum pullback, with crowded positions in semiconductors/AI being unwound, while previously underweight defensive and cyclical sectors are seeing buying interest.”

“We still lean toward viewing this as a positioning adjustment rather than a trend reversal, but the move isn’t fully complete yet. Investors are advised to ‘buckle up.’”

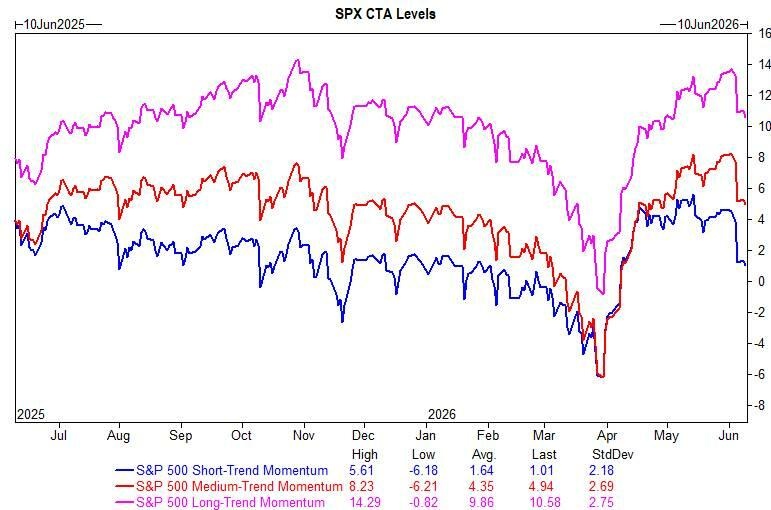

Goldman Sachs estimates that CTA strategies have already turned net sellers across various market scenarios for the coming week. The S&P 500 has breached the short-term CTA sell threshold, remains 4% above the medium-term threshold, and 9% above the long-term threshold.

CPI data remains mild; rate cut expectations still distant

May’s inflation data did not deliver any material surprises.

U.S. CPI rose 4.2% year-over-year in May—the highest in three years—while core CPI accelerated to 2.9% year-over-year. However, the month-over-month increase came in below expectations, leaving room for interpretation regarding the Federal Reserve’s monetary policy path.

Dan Carter, senior portfolio manager at Fort Washington, stated:

The greatest significance of this data lies in providing the Federal Reserve with a bit of breathing room. Had the data run hot again, it would have intensified pressure on the Fed to raise rates further, but the current outcome is sufficiently benign to allow the Fed to remain on hold.

David Kelly, Chief Global Strategist at JPMorgan Asset Management, stated:

A 4% level isn’t attractive, and of course there’s no reason to ease policy at this juncture, but I believe the Fed can afford to stay put.

The yield on the 10-year U.S. Treasury note rose modestly by 3 basis points to 4.54%, reflecting relatively muted moves at the long end. Markets continue to fully price in at least one 25-basis-point rate hike within the year.

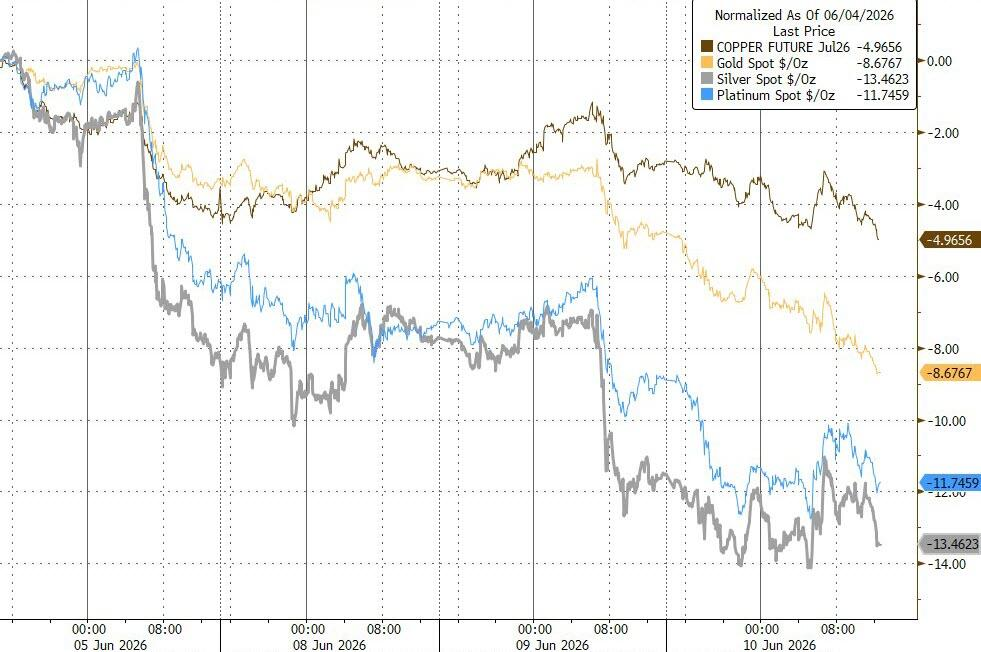

Gold Plunges Sharply; Liquidity Unwinding Triggers Market Concerns

Gold’s performance on the day stood out as the most anomalous move in the market.

Against a backdrop of a nearly flat U.S. dollar index and only a modest rise in Treasury yields, spot gold tumbled 4.4% to $4,070 per ounce—breaking below its March low and marking its lowest closing level since November 2025.

Silver declined by approximately 2% on the same day, bringing its cumulative loss over the past week to 13%.

Market participants interpreted gold’s unusual drop as forced liquidation driven by liquidity needs. Around 2:30 p.m. that afternoon, Bitcoin, U.S. Treasuries, and gold all fell simultaneously, exhibiting classic signs of margin calls and liquidity unwinding.

Bitcoin stabilized and rebounded near $61,000 that day, ending slightly higher, while Ethereum dropped 2.1% to $1,625.

Investors continued to sell off technology stocks on Monday, with the Nasdaq Technology Index closing down nearly 2.5% and the Semiconductor Index falling approximately 3.6%.

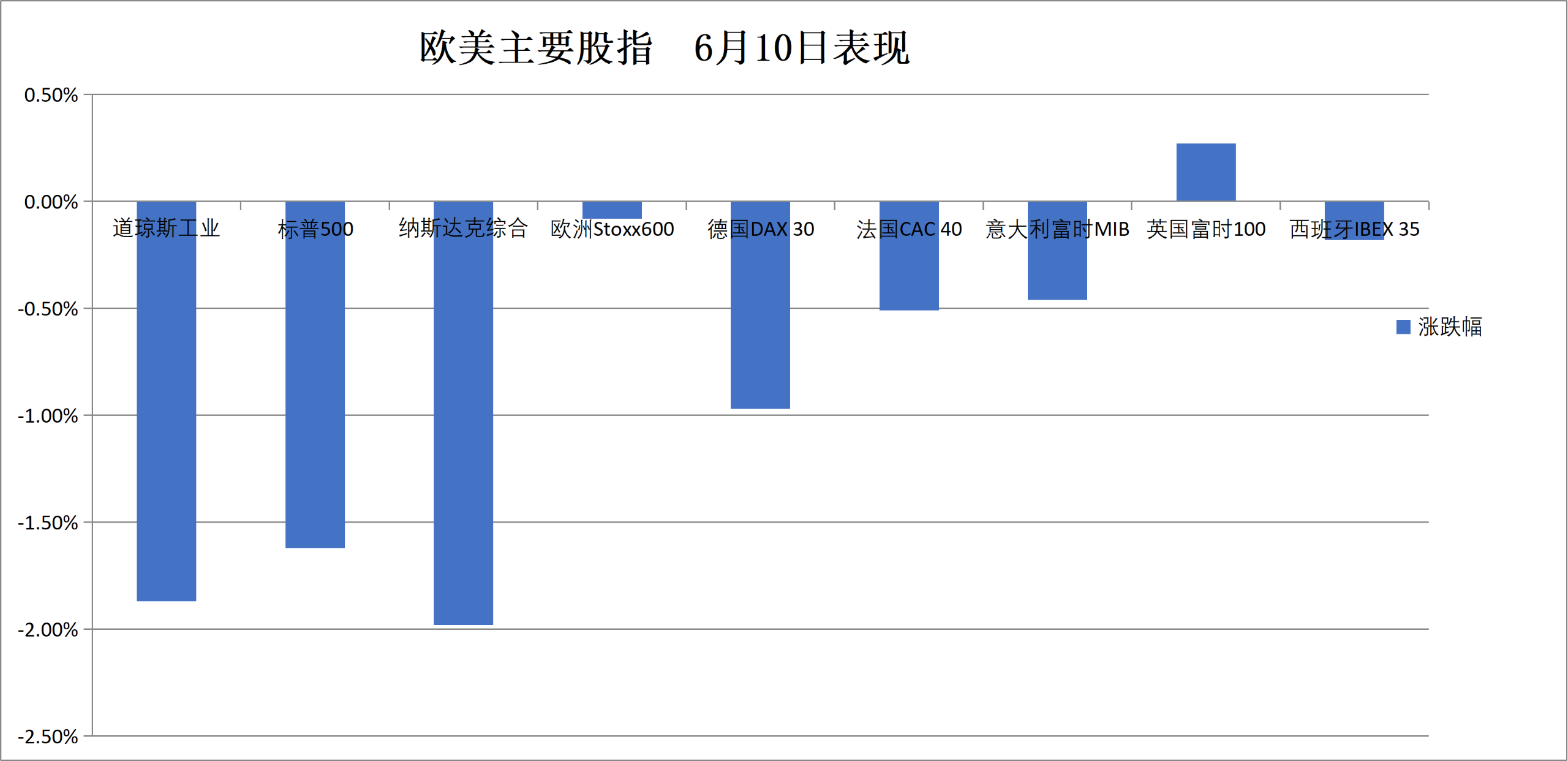

U.S. benchmark indices:

The S&P 500 Index closed down 119.66 points, or 1.62%, at 7,266.99.

The Dow Jones Industrial Average closed down 953.33 points, or 1.87%, at 49,918.78.

The Nasdaq Composite closed down 509.321 points, or 1.98%, at 25,169.501. The Nasdaq 100 Index closed down 576.472 points, or 1.98%, at 28,508.027.

The Russell 2000 Index closed down 1.10% at 2,835.462.

The CBOE Volatility Index (VIX) closed up 11.83% at 22.22.

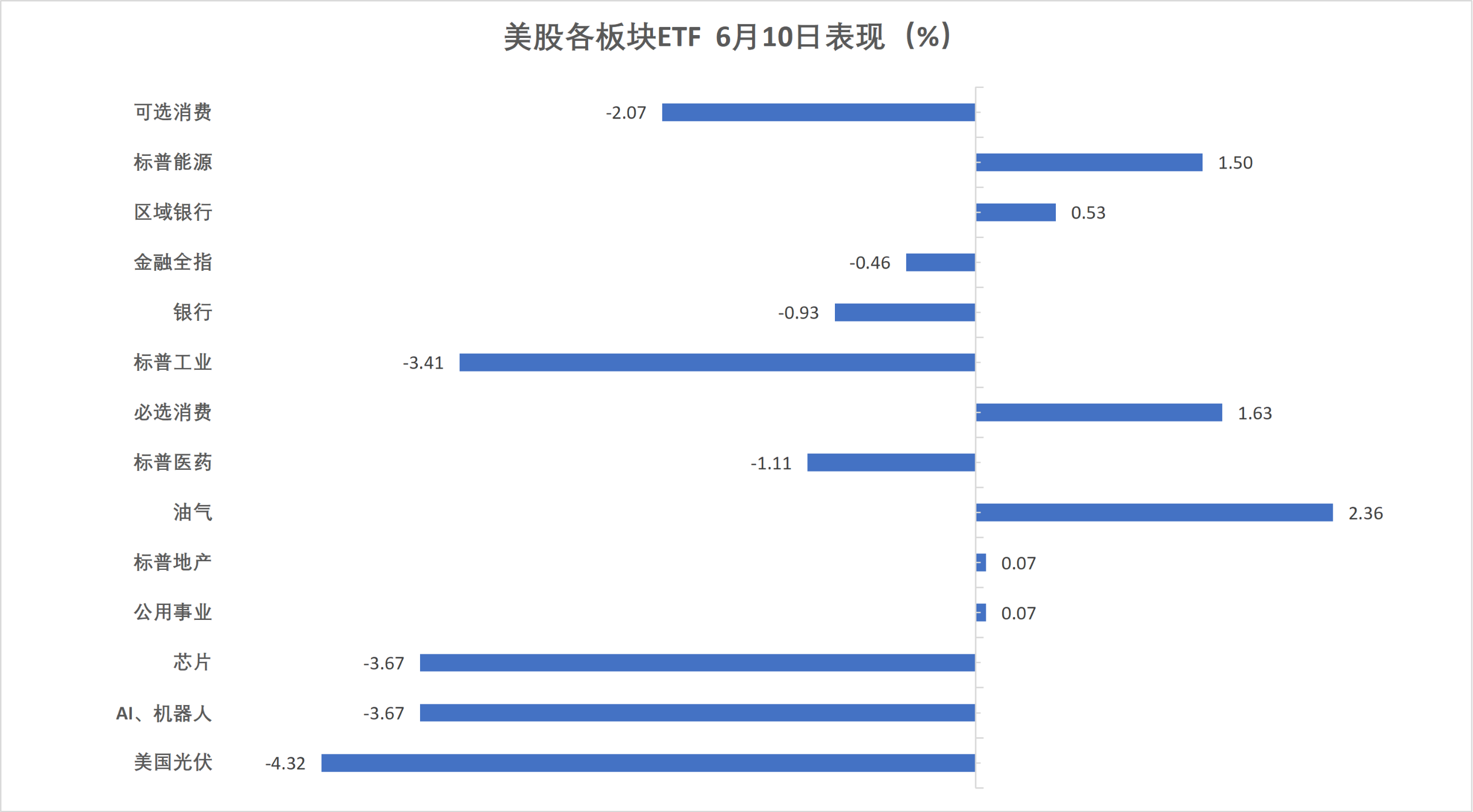

U.S. stock sector ETFs:

U.S. equity sector ETFs ended mixed, with the Global Airlines ETF down 4.59%, the Semiconductor ETF down 3.40%, and the Global Technology ETF, Technology Sector ETF, Consumer Discretionary ETF, Biotechnology ETF, and Internet Index ETF each falling by up to 2.29%.

Mag 7:

The Wind U.S. Magnificent 7 Index declined 2.17%.

$Apple (AAPL.US)$ edged up 0.35%, Microsoft fell 1.50%, $Alphabet-A (GOOGL.US)$ dropped 2.16%, Meta declined 2.33%, Amazon slid 2.53%, $NVIDIA (NVDA.US)$ fell 3.73%, Tesla dropped 3.8%.

Chip Stocks:

$PHLX Semiconductor Index (.SOX.US)$ closed down 451.348 points, or 3.57%, at 12,206.462.

Taiwan Semiconductor ADR fell 4.44%, AMD declined 4.86%, $Micron Technology (MU.US)$ fell nearly 5%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed down 0.28% at 6,280.80.

Among popular Chinese ADRs, $XPeng (XPEV.US)$ closed down 3.5%, $Alibaba (BABA.US)$ fell 3.3%, Baidu dropped 2.8%, ASE Technology Holding declined 2.4%, Tencent rose 2.6%, NetEase gained 4.1%.

Other individual stocks:

$Circle (CRCL.US)$ fell 2.70%.

Eurozone blue-chip stocks closed down more than 0.6%, with Siemens Energy falling approximately 6.5%. German equities ended nearly 1% lower, while the UK index rose about 0.3%.

Pan-European stocks:

The pan-European STOXX 600 Index closed down 0.08% at 618.17 points, showing a V-shaped intraday pattern and dropping to a new session low after 19:00 Beijing time.

The Eurozone STOXX 50 Index declined 0.66% to close at 6009.95 points.

Major Stock Indexes Around the World:

Germany's DAX 30 Index fell 0.97% to close at 24195.31 points, trading mostly lower throughout the day and continuing its downward trend since the European market open, with a sharp intraday drop after 19:00 Beijing time.

France's CAC 40 Index closed down 0.51% at 8161.83 points.

The UK’s FTSE 100 Index rose 0.27% to close at 10254.81 points.

Sector and individual stock performance:

Among Eurozone blue chips, Siemens Energy dropped 6.49%, SAP SE declined 3.23%, Adyen fell 2.43% (the third-largest decline), Hermès slid 1.8%, while TotalEnergies gained 1.01%.

Among all constituents of the STOXX 600 Index, Edenred plunged 7.85%, Aurubis dropped 7.64%, Wärtsilä Corporation fell 6.77%, and Siemens Energy posted the fourth-largest decline.

Abu Dhabi Murban crude oil futures rose 1.04% to $89.16 per barrel.

Crude Oil:

WTI July crude oil futures settled up $1.83, or 2.07%, at $90.03 per barrel.

Brent August crude oil futures settled up $1.65, or 1.80%, at $93.10 per barrel.

Abu Dhabi Murban crude oil futures rose 1.04% to $89.16 per barrel.

Natural Gas:

NYMEX July natural gas futures settled at $3.1850 per million British thermal units.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Stephen