The European Central Bank raised interest rates by 25 basis points as expected on Thursday, increasing the deposit facility rate from 2% to 2.25%. This marks the central bank's first rate hike in three years.

Zhitong Finance APP learned that the European Central Bank (ECB) raised interest rates by 25 basis points as widely expected on Thursday, increasing the deposit facility rate from 2% to 2.25%. This marks the first rate hike by the central bank in three years. The ECB stated that, amid intensifying inflationary pressures, it could no longer afford to wait until hostilities in the Middle East subside before acting. Although markets currently anticipate another 25-basis-point rate hike by the ECB in September, the central bank reiterated that it would not pre-commit to any future policy path and emphasized its capacity to navigate the current environment of heightened uncertainty.

In its statement, the ECB said: 'The outlook remains uncertain, with upside risks to inflation and downside risks to economic growth.' 'The full impact of the war on medium-term inflation and growth will depend on the magnitude and duration of the energy price shock, as well as the scale of its indirect effects and second-round impacts.'

This rate hike by the ECB represents the first policy response by a major economy’s central bank to the surge in energy prices triggered by the conflict in the Middle East. With the conflict now entering its fourth month, eurozone officials are concerned that inflationary pressures are no longer confined solely to the energy sector. Even if the United States and Iran were to reach a peace agreement soon, damage to energy infrastructure in the region implies that restoring production capacity will take time, meaning inflation may not ease readily.

This rate hike by the ECB represents the first policy response by a major economy’s central bank to the surge in energy prices triggered by the conflict in the Middle East. With the conflict now entering its fourth month, eurozone officials are concerned that inflationary pressures are no longer confined solely to the energy sector. Even if the United States and Iran were to reach a peace agreement soon, damage to energy infrastructure in the region implies that restoring production capacity will take time, meaning inflation may not ease readily.

Latest eurozone inflation data has already risen to 3.2%, with upward inflationary pressures continuing to intensify. Core inflation—excluding volatile food and energy components—has also increased substantially. Corporate pricing plans and households’ longer-term inflation expectations are likewise trending higher. Numerous policymakers have previously stressed that the central bank can no longer ignore the current energy-driven inflation shock and must safeguard market confidence in its commitment to the 2% inflation target.

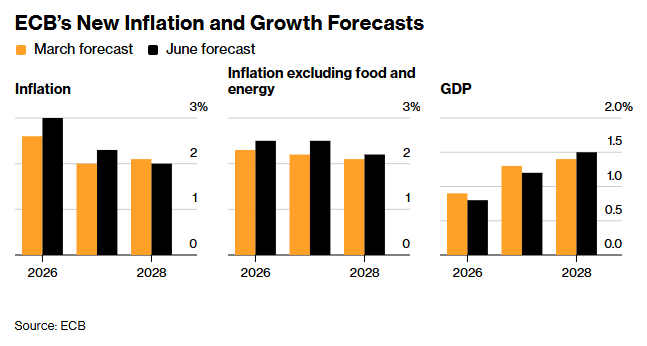

These concerns about the inflation outlook are reflected in the ECB’s latest quarterly economic projections. The new forecasts show that eurozone inflation will reach 3.0% in 2026, up from the March projection of 2.6%; the inflation rate is then expected to decline to 2.3% in 2027 (above the March forecast of 2.0%) before returning to the 2% target in 2028. The projections also indicate that core inflation—excluding food and energy—will reach 2.5% in 2026 (up from the March forecast of 2.3%), remain unchanged at that level in 2027, and fall back to 2.2% in 2028.

Meanwhile, the forecasts revised down growth expectations for the eurozone for both this year and next. The ECB now projects eurozone GDP growth of 0.8% in 2026, down from the March forecast of 0.9%, and 1.2% in 2027, below the March projection of 1.3%.

These updated projections underscore the ECB’s difficult balancing act—facing persistently elevated inflation alongside a continuously weakening economic growth outlook.

ECB President Lagarde will hold a press conference later today to elaborate further on the central bank’s stance. Additional details on the projections and scenario analyses will also be released later in the day.

Notably, the ECB was close to acting as early as April, and even some of its most dovish policymakers had signaled ahead of this week’s meeting that they now effectively had no alternative. They vividly recall the experience of 2022, when the outbreak of the Russia-Ukraine conflict triggered record-high inflation, and the ECB faced criticism for its delayed response. During that cycle, the deposit facility rate eventually rose to 4%, after which the ECB began cutting rates starting in mid-2024.

This time, ECB officials are maintaining heightened vigilance over inflation expectations, which have already risen significantly. Some worry that damage to energy infrastructure in the Gulf region and escalating global supply chain disruptions could further exacerbate inflationary conditions.

In contrast, central banks of other Group of Seven (G7) member countries are in no rush to act. The Bank of Canada held rates steady on Wednesday. Next week, the Federal Reserve and the Bank of England are also expected to stand pat, while the Bank of Japan is anticipated to continue its gradual monetary tightening cycle that began last year.

A repeat of the 2011 rate hike disaster?

Markets had widely anticipated action from the European Central Bank (ECB) even before it announced its policy decision today. Officials appear convinced that raising interest rates is now necessary to prevent surging energy prices from triggering broader inflationary pressures.

However, some economists have warned that the ECB’s determination to defend its anti-inflation credibility could lead it to make a costly mistake. They argue that there remain strong reasons for the ECB to stay on the sidelines and proceed cautiously—the eurozone economy is faltering, and market participants are highly prone to interpreting a single rate hike as the start of a new, sustained tightening cycle.

Precedents loom large. In July 2008, the ECB chose to raise rates, only for Lehman Brothers to collapse shortly thereafter, forcing the central bank into an emergency rate cut within months. Yet many economists draw closer parallels with 2011—when then-President Jean-Claude Trichet raised borrowing costs twice, only for his successor Mario Draghi to reverse course with a rate cut by year-end. Policymakers at the time were similarly concerned about soaring commodity and energy prices but underestimated the fragility of the eurozone’s financial system, ultimately plunging the region into a double-dip recession.

“The ECB is obsessed with proving its policy credibility,” said Davide Oneglia, economist at TS Lombard. “The 2011 rate hikes were a clear policy error. Today, the ECB is overly focused on inflation expectations and trapped in the psychological shadow of the high inflation seen in 2022—making a repeat of that mistake one of the biggest risks right now.”

Although inflation indicators in the eurozone have risen, some analysts argue that the increase in core inflation is not entirely driven by energy cost pass-through. Others note that key underlying price measures, such as wage growth, have yet to show signs of excessive acceleration. Michala Marcussen, Chief Economist at Societe Generale Group, stated: “If the ECB raises rates before there is clear evidence of second-round inflation effects, it will risk unnecessary tightening—that would be taking a gamble.”

Holger Schmieding, Chief Economist at Berenberg Bank, believes that an ECB rate hike would only needlessly burden households and businesses, as weak economic conditions themselves will gradually alleviate inflationary pressures. He stated bluntly: “There is absolutely no need for the central bank to raise rates while households are already under strain. With domestic demand persistently weak, this temporary surge in prices is unlikely to evolve into a persistent inflationary crisis requiring rate hikes.”

Nevertheless, another camp supports a rate hike, arguing that even if weaker economic data later forces a policy reversal, the initial hike would still be justified. Catherine Nies, Chief European Economist at PGIM, noted that policymakers would retain ample room to maneuver: “This would allow them to signal potential rate cuts promptly should economic fundamentals deteriorate significantly and business sentiment indicators continue to weaken.”

Editor/Deng