Small- and mid-cap stocks and technology shares led the gains, with the Nasdaq 100 Index closing up approximately 3.5% on the day, marking its best single-day performance in over a year. In the U.S. Treasury market, the 10-year yield fell by 10 basis points to 4.45%, while the 7-year note outperformed, with its yield dropping by 12 basis points. International crude oil futures plunged, with Brent crude falling below $89.50, down 3.9% for the day, and West Texas Intermediate (WTI) crude dropping below $86.60, down nearly 3.9% on the day.

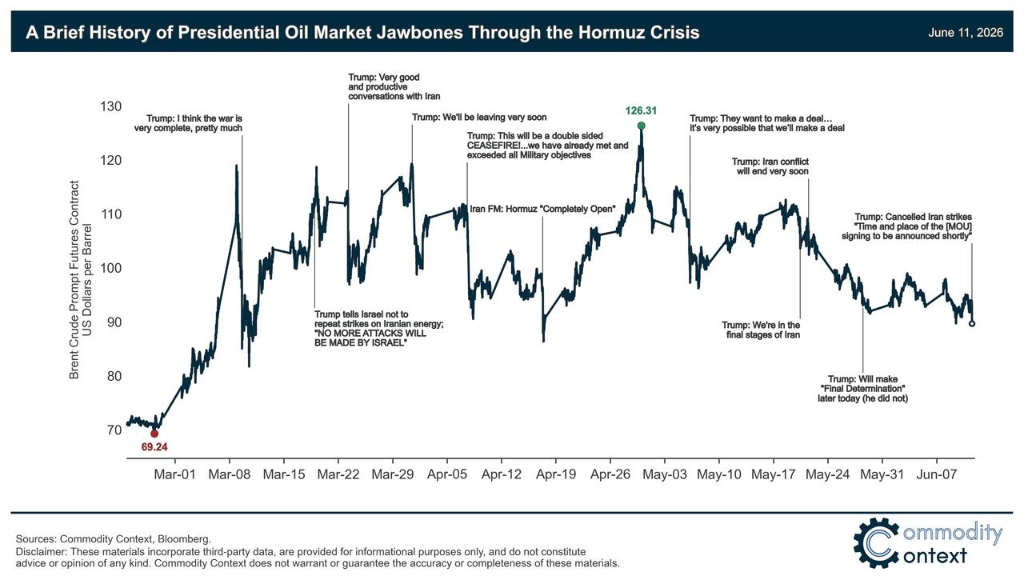

Trump signaled that the U.S. and Iran are close to reaching a peace agreement, sending crude oil prices sharply lower and easing inflation concerns, which fueled a significant rally in U.S. Treasury prices.

Meanwhile, SpaceX’s record-breaking IPO further boosted risk appetite, driving strong intraday rebounds in U.S. equities, cryptocurrencies, and gold.

During early U.S. trading hours, markets remained under the shadow of Trump’s earlier threat of military action against Iran, with oil prices staying elevated and major U.S. equity indices trading sideways.

During early U.S. trading hours, markets remained under the shadow of Trump’s earlier threat of military action against Iran, with oil prices staying elevated and major U.S. equity indices trading sideways.

During midday U.S. trading, according to China Central Television (CCTV), Trump posted on social media that negotiations with Iran had been submitted to Iran’s Supreme Leader and approved, and as U.S. President, he had canceled the planned strikes and bombing operations against Iran scheduled for that evening Eastern Time.

Financial markets reacted swiftly. All three major U.S. equity indices surged during the session, each rising more than 1%. International crude oil futures plunged, with Brent crude falling below $89.50—down 3.9% on the day—and WTI crude dropping below $86.60, down nearly 3.9% intraday.

During U.S. market hours, after posting the announcement canceling the strike plan, Trump, at an event held at the White House, touted a potential “major agreement” that could resolve the U.S.-Iran conflict and hinted that the deal might be signed as early as this weekend. U.S. equity gains subsequently widened, with all three major indices hitting new intraday highs.

In late U.S. trading, the Dow Jones Industrial Average rose by more than 1,000 points, gaining over 2%; the S&P 500 briefly climbed 2%; and the Nasdaq Composite advanced more than 2%.

Notably, both Israel and Iran denied that a deal was imminent. Iran’s official Fars News Agency reported, “Iran has not approved any agreement text with the United States.”

Zach Griffiths, Head of Macro Strategy at CreditSights, noted:

“I’m somewhat surprised by how strongly markets have rallied, given that this standoff has been going on for quite some time and substantive progress remains limited.”

According to statistics, this marks Trump's 38th announcement that a peace agreement is imminent.

Equities and bonds both rallied, with market sentiment fully recovering.

The decline in oil prices directly dampened inflation expectations, driving a sharp drop in bond yields and fueling a broad-based rally in equities.

In the U.S. Treasury market, the 10-year yield fell by 10 basis points in a single day to 4.45%, while the 7-year note outperformed, with its yield dropping by 12 basis points.

Market-implied probability of a rate hike by 2026 declined from over 100% to approximately 60%. The bond rally was strong enough to absorb the impact of that day’s weak 30-year Treasury auction and higher-than-expected PPI data.

Tony Farren, Managing Director and Head of Rates Sales Trading at Mischler Financial Group, noted:

Excluding the energy price shock, core inflation rose less than expected, which has—at least temporarily—shifted sentiment in the Treasury market.

In U.S. equities, small- and mid-cap stocks and technology shares led gains, with the Nasdaq 100 Index closing up approximately 3.5% on the day, marking its best single-day performance in over a year.

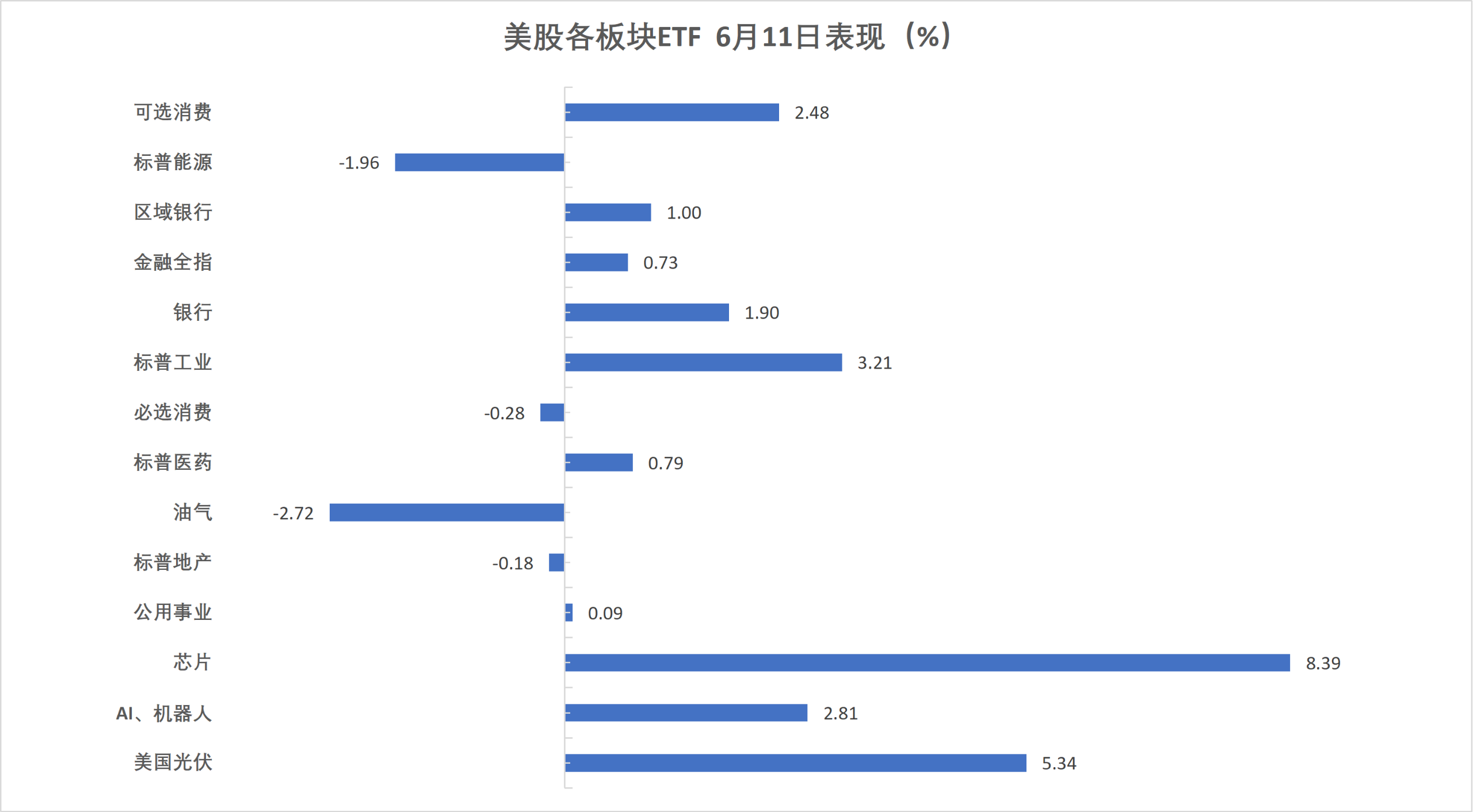

The semiconductor sector rebounded sharply, with its related index surging nearly 8% in a single day, while energy stocks were the only sector to close lower.

Short-covering amplified the market’s upward momentum, with the momentum factor rising nearly 8% on the day—its second-best performance since 2021.

Ulrike Hoffmann-Burchardi of UBS Chief Investment Office stated:

Although the path toward resolution may not be smooth, our base case scenario is that diplomacy ultimately prevails, allowing investors to refocus on solid economic fundamentals and robust earnings growth.

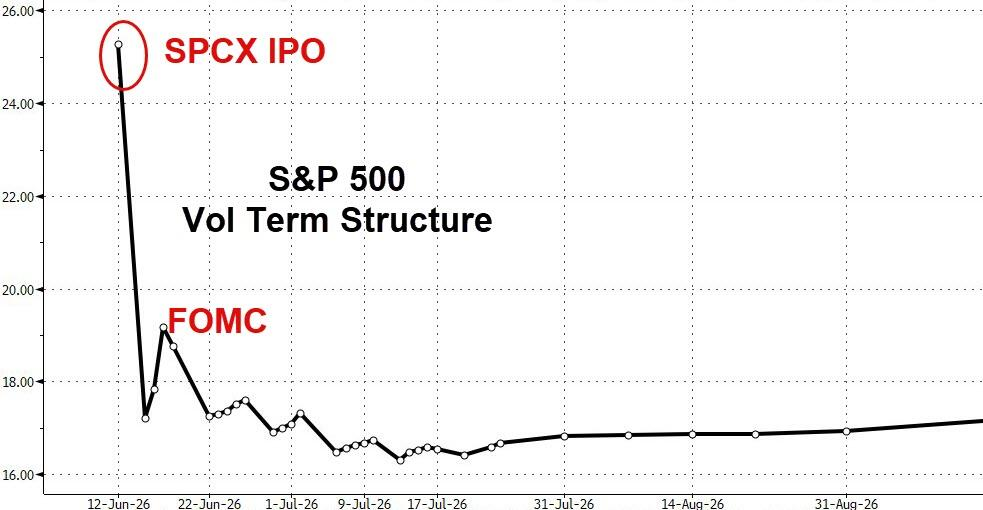

SpaceX is set to debut tomorrow, adding further fuel to an already red-hot market.

The IPO was priced at $135 per share, with 555.6 million shares offered, raising $75 billion and valuing the company at $1.77 trillion based on market capitalization. Including employee stock options and restricted stock units, the fully diluted valuation stands at approximately $1.8 trillion.

Options traders are on high alert, bracing for market volatility tomorrow.

Senior strategist Louis Navellier stated:

The IPO boom is helping to bolster investor confidence and will support a broader equity market rally. There is no doubt that we remain in a FOMO (fear of missing out) market, and the momentum of investors chasing gains is expected to persist.

The U.S. dollar plummeted due to the TACO agreement and is hovering near this week’s support low.

The weakening dollar has finally provided support for precious metals following their recent sharp decline, with gold rebounding from near $4,000 to around $4,200.

$Bitcoin (BTC.CC)$ Similarly, it rebounded, surging from $61,000 to above $63,500.

On Thursday, the three major U.S. stock indices closed higher. The Philadelphia Semiconductor Index rose 7.91%, marking its largest single-day gain since April 2025, closing at 13,171.439.

U.S. benchmark indices:

The S&P 500 Index gained 127.31 points, or 1.75%, closing at 7,394.30.

The Dow Jones Industrial Average rose 929.97 points, or 1.86%, closing at 50,848.75.

The Nasdaq Composite Index advanced 640.158 points, or 2.54%, closing at 25,809.66. The Nasdaq 100 Index gained 938.149 points, or 3.29%, closing at 29,446.176.

The Russell 2000 Index rose 3.02%, closing at 2,921.029.

The CBOE Volatility Index (VIX) declined 12.47%, closing at 19.45.

U.S. stock sector ETFs:

U.S. equity sector ETFs broadly posted gains, with the semiconductor ETF rising 6.75% and the global airline industry ETF up 6.31%. The global technology equity index ETF, technology sector ETF, biotechnology index ETF, consumer discretionary ETF, banking sector ETF, and internet stock index ETF all rose by as much as 3.73%.

Mag 7:

The Wind U.S. Mag 7 Index rose 1.14%.

$Tesla (TSLA.US)$ up 4.60%, $NVIDIA (NVDA.US)$ up 2.22%, Amazon up 1.47%, Apple up 1.39%, Google A up 0.39%, Meta down 0.45%, Microsoft down 1.77%.

Chip Stocks:

$PHLX Semiconductor Index (.SOX.US)$ closed up 7.91%, marking its largest single-day gain since April 2025, at 13,171.439 points.

Taiwan Semiconductor ADR up 3.26%, $Advanced Micro Devices (AMD.US)$ surged 7.97%, $Micron Technology (MU.US)$ 、 $Marvell Technology (MRVL.US)$ up more than 11%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed up 0.25% at 6,296.64 points, staging a strong rebound at 01:28 Beijing time—rising approximately 60 points from the 6,200 level.

Among popular Chinese concept stocks, ASE Semiconductor closed up 7.2%, $NetEase (NTES.US)$ up 0.2%, $Alibaba (BABA.US)$ down 1.5%.

Other individual stocks:

$Circle (CRCL.US)$ Up 4.74%.

Eurozone blue-chip stocks rose approximately 0.8% on the day of the European Central Bank’s rate hike, with ASML Holding, ASM International, and BE Semiconductor Industries closing at record highs. The Dutch stock market gained 1%, reaching a new closing record high on the ECB rate hike day, while Italy's benchmark index advanced more than 0.9%, and Germany’s defense ETF rose about 1.7%.

Pan-European stocks:

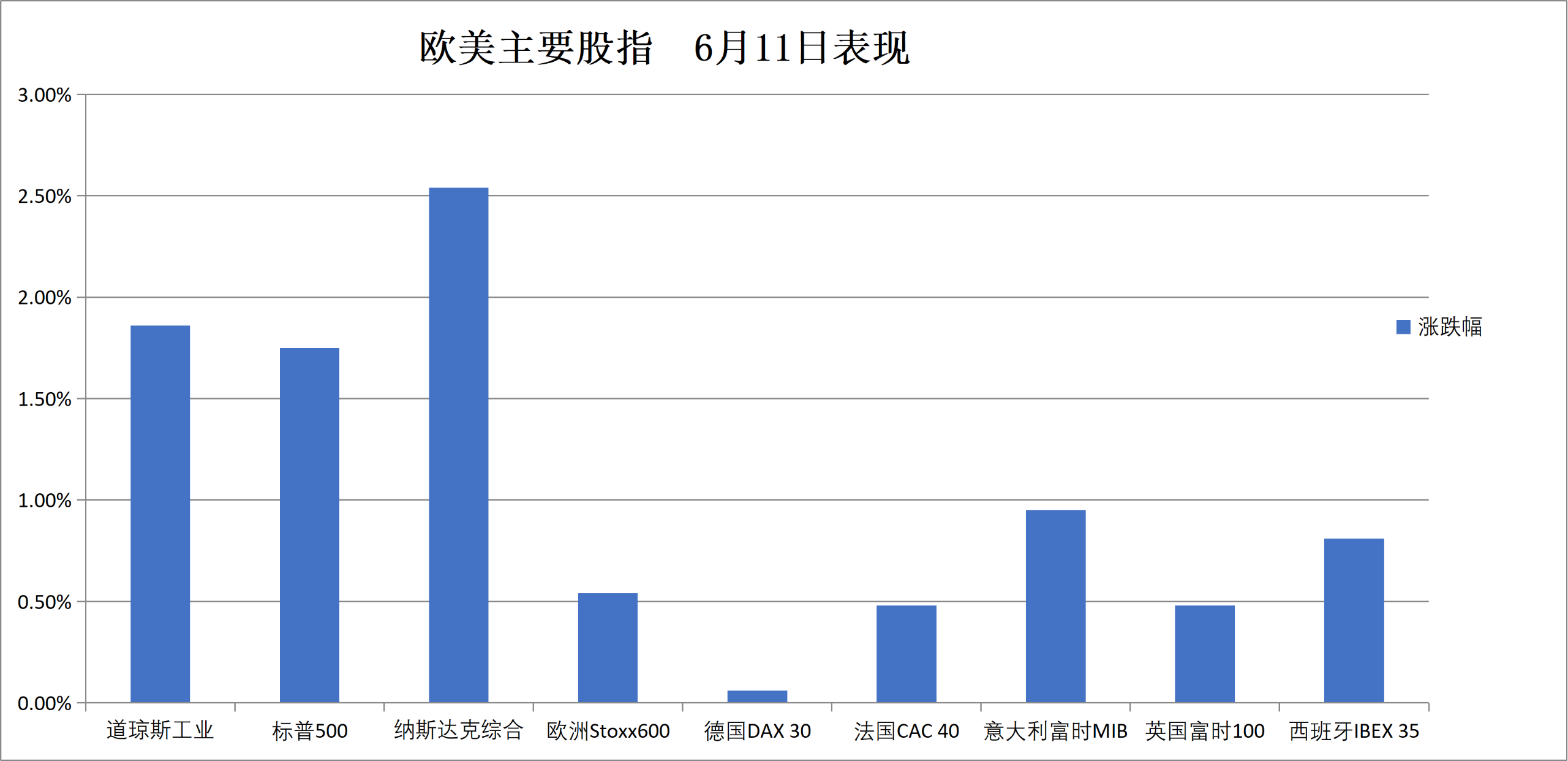

The pan-European STOXX 600 Index closed up 0.54% at 621.53 points.

The Eurozone STOXX 50 Index closed up 0.78% at 6,056.96 points.

Major Stock Indexes Around the World:

Germany's DAX 30 Index closed up 0.06% at 24,209.71 points.

France's CAC 40 Index closed up 0.48% at 8,200.80 points.

The UK's FTSE 100 Index closed up 0.48% at 10,303.88 points.

Sector and individual stock performance:

Among Eurozone blue chips, Siemens Energy rose 6%, ASML Holding gained 4.56% to close at €1,576.00, surpassing its previous record closing high of €1,514.60 set on June 8, and Infineon Technologies advanced 2.61%.

Among all constituents of the STOXX Europe 600 Index, ASM International rose 7.39% to €973.60, marking its second consecutive trading day closing at a record high. BE Semiconductor Industries gained 6.61%, also posting its second straight day of record closing highs.

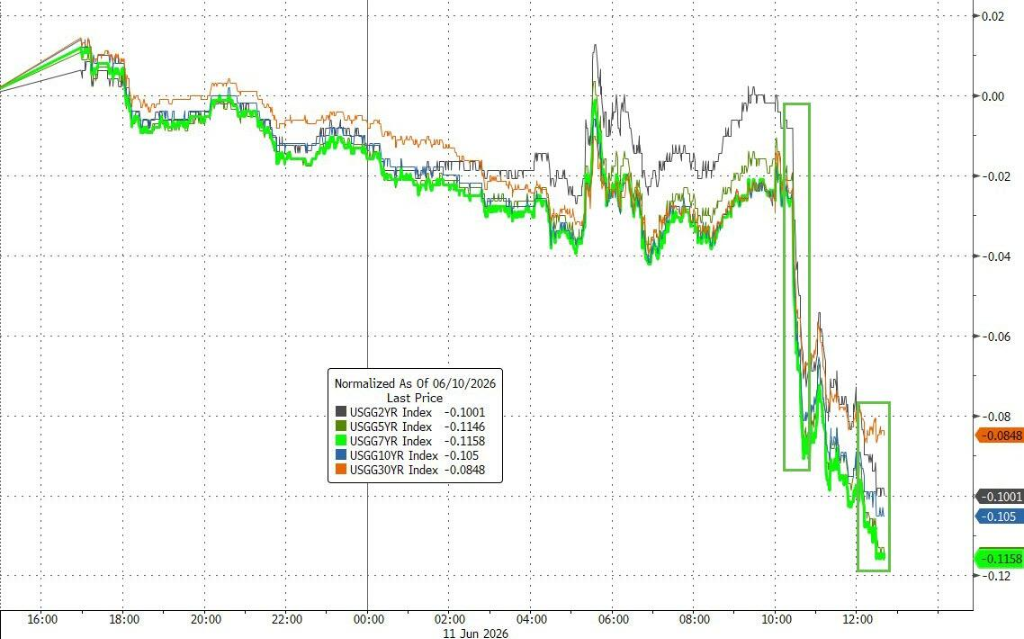

Trump announced the cancellation of strike plans against Iran, prompting a rally in U.S. Treasuries and a surge in trading volumes. German bond yields fell by at least 4 basis points, while the two-year yield rebounded after the European Central Bank’s rate hike announcement, briefly hitting a new intraday high.

U.S. Treasuries:

At the New York close, the yield on the 10-year U.S. Treasury note dropped sharply by 9.3 basis points to 4.457%.

The yield on the two-year U.S. Treasury note declined by 7.92 basis points to 4.058%.

European bonds:

At the European close, the yield on Germany's 10-year government bond fell by 4.5 basis points to 3.032%, declining steadily throughout the session and trading within a range of 3.091% to 3.021%.

The yield on the UK’s 10-year gilt declined by 2.6 basis points to 4.905%, showing a spike-and-reversal pattern following the European Central Bank’s rate hike announcement at 20:15 CET.

The 10-year government bond yields in France, Italy, Spain, and Greece fell by as much as 5.3 basis points.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Stephen