Macroeconomic Highlights

Iran has denied Trump's claim of having 'directly spoken with Iranian officials.'

According to Iran’s Tasnim News Agency, senior Iranian officials stated that Trump’s assertion that Iranian officials had contacted him was entirely fabricated. Iran has had no contact with Trump and will respond militarily to acts of aggression. Trump’s ‘false claims’ about communication with Iranian officials were merely a ‘cover to avoid going to war with Iran.’

Trump claimed he had directly spoken with Iran, which allegedly requested an end to the bombing.

On the evening of June 10 Eastern Time, U.S. President Trump told Fox News in an interview that U.S. fighter jets were operating over Iranian airspace. He stated that he had 'spoken directly' with Iranian officials and that 'Iran has asked for the bombing to stop.' Trump said the 'bombing raids will cease soon,' but did not rule out launching additional strikes against Iran. He also claimed that Israel was not involved in these attacks targeting Iran.

On the evening of June 10 Eastern Time, U.S. President Trump told Fox News in an interview that U.S. fighter jets were operating over Iranian airspace. He stated that he had 'spoken directly' with Iranian officials and that 'Iran has asked for the bombing to stop.' Trump said the 'bombing raids will cease soon,' but did not rule out launching additional strikes against Iran. He also claimed that Israel was not involved in these attacks targeting Iran.

The U.S. military confirmed it had carried out strikes against Iran.

U.S. Central Command: At 5:15 p.m. Eastern Time on June 10, additional self-defense strikes were launched against multiple targets inside Iran. These strikes are in response to Iran’s unprovoked and ongoing acts of aggression.

Iran closes the Strait of Hormuz to all vessels

In the early hours of today (June 11) local time, the Khatam al-Anbia Central Headquarters of Iran's Armed Forces issued a statement announcing that, due to the volatile security situation in the region, the Strait of Hormuz is closed effective immediately to all types of vessels, including oil tankers and commercial ships, and that any vessel attempting to pass through the strait 'will be attacked.'

U.S. Media: Trump’s Two Additional Demands to Iran Delayed Deal Finalization

According to Axios, Trump was likely to have reached a preliminary agreement with Iran by the end of May if he had accepted the terms negotiated by his team last month. However, following a Situation Room meeting at the White House on May 29, Trump decided to add two additional demands: Iran must begin diluting its stockpile of enriched uranium within 60 days, and Iran must commit to imposing no tolls on vessels transiting the Strait of Hormuz. In exchange, Trump was willing to allow uranium dilution to take place within Iran under International Atomic Energy Agency (IAEA) supervision.

According to sources and U.S. officials, Iranian Foreign Minister Araghchi informed mediators and the U.S. that he needed four to five days to provide a response, but this ultimately turned into a wait of nearly two weeks. During this period, Trump grew increasingly frustrated as media reports continued to highlight his unfulfilled promise of an imminent deal—some even mocking him. Meanwhile, hardliners in the U.S. criticized him for being too soft on Iran. Compounding the situation, Iran—both publicly and privately—stated it wanted access to a portion of its frozen assets upfront, while Trump insisted that obligations under the agreement must be fulfilled first.

Economist: Inflation in line with expectations is not a positive signal; Trump must swiftly resolve the Strait issue to reassure the Federal Reserve

Brian Jacobsen, Chief Economist at Annex Wealth Management, stated that inflation data aligning with expectations does not necessarily mean it is a favorable report. He added that aggregate inflation figures have shown little evidence that rising energy commodity prices are spilling over into core prices. The clock is ticking loudly on reopening the Strait of Hormuz—whether through force or a ceasefire. The Federal Reserve will not speculate on when this might happen, so President Trump needs to provide certainty before the Fed’s next meeting.

U.S. inflation data presented a mixed picture, with the headline figure reaching a three-year high while core inflation showed signs of cooling.

According to CNBC, U.S. inflation heated up again in May, as rising energy costs intensified price pressures on consumers, though underlying inflation remained relatively moderate. Data released Wednesday by the U.S. Bureau of Labor Statistics showed that the Consumer Price Index (CPI), seasonally adjusted, rose 0.5% month-over-month and 4.2% year-over-year in May—both in line with market consensus expectations from a Dow Jones survey. This marks the first time in three years that the U.S. inflation rate has surpassed 4%. Although the sharp increase in energy prices has raised concerns about the economic outlook, the overall figures largely met expectations.

The year-over-year increase of 4.2% was not only higher than April’s 3.8%, but also the highest level since April 2023. However, excluding the volatile food and energy components, core CPI rose 0.2% month-over-month and 2.9% year-over-year in May. The year-over-year core CPI matched market expectations, but the month-over-month gain came in below the anticipated 0.3%, indicating that while underlying inflationary pressures have rebounded somewhat, the pace of acceleration was less severe than previously feared by markets.

U.S. Stock Market Update

All three major stock indices declined; most semiconductor stocks fell, while shale oil stocks rose against the trend.

All three major U.S. equity indices closed lower: the Dow Jones Industrial Average fell 1.87% to 49,918.78 points; the Nasdaq Composite dropped 1.98% to 25,169.50 points; and the S&P 500 declined 1.62% to 7,266.99 points.

$Star Tech Stocks (LIST2518.US)$Most stocks declined, with Broadcom down over 5%, Micron Technology and AMD each falling nearly 5%, Tesla and NVIDIA dropping close to 4%, Alphabet-A (Google) down more than 2%, Microsoft slipping over 1%, and Apple edging slightly higher.

$Popular Chinese Concept Stocks (LIST2517.US)$Mixed performance: the Nasdaq Golden Dragon China Index fell 0.28%, Taiwan Semiconductor dropped over 4%, Alibaba declined nearly 4%, Baidu fell 3%, Nio slid almost 2%, while Yum China rose over 2%.

$Semiconductors (LIST2015.US)$Most semiconductor stocks declined, with the Philadelphia Semiconductor Index down 3.57%. Qualcomm fell nearly 7%, Broadcom and ARM each dropped over 5%, Taiwan Semiconductor, Micron Technology, and AMD all declined more than 4%, and NVIDIA fell 3.7%.

$Shale Oil (LIST2585.US)$Most energy stocks advanced, with Devon Energy rising nearly 6%, Apache Corporation up almost 4%, ConocoPhillips gaining nearly 3%, Chevron increasing close to 2%, and Occidental Petroleum and Exxon Mobil both climbing over 1%.

Stock-specific news

Oracle fell over 10% in after-hours trading as its quarterly capital expenditures exceeded expectations.

Oracle (ORCL.US)Capital expenditures for the fourth fiscal quarter amounted to $15.9 billion, bringing total annual capital spending to $55.7 billion, above the previously projected $50 billion. Adjusted revenue came in at $19.18 billion, versus analysts’ expectation of $19.09 billion. Fourth-quarter software revenue was $6.82 billion, compared to an expected $6.88 billion; software license revenue was $1.88 billion, below the forecast of $1.93 billion; and software support revenue was $4.94 billion, slightly under the expected $4.98 billion.

Fourth-quarter Infrastructure-as-a-Service (IaaS) cloud revenue was $5.79 billion, exceeding analysts’ estimate of $5.72 billion. Total cloud revenue (IaaS + SaaS) for the quarter reached $9.91 billion, slightly below the expected $10 billion. The company reaffirmed its guidance for total revenue of $90 billion in fiscal year 2027. It also raised its adjusted earnings per share (EPS) outlook for fiscal 2027 to $8.05, in line with analyst expectations. For the first fiscal quarter, the company projects constant-currency revenue growth of 27%–29% and adjusted EPS of $1.72–$1.76, compared to the consensus estimate of $1.69.

Amazon secures $17.5 billion credit facility led by Citi

$Amazon(AMZN.US)$In a regulatory filing, the company disclosed that it has signed a $17.5 billion loan agreement with a syndicate led by Citigroup. According to the filing submitted on Wednesday, lenders agreed to provide this delayed-draw term loan (DDTL), with the facility available until the end of September this year. Each time Amazon draws on the credit facility, it must repay the borrowed amount within three years from the drawdown date. The loan’s interest rate will be set at SOFR (Secured Overnight Financing Rate) plus a margin of 62.5 to 87.5 basis points, depending on Amazon’s credit rating.

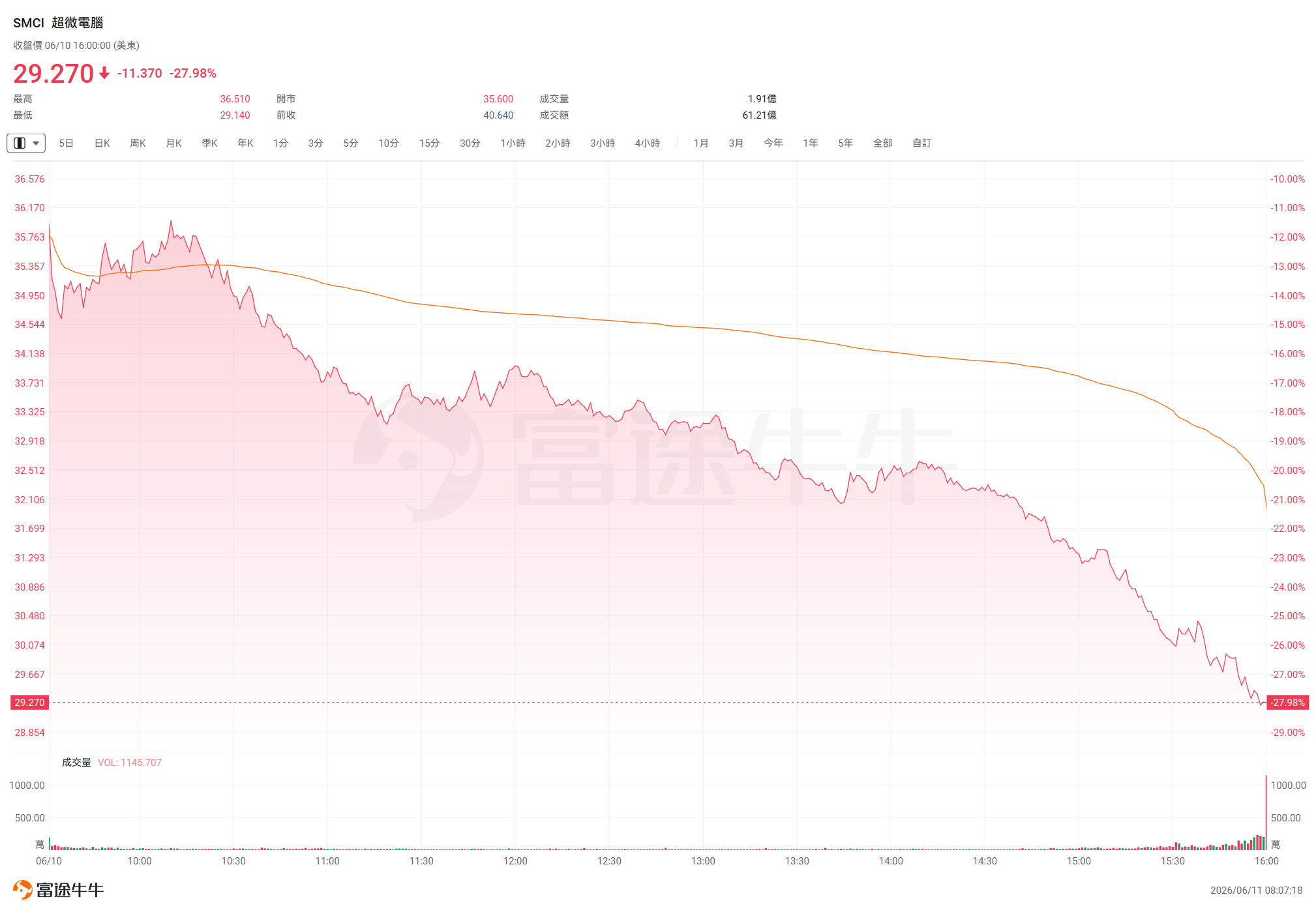

Super Micro Computer plummeted nearly 28% in the previous trading session and plans to raise $7 billion in equity financing to support its AI business.

$Super Micro Computer(SMCI.US)$announced plans for a $7 billion equity and equity-linked financing transaction to raise funds for procuring components to fulfill approximately $39 billion in customer orders for AI servers. The financing includes a $5 billion underwritten offering and a $2 billion at-the-market (ATM) equity offering.

SpaceX's IPO attracts billions of dollars in subscriptions from Middle Eastern sovereign wealth funds

SpaceX's initial public offering (IPO) has attracted billions of dollars in subscriptions from Middle Eastern sovereign wealth funds. According to informed sources, Saudi Arabia’s Public Investment Fund and Kuwait Investment Authority have each placed orders for shares valued between $1 billion and $5 billion. They also indicated that Qatar Investment Authority, with assets under management of $580 billion, may also make a significant investment commitment.

Google launches DiffusionGemma, an experimental open-source model

Google-A (GOOGL.US)Released the open-source experimental model DiffusionGemma, which disrupts the traditional token-by-token generation paradigm by generating 256 tokens in parallel during each forward pass. In real-world tests on H100 GPUs, it achieves over 1,000 tokens per second—up to a fourfold speedup. The model activates only 3.8 billion parameters and, when quantized, can run on consumer-grade GPUs with 18GB of VRAM, offering developers a new technical pathway for low-latency local workflows.

OpenAI founder Sam Altman expects OpenAI to go public within the next year

According to people familiar with the matter, OpenAI CEO Sam Altman sent an internal message to employees on Monday, indicating that OpenAI is expected to go public within the next year. The company is preparing a new artificial intelligence (AI) model. (The Information)

Sanofi fell more than 2% in the previous trading session after halting development of a rare disease drug following the failure of its Phase III trial

French pharmaceutical giant$Sanofi (SNY.US)$On Wednesday, the company announced it would terminate early a clinical study of an experimental drug for a rare autoimmune disease after the late-stage trial failed to demonstrate efficacy. This latest setback further intensifies the operational pressure on recently appointed CEO Belén Garijo.

Following the Phase III failure of riliprubart, market confidence in Sanofi’s R&D capabilities is likely to be further tested. Analysts note that new CEO Gary must quickly revitalize the company’s pipeline and improve clinical trial success rates; otherwise, Sanofi will struggle to navigate the earnings trough caused by the Dupixent patent cliff.

SK Hynix is reportedly set to list in the U.S. as early as August.

According to informed sources,SK Hynix (000660.KR)Plans to list in the U.S. as early as August. The U.S. Securities and Exchange Commission (SEC) is likely to approve SK Hynix’s American Depositary Receipt (ADR) listing application during the week of June 22. In a statement, SK Hynix said, “SK Hynix plans to issue American Depositary Receipts (ADRs) within 2026, but specific details, including size and timing, have not yet been determined.” SK Hynix announced in March that it had confidentially submitted its U.S. listing application. A source at the time indicated the offering could raise up to $14 billion.

Rocket Lab Founder: Only Two Companies Globally Have Achieved Scalable Space Launches—SpaceX and Rocket Lab

U.S. private space company$Rocket Lab (RKLB.US)$Peter Beck, founder and CEO, recently stated that to date, only two companies globally have truly achieved scalable and highly reliable orbital launches: SpaceX and Rocket Lab. During the development of the Electron small-lift launch vehicle, he systematically tracked 142 startups attempting the same mission, nearly all of which have since failed.

He emphasized that having ample funding does not guarantee success; near-perfect execution across all aspects is required. Beck defined Rocket Lab’s long-term goal as 'end-to-end control over the entire aerospace value chain.' Today, Rocket Lab is not only a launch service provider but also engages in satellite manufacturing, spacecraft component supply, and can deliver services directly from orbit.

$Alcoa Corporation (AA.US)$It fell more than 9% on the previous trading day, marking its worst single-day performance since April 2025. The chief financial officer stated that its alumina segment is under 'significant pressure' due to the war.

Top 20 by trading value

Hong Kong Market Outlook

Southbound capital increased its holdings of Hong Kong-listed stocks by over HK$8.2 billion, purchasing nearly HK$2 billion worth of Tencent shares, net buying over HK$1 billion of Yangtze Optical Fiber & Cable, and net selling nearly HK$2.4 billion of Alibaba.

On Wednesday, June 10, southbound capital recorded net purchases of HK$8.243 billion in Hong Kong stocks.

$Ying Fu Fund (02800.HK)$、Tencent (00700.HK)、$Yangtze Optical Fibre and Cable Joint Stock Limited Company (06869.HK)$Net purchases amounted to HK$4.056 billion, HK$1.995 billion, and HK$1.056 billion, respectively;

$Alibaba-W (09988.HK)$、$CNOOC Limited (00883.HK)$、$SMIC (00981.HK)$Net sales amounted to HK$2.372 billion, HK$195 million, and HK$962.7 million, respectively.

Ant International is considering raising USD 1 billion, potentially paving the way for a Hong Kong listing.

According to Bloomberg, citing people familiar with the matter, Ant Group’s international business is considering raising approximately USD 1 billion to accelerate its expansion. The funding round could value Ant International at USD 10 billion or more. The sources said the capital raise may help pave the way for a potential Hong Kong listing of Ant International as early as this year. They added that discussions regarding this funding round are still ongoing and no final decision has been made.

CSOP Asset Management refuted claims that leveraged ETFs exacerbated SK Hynix's stock price volatility.

According to Bloomberg, the fund manager of the largest leveraged exchange-traded fund (ETF) tracking SK Hynix recently refuted allegations that the USD 10 billion product is exacerbating share price volatility for the South Korean chipmaker. Wang Yi, Chief Investment Officer at CSOP Asset Management Limited, stated that the ETF listed in Hong KongSouthern Two-Times Leveraged Hynix (07709.HK)has virtually no correlation with SK Hynix stock price fluctuations. He noted that CSOP’s analysis found that even on some of the most volatile trading days for the stock this year, the daily rebalancing impact from the fund remained minimal.

Pop Mart: Non-Labubu products accounted for approximately 50% of total revenue in the U.S. market last year.

$Pop Mart (09992.HK)$Chief Operating Officer Si De disclosed segment data for Pop Mart’s largest overseas market, stating that non-Labubu products represented roughly 50% of total U.S. market revenue last year. He noted that in markets such as Japan, South Korea, and Southeast Asia, non-Labubu product lines already constitute the majority. He added that Pop Mart’s other IPs have also experienced strong growth and attracted a large user and fan base, though they have been overshadowed by Labubu—for example, the Starry People series.

Today's Focus

Keywords: U.S. PPI, SpaceX IPO pricing

On the economic data front, figures to be released include the ECB deposit facility rate as of June 11 for the euro area, the number of initial jobless claims in the U.S. for the week ending June 6, and the year-over-year U.S. PPI for May.

20:15 – ECB deposit facility rate as of June 11 for the euro area

20:30 – U.S. initial jobless claims for the week ending June 6

20:30 – U.S. May PPI year-over-year and month-over-month

Regarding financial results,$The Lovesac(LOVE.US)$released its earnings report before the U.S. market open,$Adobe(ADBE.US)$、$Lennar Corporation (LEN.US)$released its earnings report after the U.S. market close.

On the major events front,$SPACE EXPLORATION TECHNOLOGIES CORP(SPCX.US)$final pricing will be announced, and the World Cup kicks off today.

Looking to pick stocks or diagnose stock performance? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Looking to pick stocks or diagnose stock performance? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Editor/melody