Recently, a bearish research report on CPO (co-packaged optics) published by SemiAnalysis has stirred the optical communications market. The report noted that large-scale commercial deployment of CPO will be delayed until 2028–2029, hindered by low packaging yields, integration complexity, and insufficient cost advantages.

Morgan Stanley subsequently echoed this view, forecasting global optical engine shipments in 2027 to reach only 6–7 million units—far below the market’s expectation of 20–30 million units—and concluded that the true inflection point for CPO adoption may not arrive until 2028. The period from 2026 to 2028 will be a transitional phase characterized by coexistence among pluggable modules, near-packaged optics (NPO), and copper interconnects, with NPO serving as the 'middle ground' between CPO and conventional solutions.

The discourse between these two institutions may have shaken market assumptions about CPO’s rapid near-term adoption. Yet beneath this divergence, a more fundamental consensus is rapidly forming: while full-scale CPO rollout may require additional time, demand from AI clusters for high-bandwidth optical interconnects remains undiminished.

Against this backdrop of industrial dynamics and shifting expectations, near-packaged optics (NPO) has quietly moved to the center of the stage.

Against this backdrop of industrial dynamics and shifting expectations, near-packaged optics (NPO) has quietly moved to the center of the stage.

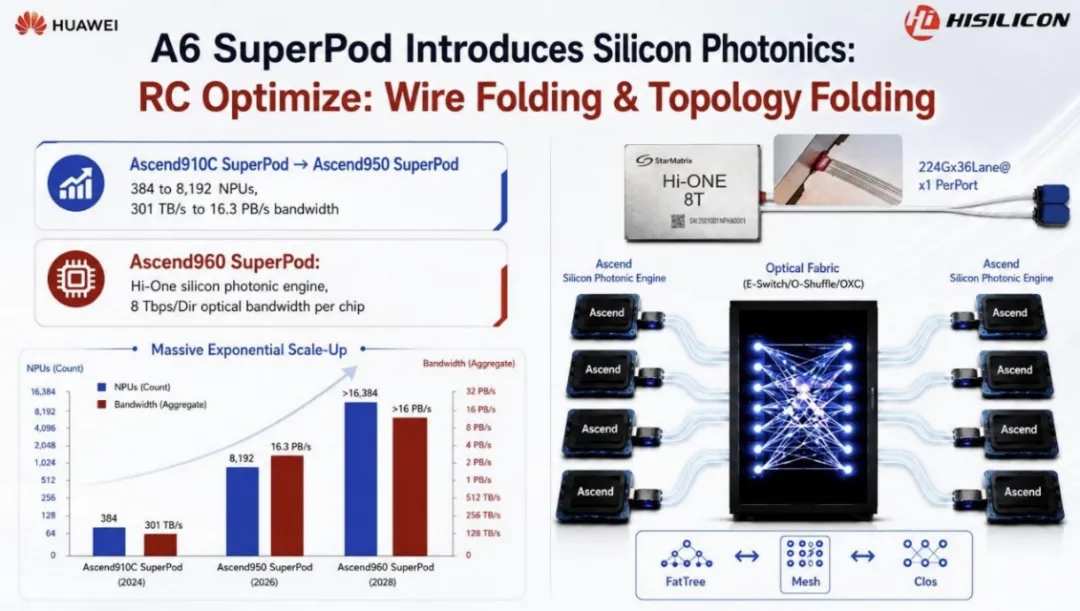

on$NVIDIA (NVDA.US)$In the newly unveiled Rubin Ultra NVL576 design, the number of NPO optical engines has nearly doubled, with the per-GPU optical engine capacity increasing from approximately 2.25 to roughly 4.0 at 3.2T, representing a 78% surge. At Huawei’s 2025 Global Connect event, the company’s Ascend roadmap explicitly confirmed the integration of its proprietary Hi-ONE silicon photonics engine into the Ascend 960 super node, delivering 8 Tb/s bandwidth per module and enabling all-optical interconnects within the super node.

Meanwhile,$Taiwan Semiconductor (TSM.US)$The silicon photonics integration platform COUPE is scheduled to enter mass production in 2026,$NVIDIA (NVDA.US)$、$Broadcom (AVGO.US)$、$Alphabet-A (GOOGL.US)$as substantial orders continue to materialize.

These strategic choices by industry leaders signal that NPO may already be becoming standard in leading-edge AI architectures. They collectively affirm that NPO is not a low-cost substitute for CPO, but rather the most immediately viable and commercially rational technological pathway in the ongoing evolution of AI clusters from copper-based to optical interconnects.

This trend invites deeper reflection: why has CPO, despite widespread enthusiasm, encountered significant deployment hurdles, while NPO has successfully bridged the final gap from lab to data center? What underlying industrial logic and competitive dynamics are shaping this shift in optical interconnect technology roadmaps?

Why NPO?

AI cluster scale expansion is pushing copper cabling to its physical limits.

It is widely recognized that the exponential growth in AI chip bandwidth is driving traditional copper interconnects to their physical limits.

From Blackwell to Rubin, per-chip bandwidth has advanced from hundreds of gigabits per second (Gb/s) to terabits per second (Tb/s), forcing the effective transmission distance of copper-based SerDes to shrink dramatically from the traditional 100 cm to just 5 cm. As communication rates scale to multiple Tb/s per chip, copper cabling is failing across multiple dimensions—distance, power consumption, thermal management, and routing density. SerDes transmission distances are drastically compressed, cables become excessively bulky, panel installation becomes impractical, and thermal and power delivery margins are exhausted.

Under this trend, upgrading intra-rack connectivity from copper to optical interconnects has become an irreversible trajectory for industry evolution.

by$NVIDIA (NVDA.US)$Take the Rubin Ultra NVL576 architecture as an example: rather than adopting a radical all-optical interconnect solution, the system employs a hybrid copper-optical architecture that balances cost and performance—a design that currently represents the dominant implementation in the industry.

Within a single NVL72 rack, short-reach GPU interconnects continue to use copper cables, leveraging their advantages of low cost, low latency, and flexible routing to ensure efficient communication among high-density compute units inside the rack. However, the NVL576 system, composed of eight interconnected NVL72 racks, fully adopts optical interconnect solutions such as NPO and CPO for long-reach, high-bandwidth inter-rack connections, thereby completely overcoming the signal attenuation bottleneck inherent in long-distance copper transmission and enabling stable operation of the 576-GPU hyperscale cluster.

This marks the first time optical interconnects have moved beyond data-center-scale Scale-out scenarios into rack-scale Scale-up scenarios, gradually blurring established industry boundaries.

Across the industry, the transition from copper to optical interconnects within racks is now an inevitable trend. As cluster sizes exceed hundreds or even thousands of GPUs, copper’s triple constraints—power consumption, bandwidth, and reach—are magnified exponentially, accelerating the adoption of optical interconnects and creating fertile ground for NPO technologies.

Demand convergence triggers a 'positioning race' among supply chain players.

On the other hand, global AI computing giants are simultaneously betting on NPO, generating strong demand convergence, which is also driving$Alphabet-A (GOOGL.US)$、$Alibaba (BABA.US)$、$TENCENT (00700.HK)$Domestic and international cloud providers have followed suit, transforming NPO from a single-vendor solution into an industry-wide consensus.

As a bellwether in AI computing, NVIDIA’s NVL576 architecture—mentioned earlier—has become the core engine driving NPO volume adoption. This architecture continues its hybrid copper-optical design, increasing the number of 3.2T NPO optical engines per GPU by 78%, nearly doubling the total optical engine count.

According to broker forecasts, NVL576 system shipments could reach 8,300 units by 2027, translating into demand for approximately 21.6 million fiber array units (FAUs)—a massive volume that will directly drive full-scale capacity ramp-up across upstream optical component suppliers. Jensen Huang has explicitly stated that the next-generation Feynman architecture will debut in 2028. Each architectural upgrade brings further increases in optical engine density.

Huawei is also accelerating this trend.

At its 2025 Global Connect Conference, Huawei unveiled a three-year roadmap for its Ascend AI chips, planning to launch a series of products—including the 950PR, 950DT, 960, and 970—between 2026 and 2028, targeting near-annual generational upgrades with doubled compute performance each time.

The Hi-ONE optical engine was specifically developed to support this continuously expanding cluster scale—it reduces the required SerDes transmission distance from approximately 100 cm to about 5 cm, while extending the optical reach from under 1 meter to 100 meters, making physically feasible distributed, gigawatt-scale hyperscale data centers that span multiple clusters.

In the upgrade path from Ascend 950 to Ascend 960 series chips, Huawei integrates the Hi-ONE NPO optical engine, achieving a per-module bandwidth of 8 Tb/s—placing it among the industry leaders. According to the roadmap, Ascend cluster scale will expand from the Ascend 910C SuperPod (2024), which houses only 384 NPUs, to the Ascend 950 SuperPod (2026) with 8,192 NPUs, increasing total bandwidth from 301 TB/s to 16.3 PB/s. The deployment of these tens-of-thousands-of-chip supercomputing clusters will continue to drive iterative development and shipments of high-specification NPO products.

Meanwhile, Huawei’s Hi-ONE solution innovatively adopts a DSP-free, fully optical scaling architecture, streamlining signal processing units to further reduce power consumption and latency, thereby establishing a differentiated technical approach distinct from overseas vendors.

Driven by these two industry leaders, key global players across the supply chain are rapidly entering the market and securing strategic positions.

$Taiwan Semiconductor (TSM.US)$COUPE's silicon photonics integration platform will enter mass production in 2026, integrating electrical and optical ICs and leveraging advanced packaging technologies such as CoWoS and SoIC, thereby becoming a "key cornerstone" of the CPO/NPO industry chain.

In early 2026, Google officially placed a purchase order for 12 million NPO optical modules to support the deployment of its next-generation TPU v7/v8 computing clusters, with deliveries concentrated between Q3 2026 and Q2 2027.$Alibaba (BABA.US)$、$Amazon (AMZN.US)$、$Microsoft (MSFT.US)$、$TENCENT (00700.HK)$Other cloud service providers are also advancing in-rack optical interconnect upgrades within their new-generation server clusters. The industry has converged on a consistent strategic direction centered around Scale-up high-density architectures, rapidly accelerating NPO adoption and simultaneously driving sustained growth in demand for upstream core components such as InP lasers and silicon photonics chips.

In early June 2026, Lightmatter officially announced its entry into NVIDIA’s NVLink Fusion ecosystem, unveiling its Passage CPO and NPO products, which reportedly reduce fiber and connector requirements by 50%, thereby addressing the bandwidth bottlenecks limiting AI cluster scalability. This collaboration marks optical interconnect technology as an official component of NVIDIA’s AI factory architecture. By joining the NVLink Fusion ecosystem, Lightmatter will enable customers’ semi-custom XPUs to directly connect to NVIDIA switching chips via its CPO and NPO products, facilitating high-bandwidth, low-latency interconnects across vendor boundaries within the ecosystem.

$Broadcom (AVGO.US)$Also in 2026, Broadcom launched the industry’s first 3nm 400G-per-lane optical PAM-4 digital signal processor, Taurus™ BCM83640, supporting 1.6T transceivers and various linear optical devices. Notably, Broadcom introduced a VCSEL-NPO engine solution tailored for AI Scale-up networks, offering exceptional energy efficiency of approximately 1 pJ/bit and a breakout bandwidth density exceeding 0.6 Tbps/mm, while promising cost competitiveness comparable to active copper cables—delivering a highly compelling optical interconnect solution for next-generation AI infrastructure.

Additionally, Israeli fabless semiconductor company NewPhotonics has also launched an NPO solution, further enriching the NPO industry ecosystem.

Notably, demand resonance has extended beyond NPO itself. Citi forecasts that Scale-up-oriented CPO switches will begin deployment by the end of 2027, with demand reaching 169,000 units that year. NPO is catalyzing a broader optical interconnect ecosystem rather than merely enabling a one-for-one product substitution.

The surge in end-market demand has unlocked significant near-term growth potential for the NPO segment.

From a per-unit perspective, NPO modules typically consume around 9W of power, offering clear energy efficiency advantages over conventional pluggable optical modules and aligning closely with data centers’ core objectives of cost reduction and operational efficiency. This positions 2026–2027 as a period of explosive NPO deployment. NVIDIA’s NVL576 product line alone is expected to generate tens of millions of optical engine units in demand, serving as a cornerstone driver for sector growth.

Globally, the NPO market reached USD 3.8 billion in 2025. Industry analysts project that the NPO market will grow at a compound annual growth rate (CAGR) of 19.3% from 2026 to 2034, expanding to USD 18.6 billion by 2034—a nearly fivefold increase over the decade, reflecting substantial growth potential.

It is evident that the investment and industrial value of the NPO segment has gained universal market recognition. The rise of NPO represents not merely a shift in technological pathways, but a systemic restructuring of value distribution across the supply chain. Optical engine manufacturers are capturing higher added value, silicon photonics penetration is accelerating rapidly, packaging platforms have become critical strategic footholds, and global giants are intensifying their involvement. Collectively, these developments point to a singular conclusion: NPO is transforming the optical communications industry from a standardized component model toward a high-value systems integration paradigm.

The Technology Roadmap Competition: The Key to NPO's Success

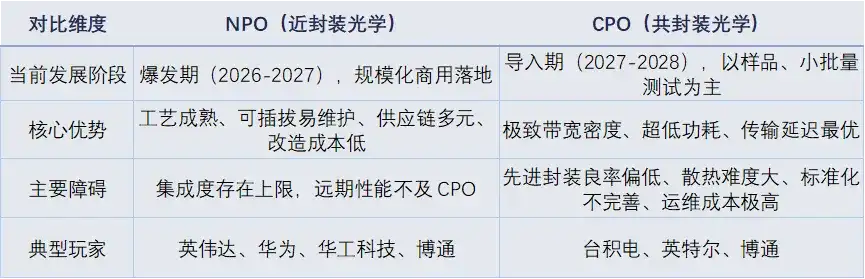

During the evolution of AI optical interconnects, multiple technical pathways—including pluggable optical modules, NPO (Near-Package Optics), CPO (Co-Packaged Optics), and OCS—are developing in parallel, resulting in a far more fragmented landscape than the market anticipated. In this protracted technology roadmap competition, NPO has emerged as the transitional solution bridging conventional approaches and ultimate technologies, thanks to its precise positioning, balanced performance, and practical deployment advantages.

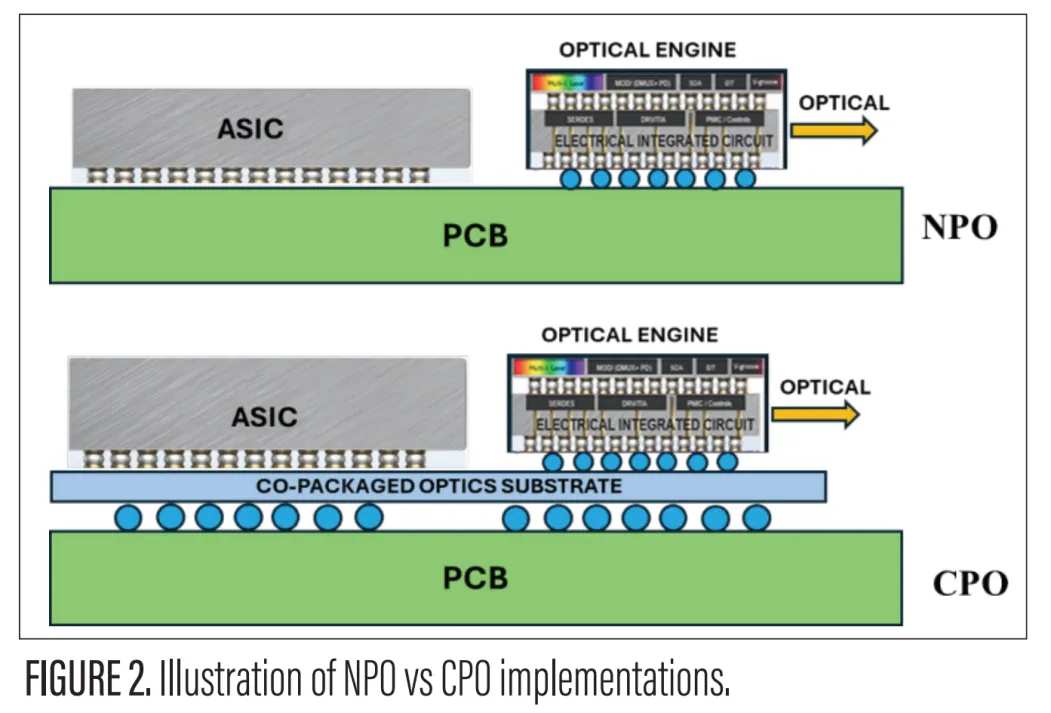

From a technological standpoint, the evolution of optical interconnects follows a clear gradient of integration: pluggable optical modules → NPO (Near-Package Optics) → CPO (Co-Packaged Optics). These three approaches exhibit distinct differences in optical engine placement, integration complexity, and operational maintainability. Each step up this integration ladder trades off some degree of serviceability for higher bandwidth density and lower power consumption.

Traditional pluggable optical modules position the optical engine on the front panel of equipment, resulting in the longest electrical transmission path and relatively higher power consumption and latency. However, their strengths lie in high standardization, ease of hot-swappable maintenance, and a mature supply chain ecosystem, making them the dominant solution in today’s data centers.

NPO places the optical engine on the same substrate as the ASIC but in a physically separate area, significantly shortening the electrical transmission path and thereby reducing power consumption and latency. It retains the optical engine’s independent pluggability while achieving a pragmatic balance among integration level, thermal management, maintenance costs, and supply chain ecosystem maturity.

CPO, by contrast, fully integrates the optical engine and ASIC within the same package, compressing the electrical path to the micrometer scale and achieving optimal signal integrity. However, this comes at the cost of a closed ecosystem, lack of hot-pluggability, and significant thermal challenges. Mass production remains extremely difficult due to an 'impossible triangle' of reliability, cost, and serviceability that cannot be simultaneously optimized.

As one industry expert succinctly defined it: the fundamental distinction between CPO and NPO lies in whether the optical engine and ASIC share the same substrate.

For a long time, the market assumed CPO would ultimately replace NPO. However, from the perspectives of technological form, commercialization progress, and deployment scenarios, the relationship between NPO and CPO may not be one of simple substitution, but rather a question of which better aligns with the current stage of industrial development.

From the perspective of technical architecture and commercialization progress, although CPO holds theoretical performance advantages, it currently faces multiple industrialization bottlenecks. On one hand, CPO imposes extremely high requirements on advanced packaging, optical coupling, and chip integration processes; yields for silicon photonics chips and opto-electronic co-packaging remain difficult to scale up rapidly, keeping mass production costs persistently high. On the other hand, CPO deeply integrates optical engines with main chips, meaning that a failure in the optical component could render the entire high-value ASIC chip unusable, significantly increasing repair complexity and equipment loss risk. Moreover, the current CPO supply chain is highly concentrated, with a multi-vendor ecosystem yet to emerge; leading cloud providers and compute infrastructure vendors are therefore adopting a cautious stance due to supply chain security concerns.

In contrast, NPO is based on an iterative evolution of mature manufacturing processes and does not require disruptive changes to existing chip packaging systems. Its yield rates and costs in mass production are already under control. Furthermore, NPO retains a pluggable design, allowing optical engines to be independently removed and replaced—seamlessly integrating with data centers’ existing operational and maintenance frameworks. A mature, multi-supplier ecosystem has already formed around NPO, resulting in minimal barriers to commercial deployment.

From the standpoint of application scenarios, the boundaries between the two technologies are also clear: for today’s mainstream Scale-up, high-density computing clusters—particularly GPU-direct interconnect scenarios—NPO offers the best overall cost-performance ratio and has become the preferred choice among vendors. CPO, meanwhile, targets future ultra-high-density switching nodes and premium custom clusters with extreme energy efficiency requirements, making widespread adoption unlikely in the near term. Technologies such as OCS and upgraded CPO variants will find value in specific, niche cluster applications.

Beyond technical specifications, NPO’s lead over CPO in commercial deployment fundamentally reflects a pragmatic industry-wide decision driven by core considerations including cost, supply chain resilience, and operational maintainability—a clear sign of market rationality returning to center stage.

Balancing Performance and Cost: 3.2T NPO has already reached mature mass production, with confirmed orders scheduled for delivery by 2026. HG Tech has already begun volume shipments of its 3.2T NPO products to leading customers, with a clear roadmap for further scaling. While CPO has a well-defined long-term roadmap for speeds beyond 3.2T, it remains in a phase of high R&D costs and low yields in the short term, making it incapable of supporting deployments at the tens-of-millions scale.

Restructuring Supply Chain Leverage: A unique advantage of NPO lies in its ability to expand the value proposition and assembly role of optical module vendors. If CPO were to become dominant, advanced packaging platforms—and their controlling entities—would gain overwhelming influence across the supply chain. In contrast, NPO preserves external manufacturing capacity for optical engines and maintains pluggability, granting OEMs/ODMs renewed bargaining power. This elevates silicon photonics design firms and optical module manufacturers from mere 'assemblers' to core participants in the ecosystem.

Risk Mitigation on the Customer Side: Cloud providers and AI chip vendors exercise great caution in selecting technology paths, favoring solutions that offer strong serviceability, low technological lock-in, and a robust multi-vendor supply ecosystem. NPO precisely meets these requirements, whereas CPO’s closed ecosystem and high maintenance costs are not fully aligned with the operational logic of CSPs (Cloud Service Providers) focused on large-scale deployment.

In the long run, CPO undoubtedly represents the ultimate technological direction—offering unparalleled integration density, superior power efficiency, and bandwidth density, embodying the ideal vision for optical interconnects. However, during the 2026–2027 window, comprehensive considerations around technological maturity, supply chain readiness, and customer acceptance have positioned NPO as an indispensable bridge. Its value does not stem from being cutting-edge, but from being 'just right'—perfectly matching the urgent demand of current AI clusters for high-bandwidth optical interconnectivity.

Bernstein’s research report states bluntly that although CPO offers advantages in power consumption and cost, its widespread adoption is unlikely before 2028 due to manufacturing and maintenance challenges. In contrast, NPO can be rapidly deployed using mature processes and benefits from a multi-vendor ecosystem and significantly lower maintenance costs. From the customer perspective, CSP clients generally favor the more maintainable NPO solution, viewing it as a technology choice suitable for longer-term use.

CICC also forecasts that, thanks to NPO’s advantages in maintenance costs, reliability, and replicability across the supply chain, large-scale NPO orders on the Scale-up side are expected to materialize first among certain CSP clients as early as 2027.

How long will NPO’s window of opportunity last?

By integrating the maturity timelines of various technical approaches, customer deployment plans, and industry growth data, the development cycles of NPO, silicon photonics, CPO, and upstream core materials can be divided into two phases—short-term and medium-to-long-term—to forecast the sector’s evolution over the coming years.

Short-term surge (2026–2027): Mass adoption of NPO

The period 2026–2027 will be the golden growth phase for NPO and the core stage for revenue realization in this sector. The global NPO market’s compound annual growth rate (CAGR) of 19.3% will be largely realized during this window.

The primary driver of this growth wave stems from large-scale orders placed by leading customers: mass shipments of NVIDIA’s NVL576 series racks, full-scale deployment of Huawei’s Ascend 950/960 clusters, large-scale rollout and continuous expansion of Google’s TPU v7/v8 systems, and accelerated investments by other industry players—all generating substantial demand for NPO products. Additionally, the low power consumption of NPO modules—around 9W—aligns with data centers’ energy efficiency and carbon reduction goals, further accelerating adoption by smaller cloud providers and computing enterprises. During this phase, the sector’s focus will center on capacity ramp-up and shipment growth of NPO systems, optical engines, and associated components.

Medium-to-long-term evolution (2028–2031): Silicon photonics and CPO take over

In the medium to long term, starting from 2028 onward, the growth dynamics of the optical interconnect industry will gradually shift. NPO’s growth rate may moderate, while silicon photonics and CPO technologies emerge as the new core growth engines, driving the industry toward higher integration levels and greater bandwidth density.

The growth trajectory for silicon photonics is clear. According to GM Insights, the global silicon photonics market is projected to expand from USD 2.3 billion in 2026 to USD 7.0 billion by 2031, reaching USD 17.8 billion by 2035—a CAGR of 25.3% over the 2026–2035 forecast period. LightCounting further predicts that by 2031, silicon photonic chips will account for 42% of the total optical chip market, becoming the dominant force. Optical interconnect applications will also continue evolving—from today’s Scale-out architectures toward Scale-up vertical scaling, and ultimately into the longer-horizon vision of Scale-in, featuring integration within chips themselves.

At the roadmap level, following several years of technological refinement, yield optimization, and ecosystem maturation, CPO is expected to reach a production peak around 2028, primarily targeting high-end switching nodes and chip-level interconnect applications, thereby establishing a differentiated development path relative to NPO. By then, NPO’s role will gradually transition from its current dominant position to that of a coexisting solution, maintaining long-term coexistence with CPO in specific scenarios.

In short, a trend toward technological diversification is rapidly taking shape: NPO is leading in volume deployment, CPO is poised for growth, and XPO—an emerging high-density, liquid-cooled, pluggable optical form factor designed for next-generation AI data centers—is beginning to enter industry consideration and is expected to coexist with NPO and CPO over the long term.

Final Remarks

Underlying the competition among technical roadmaps is the dynamic alignment between the evolution of AI computing architectures and the maturity of optical interconnect technologies.

The industry’s evolution—from copper cables to optical interconnects, and from pluggable modules to NPO and CPO—has never been a zero-sum game of mutually exclusive choices, but rather a protracted process of complementary pathways and gradual upgrades.

The sudden rise of NPO marks precisely the opening chapter of this extended cycle—a new starting point for the AI optical interconnect industry’s journey toward an era of diversification, high density, and fully optical interconnectivity.

Editor/melody