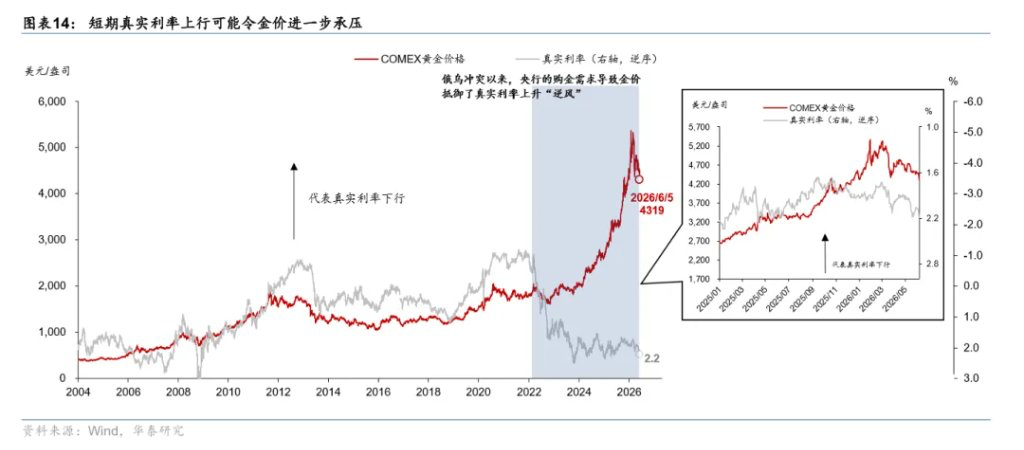

Gold prices have retreated more than 20% from their March peak, entering a technical bear market. Market pricing dynamics have shifted from geopolitical risk to interest rates and inflation—U.S. CPI rose to 4.2% in May, fueling expectations of rate hikes and driving up the dollar and U.S. Treasury yields, which exerted downward pressure on non-yielding gold. In the short term, gold continues to face triple headwinds from interest rates, the U.S. dollar, and liquidity; however, over the longer term, global debt expansion, central bank gold purchases, and de-dollarization trends remain intact.

After a rally that repeatedly hit record highs this year, gold is now undergoing its sharpest correction in recent years.

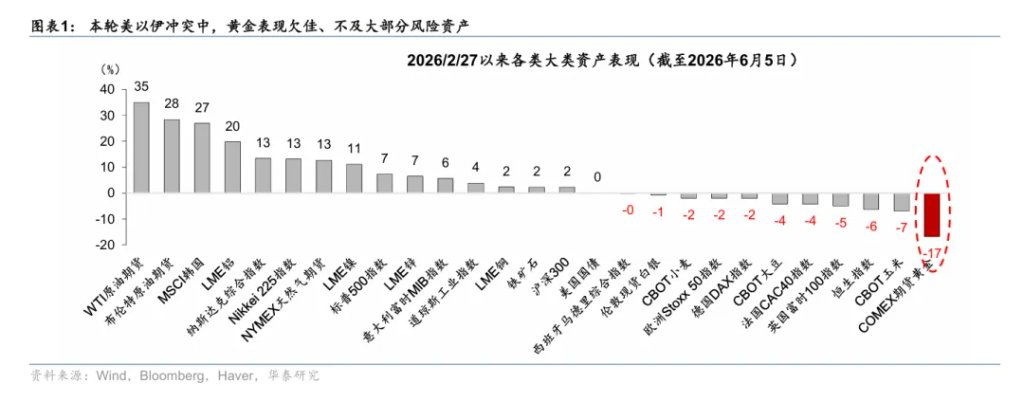

Against the backdrop of escalating Middle East conflicts and global energy supply concerns triggered by the blockade of the Strait of Hormuz, gold has not only failed to demonstrate the resilience typical of a traditional safe-haven asset but has also declined by more than 20% from its March peak, officially entering a technical bear market. This unusual behavior suggests that geopolitical risk is no longer the dominant driver of gold pricing; instead, it is being reshaped by repricing dynamics related to inflation, interest rates, and liquidity.

With the U.S. Consumer Price Index (CPI) rising 4.2% year-over-year in May—the highest level since 2023—market expectations for a Federal Reserve rate hike this year have surged. According to CME FedWatch data, the probability of a 25-basis-point rate increase in December has risen to 43%, up from 14% a month ago. The U.S. dollar index has climbed to a near two-month high, and Treasury yields continue to rise, exerting significant pressure on non-yielding gold.

With the U.S. Consumer Price Index (CPI) rising 4.2% year-over-year in May—the highest level since 2023—market expectations for a Federal Reserve rate hike this year have surged. According to CME FedWatch data, the probability of a 25-basis-point rate increase in December has risen to 43%, up from 14% a month ago. The U.S. dollar index has climbed to a near two-month high, and Treasury yields continue to rise, exerting significant pressure on non-yielding gold.

Meanwhile, gold’s correlation with risk assets is strengthening. FactSet data shows that since June, the correlation coefficient between gold and the Nasdaq 100 Index has reached as high as 0.91. When both geopolitical and inflation risks rise simultaneously, investors tend to favor cash, the U.S. dollar, and bonds over gold, causing this traditional safe-haven asset to lose its historical independent pricing mechanism.

Although most institutions still maintain a long-term bullish outlook on gold, in the near term, developments in the Strait of Hormuz, tightening global liquidity, and rising real interest rates could continue to weigh on gold prices.

Interest Rates Have Become Gold’s ‘Biggest Enemy’

The primary driver behind gold’s recent decline is not geopolitics, but interest rates.

U.S. Bureau of Labor Statistics data shows that the CPI rose 4.2% year-over-year in May, marking its highest level in over two years. Meanwhile, U.S. nonfarm payrolls increased by 172,000, significantly exceeding market expectations and reinforcing perceptions of U.S. economic resilience.

Chris Gaffney, Head of Global Markets at EverBank, stated that the recent sell-off in gold is essentially a result of repricing expectations around the interest rate path. As markets shift focus from rate cuts to potential hikes, the opportunity cost of holding gold has risen markedly.

Market data shows that the yield on the U.S. 30-year Treasury has surpassed 5%, while the 10-year Treasury yield has climbed above 4.5%. For gold—a non-income-generating asset—higher real interest rates translate into reduced attractiveness.

As a result, Citi analyst Kenny Hu’s team lowered its three-month gold price target from USD 4,300 to USD 4,000 and warned that if the Strait of Hormuz remains blocked into late summer, gold prices could even fall toward USD 3,500.

Why Has the Hormuz Crisis Not Pushed Gold Prices Higher?

Conventional wisdom holds that war is bullish for gold. However, the current Middle East conflict has produced a markedly different outcome.

Multiple institutions believe the key reason is that this conflict initially disrupted energy supply rather than the financial system itself. The blockade of the Strait of Hormuz caused a sharp rise in oil prices, fueling global inflation expectations. In this context, market concerns have shifted away from safe-haven demand toward the likelihood that central banks will maintain high interest rates—or even hike them further.

Research institutions note that the surge in oil prices has created not a typical safe-haven environment, but rather a stagflation-like macroeconomic shock. Rising energy costs are squeezing global demand and liquidity, dragging down the performance of most assets—excluding energy—including precious metals and industrial raw materials.

From this perspective, gold is not benefiting as a safe-haven asset; instead, it is among the victims of the liquidity contraction triggered by the energy shock.

Gold Is Losing Its Status as an Independent Safe-Haven Asset

More notably, the correlation between gold and risk assets has significantly strengthened.

Michael Armbruster, co-founder of Altavest, stated that gold has recently moved almost in lockstep with U.S. equities. Gold rises when the Nasdaq rises and faces selling pressure when the Nasdaq declines.

Market analysts believe that in times of tightening liquidity, gold is increasingly viewed as a source of funding rather than a safe-haven asset.

This trend is also evident in ETF fund flows. Over the past two years, AI-related assets have consistently attracted global capital inflows, while gold ETFs have significantly underperformed. As funds concentrate into AI, semiconductors, and leveraged products, gold has gradually lost its previous status as a safe-haven asset.

Meanwhile, gold recently fell below its 200-day moving average for the first time in two and a half years. Ole Hansen, Head of Commodity Strategy at Saxo Bank, noted that this represents a major setback for a technical bull market that had persisted for four years and has triggered additional exits by systematic and trend-following funds.

Central bank buying and de-dollarization rationale remain intact

Despite near-term pressures, most institutions have not abandoned their long-term bullish outlook on gold. Citi maintains its $5,000 price target for the next six to twelve months. Yardeni Research likewise keeps its year-end target of $5,500 and long-term forecast of $10,000 unchanged.

The core rationale underpinning this long-term view remains unchanged. First, global debt levels continue to rise. The market widely believes that in a high-debt environment, central banks will struggle to sustain high interest rates over the long term, making monetary easing the prevailing direction ahead.

Second, demand from central banks for gold remains robust. In recent years, central banks have been the most consistent source of buying in the gold market. For many countries, gold is no longer merely a safe-haven asset but an essential reserve instrument for mitigating risks associated with the U.S. dollar system.

Furthermore, evolving geopolitical dynamics and the ongoing restructuring of the international monetary system continue to support gold’s strategic allocation value. Christopher Louney, analyst at Royal Bank of Canada Capital Markets, believes the recent pullback in gold prices reflects a temporary waning of market interest rather than a fundamental breakdown of the long-term thesis.

Market focus centers on two key variables

For gold, future price direction will largely hinge on two critical variables.

The first is when the Strait of Hormuz resumes normal shipping operations. If energy supplies gradually recover and oil prices retreat, market concerns over inflation and further rate hikes will ease somewhat.

Second is when U.S. Treasury yields will peak. Currently, the greatest pressure on gold stems from persistently rising real interest rates. If the Federal Reserve concludes its 'price discovery' phase and bond markets regain stability, the liquidity headwinds facing gold are expected to ease.

Therefore, in the short term, gold remains under triple pressure from interest rates, the U.S. dollar, and liquidity. As summarized in a Huatai Securities report: 'Until the strait opens, gold struggles to rise.'

However, over a longer horizon, factors such as global debt expansion, central bank gold purchases, de-dollarization, and rising fiscal deficits remain unchanged. This suggests that the current bear market resembles a sharp correction within a prolonged bull market, rather than the end of the uptrend.

Editor/Deng